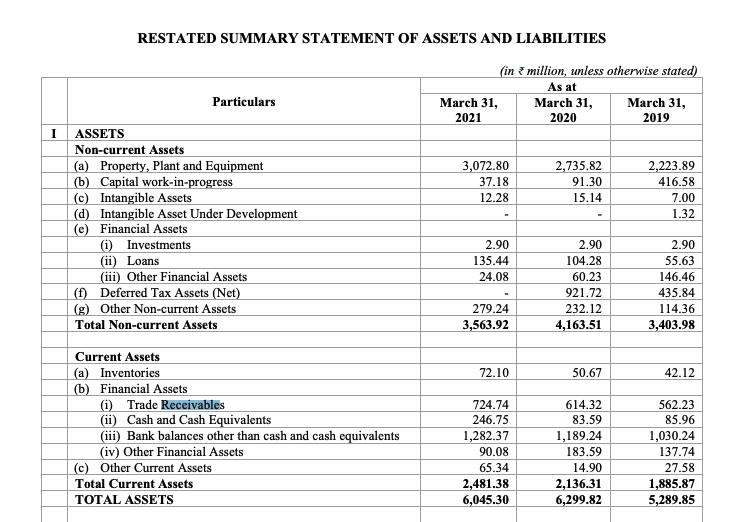

Let us analyse some more data from their DRHP this time around receivables.

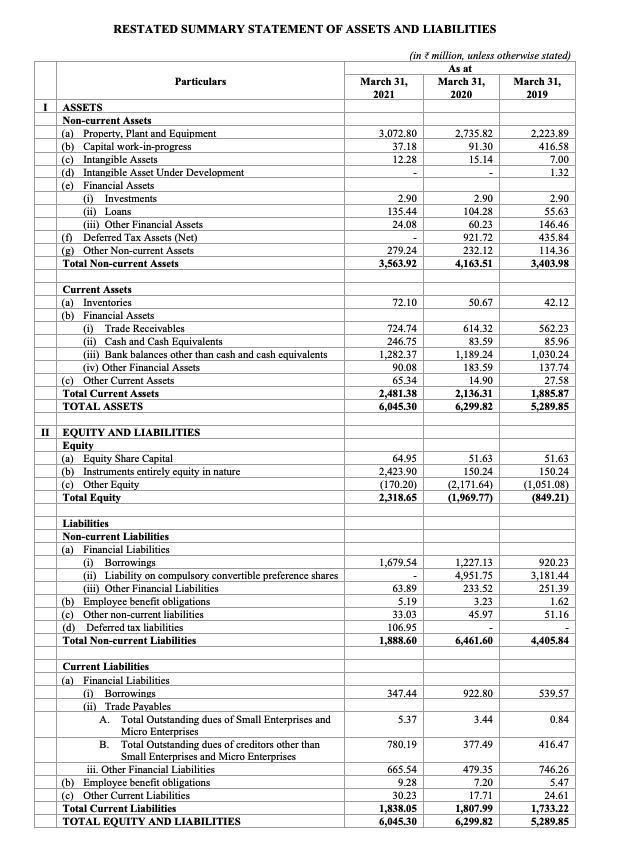

Receivables from last 3 years.

