My complete research on KRISHCA STRAPPING SOLUTIONS

About

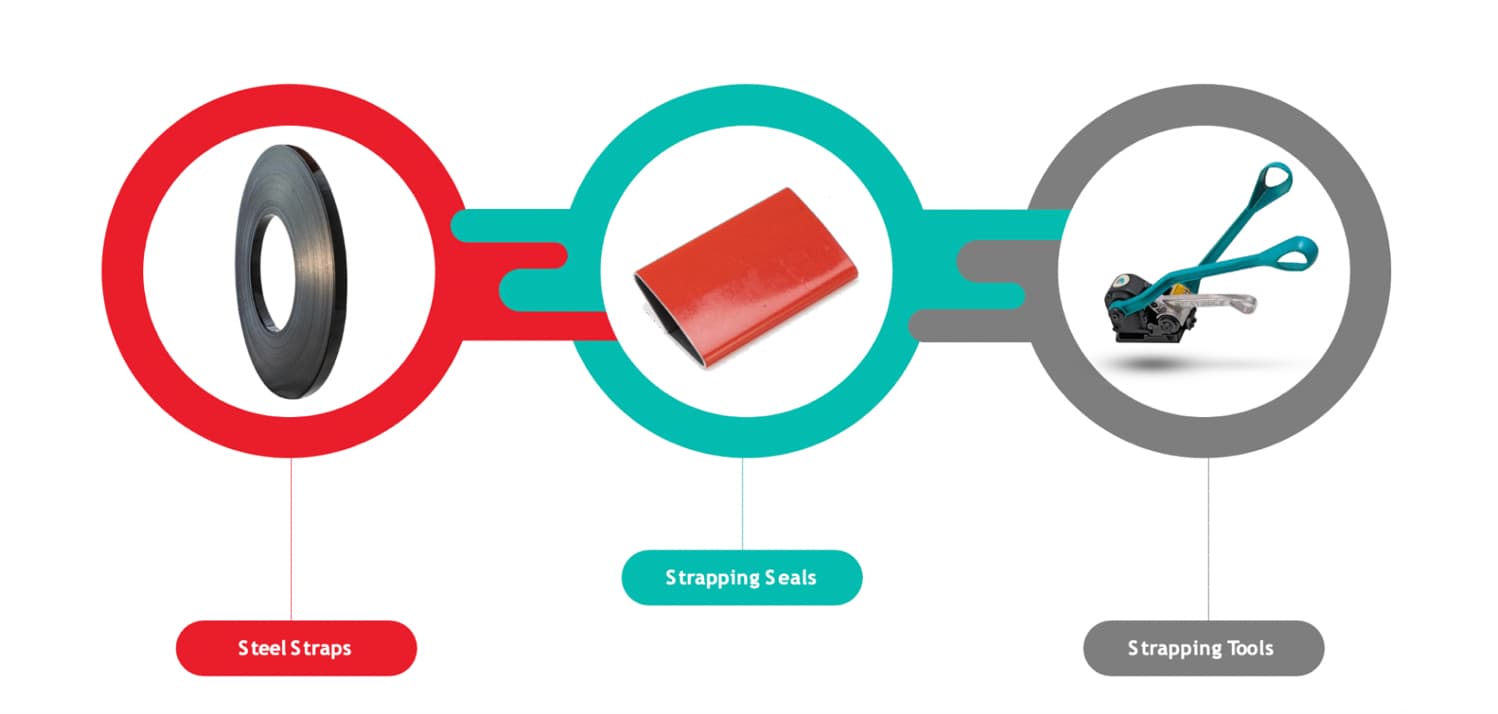

Incorporated in 2017, Krishca Strapping Solutions Limited is a manufacturer and wholesaler of Strapping Tools and Seal.

Krishca partners with top manufacturers to provide a complete range of steel strapping tools for various packaging applications.

Quality is always assured at Krishca because they only purchase from ISO certified primary steel mills.

