Transcript of Q3 FY24 earnings conference call released by the Company

https://nsearchives.nseindia.com/corporate/KRISHCA_10022024094248_Q3EarningsCallTranscriptFeb0724.pdf

Hey guys just an update. While the company in its press release today has declared the successful commissioning of its new strapping line (on 14 May), in its last concall it declared that the line would be operational by Feb end. Guess there has been some delay in its execution.

Disclosure: Not invested but tracking.

6 Likes

FY24 Result released by the company

https://nsearchives.nseindia.com/corporate/KSSLQUICKRESULTS27052024_27052024210315.pdf

Revenue up by 45%

PAT up by 42%

PAT Margin is 12.6%

6 Likes

Hi,

I have been studying Krishca for sometime now. Here are 3 major questions and some data in order to try and understand the business better. Please feel free to chime in with your inputs and feedback. Also, any other example of a small ancillary in an oligopolistic setup dependent on a big commodity industry will help

Q1. How will the business perform in a cyclical downturn?

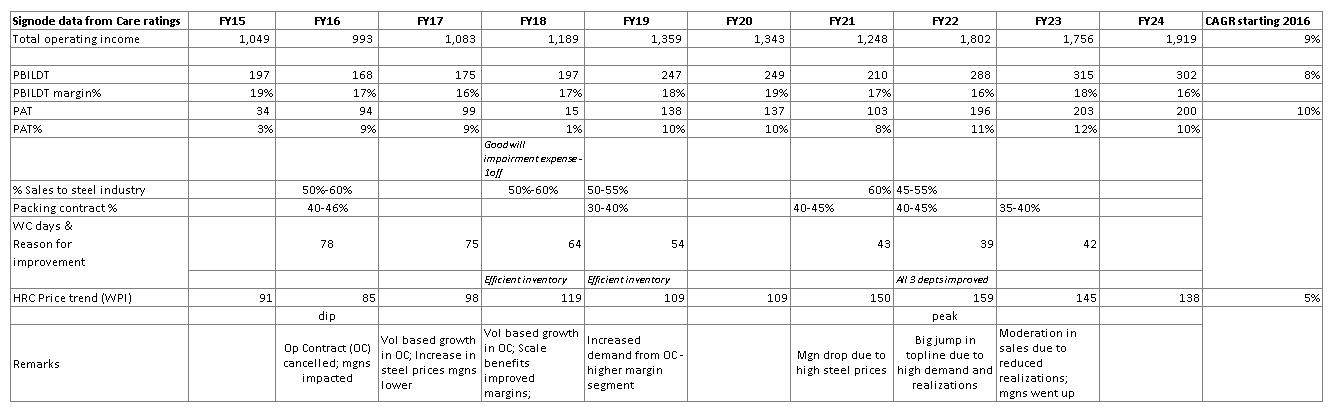

Quick Answer → Signode India (biggest competitor) has shown consistent growth (9% CAGR) and more or less steady margins (16-19% PBILDT) over last 10 years. Thus, the business or industry seems only mildly cyclical based on this limited dataset

Details → I collated Signode India financials from care ratings report - available publicly - you can go to screener premium and find them under Tools → “credit rating reports”

Key observations:

-

FY16 was a cyclical dip for steel industry based on bottoming out of steel prices. Even that year, Signode did 17% PBILDT margins. Topline suffered a bit due to OC (operations contract) getting cancelled but impact was a mere 5% over FY15

