As far as KRBL is concerned, I guess the global rice shortage may not be a big trigger…because they are exporting mostly basmati rice, and the closest alternative is a similar variety from Pakistan…so if Pakistan has shortage of the similar variety, then yes, KRBL benefits, which happened in Q3 and will probably happen in Q4 as well…and they mainly export to Middle East…and Iran but that has some payment issues currently…their exports to other countries is not material currently.

2 Likes

Source: FundIndia Report on KRBL

KRBL Ltd. – India Gate Basmati Rice

With a rich industry experience of more than a century, KRBL Limited today has created its place as the top player in the Indian rice industry and also as India’s first integrated rice company. Operating primarily in the realm of manufacturing and marketing of rice products, the Company’ success has been derived by operating responsibly, executing adeptly, manufacturing innovatively and capturing new opportunities proactively. KRBL has its two manufacturing facilities spread across the states of Uttar Pradesh (Gautam Budh Nagar) and Punjab (Dhuri). The four state-of-the-art grading, sorting, and packaging facilities of KRBL are located at Sonipat, Gautam Budh Nagar, Dhuri, and Alipur. With its corporate office in Noida, UP and registered office in Delhi, KRBL has its product presence not only in India but also across the globe. KRBL exports basmati rice products to 90+ countries and leads the basmati rice consuming market in the branded segment.

Products & Services:

The Company offers its rice under a range of brands, including India Gate, Nur Jahan, Telephone, Train, Unity, Lotus, Lion, Doon, Aarati, Shubh Mangal, Al Wisam, Al Bustan, Alhussam, Blue Bird, City Palace, Necklace, Southern Girl, Taj Mahal Tilla, Bemisal and Indian Farm, among others.

Subsidiaries: As on FY22, the Company has two Subsidiaries viz., KRBL DMCC, Dubai and K B Exports Private Limited, India.

Key Rationale:

-

Leading player in Indian basmati rice sector – KRBL is a fully-integrated rice company with an operational track record of over three decades. Moreover, the company’s promoters have several decades of experience in the basmati rice industry. It is India’s largest exporter of branded basmati rice. The company’s brand “India Gate” is recognised as the world’s no.1 Basmati Brand. KRBL’s agri-business is integrated in nature with presence across the value chain comprising contact farming and seed development, milling of paddy, captive husk-based power generation and processing of by-products. Moreover, a wide distribution network and established client base have enabled KRBL to emerge as one of the leading players in the industry.

-

Expansion – The company’s facilities are suitably located in Punjab, Uttar Pradesh and Haryana, ensuring easy access to the key raw material, paddy, which is procured during the harvest season (October to January). Moreover, these states have numerous other small-to-medium-sized basmati rice milling units, which provide semiprocessed/milled rice to KRBL for its processing facility. The company is on the process of opening three new plants where the first one is situated in Gujarat which is expected to begin production in April 2024. The company has acquired land for its second plant in Karnataka and is looking for land in Madhya Pradesh for its third plant. Total Capex of Rs.250 crs will be spread between the next two financial years.

-

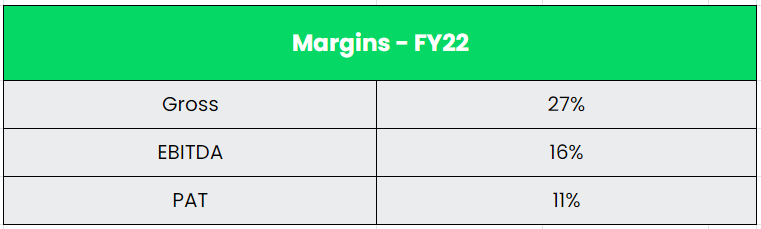

Q3FY23 – The company reported highest ever quarterly revenue of Rs.1536 crs, an increase of 33% YoY in Q3FY23. The revenue growth is supported by both the domestic and exports segment. Segment wise, Domestic business reported a revenue growth of 32% YoY to Rs.998 crs in Q3FY23 and exports business reported a revenue growth of 38% YoY to Rs.523 crs for the same period. The gross margin of the company improved from 20% in Q3FY22 to 28% in Q3FY23. The EBITDA for the company reported a massive 158% YoY growth to Rs.279 crs with a margin of around 18%. The profit after tax of the company had a growth of 180% YoY to Rs.205 crs. Three new regional variants of rice launched in the market namely Sona Masoori, Gobindobhog and Kolam rice.

