Business Details:

-

About the company: It started in 1997 as an engineering company, manufacturing equipment for the milk and dairy industry and around 2006-07, it got an opportunity to work on a product called the Bulb Bar for naval ships for defence.

-

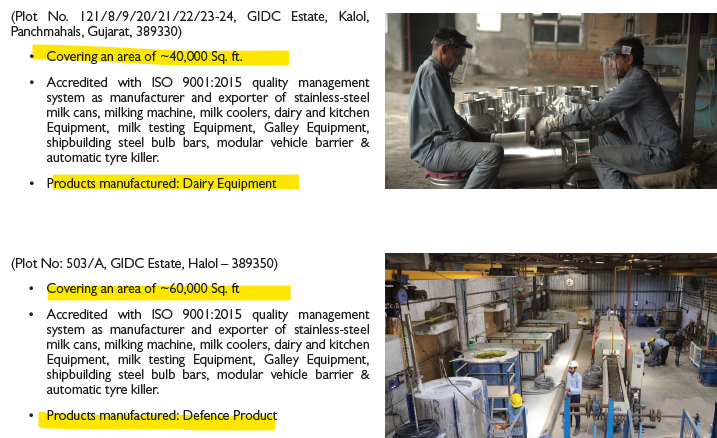

Manufacturing plants:

-

Product:

-

One of the prime products is steel bulb bars. Steel bulb bars are profiles, that are used as stiffeners for the hull construction of warships, and naval ships. These are used for the frame members to support the main structure.

The key feature of the bulb bar is that the strength-to-weight ratio is about 3 times, because of its unique shape. Because of the strength-to-weight ratio being 3 times, one can reduce the weight of the final ship, which means that one can take in more ammunition, be more personal, & most importantly reduce the weight.

-

special steel, ballast bricks, which are used for naval critical platforms. These are used for balancing. The key feature of this particular product is the magnetic permeability of this is near zero, making it very, very difficult to detect on any radar or something.

