Any idea, how the decline in production of Rice impacts the business of KRBL and LT foods?

Decline in rice production will result in higher prices of rice. Infact because of the above news, rice prices have already increased by 30% in the last few months. This generally reduces margins of krbl. But the management on conference call yesterday mentioned that price of rice in international market is very high so they will Infact be able to maintain the margins. They will also increase the sales by 600 cr (in fy23) due to new dealer they arranged in Saudi.

The commentary is bullish and I believe they are correct in their forecast. But the market is not appreciative of the stock price. Can’t say exactly why, but I guess probably because no body wants to take even a remote chance of India banning export of rice due to global food situation.

- Jatin

5 Likes

KRBL is primarily selling Basmati rice. Basmati rice goes through 1-2 years aging process. As such rice bought today will be sold in FY25 at the earliest. Hence its margins will depend on prices prevailing at the time. Currently if there is a drop in rice output and price goes up, its inventory (though KRBL inventory has been dropping for some time now, from 3129 crs in FY19 to 2304 crs today) will gain in value and the company will see higher margins. Even if there is a ban on export of rice, Basmati rice is unlikely to be part of it, as it is more expensive and not really part of govt buying program under MSP.

4 Likes

Q1FY23 CONCALL NOTES:

•SALES GROWTH TO CONTINUE: We have an excellent order book and our first quarter results are already with you. Both domestic as well as exports sales are showing remarkable progress and this growth trajectory will continue in the times to come.

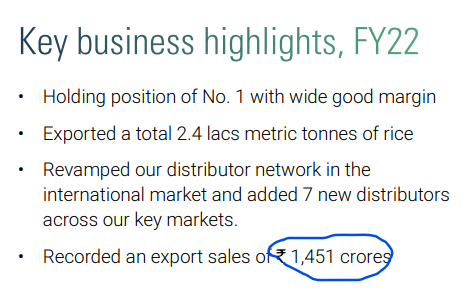

• SAUDI MARKET: In Saudi Arabia, we are expecting with the current arrangement that our top line will increase by minimum Rs. 300 to 400 crores extra over the past performance. This Rs. 400 crores definitely will add up in the top line, besides we are yet to decide for another distributor for HoReCa segment and general trade, which we believe we would be finalizing somewhere within September-October and that will add, in this financial year, to about Rs. 300 crores. So, we are expecting Rs. 700 crores jump in the Saudi top line itself this year.

• IRAN MARKET: In FY23, definitely we will have a respectable share in Iran because a good channel has been emerged and that channel is a legal channel to export to Iran. We are quite confident that our share in the next 3 quarters will be quite impressive as far as Iran shipments are concerned.

• SPILLOVER OF REVENUE TO Q2: In the current quarter, Saudi numbers are there, but there were certain payments which could not come. So, they are not reflecting. Otherwise, this number would have increased by another Rs. 70-80 crore.

Yes, there is a spillover of other countries, which I’ll not like to discuss, but there is a spillover. The total spillover may be up to the tune of Rs. 150 crores.

• BASMATI PADDY SCENARIO: When we talk about rice, we should keep in mind that there are two different commodities, i.e., basmati rice and non-basmati rice. There is no linkage whatsoever between the two as far as production, price and markets are concerned.

As regards basmati rice, the sowing is good and according to the field survey, the production of basmati rice will increase by 25% in crop year 2022-23. This is mainly due to high prices witnessed by the farmer last year. Recently, we witnessed that the early crop which comes in the month of July-August that is 1509 basmati rice fetched a price of Rs. 32,000 to 33,000 per metric tonnes giving the farmer a revenue of Rs. 70,000 per acre whereas non-basmati with the new MSP will fetch the farmer around 62,000 per acre, which certifies that the price of basmati paddy, in spite of 25% hike in production, will still remain firm and the export prices will also fetch good prices

• FRIEGHT AND LOGISTICS CHALLENGES ARE LARGLY BEHIND: We are now starting to see the situation ease out with freight levels coming down and availability of containers, labor, transportation, and warehousing space are considerably improved. There is no impediment as far as logistics are concerned except that freight rates though they have come down but still are on the higher side. But it does not affect to the industry anymore since the freight charges are built up in the pricing.