-

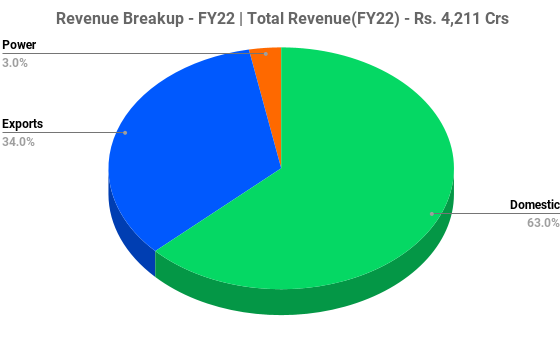

Financial Performance – The company’s inventory position as on Q3FY23 is Rs.4436 crs vs. Rs.3168 crs last year. The inventory position splits into Paddy segment at Rs.2252 crs and Rice segment at Rs.2018 crs. Working capital days increased on account of higher inventory. The company’s revenue and PAT have grown at a CAGR of 10% and 17% between FY12-22. The company’s reserves have grown at a CAGR of 17% between FY17-22. The company’s liquidity position is strong with an overall cash and Investments of ~Rs.1600+ crs with a low debt to equity ratio of 0.03x.

Industry:

India accounts for more than 22% of the world’s rice production through its 48 million hectares of rice plantation area – only 2.4% of the global land. Considered as the staple food for nearly 70% to 75% of the national population, the Indian rice industry is still being largely dominated by unorganised players because of the easy availability of rice through small retail stores. India has been the world’s largest exporter of rice since 2012. Currently, India exports more rice than the combined shipments of the next three largest exporters – Thailand, Vietnam and Pakistan. India’s rice exports have crossed a record $11 billion in 2022-23, an increase of 16% from FY22. The volume of shipment, however, remained around the same level as last year at 22 million tonnes (MT). In FY22, India, which has an around 45% share in global rice trade, exported more than 21 MT of rice valued at $9.6 billion. The increased realisation in rice exports has been achieved despite banning broken rice shipment and the imposition of exports tax of 20% on white rice in India last year. India has shipped $11.14 billion of rice, which includes basmati ($5 billion) and non-basmati ($6.14 billion) during FY23. In terms of volume, the country has exported 4.9 MT of aromatic and long grain basmati and 16.1 MT of non-basmati rice. India annually exports 4.5-5 MT of basmati rice and has an 80% share in the global trade of aromatic rice.

Growth Drivers:

-

India’s branded basmati rice penetration is only at 20% (% of the household penetrated) and the overall basmati rice penetration is at 41%. So, there is a huge room for penetration in the branded Basmati rice segment.

-

Provision of Rs.450 crs has been made for the Digital Agriculture Mission started by the Government, and about Rs.600 crs allocated for the promotion of Agriculture sector through technology.

-

An increase in demand for personal care and home care products along with rapid urbanisation, higher income levels, and evolving preferences is expected to drive growth in surfactants consumption.

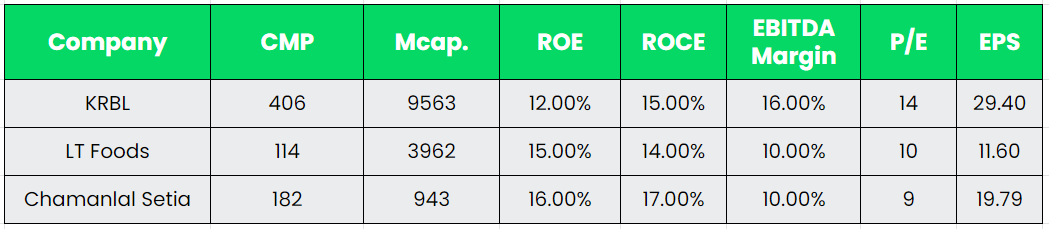

Competitors: Lt Foods Ltd, Chaman Lal Setia Ltd, Kohinoor, etc.