-

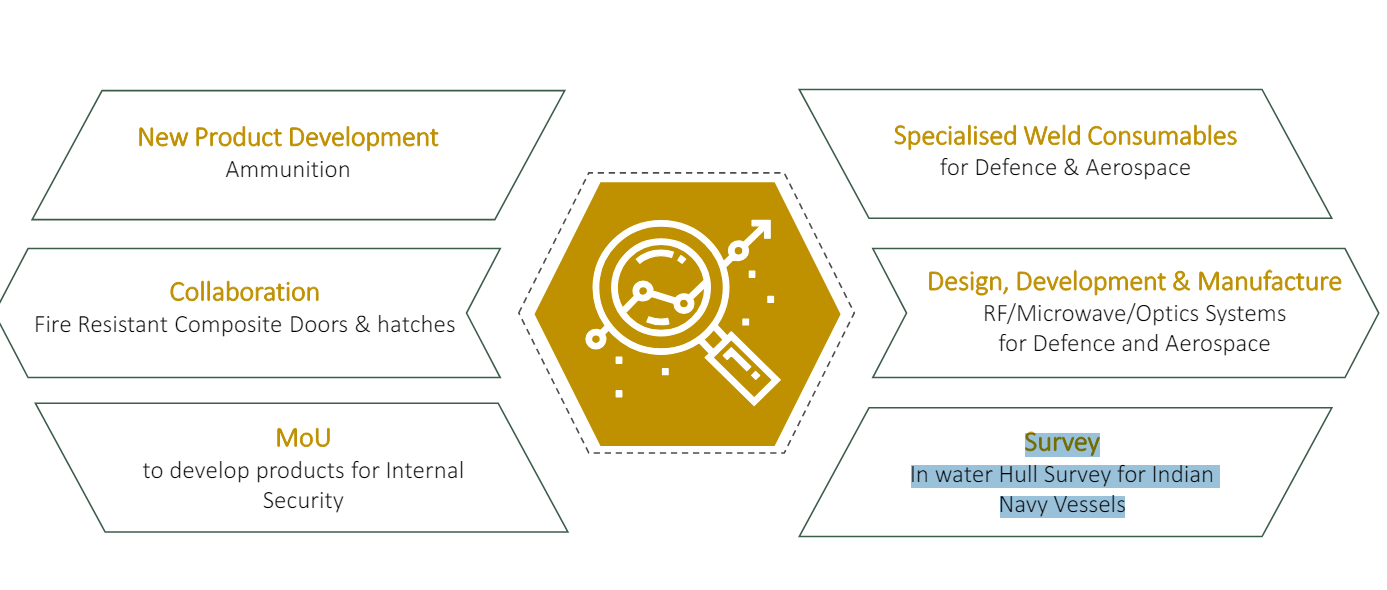

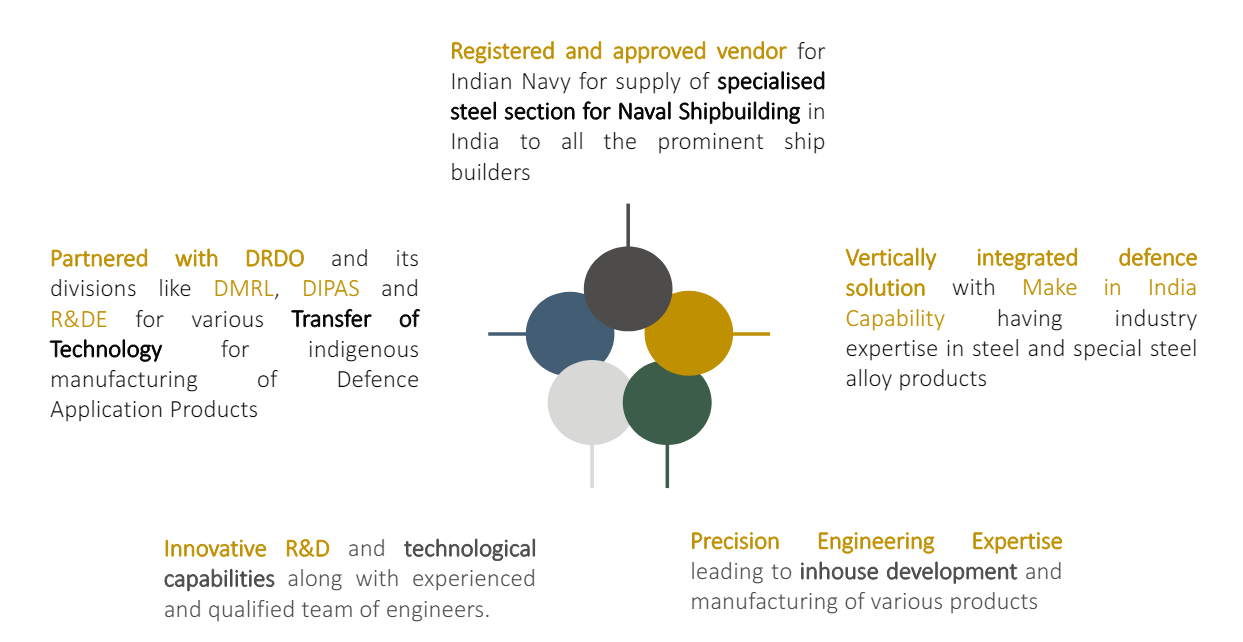

Heavy Vehicle Factory Steel Profile: These are special profiles which are used for the manufacture of the T-90 tanks by one of the ordnance factories. And before our development, these were all being imported from Russia. We’ve successfully been able to indigenize and execute for the same.