• NEWER PESTICIDE COMPLIANT BASMATI VARIANTS: This is to confirm that during this Kharif Season, IARI has distributed seeds of 3 new varieties of basmati rice which possess inbuilt resistance to bacterial blight and blast disease, as I had mentioned you last year as well. IARI has supplied seeds to farmers of improved 1487, 1885, and 1886 rice varieties in which 2 genes have been inserted, which could withstand the attack of bacterial blight and blast disease that adversely impact the crop yield. Three varieties would gradually replace the existing basmati rice varieties of 1121, 1509, and 1401 which are cultivated in more than 90% of about 2 million hectares of aromatic and long-grain rice grown areas. The above program of IARI will multiply the seeds this year which will result into a commercial crop during the crop year 2023-24. This will give a big leap to basmati exports practically in the EU and the USA, including few countries in the Arab world. Though the restriction of pesticide residue is nothing but a non-tariff barrier, the challenge which was accepted by the Indian exporters and now we have come up with the new varieties to ensure that Indian basmati rice is fully compliant.

Q: We are not that good in the US market. And you said with new varieties, the pesticide residue level will be complied. So, what would be our strategy for the US market? Anil Kumar Mittal: Definitely, not this year but next year, when the commercial crop comes of compliant rice, definitely our share will increase not only in America but in many other markets where there is an obstacle of being non-compliant. I am quite sure that we will do much better in these countries when the compliant rice is available in abundance.

• UNITY BRAND: Unity brand has grown by more than 100% to Rs. 150 crores in quarterly revenue. Consumer pack continues to grow in healthy double digits year over year in volume terms. Unity brand has historically been primarily a HoReCa brand. More than 85% of revenues still come from the HoReCa segment for that brand.

• GST ON UNBRANDED PRODUCTS: And I would like to add one thing due to the recent GST notification where the taxability on the branded and unbranded has become equal and we are now at a level playing field. We used to pay 5% tax while others chose not to pay. Now I have changed my packing from Unity 25 kg to 30 kg. As per Government notification, above 25 kg, there is no tax for everybody whether it is a registered brand or a non-registered brand. I hope, with this, our HoReCa sales will improve very much.

• Overall, rice sales realization increased by 13% while volume increased by 7% over the Q1 FY22.

• We must be following first in, first out. (FIFO), so by that method, you would have paddy prices over the last season as well? Ashish Jain: No, we don’t follow FIFO. In our case, the fixed products are valued on a net realization basis while the raw material is at cost.

7 Likes

Things are certainly coming together quite well for KRBL

- Income Tax issue is resolved

- Saudi Market issue (Distributor issue) is resolved.

- Iran market Issue showing positive development (sales through legal channel).

- Domestic market showing robust growth.

- Pesticide norm compliant basmati could open up multiple big new export markets.

- GST on unbranded products could provide another boost in domestic sales.

- The planned capex for Regional rice products offer great potential as well.

Only one issue now remains - ED case against Joint MD Anoop Kumar Gupta

A case which is not related to business operations themselves.

So, all in all, the KRBL story is shaping up quite well for the future.

DISCLOSURE: INVESTED

8 Likes

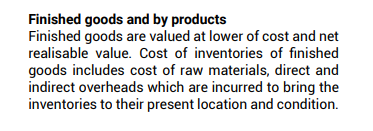

There is some discrepancy in inventory valuation method: the CFO says finished (I presume ‘fixed’ is a typo here) goods are valued at net realisable value while the notes to accounts says it is lower of cost or net realisable value.

As per concall:

As per AR:

In fact he repeats the valuation of FG at NRV later in the concall again.

If it is indeed NRV, the notes to accounts are incorrect to that extent. Also when a company values FG at NRV they are in fact showing profits ahead of actual sales. And the sales may happen at a lower price later. Hardly any company does this. But if KRBL is doing this, it would certainly be aggressive accounting.