Peer Analysis:

Amongst peers, KRBL has the best operating margin profile backed by its strong brand presence. The balance sheet of the KRBL is strong than its peers in terms of debt profile and reserves growth. We took TTM EPS and P/E for comparison.

Outlook:

KRBL has expanded outlet penetration by 15% YoY to reach a numeric distribution of 39.2%, and has expanded its distributor count by 40% to take the number to an upward of 700-plus dealers and distributors. The company procured around 40% higher basmati paddy this year at a competitive price. Average price of basmati paddy procurement from last year is 15% higher. KRBL is targeting 20%-25% of the HoReCa (Hotels, Restaurants & Café) segment, and is looking at doubling its revenues in this segment in the next two years. It is also developing pesticide-free and resistance-free commodity varieties, which will help capture the European and American markets, and are expected to be available in FY24. The Management highlighted that the market value will always be 15-20% higher than the procured value of the inventory. Based on that, the market value of the company’s inventory will be around Rs.5000 crs. In the exports business, KRBL has shortlisted 2-3 distributors in Saudi Arabia, and hopes to finalize one of them in a very short period. The board hinted that they may discuss on rewarding the shareholders through a dividend or Buyback in the upcoming meeting.

Valuation:

The company has been able to maintain sales and realization growth momentum and is expected to continue to do so on the back of brand strength, market reach, robust selling & distribution network, established presence in Middle-East, ample capacity and right product-mix. We recommend a BUY rating in the stock with the target price (TP) of Rs.490, 16x FY25E EPS.

Risks:

- Regulatory Risk – The company is exposed to the changes in the trade policies of key importing countries, which can impact export revenues. The company is also exposed to the changes in Government regulations, as witnessed recently like the ban on export of broken rice and levy of 20% duty on some varieties of non-basmati rice.

- Climate Risk – Given its operations in the agricultural industry, the company is highly exposed to climate change risk which result in the bad or improper monsoons.

- **Competitive Risk –**The basmati rice industry is highly fragmented and is marked by the presence of numerous organized and unorganized players. This intensifies competition and limits the pricing flexibility of the industry participants. However, KRBL benefits to an extent because of its strong brand presence.

3 Likes

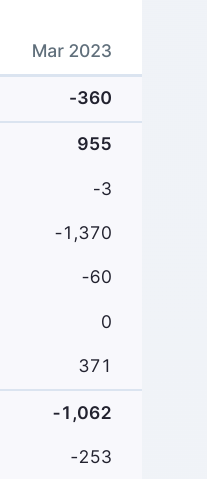

Can you someone help me understand why the Cashflow from Operations went negative this year? Was there an inventory write off?

they have added raw material inventory rice this year by big amount…

1 Like

Q4FY23 Concall notes:

• Key export destinations: UAE - 532 crores (includes 375 crores unbranded), Saudi Arabia - 414 crores, China - 242 crores, Australia - 117 crores.

• Strong domestic business momentum:

o India full year revenue grew at 26% in value to close at INR 3,335 crores. - The year marked a new high for KRBL with our portfolio crossing a household penetration of 1 crores households landmark with an 11.5% increase against the package basmati penetration growth rate of only 2.5%

o Volume Market share: 32.5% in traditional trade, while Modern Trade registered a highest ever market share of 58% in the quarter.

o Unity brand stands at INR 750 crores+ in the KRBL portfolio with a 50% growth over last year.

o HoReCa business with a healthy 28% volume growth in the full year (GST rationalization measure implemented from mid of the financial year has given the strong tailwind)

o This year, company has expanded its distribution network quite aggressively, growing at 40%, to reach a 750-plus dealers and distributors. And on the outlet front, the current penetration of package basmati in India is about 7 lakh outlets. And as a brand, KRBL is available in about 3.3 lakh outlets.