-

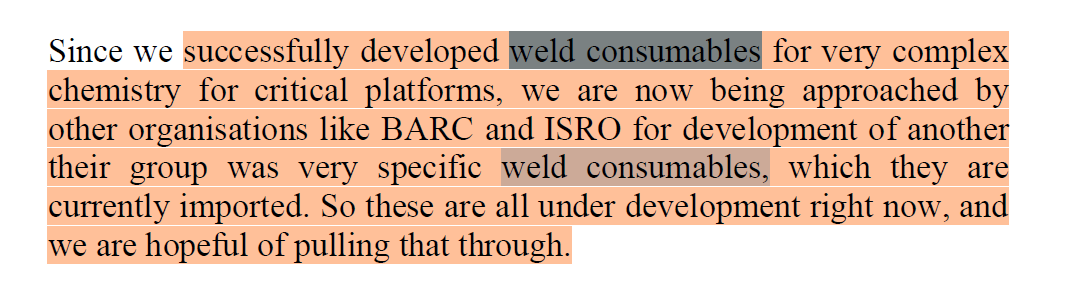

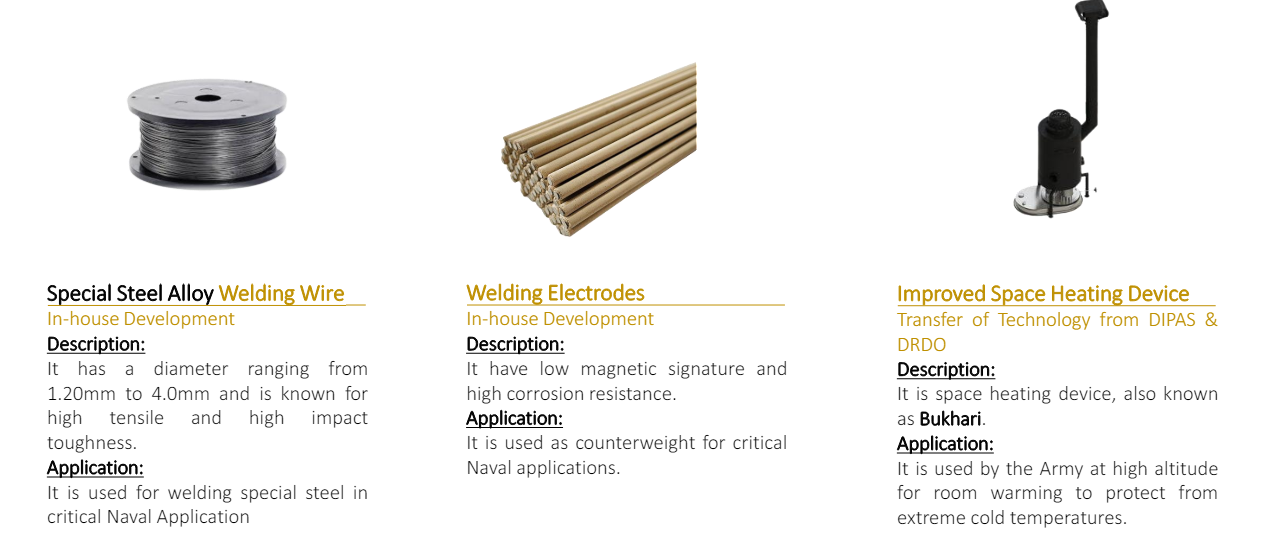

Welding wire and the welding electrodes: These are again complex chemistries containing special metals like nickel, titanium, nitrogen, and so on. These are used for very high tensile environments used for welding plates which are used for critical platforms, again, of the navy. This also was a product that was being imported from Russia, which we’ve successfully been able to indigenize and are supplying the same as of now.

-

‘Bukhari’: It’s a room heating device and it has developed this product in joint development with DIPAS, the DRDO lab, which is the Defence Institute of Physiology & Allied Sciences. So, they developed products for high altitude, which are to be used by our army men at minus 20 in Ladakh, Siachen, and so on.

-

Diary business products:

-

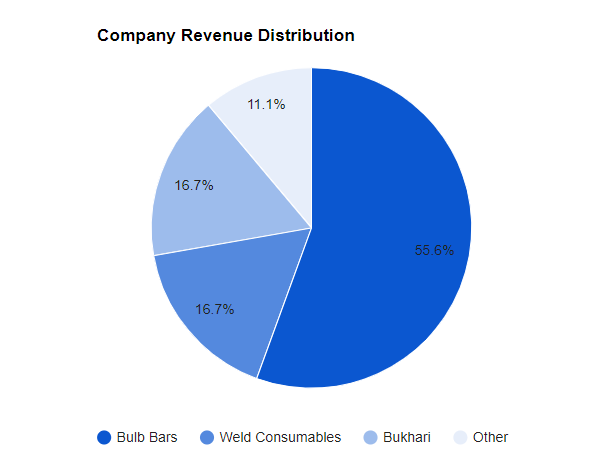

Product breakup for Fy25:

-

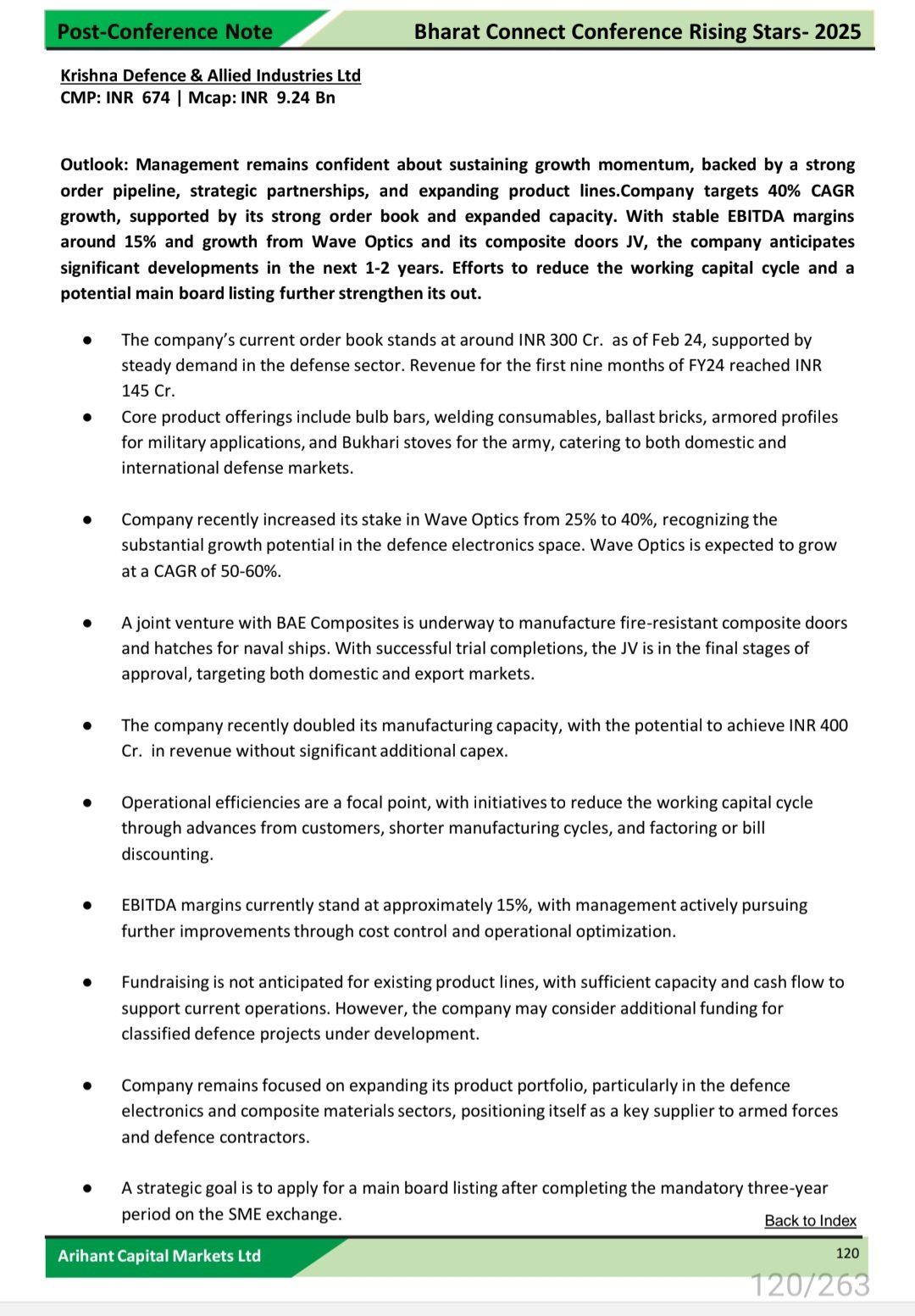

Orders: It stands above 230 cr having bulk of orders for Bulb bars & expects additional orders in this financial year.

-

Bukhari product: It has bagged an order about close to ₹64 crores.

-

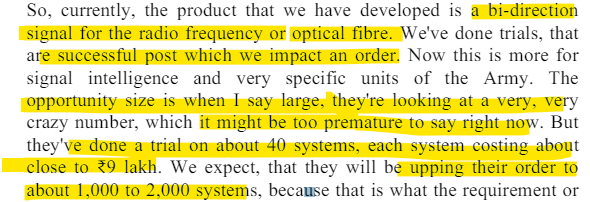

Specialized converters for radio frequency to optical Fibres: It has got the order from L&T for about close to 3 crores for the supply of the same

-

In-Development: trying to work on a particular ammunition called the Super Rapid Gun Mount, which is again used for a naval gun. This is a work in progress, things are moving, but slightly at a slower pace because it is still a design stage for us.