The company raised 17.93cr through a fresh issue (not ofs, which means promoters believes in the business).

The issue was utilized for:

A) Capital Expenditure for setting up of New Strapping Line

B) Repayment of Borrowings

C) General corporate expenses and issue expenses

Already reduced the borrowings, and also planning to commission the capex by December 23.

The company website is top notch and very smooth.

The company is proud to be India’s first “Lead-Free” and eco-friendly production line for the heat treatment of steel strapping.

The industry they are catering to is steel mills, mainly JSW Steel, Tata Steel etc, all those are bigger steel mills.

The steel is produced at a very high temperature. Their steel straps are used to pack when the steel coil comes out of the oven, which is almost 200-degree, 300-degrees. There is no other material/product which can withstand this temperature during packing.

Offers guaranteed high quality straps with optimal physical and geometrical properties, as every millimetre of the strap undergoes a rigorous quality control test.

Offers three types of straps: Prime, Super Prime and Ultra prime.

Each millimetre of the strap undergoes a state-of-the-art heat treatment process using PLC-controlled automation that delivers superior elongation, shock resistance, and break strength.

Their automated quenching process ensures uniform grain structure across the entire length of the strap, while the heat treatment produces a distinctive blue-shimmering oxide layer that acts as a natural barrier against corrosion.

Krishca’s technology provides the company with a competitive advantage over its rivals, as it has a lower cost of production than the industry standard by reducing the rate of scrap generation, making the production process more energy-efficient, and reducing environmental impact.

All their Steel Strappings are treated with a Wax coating finish. This lubrication allows the strapping to flow smoothly in automatic machines, tools and around corners of the products. They offer three types of surface finishing.

-

Blue Tempered

-

Painted

-

Zinc

Apart from providing high quality strapping solutions at competitive prices, they also provide unique and customized colour printing on the steel seals to facilitate customer’s branding.

Their commitment to providing the highest quality tools to their customers is reflected in their prompt and effective solutions for their packaging needs. Their service team consists of factory-trained engineers who work closely with each client to identify the most effective strapping tool for their specific application.

State of the art equipment

A) PLC Controlled automatic production line

B) Automated heat treatment process-Uniform grain structure

C) Pollution-free production process - Lead-free

D) Super Jumbo coils upto 500 Kg

High-Quality Compliance

The steel strap quality requirements of the company are in compliance with American, European, and Indian standards.

IS 5872:1990 - Cold rolled steel straps (box strappings) specification;

ASTM D-3953 - Standard Specification for Strapping, Flat Steel and Seals; and

BS EN 13246:2001 - Packaging.

Its products are sold under the “Krishca” brand., which has garnered 7.5% market share amidst peers like Signode India, Grip Strapping, Tata Steel BSL, and Walzen Strips.

Since they already have steel strapping, and also are very comfortable in supplying strapping tools to do a packing contract.

Let’s say a TMT bar is being produced in a steel mill. They will need a strapping tool and also steel strapping to do the packing and the manpower to do the packing.

So out of three elements, they have the steel strapping and the strapping tools.

And now will start with packaging contracts.

In the long run, three years to four years, they are aiming to get at least 30% of revenues from packing contracts.

Since the COVID lockdown was imposed. So in the first financial year, they were not able to cater the large volume customers like JSW and Tata Steel because they never completed the vendor registration in the first year. So were mainly supplying to the local coming out players.

So the customers were very limited, hence higher revenue concentration.

But now in the last one to two years, have added many new customers like JSW Steel.

Out of the total contracts and orders, about 40% are long-term contracts from various mills, which have a contract of five years.

And POSCO, which is a Korean company, they are supplying to the entire six service centers in India. There they have a six-month contract.

And there are packing contractors with whom they have a one or two-year contract.

So the remaining 60% of sales will go to multiple people on a spot basis.

Company has employed 50 employees as of February 15, 2023 on payroll. The above includes employees in the top and middle management, and also employees and labour who are part of the manufacturing unit, human resource, administrative staff and office staff.