• Regional rice: Anchored under our master brand India Gate - Sona Masoori, Govind Bhog and Kolam rice have been launched in the market and are garnering good response. We have already crossed the milestone mark of INR 100 crores sales in the financial year 2023 in the regional rice category.

Our total addressable market has increased from INR 15,000 crores to INR 35,000 crores with our foray into regional rices.

• Loose basmati rice which contributes close to 65% of the total consumption of basmati in India. This presents a huge headroom for growth for KRBL in the domestic business.

• Basmati Standards by FSSAI: One other important tailwind expected to come for our business is the introduction of the new basmati standards by FSSAI with effect from 1st August 2023. Over the years, due to mass commercialization, there is a significant amount of adulterated basmati available in trade, making the prime objective of this regulation to safeguard the integrity of the grain and maintain an authenticity of flavour and taste. This resolution will have a number of positive impacts within domestic business scenario. First, increased literacy within the trade and subsequently consumer on basmati quality. Second, eradication of players indulging in unfair business as basmati adulteration practices, leading to consolidation of market share amongst top branded players. And third, an accelerated shift from loose and unregulated basmati to packaged and regulated basmati. We see this as a watershed moment for the industry and expect this to be a significant growth driver in the coming years.

• Lower export sales: Total value of goods dispatched during the year, but their revenue yet to be recognized pending receipt of payment at the end of the quarter was at 441 crores. This is the number as of March 31, 2023 as against 216 crores as of March 2022. A significant portion of this is expected to be recognized as revenue in Q1 FY 2024. We recognize revenue only once the payments are received.

Bulk export sales resulting in lumpy sales nos: Part of our exports also include bulk exports. That tends to be lumpy. So you may have quarters in which there is significant bulk exports and then you may have a quarter like Q4, where it doesn’t happen. So first, on a quarter-on-quarter basis, that’s primarily the reason why you will see export revenue moving. On an annual basis, we do about INR800 -INR900 crores of bulk exports.

• Saudi Market: HoReCa Distributor is still not done, but we are expecting that it will be done in the next 1 or 2 quarters. – Better sales expected this FY – FY24 expecting to get back to 1000cr sales.

• Modern Trade vs General Trade: Our Modern Trade and e-commerce channel actually for us is more profitable if I compare the overall P&L account because expenses are quite less compared to general trade. So in general trade, we will have a lot of manpower and other expenses to cater to that wide spectrum of retailers, when Modern Trade because of the consolidation of supply chain and other effects, our cost tends to be lower. Also, Modern Trade and e-commerce, this category of staples is I would say crowd-pullers or footfall drivers really. So these channels also invest heavily on these particular categories. So the cost of doing business to sum it up is lower compared to general trade.

• Aged rice vs new crop effect on margins: So between our Q3 and Q4, there is a part of sales that is what we call it aged rice or aged rice sale. So obviously, that inventory is what we carried from the year previous to that. And our inventory cost would be quite stagnant on that. But there’s a big portion of sales that happened in Q3 and Q4, which is new crop, which is the parboiled rice and the steam rice. For those – because it’s new crop and as you know, the crop season this year, the prices were quite high. So our input costs on the raw material was quite high. So that would be an effect between Q3 and Q4 that you see would be an impact on margins.

• Ebitda Margins: One of these factors that causes variance is the quantum of bulk sales, especially export sales, where we have limited predictability in terms of when that revenue will get recognized. However, overall, what we aim for is that during the year, we maintain the margin in the 17% to 18% trajectory. So the EBITDA margin range that we look at is a minimum of 17% to 18%. So that’s what we are looking to achieve through the year.