-

Clients:

-

No royalty to DRDO or BARC for supplying to Indian defence forces:

-

Order delivery Timeline: It varies from order to order. Some orders have been done in about six months. Some orders may be 18 months or 24 months also.

-

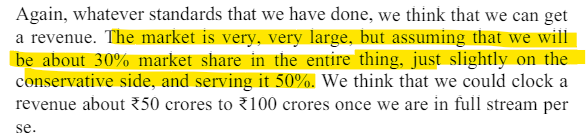

Capacity: With current capacity, it can do about close to 180-200 cr in terms of revenue. With brownfield expansion, it can be able to up to about 350-400 crores in terms of revenue.

-

Bulb bars: It can do 2,000 tons to 2,500 tons annually with our existing capacity and with the capacity expansion, we should be able to achieve several close to 4,000 tons.

-

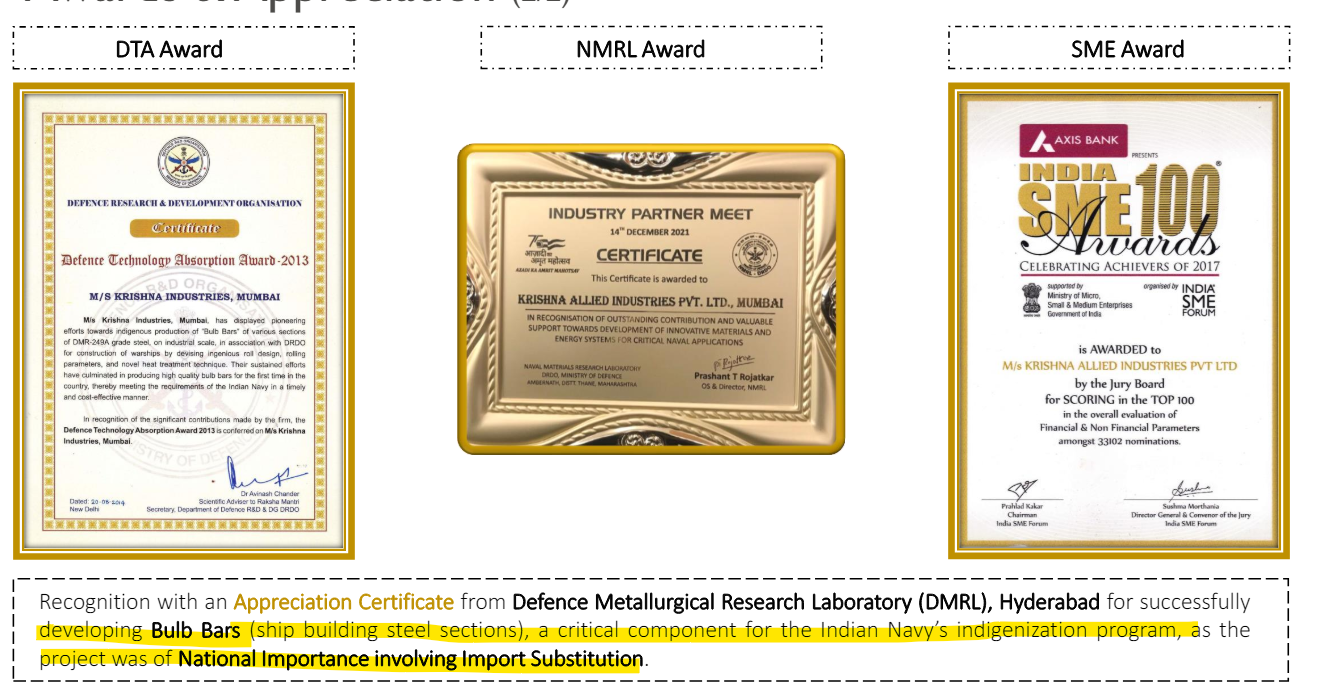

Awards :

Growth:

-

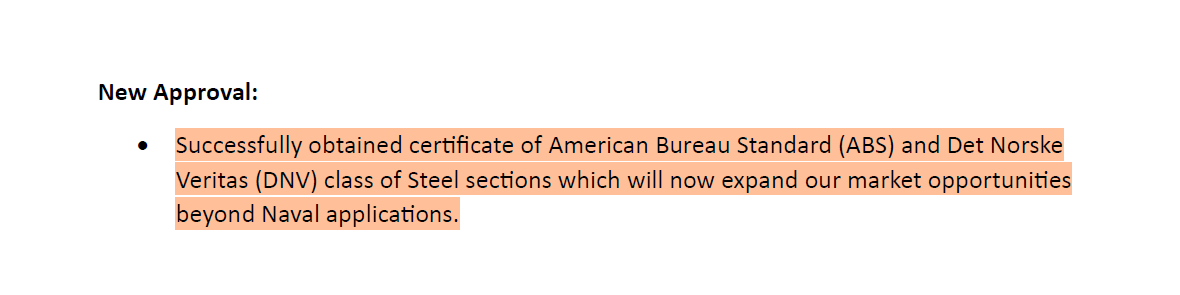

It has got approval for the bulb bars for supply to post guard vessels that are there & also bagged an order related to that.

-

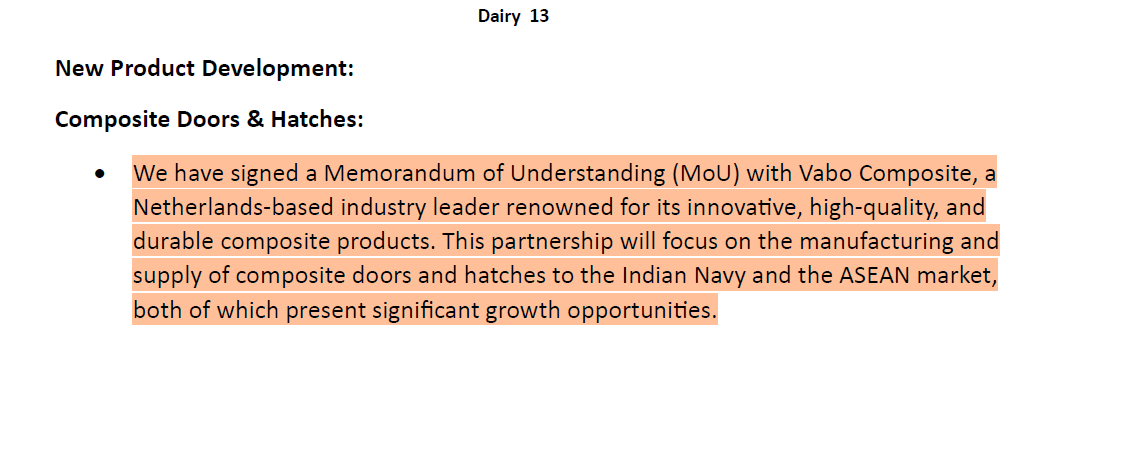

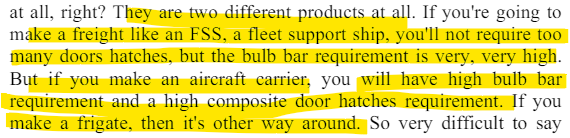

Manufacture of fire-resistant composite doors & hatches replacing existing steel doors and hatches in all naval ships. They have tied up with the Netherlands company & if we want to start to manufacture the same in collaboration with them as a joint venture, plans to replace all the hatches due to the corrosion & the heaviness properties of composite doors are much lighter, again, adding to a feature where you can reduce the weight of the ship.

-

They have an MoU with IIT Bombay, & developing a product for the army for combat, which is a spherical robot. We’ve done the prototype and, again and field trial to take through.

