Q2FY23 CONCALL NOTES

• ADVANTAGE OF GST: KRBL is going to have enormous advantage with the imposition of GST on unbranded prepackaged rice. This has brought parity between private label and established brands. With the imposition of 5% GST, the demand for KRBL brands have improved significantly which would be witnessed in the third quarter.

Growth has been equally contributed by the general trade and modern trade e-com channels. It is notable that within the general trade channels, bulk pack segment has led the growth. The decision to charge 5% GST on pre-packaged food nullifies the advantage local players had over established brands. We have been looking forward to this for the last 5 years. This decision will formalize the sector and lead to healthy competition.

We got a big benefit in HoReCa due to the abolition of 5% GST on a pack above 25 kg. Now our every pack which is of HoReCa is 30 kilos which is out of GST ambit. Number two, we are doing all our 30 kg sales in India Gate or Unity or our registered brands. Previous year, we used to pay 5% GST and our competitors were not paying any tax because they were not branding under their registered brand. So that was a big benefit, and we are getting this benefit in third quarter. You will see in quarter 3 our HoReCa sales, especially in the domestic market, will take a jump. And I should not say, but it will take a jump of nearly 50% more in quarter 3, what I am expecting.

• SAUDI BUSINESS: We have still to finalize the HoReCa segment for which our efforts are ongoing, and we expect that during Quarter 4 we will be able to finalize it. As regards the INR 1100 crore business of Saudi, I am quite positive that we will be able to do at least INR 550 – 600 crore this year, and another INR 500 crore in HORECA business once the distributor is finalized.

• LONG RUNWAY FOR COMPOUNDINIG GROWTH: While the basmati penetration in India is at 42%, the packaged penetration hovers around 20%. We are constantly reminded of the immense headroom for growth in the segment of this business.

We consume around 95 million tonnes of non-basmati rice annually, whereas basmati rice consumption is just 2.5 million tonnes. So, as you can well imagine, there is a very big scope of growth for basmati trade as far as domestic market is concerned

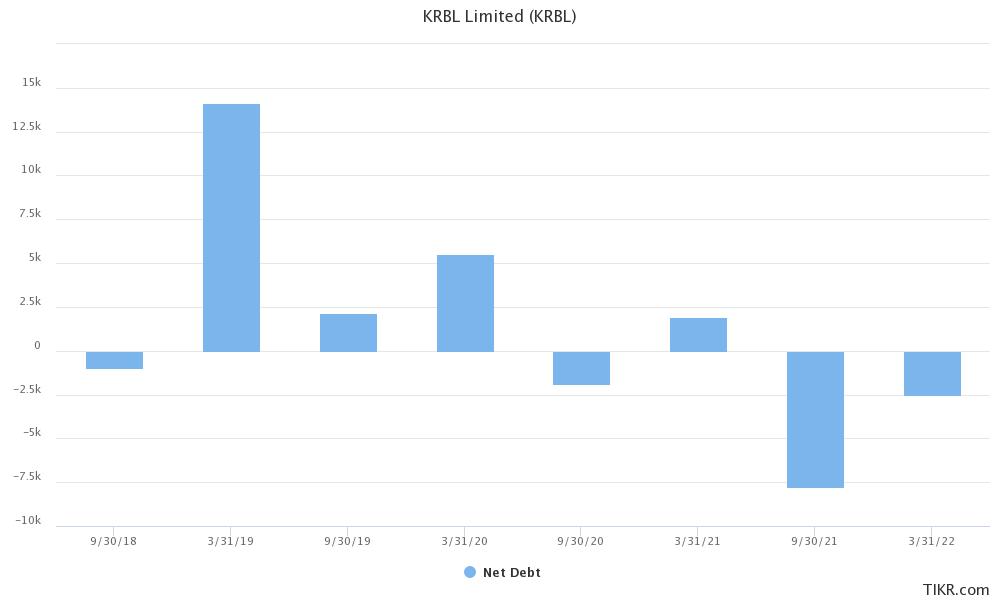

• PADDY BUYING TO INCREASE SUBSTANTIALLY BECAUSE OF ROBUST DEMAND: And number two, I’ll be buying more quantity by not even 25%, it can go up to 30%, 35% more buying, because our demand in Saudi Arabia has gone up, our demand in domestic market and requirement of the branded rice has gone up. So, because whatever paddy we buy today, we have to take it in mind for the next 2 years. So looking at our demand, we will be buying 30% to 35% extra. That means 15% prices more, 30%, paddy is more. So, we’ll be taking around INR1,000 crore, INR1,500 crore from the bank this year. And naturally, our ROCE will become better.

• On the distribution front, we are diligently expanding our direct distributor network to town Class 1, town Class 2 and rural markets of India. We have effectively appointed 167 new distributors in this financial year so far, and we are on track with our target to expand our distribution reach to 250 new towns by the end of this financial year. Our numeric distribution percentages had already increased by 370 basis points in quarter 2, but we’ll be seeing the true results of this in the subsequent quarters.

• I’m happy to share that Unity brand has grown by over 40% in this financial year and is on track to reach the INR1,000 crore mark by the end of financial year 2025.

• We have developed a strong pipeline of new product introductions which span across the value-added rice segment as well as the health segment. We will see us launching few of these products in the next 2 quarters.

• We cannot say, but our expectation is looking at the crop and the demand. And the carry forward stock in the industry was practically zero this year. So, everyone is taking rice, and we expect the prices to be higher.

• So, we are comfortable as far as pricing is concerned because of our brand. It is fully shielded by our brand.

• Yes, whenever we go to the ministry, we always compare basmati rice with whiskey and wines. Basmati is the only grain in the world where the older it is, the better. And, we have been working on this basis only, whether it is GI or it is pricing. But we found out that it is not commercially viable to age the rice for more than 2 years, because cost, interest and so many things are involved. That is why we have kept it at 2 years. Last year we fell short by just few hundred tonnes of 2-year-old stocks. We went to the market and were willing to pay even Rs.50 / kg extra for a 2-year-old Basmati rice. Much to our astonishment, not a single kilo was available. I can confidently say, that in the whole of India nobody other than KRBL is having 2-year-old Basmati stocks as of today. This is where our advantage comes into play. We stand a cut above others clearly in terms of pricing & quality.

• And I would like to add one thing in the last 30 years of KRBL history, KRBL has never done inventory devaluation. It is always lower than the market price, and that is the reason why we carry aged rice

• There are 3, 4 advantages with KRBL. Our carrying cost is lower compared to the industry. We always make cash payment to the farmer and others, and thus we get 3% to 4% cheaper paddy from the market compared to many. I will not say we are the only ones who work like this, but our payment to the farmer is so excellent that we always get a cheaper paddy. Thirdly is the brand, the premium on the brands. Given these 3 points, we cannot afford at any cost to remain without the raw material. We cannot go to the market after 6 or 7 months in search of the right quality of paddy or rice. As I said earlier, we fell short by a very small quantity last year and we couldn’t get any quantities even when we were ready to pay extra. So, this year, we have decided to buy more quantities, looking to the price levels, inflation and all other costs. I was thinking of 25%, but Anoop said that we are going to buy 35% higher volumes over last year.

• ON PRIVATE LABELS: But in future, that can be a big risk to our brands because e-commerce is taking more and more share, more business-like of the whole market.

Ayush Gupta: We see e-commerce to be a very consumer-focused channel. So, consumer demand and brand strength continue to be the prominent drivers to sale. So private label player does not stand to gain a lot of penetration or market share from an e-commerce perspective because the consumers are more brand-conscious and less price conscious, I would say.

.

.