• Split of business between basmati and non-basmati in volume terms: Domestic branded basmati - 370,000 tons. Domestic Non-basmati branded - 21,000 tons. Exports basmati branded - 88,000 tons, Exports non-basmati - 5,000 tons.

8 Likes

I recently came across this bottle in a supermarket in USA. This is like saying Champagne made in Italy. I thought that Basmati has a GI tag and can only be used by rice growers in

India and Pakistan. I dont know much about this, but looks like a violation when they use the word Basmati.

1 Like

The story behind this:

Excerpts:

In the mid-70s, the prices of Basmati rice in India had spiralled due to increasing demand from West Asia, resulting in a clamour in India to ban its export. The Indira Gandhi government succumbed. But a couple of American entrepreneurs wasted no time in importing Basmati seeds and growing the rice in climatic conditions similar to Dehra Dun’s.

The pioneer in US-grown Basmati is the Texmati farm located 40 miles from Houston. According to the owner, Don Braddock, he started marketing his brand in 1977 and business has since grown several-fold. Today, Texmati can be found in some major food chain-stores, selling at nearly twice the price of Basmati available in Indian grocery stores.

To make matters worse for the Indian importer, the US Food and Drug Administration (FDA) has put India-grown Basmati on the blacklist after a series of wounding rejections on the ground that the rice had either too much “foreign element” or enough husk to be branded paddy instead of grain.

FYI: Year of this above article is 1989.

For the current status:

Excerpts:

A re-examination case was filed in April 2000. Soon afterwards, RiceTec withdrew its basmati-like claims for its brand Texmati.

Later, the US Patent Office passed a judgment that “a substantial question of patentability has been raised in respect of the remaining claims” of RiceTec.

RiceTec later withdrew the crucial patent claims and the threat to the export of basmati rice lines from India was averted. India also learnt its lesson and introduced sui generis systems – i.e. ones developed to suit each country’s needs and priorities – to avoid future challenges