-

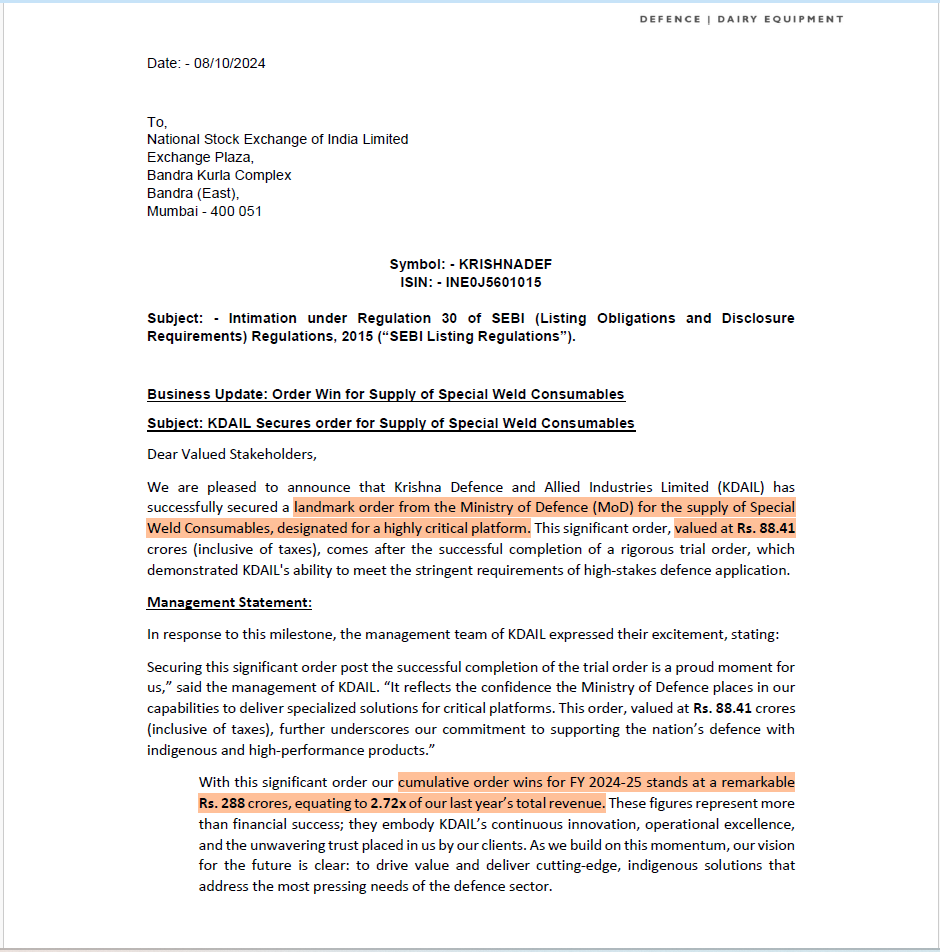

It has been approached by other wings of the defence forces for developing specialized well-consumables, which currently they are importing.

-

Started a new company in Bangalore to work on making specialized converters, which convert radio frequency to optical fibre and optical fibre to radio frequency. This would open up the company’s diversional fact to get the defence electronics front.

-

It has tied up with other company out of IIT Madras, which has developed an underwater ROV. So, they’ve synchronized with them to be able to use this product for the naval application as a service job to be able to do the hull thickness measurement, hull thickness and cleaning of the marine growth that happens on ships once they are at sea. This helps in reducing the dry dock time and increases the time that the ship can be at sea.

-

Growth guidance: Revised target from 30% to 35% to 40% yoy for the next three years.

-

EBITDA margin: It aspires to have a 20% margin against 15% as of now.

TAM:

- Opportunity size in Wave Optix:

- Shipbuilding is 5-6 years cycle:

- Huge demand for bulb bars in FSS and aircraft carriers:

- Composite doors and hatches Market Size:

- Ships required over the next 5 years is 40:

- Make in India initiative is boosting indigenisation of defense products:

- Government policies &Inititives:

- Defense Budget Outlook:

Strategic Intent:

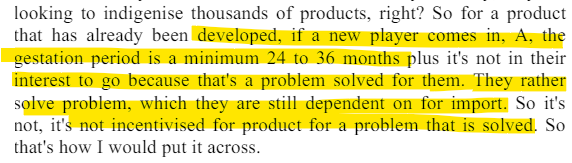

- Import Substitution: Earlier bulb bars were imported by the country by it has successfully developed the product and supplied these bulb bars to all the leading shipyards in the country i.e. Mazagon Dock, GRSE, HSL, L&T, Goa Shipyard, so on and so forth and other is welding wire and the welding electrodes.

- Increase stake in WAVEOPTIX from 25% to 51% as the opportunity is huge.

- On the composite doors and hatches, We expect to finalise on the JV with our foreign partner with stake around 51%.