-

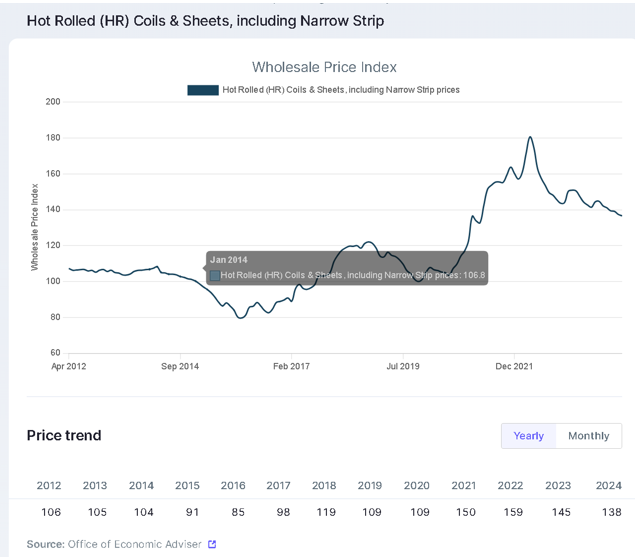

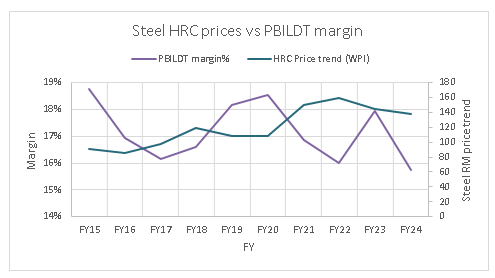

Over the course of last 10 years, Signode’s operating margins have been in 16-19% range. There is weak negative correlation of (-0.35) between steel prices and their PBILDT margins

-

Topline growth CAGR has been around 9% in last 10 years

-

Roughly 50-60% of sales is to steel industry and Packing contract (or OC) contribution to revenue has been roughly 35-45%

-

Working capital days have come down from 78 to 42 over last 10 years due to efficient inventory management

Q2. Does the business have any bargaining/pricing power?

Here is a snippet from one of the Signode India’s care ratings report:

Over the past few decades, industry structure has changed from a monopoly to an oligopolistic setup. Krishca promoter has mentioned in past that big steel players such as Tata, JSW, SAIL were desperately looking for new vendors to de-risk the supply.

Will the bargaining power hold? → looking for inputs

Going by theory of “Kinked demand curve under oligopolies”, prices are quite sticky since you want to deter a price war on one hand but also not increase price unilaterally since competitors will not follow. Comes down to relationship, product differentiation etc…

Q3. Is the opportunity size big enough?

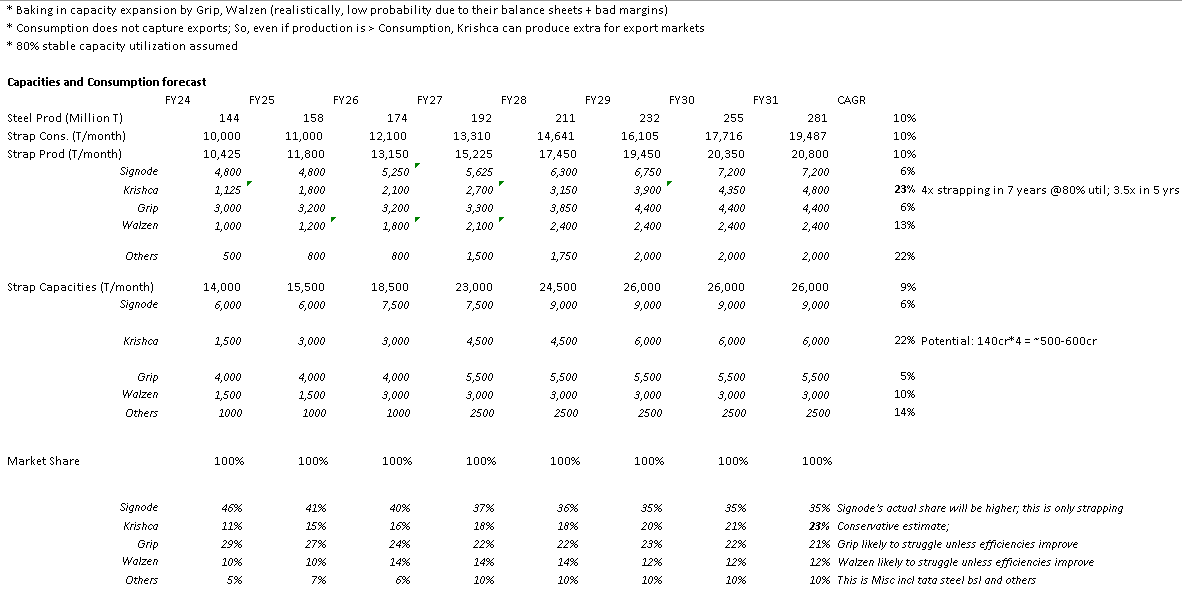

Quick answer → they can grow their domestic capacities and production by ~22% for next 6-7 years provided steel capacities meet their target growth & given, we don’t see import of cheap steel straps

This has been the most troubling question since the promoter mentioned in concall that Indian strapping market is only ~3000cr including packing contracts. Dubai market is another 300-400cr directly (without adding the potential to supply to Americas and Europe).