7 Likes

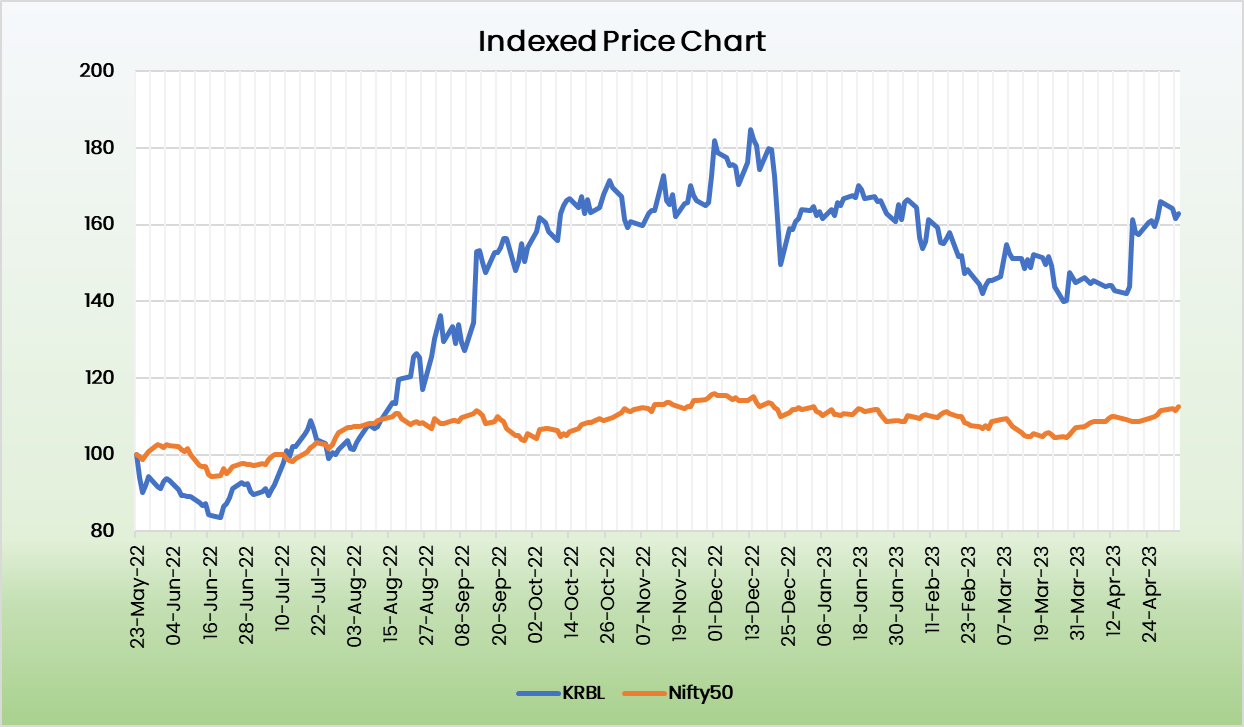

Guys any idea why Lt foods has rallied almost 60% but Krbl who is the segment leader and has always demanded premium valuation compared to Lt foods now trades at the same valuation as LT foods now.Any reason why krbl hasn’t participated in the market rally given rice prices are increasing all around World and there is very strong demand for rice given floods all around the world.

Is there something which the Big fish are seeing and the retailers aren’t?

1 Like

I doubt KRBL would have much impact from this unlike its Peers.

" India has banned the export of non-basmati white rice due to a delayed monsoon and heavy rainfall damaging crops, raising concerns about production shortfall."

Both LT foods and krbl are exporting basmati rice so they both are not effected by this news .Moreover krbl is the biggest exporter and it has procured record levels of inventory last year ,combined with the fact that it doesn’t need to borrow money to buy rice like Lt foods.

1 Like

I think its because of the sub optimal q4 results. If Q1 results are upto the mark, then it should go up as well

1 Like

Few reasons I think…

- Overhang of the allegations of involvement in a defence related wrongdoing.

- Growth rate of KRBL in revenues and profits has been less as compared to LT Foods.

- One reasons for KRBL’s sub-optimal growth could also be the delay in appointing distributor for one of the Middle East countries.

- LT Foods has improved its debt:equity ratio over the last few years.

- Because of better growth and D:E ratio, there has been a good rerating of the PE multiple in case of LT Foods.

Disc: invested

2 Likes

My view is other way around. Its not KRBL lost its premium, LT Foods is gaining its premium. If you see the profits and cashflows reported by LT Foods, is much consistent. They gradually evolved into products other than rice and even rice, they have differentiated approach in different geographies and all are throwing good money. And it is trading at a valuation as if they are some broke company. Whereas KRBL has some one-off quarters with some reasons every now and then. So market may start giving such premium to LT Foods.

Agree to @pranavpallod12 , that may be because of Q4, KRBL price may be stagnant. This may move little higher if they post spectacular results in Q1 (Because as per management, they sales which supposed to get recognized in Q4 will be recognized in Q1, then we should expect much higher profit than regular quarters)

8 Likes

I also believe that it might be due to Q4 performance where there was delay in recognising revenue but i personally believe that krbl given it’s margin which are always higher then Lt foods and brand presence would always trade at a significant premium .Let’s see what the market has in store for us,I just hope there is no major big surprise in the coming quarters.Times like these are when commodity stocks can make investors supernormal profits.

And when there is panic, it will be having ripple effect in all category…And it’s LTfoods which caters Western countries…

Non-Basmati Business Revenue Details

| Year | Revenue split (non-basmati rice) | Export value (non-basmati rice) |

|---|---|---|

| FY2021 | 1496 | 1206 |

| FY2022 | 1837 | 1531 |

Good detailed artical sir but what do u think can be d effect after India has banned exports to other countries

KRBL to consider buyback of the shares on Aug 10.

Yet to know which method they will follow to do the buyback…In my personal opinion they will go for open market purchase with price cap at 550/share…![]()

3 Likes