Apart from this, they also engage contract laborer to facilitate manufacturing operations.

EPFO payments are being done for 40+ employees, proving their employee strength of 50. The amount being paid is also being increased regularly.

A very sophisticated setup with strong focus on quality for a company this size.

The MD has vacant land, which is used as security against their short term borrowings, we don’t know if this is personal land or for a company.

Clientele

Management

One interesting thing to note is these companies were incorporated in 2023 feb, except markwell

Found some info on markwell- it is into high resolution inkjet printers, continuous sealing and vacuum packaging. They are working in collaboration with a German based company

About Us | Markwel | Large Character Coding and Marking | High Resolution Inkjet Printer | Laser systems

I couldn’t find the website of any other company from the above list, except markwell.

The MD is 30 years old and was previously in the cyber security business, a bit risky as the business he is doing now is all very different.

Although He has performed a detailed market research on steel strapping for almost a year between 2017-18 for setting up this Company, and also the overall numbers speak volumes.

He has over 3 years of work experience as a cyber-security consultant in the UK where he has handled several cyber security compliance projects for companies such as Visa and Samsung.

The Chief of Operations- Rajarathinam Govindaswamy has previously worked for TUBE INVESTMENTS INDIA for 33+ years.

The CFO is holding a marketing degree? And is the wife of the MD, and the wife’s sister is also a director, with close to 13% equity ownership.

The CFO of Phantom Digital is also an independent director here.

The management is very confident on the growth and demand for the company and its products, hence doubling the current capacity which is not even fully utilised right now.

The management is very thoughtful and smart and does not take irrational decisions, and is also very ethical and aware –

Seeing that Krishca cannot supply to the US due to the anti dumping duty, it decided to set up a base in the Middle east and use it as a trading arm. They took this decision as they already supply to the Middle east, have done market research there and have some lay of the land.

If they wanted they could just route the products from India to the US through the Middle East, but they know that it’s not ethically correct and hence did not act on it.

Entry barrier

The manufacturing process consists of a total of 15 steps, which is very complex. This is very difficult to do and thus acts as an entry barrier for new entrants.

The major entry barrier in this industry is getting your product approved at all levels.

It took them almost three years (covid elongated the process a bit) to get their products approved because steel strapping is a very safety critical item.

The items packed with steel strapping are weighing between 10 tons to 25 tons.

Even if there is any small crack in the strap, it will break, it will lead to a very severe accident or fatality.

So steel mills give utmost importance to steel strapping purchase.

If you look at the public sector, like SAIL and Vizag steel, all those steel companies, that is even more difficult because they will ask to provide a PO from private mills for at least INR10 crores, INR15 crores worth of purchase orders in the last two years.

So even to participate in the PSU, one needs at least three and four years of experience and market presence.

Moat

Quality- They have India’s first ‘Lead Free’ environment friendly production line for the heat treatment of steel strapping.

Company has a lower cost of production than the industry standard by reducing the rate of scrap generation, making the production process more energy efficient.

They are using an induction based furnace and competitors are using a muffle based furnace. So, the energy cost is almost 50% of competitors.

Their customers save 3000 – 4000 Rs/Ton in freight charges when purchasing from Krishca instead of other players, due to its plant location.

When they compete against a US company (Signode) and a German company (Grip), their overheads are much lower, due to cheaper availability of labour and materials in India.

State of the art production line: own India’s most advanced, Integrated and fully automated production line. Their production cost is less than 50% of the competitors.

Their production is the only fully automated production line.

From the start to end, it is a single production line which is fully automated. If you look at the competitor, all other people are doing a two or three step process. So, this provides them with the lowest production cost in the industry when compared with competitors.

Remarkable surface finish: They use special grade water based paints and their custom designed modern oven dries the paint inside which results in a blister free, uniform paint finish across the entire length of the strap.

Custom Branding: provides Industry leading packaging customization in strapping Colours and logo printing on seals.