Competitive Advantages and Intensity:

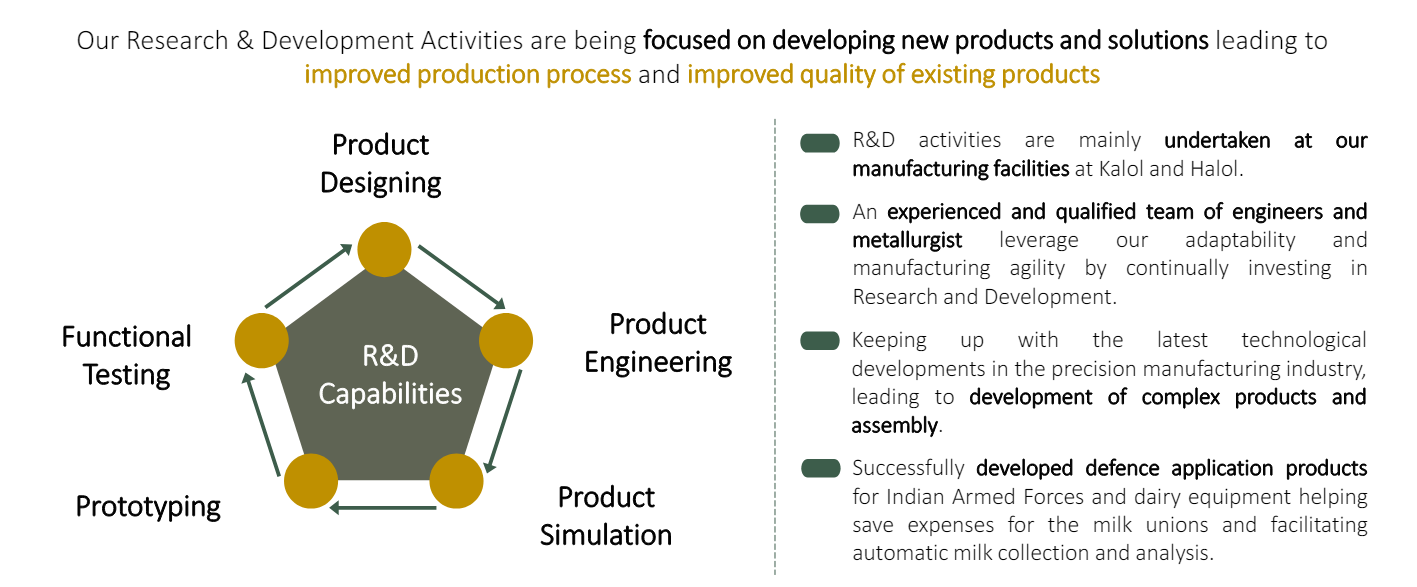

- In-house R&D capabilities: It has an in-house research team. They also have a NABL-approved lab also, which plays a big role in developing homegrown defence solutions that replace imported products. So, we’ve been a company, we’ve been trying to focus on imported products that could be indigenized and used by the services, all three services per se.

- Our manufacturing capability includes a wide range of critical assemblies and precision components with close tolerances made possible through in-depth know-how on metallurgy, precision machining, assembly, and specialized fabrication facilities with a series of multi-level inspections during the production process.

3. Huge Entry barrier:

Financials:

- EBITDA margin has increased to 14.51% in FY’24 vs 13.91% in FY’23.

- PAT surged by 84.86% to ₹97.90 million in FY’24 vs 52.96 million.

- total revenue of the company stood at ₹1,064.28 million in FY’24 against ₹636.53 million in FY’23 thereby showing a growth of 67.20%

- Fund Raise: The fundraise to 15 to 20 crores towards CapEx, and the remaining about ₹35 crores to ₹40 crores towards working capital because of the order flow.

RISK:

- Raw materials mostly consist of steel and any price esclation can have impact to the bottomline and steel prices have to be monitored as it has been increasing.

- Shipbuilding is hugely dependent on government policies and any government stability or change can impact the policies and sector.

- Company execution capabilities needs to be monitored as that can be potential risk to the company’s growth.

- Working capital management is a major hindrance in SME companies, as the company is trying to bring it down to below 100 days.

- Major clients are government companies and can lead to payment getting delayed.

- Sector as a whole has given huge runup, needs to evaluate on future growth as any slowdown can derate the sector.

Disclaimer- invested, biased, DYODD.