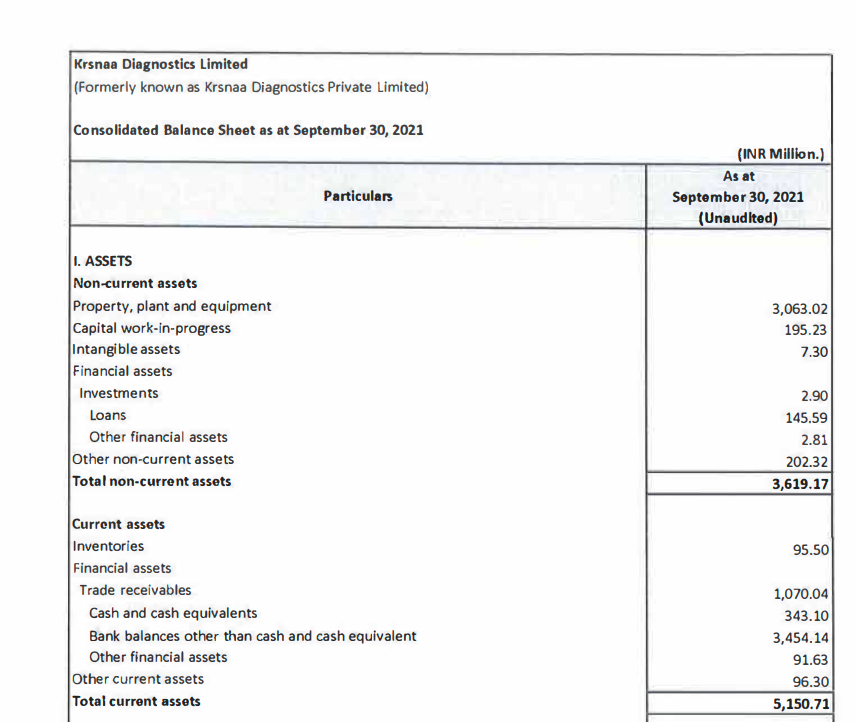

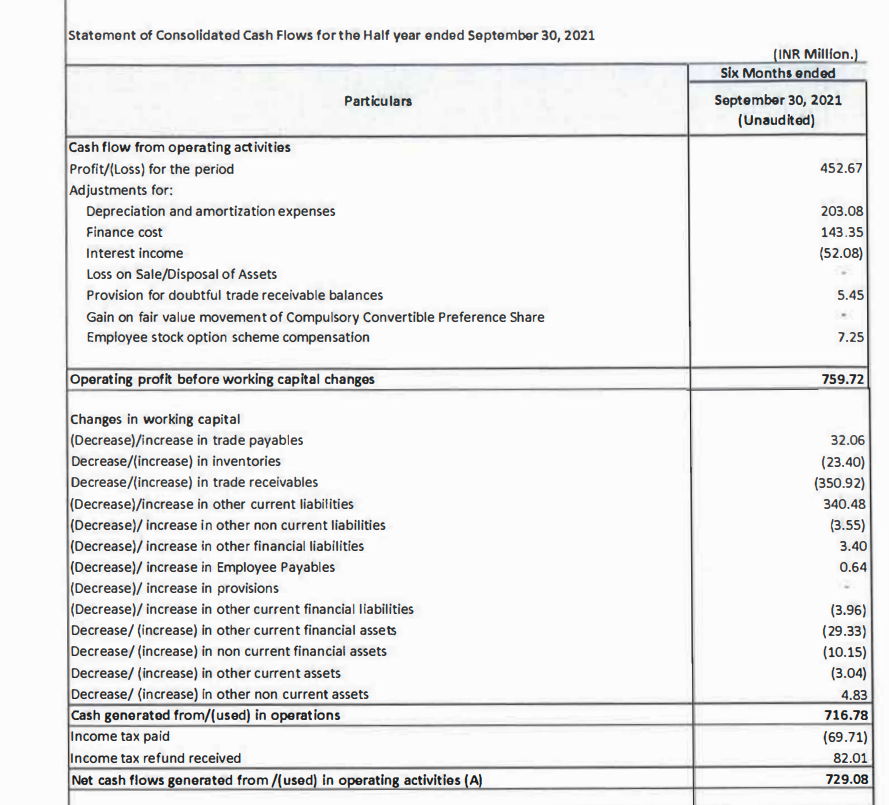

Receivables in latest Sep-21 balance sheet:

While they have handled receivables rather well between 2019 & 2021. Going from 56cr to 72 cr while revenue base scaled from 209 cr to 396 cr. Receivables as a % of scales scaled down from 26.7% in FY19 to 18% in FY21.

However, situation has deteriorated back to FY19 levels in Sep-21 Q. 107 cr receivables for TTM sales of around 450 cr. Works out to around 23.6% of sales being stuck in receivables.

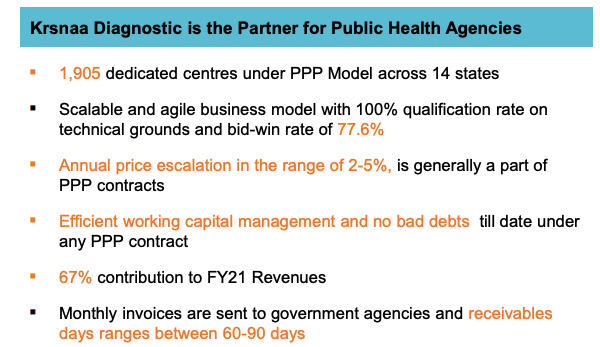

This works out to receivable days of around 86. THis is average over entire business. They claim in preso to have receivable days of 60-90 for PPP:

However, the data does not back this up. Average for entire business itself is around 86 days. private is most likely better in receivables than government. It would not be unreasonable to conclude that PPP biz receivables are > 90 days.