He has also mentioned that the company will organically grow into primary packaging. With no estimates and details on the size of this primary packaging market, competition intensity, margins etc., I tried to only focus on domestic strapping market and project the capacities and consumption based on steel industry growth assumptions. This could be an incorrect approach since steel industry projections are unreliable and should be taken with a pinch of iodized salt ![]()

Key Observations:

-

Base assumption - Steel production reaches ~250-300MTPA by 2030; Strap consumption mimics steel production that assumes no imports of strapping

-

Even if Signode grows its capacity by 1.5x in next 7 years & Grip, Walzen also put up 1 additional 1500T/month plant → Krishca will have space to 2x its current capacity base from 3000T/month (2 plants) to 6000T/month. This is conservative and not counting in the space for middle east expansion. A 4x capacity (since 2nd plant got commissioned recently in May; capacity till FY24 was 1500T/month that can expand 4x to 6000T/month) for steel strapping in 7 years would mean roughly 140cr*4 = 500-600cr of revenue potential just from steel strapping (22-23% CAGR)

-

Signode India has been paying heavy dividends back to its parent MNC. Not sure if this means they are not interested in heavy reinvestments in India and treating this subsidiary more like a cash cow for now; This presents an opportunity for Krishca to steal more market share through capacity expansions & getting to 20-25% market share in ~7 years

-

Grip seem to have a stretched balance sheet based on ratings report by acuity dated july 5, 2023 → this makes them unlikely to expand aggressively in future (assumption)

This is more of an excel spreadsheet based analysis. I will request fellow members who are tracking the industry closely or understand such dynamics to feel free and provide their views. Thanks a lot

@Rakesh_Arora @DEBASHISH @jitenp

Disc - for educational purposes. Invested but re-considering position sizing

15 Likes

Anyone attended the concall?

Any notes if you can mention.

Expansion plan and Growth projections?

1 Like

I attended the call ( Krishca Concall Updates -whatsapp Fwd ):

Over 200 customers.

Major order from Vedanta Ltd worth ₹20.25 crore.

Successfully commissioned a new strapping line on 13th May 2024.

High margin product will be produced.

Current order book worth ₹28.8 crore.

Participating in 5-6 contracts, more than the Vedanta order.

New plant increases monthly capacity from 1,500 tons to 3,000 tons, with peak capacity at 2,500 tons.

Peak capacity could result in ₹300 crore in strapping sales.

Biggest competitor does not offer color strapping; the company provides custom branded straps in the southern region.

People in Raipur and Jalna are indifferent to branding.

On steel prices volatility:

Fixed and variable components; fixed comprises value addition and margins, passed on to customers.

Margin component remains consistent with a one-month lag; long-term contracts have a price variation clause.

Competition from Middle East and China:

Chinese pricing is lower; FTA with UAE provides a 5% duty benefit.

Local presence in the Middle East, offering end-to-end packing solutions.

Plant in the Middle East could source raw materials from China, Korea, or other countries.

Business depends on steel production.

Peak utilization expected within the next 4 years.

Looking for a joint venture in the Middle East; updates expected within 6 months.

Expansion focus on US markets, Sri Lanka, Bangladesh, Australia, and Europe.

Targeting large volume buyers.

FY24 exports were ₹17 crore; FY25 exports expected to double, aiming for ₹100 crore in 5 years.

Targeting a minimum of 25% pa CAGR for next 4-5 years .

Operating margin expected between 15%-20%.

Market share:

Over 10% in steel strapping.

Less than 5% in packing contracts.