During covid Krishca focused on R&D and came up with a line which can process multiple grades of steel (raw material), and also their induction oven can tune the temperature very easily between 300-degree to 700-degrees. Therefore they can use various alternate grades of steel which are cheaper compared to the traditional grades used by competitors. Hence even in the raw materials they are saving about 5% to 6% compared to the competitors.

Having a lower employee cost as the line is automated, so require fewer employees when compared to peers.

Due to all these reasons their peers have a single digit margin, whereas Krishca has close to 20% ebitda margin.

Positives

The management gave a growth guidance of 35-45% for FY24 due to increased sales from current operations plus revenues from the new strapping line, which will come online by December 2023.

Trade receivables as percentage of sales has been coming down Y-o-Y.

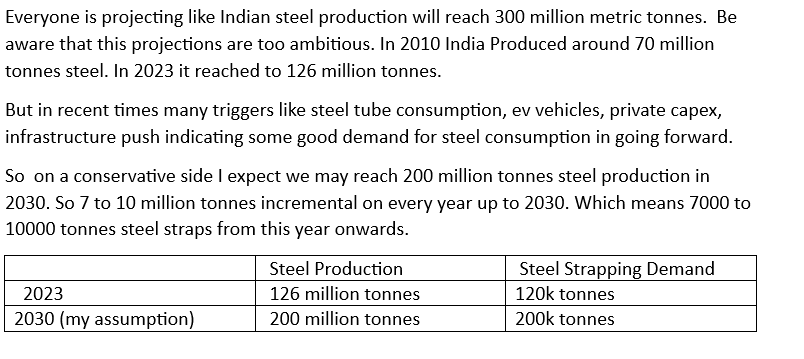

As per the Nation Steel Policy 2017, total Indian steel output is projected to reach 300 Mn Tons by 2030. To Cater the Industry’s rising output as well as to serve the overseas market, they plan to double their capacity.

Very important points above

Only steel strapping manufacturer in Chennai

Zero litigations, neither against/by the company, nor against/by the directors.

Company is able to pass on raw material costs on a monthly basis, except for longer term contracts.

The margins are not impacted by the volatility in the steel prices as they have a quarterly contract with some suppliers, and have a 6-month contract with some suppliers. And also, have a monthly spot price supplier.

So, they have different combinations of suppliers. So, even if there is a sudden price increase, let’s say in July, August, they will mostly buy from the quarterly supplier or 6-month supplier. So, they will keep the price the same for 3 months, 6 months period. So, like that, by having multiple suppliers with different pricing policies, they are able to protect themselves.

Signode the industry leader cannot supply to the Middle East through the Indian plant, as they already have an internal agreement to only supply from Turkey, even the other international players are somewhat restricted due to their international presence. Hence Krishca will benefit here as Turkey cannot compete with Indian pricing. Therefore Krishca will be more attractive for the customers there.

For the first time they are participating in a PSU tender in August. Have recently got all the credentials to participate in the tender itself. In the PSU sector the margins are higher

In addition to expanding the production capacity, also venturing into the

packing contract segment.

- appointing a head of packing contract division from August 1st.

- The reason for entering the packing contract is that it provides a very stable order. Each packing contract is a minimum one year, even up to five years. So once they get a packing contract, steel strapping sales are assured for a minimum one year at an agreed price. So this gives them assured revenues.

- This will help them gain more customers, bigger contracts, and more predictable revenues.

- The margins in this business is upto 15%, but can help Krishca garner a significantly higher topline.

Steel strapping imports.

- There is a BIS certification required for any steel strapping manufacturer to supply to India. If you look at the overseas suppliers, there is only one company in the world that has BIS out of India. Only that company is able to supply to India, which is a Korean company.

- None of the Chinese mills have BIS. Let’s say, somebody goes ahead and gets a BIS. They still have to face import duty, which is 7.5%. And there is an import duty for steel strapping grade, almost 10%. So, roughly 18% additional tax somebody has to pay in order to supply to India.