4 Likes

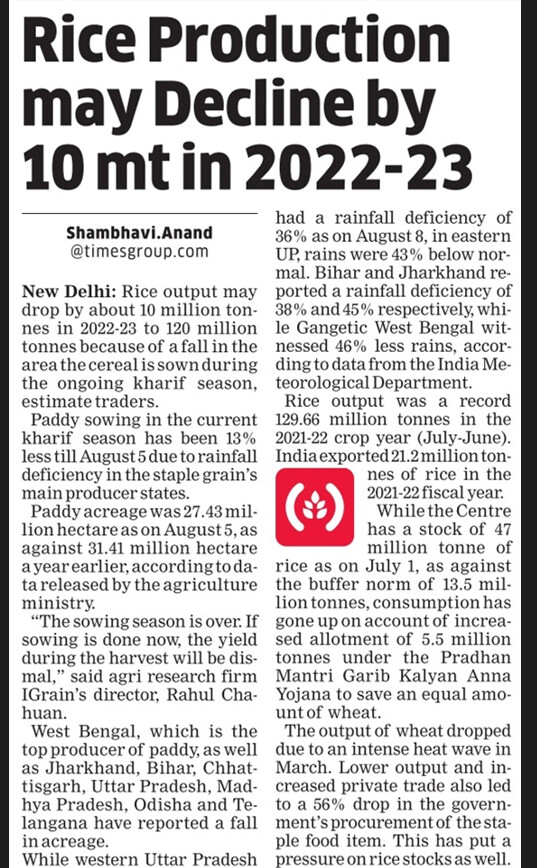

Centre imposes 20% duty on rice exports of various grades

The government has excluded parboiled and basmati rice from the export duty, but white and brown rice will draw the duty, which accounts for more than 60% of India’s exports, said B.V. Krishna Rao, president of the All India Rice Exporters Association.

Source:

Just to provide some context from Annual Reports of both listed major exporters. KRBL and LT Foods

KRBL -

I think export value for non-basmati would not be more than Rs. 500 Cr. which is about 10% of full year revenue. Given this is coming in Sep. I expect revenue impact this year of about Rs. 250 Cr.

LT Foods -

3 Likes

Not necessarily, they might actually be over-reporting their total expenses because of this, depending on how the price of paddy moves.

Scenario 1

If paddy price today is 100, but 6 months later it goes to 200, their stated COGS will be 150 (assuming equal volume purchased at both prices) however actual COGS will be 100, at least for the aged rice.

Scenario 2

If paddy price falls from 100 to 50, their stated COGS will be 75 however actual COGS will be 100, at least for the aged variety.

Looking at the movement in margins along with price of paddy at time of procurement will shed more light. Can someone share a source where procurement prices can be obtained? The company has only intermittently shared their procurement prices in concalls

3 Likes

With the average realizations in Basmati rice per kg steadily increasing, it’s reaching a high point where it was close to 10 years ago.

over the past year the value of basmati rice exports has been steadily increasing too, which are good signs for this space.