Long-term goal to capture 30% of the overall market.

Delay in commissioning the new plant due to machinery supply and installation delays.

Current utilization of the new plant is less than 15%.

Sent from my iPhone

15 Likes

Notes from Q4 FY24Concall:

1. Capacity & Capex

-

Peak production capacity of 2500 Tons annually (out of 3000 T, 1500+1500) from both plants. 10 months out of 12 months (83% utilization) based calculation

-

110 million steel seals capacity - multiple types of seals - at current avg price * peak capacity = peak revenue of around 15-20cr from seals

-

Peak revenue potential (strapping + seals): 300cr + 15-20cr = 315-320cr

-

Target time for peak revenue: 4 years

-

In Parallel, Packing Contract growth can give us a very good revenue considering the market size

-

2nd plant got commissioned in May. 16-17cr invested in 2nd plant capex line. Reason for delay in commissioning → Machinery was delayed for 3.5 months → during installation also, we have one of a kind line, took longer than expected for installation and trials

-

Capex plans for FY25-26 → We are contemplating various expansion plans. There will be a further capex this year, in a couple of months, we will make the announcement

2. Market expansion

-

Chinese risk in the Middle east? → FTA with UAE, 5% duty benefit if the customer buys from India - We also have local presence in the middle east, and we offer total packaging solution vs. Chinese/Koreans who can only provide strappings - We provide HDPE/LDPE etc. to them too

-

What if Chinese also set up a unit in middle east? → we will be at par with any manufacturer in that region because we can now buy from China, Korea or wherever pricing is cheap

-

Reason for delay in Middle east expansion? → Capex heavy investment, we are just off 1 capex, want to grow this before starting another capex. Also, looking for a strong partnership in the region. We are talking to people and getting more info about that market every day, so delay is good, we want to do this in a better way

-

US/Europe expansion plans? → If I produce from another country and supply to the US, that will take up to 2 years max. But what we are doing, we started exporting directly from India to the US. Even after applying the anti-dumping duty of 25%, our price is still attractive vs. the local manufacturer price. Even this quarter, we have done close to 1cr, these are repeat orders. This year also we can do decent sales despite the duty. By the time we set up a plant in middle east, we will have ready set of customers to supply to

-

We are also focusing on US, Sri Lanka, Bangladesh, Australia, Africa, Europe etc. Wherever we can get large volume buyers in the world

-

Domestic-Export split: 88cr from domestic in FY24, 17cr from exports.

-

Domestic diversification → we are supplying pan India basis

-

Fy25 Export target: confident of doubling this number; Down the line 5 years → we will be maintaining at least 100 cr export sales including all products

3. Distribution

-

Currently, there are no distributors in India. We do direct sales. Time to time, dealers also purchase from us, but they don’t have any exclusivity

-

In middle east, we do have some distributors, for small clients buying upto 5-6 lacs per month - we have some 3 different distributors for various products

-

For big clients (at least 30 lacs per month) in overseas market, we deal directly; Same concept is being tried in other overseas market

-

Network plans this year - at least we will appoint distributor in all major countries/continents this year

4. Packing contract growth and orderbook

-

Top 10 customer contribution - last year was 52-55 cr - roughly 50% contribution

-

PSU margins better - SAIL is the biggest buyer - we are currently supplying to the Salem plant, smallest plant. To supply to Rourkela or Bokaro, stringent requirements - we are yet to fulfill those requirements. Hoping to enter big steel plants in east; once we do, we can expect a better margins from PSU

-

Currently, In terms of orderbook, PSU contribution is very less. 1 more order we are expecting from Vizag

-

Getting small small orders and getting eligibility into bigger contracts

-

Competition for these orders → 3 companies

-

Packing Contract given at client-plant-production line level. For e.g. JSW has 15+ different locations or plants → each plant has different production lines → in each production line also, we get contract from a different guy

-

By entering 1 location, we open up the opportunity to participate in all locations

-

Bid pipeline → 200cr; some of these orders are around 60cr annually. Hit ratio? → 20% expected from current pipeline = 40cr. Participating in 5-6 bigger contracts than Vedanta; Positive that this value will increase substantially in coming months