- The Chinese are cheaper by only 20%, so even if they enter the markets they will be at par with domestic suppliers.

Setting up a new office in Dubai, already in the process of incorporating a subsidiary.

- In the US there is an anti dumping duty of 50% for steel strapping. So another reason for setting up a base in MIDDLE EAST is to get the access to export their products anywhere in the world without any anti dumping duty.

- By the end of July, they will have an operational warehouse and office in Dubai and already have a few people to join from August.

- So, from their new office in Dubai, they are expecting to increase revenues not only by selling steel strapping, but also trying to trade other items to provide a total packaging solution to customers.

- In the Middle East, there is not even a single steel strapping manufacturer in the entire Gulf Middle East region. So that’s where they wanted to explore initially. And already most of their export sales are going to the Middle East only.

- And the major goal of setting up an office in Dubai is that after one and half - two years, they are going to come up with a production line in the Middle East.

Management is confident of a minimum increase in revenue of 40% year on year for the next five years.

Operating leverage-

- The company achieved an overall capacity utilisation of 55% approx. for FY 2022- 23.

- Currently it is operating at 60%, expected to go to 75% (can do 150cr from current capacity at optimum utilisation).

- As and when their volumes increase, the fixed costs are going to remain the same and hence the margins will improve.

Huge potential to increase exports, the management wants to take exports to 30% from approximately 7% now.

Negatives

Does not own the registered office of the company, it is on lease

The CFO of Krishca has a marketing degree, she is the wife of the MD, a bit shady.

The steel industry is highly cyclical and volatility in steel prices may have an adverse effect on the Company’s results of operations and financial condition. As and when the steel price drops the topline also takes a hit, although there is no or only a miniscule impact on the margins.

Basically for the topline to grow the steel prices rising is a god thing

Have issued Equity Shares (through rights and bonus issue) during 2019, 22, 23 at a price below the Offer Price.

Given that their business revolves around steel strapping, the growth of the steel industry and its demand plays a major role.

Company is substantially dependent on few customers/suppliers for their operations. As on February 15, 2023, the top 10 customers account for 68.73% of their sales. Similarly, their procurement is 92.48% from top 10 suppliers and more than 68% from top 5 suppliers (mar 23).

Their services are skilled and creative manpower intensive.

They spend significant time and resources in training the manpower they hire. The success is substantially dependent on their ability to recruit, train and retain skilled manpower.

High attrition and competition for manpower may limit their ability to attract and retain the skilled manpower necessary for future growth requirements.

Since they will just be starting with the packaging contracts this year, the first 3-4 contracts will be hard and they will face some issues which may impact margins (my opinion).

Have given the guidance of 35-45% topline growth based on the commercialization of the new strapping line, which is expected in December. If somehow the line gets delayed, it will impact/delay growth.

‘’the Board of Directors of the Company have been authorized to borrow money from time to time, any sum or sums of money as the Board may deem fit, notwithstanding that the money to be borrowed together with the money already borrowed by our Company may exceed in the aggregate, its paid up capital and free reserves and security premium (apart from temporary loans obtained / to be obtained from bankers in the ordinary course of business), provided that the outstanding principal amount of such borrowing at any point of time shall not exceed in the aggregate of ₹ 50 crores (Rupees Fifty Crores Only).’’

SHADY

Capacity

Manufacturing facility in Chennai with capacity of 18,000 MT of steel straps and 80 million Seals per annum.

Company intends to double its production capacity, and the proposed facility is capable of producing Ultra High Tensile Steel strapping which will enable the company to enter into new segments like wagon lashing and jute packing.

Increased capacity of seals by 30%.

The company achieved an overall capacity utilisation of 55% approx. for FY 2022- 23.