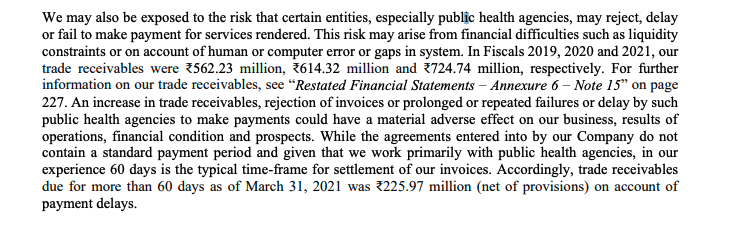

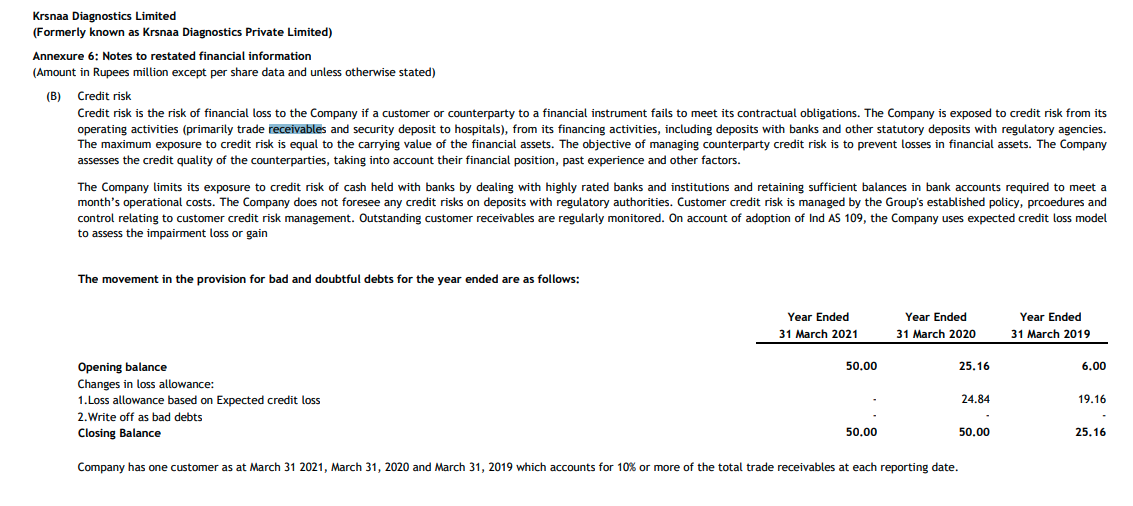

Here is another para from DRHP on risk wrt receivables:

The receivables > 60 days was around 31% of the receivables. I would be very interested in figure out same number for > 90 days & > 180 days receivables & how this deteriorated in sep-21 balance sheet & how this evolves in mar-21 balance sheet. I am surprised we did not see enough probing around receivable deterioration in Q2 Q3 concall.

One good thing is that they havent written off any receivables at least between mar-19 & mar-21. Should ask management whether they have in FY22 better know now rather than when annual report comes in Jun-22.

One interesting thing is that this deterioration of receivables HAS NOT impacted cashflows yet. Why?

Their “Other current liabilities” has also gone up by 35cr or so which has totally offset the deterioration in receivables. Note that the payables has not gone up that much (only 3 cr). So i would also want to dig deeper into this “other current liabilities”

And their “other current liabilities” have always been fairly low at around 3cr or lower earlier. For this to blow up by almost same amount as receivables going up is definitely extremely convenient (not alleging any wrong doing here, only pointing out the coincidence/facts).

If you go into the breakup of the other current liabilities in DRHP you see that these do seem to be somewhat similar to payables.

- statutory dues payables

- advances from customer

- deferred revenue

i dont think #1 would go up since revenue base has not exploded.

I dont think #2 would go up coz they are having difficulties collecting billed revenues. Advances from customers going up by 30cr is somewhat unreasonable imo.

I dont think they have deferred revenue because they recognize revenue at the time of their test. that is their revenue recognition policy. So, how did other current liabilities go up almost the right amount to compensate the deterioration in receivables? It remains a mystery to, me, but definitely worth solving.

Possible solutions:

- balance sheet/p&l/cash flow statement jugglery that i dont understand

- Advances from punjab government contracts. Is that how these tenders work? I dont think so

- Some new line item coming in other current liabilities which I have not anticipated.

Definitely will ask in next concall if we cant figure out before then.

Disc: Have a small position, understanding the company.