-

Current Packing contract orderbook → ~27cr

-

More than 50% contribution of packaging contract to topline in coming years. Expecting significant growth in PC in both domestic and export market

5. Guidance

-

Topline growth → Minimum 25% overall growth this year and this trend will continue for next 5-6 years

-

Domestic growth → targeting 25% overall growth this year; Exports at least 50%

Put together overall, at least 25% in strapping space; Packing Contract also same -

This year we will be able to maintain the ongoing growth% in PAT

-

From long term perspective, the intention would be to keep the Operating margins in long term will be between 15-20%

-

Market share - Long term Aim to capture 30%+ market

Current Strapping market share - more than 10%

Packing Contract - much less than 5% -

Utilization for new plant this year → just started commercial production → it is not running continuously → current would be less than 15% → this year it will reach at least 40-50%

6. Industry & Risk specific

-

Downcycle in the industry? - if steel production of India goes down, defs our sales will also go down

-

If Steel prices go down, impact on margins? → absolute margins → pricing = fixed + variable component; fixed component comprises our value addition such as production cost, salaries etc. and our margins → so, whatever is the steel price increase or decrease MoM or QoQ, we pass that change to the customer → so, the absolute value also remains intact; lag of 1-2 months.

-

In long term orders, there is a clearly defined price variation clause; Any contract with high steel strapping contribution is having a price variation clause

-

Margin spread is fixed or absolute. Impact on Margin% → So, when steel prices are high, the margin % is lower since the margin is a smaller proportion of topline and vice-versa

Low steel prices environment → better margin %

High steel prices environment → lower margin % -

TMT sector - Low tensile straps - biggest competitor does not give color strapping (only 2 manufacturers in India) - We are very strong in south market, TN, Kerala, Karnataka - In secondary TMT market in Raipur/Jhalna, they don’t care about branding if the quality is good - but in our market, branding is important

7. Misc

-

200+ customers

-

3 verticals: 1. Direct sales of strapping and strapping tools 2. Packing contracts 3. Primary packaging - all the allied products except steel strapping

-

Margin profile in trading other products better than steel strapping

-

PC vs strapping biz margins: very similar margins

-

Reward shareholders → right now, cant commit. We will look at something

17 Likes

Just wanted to say that I keep coming back to this thread every time I need some answers or want to check on the key monitorables, guidance etc. It almost always answers all my questions so thank you once again ! After building conviction in the fundamentals of the company, I was just tracking it from the sidelines for a few months to see what the support range was for this stock. I felt like 200-220 was that zone and when it recently took support there and moved up (4th attempt in the last 6-8 months), I finally bought it 3-4 weeks ago. Eager to see how the next set of results pan out.

Note - Invested, biased and not qualified or knowledgeable to give any kind of investment/trading advice.

3 Likes

Krishca fund raise 020724.pdf (4.7 MB)

- Looks like Sanjay Gupta (Apl Apollo ) invested in Krishca strapping as a strategic investor

- Looks like Shyam Steel family also invested.

- Big boys in the steel business are backing Krishca

Disc :Views may be biased bcos of holding ,please do your own due diligence

12 Likes

Shyam steel investing in Krishca is good especially because they also recently gave a packaging contract to Krishca for their TMT strapping, worth over Rs. 1.81 crores. So they must really like Krishca’s products and believe in their business.

Note - Not investment advice and I am definitely biased as i am invested ![]()

7 Likes

My question is why did the company go for preferential allotment instead of rights, is it not bad practice on part of the management ?

1 Like

From what I have read that, the issuance of preferential share requires very less paperwork. I think it is more convenient for the management to raise money this way. I have also seen other SME and microcap stock doing same thing to raise money.

1 Like

In SMEs, this is the pattern going on, after a few months company raises pref. All the SMEs are doing the same.

How to interpret the preferential issue price of 233 which is way below the current CMP.

Is it negative for the stock price?

It is like sureshot 70% profit for the preferential allottes.

Why can’t they go for debt if they are so much confident about their growth?

At the time the price was decided, the stock ran up a lot after that, that’s why the discount looks huge. Just see the price action for the past few days and you’ll know what i mean.