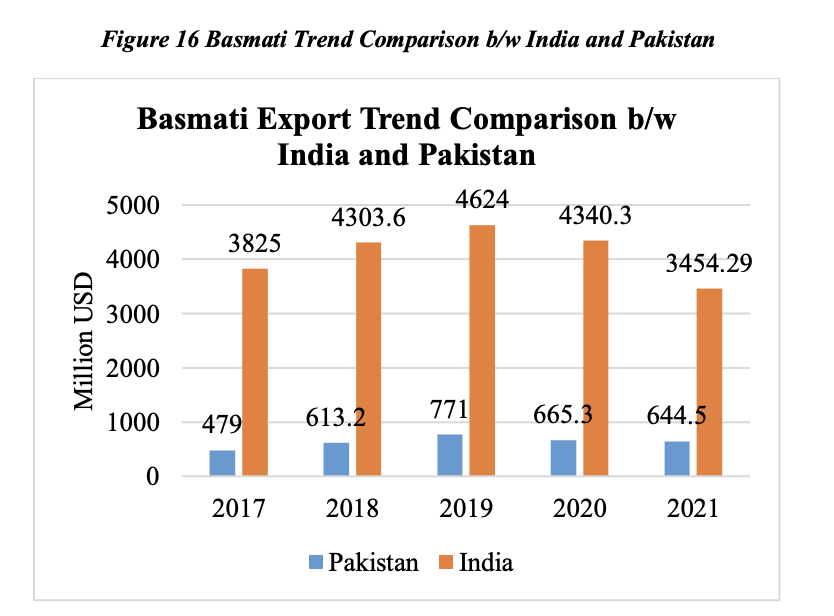

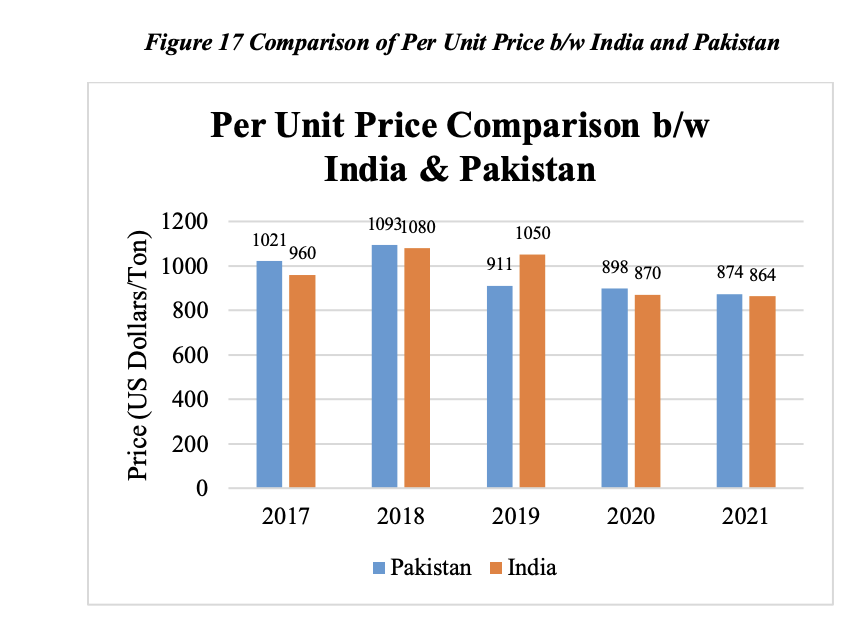

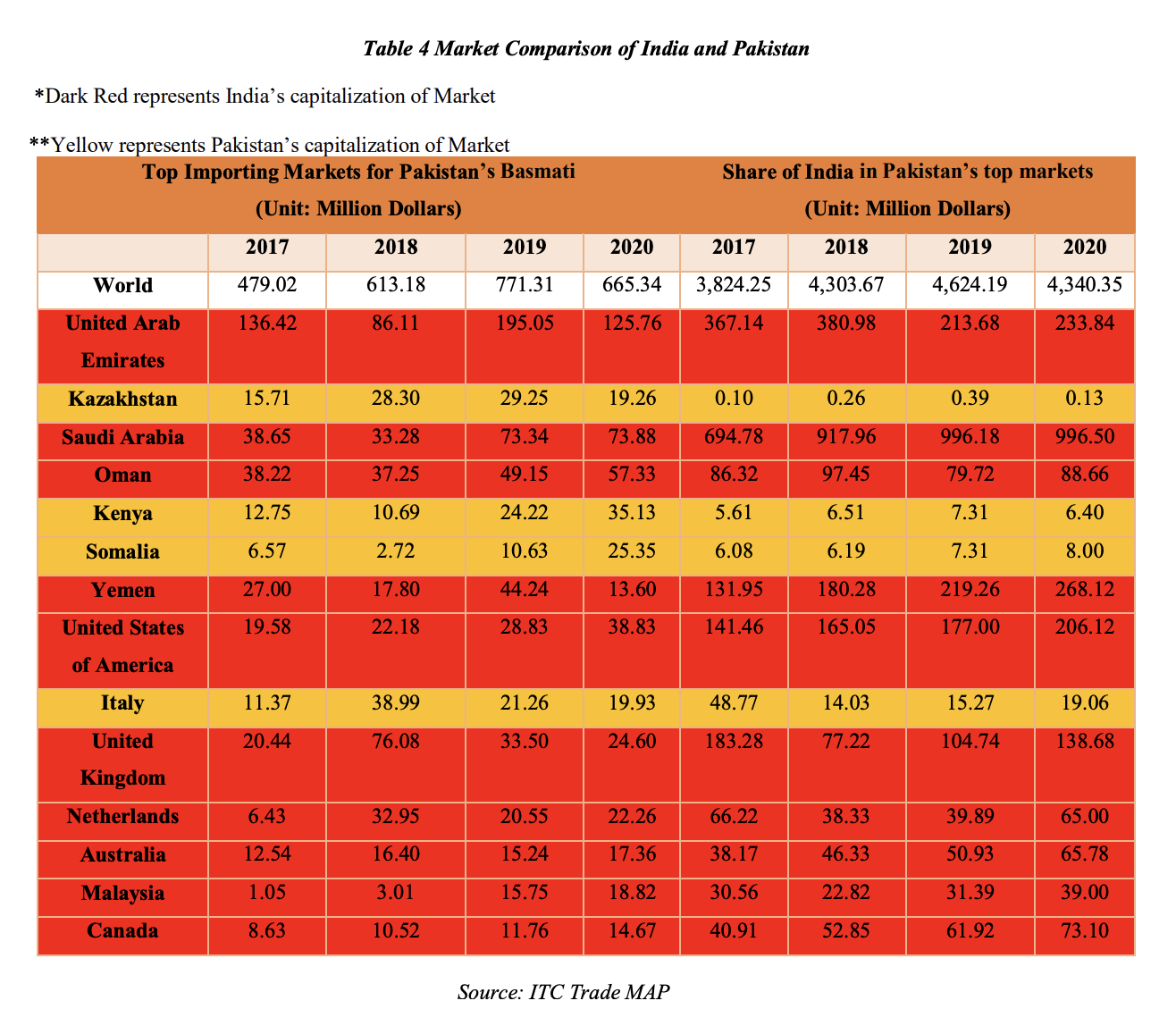

Unfortunately with floods in Pakistan, there might be an opportunity for India to grasp some market share in the near term.I had come across this document that shared the market size b/w the two countries. source: link