Geographical Revenue Bifurcation

Financials

Financial highlights of FY23,

- total revenue was INR72.4 crores in the last financial year which is a 386% growth when compared to FY22

- current EBITDA is INR13.87 crores which is almost 330% growth compared with the previous year

- current EBITDA margin is about 19.15% which is almost 2% increase when compared against the previous financial year

- Net profit for FY23 is INR9.34 crores which is a significant growth of 518%. So, almost five times our net profit has increased when compared against FY22

- Net profit margin is about 12.9% compared to 8% in the previous year.

- current earnings per share reached INR10.68 paisa compared to INR2.22 paisa in the previous financial year.

The sales have been growing multifold since the last three years

Cash flow from operations have suddenly rocketed in FY23, majorly due to increase in trade payables and wrongful writing of short term borrowings in cash flow from operating activities instead of financing activities.

Trade payables have shot up close to 8 times, although all these are outstanding for less than 1yr, so we need not worry about them defaulting

Although the receivable days have increased, the inventory levels have come down by more than 50%, hence bringing down the working capital days.

The reserves and surplus was previously negative, now in FY23 have turned positive significantly.

Long term borrowings have come down.

The short term borrowings have shot up.

The plant and machinery has come down a lot from previous years, due to very high depreciation.

CWIP has increased a lot, indicating that they are deploying the IPO funds for the capex.

The inventories have increased multifold, due to increase in finished goods.

Trade receivables have more than doubled, may be due to significant sales growth of close to 300%. Out of this majority is outstanding less than 6 months and rest is 1 year

Industry

The Global Steel Strapping Market Size was estimated at USD 1218.74 million in 2022 and is projected to reach USD 1533.15 million by 2028, exhibiting a CAGR of 3.33% during the forecast period.

Indian steel industry is the second largest in the world with the output of 113 Mn tons per annum in FY 2021 - 22. As per the Nation Steel Policy 2017, total Indian steel output is projected to reach 300 Mn Tons by 2030.

The per capita consumption of steel has increased from 57.6 kgs to 74.1 kgs during the last five years.

Easy availability of low-cost manpower and presence of abundant iron ore reserves makes India competitive in the global set up.

Based on the market research, the current market size of steel strap consumption in India is 9000 – 11000 Ton per month.

As the industries which use steel strap are projected to see a rapid growth in the next 15 years, the steel strap consumption is also expected to see 5-10% growth each year.

What would increase consumption of steel

In the next three years from June 2021, JSW Steel is planning to invest Rs. 47,457 crore (US$ 6.36 billion) to increase Vijayanagar’s steel plant capacity by 5 MTPA and establish a mining infrastructure in Odisha.

In August 2021, Tata Steel announced to invest Rs. 3,000 crore (US$ 404.46 million) in Jharkhand to expand capacities over the next three years.

In October 2021, ArcelorMittal and Nippon Steel Corp.'s joint venture steel firm in India, announced a plan to expand its operations in the country by investing ~Rs. 1 trillion (US$ 13.34 billion) over 10 years.

In May 2022, Tata Steel announced a CAPEX of Rs. 12,000 crores (US$ 1.50 billion).

The Union Cabinet, Government of India approved the National Steel Policy (NSP) 2017, as it intends to create a globally competitive steel industry in India. NSP 2017 envisages 300 million tonnes (MT) steel-making capacity and 160 kgs per capita steel consumption by 2030-31.

The Government of India raised import duty on most steel items twice, each time by 2.5% and imposed measures including anti-dumping and safeguard duties on iron and steel items.

In July 2021, the Union Cabinet approved the production-linked incentive (PLI) scheme for specialty steel. The scheme is expected to attract investment worth ~Rs.

400 billion (US$ 5.37 billion) and expand specialty steel capacity by 25 million tonnes (MT), to 42 MT in FY27, from 18 MT in FY21.

In addition, enhanced outlays for key sectors such as defence services, railways, roads, transport and highways would provide impetus to steel consumption.

WILL POST SOME IMPORTANT DETAILS ABOUT ITS PEERS SOON.

till then do share your observations and learnings