5 Likes

Preferential equity is the best way to raise funds.Stock is reacting to that only.

3 Likes

https://nsearchives.nseindia.com/corporate/KRISHCA_04072024201349_KRISHCAEGMNOTICE2024.pdf

Objects of the Preferential Issue/ Issue of Equity Shares and Warrants: -

- Expansion of manufacturing facilities of the Company. - Rs. 46.50 crs.

- Working Capital Requirements of the Company. - Rs. 12.50 crs.

- General Corporate Purpose. - Rs. 9.04 crs.

Promoters holding after dilution: 52.07%

Note:- All information below are gathered through internet. So, it may not be true.

Strategic investors:

- M/s. S Gupta Family Investments Pvt Ltd - Apl Apollo Group.

- M/s. Subham Buildwell Private Limited - Shyam Metalics & Energy Ltd.

- M/s. Narantak Dealcomm Limited - Shyam Metalics & Energy Ltd.

- M/s. Real & Sons - Real ispat and power limited.(Raipur)

- M/s. Shri Bajrang Commodity - Shri Bajrang Power & Ispat Ltd.(Raipur)

Other prominent Investors: –

- Sachin Kasera – Svan Investment Managers. (Before co-founding Svan Investment Managers, Sachin kasera was Fund Manager at Lucky Investment Managers from 2009 to 2019).

- Jigar Chandrakant Shah – Svan Investment Managers.( Before co-founding Svan Investment Managers, he spent over sixteen years at Motilal Oswal catering to HNIs and institutional clients).

- Svastha consulting LLP –- Ashish Kehair. ( Managing Director and CEO of Nuvama Wealth Management Limited.)

- M/s Marigold Partners – Sachin Kasera.

Disclosure: - Invested. Not a buy or sell recommendation.

11 Likes

The success story of Krishca Strapping Solutions.

8 Likes

My take way is this new Specialty steel division, currently only 1 company in India is making these products , Krishca will be the second one.

9 Likes

Krischa’s move to set up a manufacturing facility in the Middle East is shaping up to be quite an interesting puzzle. As I dug into potential locations, I stumbled upon some surprising details about trade agreements and regional dynamics.

You might find it interesting that two GCC (Gulf Cooperation Council) countries have had Free Trade Agreements (FTAs) with the U.S. since 2006. Yet, trade volumes with these nations remain surprisingly low. So, what’s behind this?

Bahrain: Bahrain is home to the U.S. Navy’s 5th Fleet, which oversees naval operations in the Persian Gulf, Red Sea, Arabian Sea, and Indian Ocean. It’s also a key logistics hub for missions in Iraq, Afghanistan, and Syria. While this makes Bahrain a significant strategic partner, it also means navigating a complex web of regulations if you want to set up a manufacturing plant there.

Oman: Oman’s location near the Strait of Hormuz is another crucial factor. This strait is a major chokepoint for about 20% of global oil and gas shipments, offering direct access to the Indian Ocean. This strategic position makes Oman important for monitoring regional oil flows and potentially isolating Iran if necessary. But, as with Bahrain, its strategic importance brings a host of regulatory hurdles & long standing approval processes.

So, that leaves us with the UAE, Kuwait, and Saudi Arabia as potential alternatives. The UAE stands out for being the most business-friendly, but there’s a catch. Former President Trump has hinted that if re-elected, he might impose a 25% tariff on steel and steel products from all non-FTA countries, which would include the UAE too.

This future tariff could make exporting from the UAE a challenge in future.

For Krischa, picking the right location is crucial. If they can establish a presence in Bahrain or Oman, they could potentially see significant sales up to ₹500 crore within a year, thanks to the U.S. FTA, along with FTA with Singapore and direct access to the broader GCC market.

If Bahrain or Oman doesn’t pan out, they would still have access to local markets but might face the potential 25% tariff on steel if they’re in the UAE.

In the end, Krischa’s choice of location will be key to their success and efficiency in the Middle East.

Let’s see !!! This is just my opinion, I am no expert on Middle East, Always open for a healthy discussion.

You can follow me on twitter - x.com

9 Likes