A few interesting points to note from this document in regards to Basmati:

- The top importing markets for Pakistan’s Basmati include UAE, Kazakhstan, KSA, Oman, Kenya

and Somalia. - Pakistan and India are the top producers of Basmati. They together account for 90% of total

exports. In 2021, 0.737 million tons of Basmati rice was exported to UAE, Saudi Arabia, Oman,

Yemen, China, UK, Kazakhstan, USA and Kenya at an average price of $900/ton. Pakistan still

had a surplus quantity of 0.84 million tons. - The top importing markets for Basmati rice in the world include European Union, Middle East,

KSA, Iran, USA, UK, Belgium, Yemen, Spain, Italy and Qatar. - Price trends over the past 5 years:

5. Pakistan’s market share in UAE has also squeezed as compared to pre-pandemic era. Pakistan’s share in Kazakhastan, Kenya, Somalia, and Italy is increasing. These markets are promising for Pakistan as India has not captured these markets as of yet. < Opportunity for indian players to grab some short term opportunity here >

- Overall market:

disc: Invested as a techno funda bet, no trades in the last 30 days. (https://invst.ly/z2muh)

16 Likes

Wearing my product management lens ![]() and doing a quick back of the tissue paper

and doing a quick back of the tissue paper ![]() calculation -

calculation -

The total export basmati market size of KRBL (& likes)

= Total Meals when basmati is consumed

= Avg. annual meals per person * population of basmati importing nations

Common sense in my mind says:

- Avg. Annual meals per person - roughly remains constant unless people create a new staple way of eating basmati or invent a new popular wildly addictive drink out of it

- Population growth of these nations - won’t explode, gradual growth maybe, nothing that can have a lollapalooza effect

- These importing nations - too are a constant (no other country imports basmati)

- Rate /kg - is almost already is at a peak (Thanks @ganeshrpl), can’t practically go beyond a point

The likely possibilities of export sales growth can be:

- Tap into nations not yet present in (Kenya, Italy…etc.) - competition from Pak will be there, can’t be zero

- Convert non-basmati nations into basmati nations & make them addicted to it (make US, Australia, Germany, France, etc. ) - possible not probable, surely not within an year

- A newer way of basmati consumption begins - becomes animal feed, etc. ( very unlikely)

So what really are the themes for KRBL (& likes ) that will really get them their re-rating -

- Brand Extension (LT is ahead here…with Organic, Convenience products)

- Portfolio Expansion

- Increase of Non Basmati Revenue

- Rising Domestic Consumption of Branded Rice

What could be the other possible themes?

7 Likes

Good analysis, to figure out secular themes… but the reality of world presents short term opportunities too, especially for a cyclical industry like this. Like this year, global food shortages (due to war in the Ukraine-Russia wheat belt), floods in Pakistan, drought in China creating supply-side windfall opportunities resulting in price increases. This will translate to windfall gains which can be reinvested in Brand Extensions, Portfolio expansions which you mentioned, to smoothen out the cyclicality in the long term

3 Likes

Domestic consumption should be the main theme along with export market of Iran…KRBL is fully integrated player from seed level itself…Great brand recall will help KRBL to get FMCG valuations over a decade time.

2 Likes

Could you please share more details on how KRBL is integrated from the seed level?

U can also go through their concalls for more details. They are coming up with new varity of basmati which requires minimum pesticides requirements so that KRBL can explore market such as Europe and some gulf countries as well as USA where pesticides residual in rice is big hurdle for Indian basmati exporters.

3 Likes

L t foods results are out margins are same but the topline has gone up by almost 7% QoQ and 30% YOY ,the net profit remains the same due to higher interest cost ,If krbl is able to give a similar growth it might post it’s highest ever topline .Results are on nov 11 which is friday and maybe posted after market hours so i am little skeptical about that but let’s hope for the best.

Disc :Invested

Just random musing, does oil prices have have any co-relation to KRBL revenue/profits ? As it seems it basmati rice exports to middle-east (UAE, KSA, Iran(I assume it doesn’t export to Iran)) whose economies are pretty oil price sensitive ?

1 Like

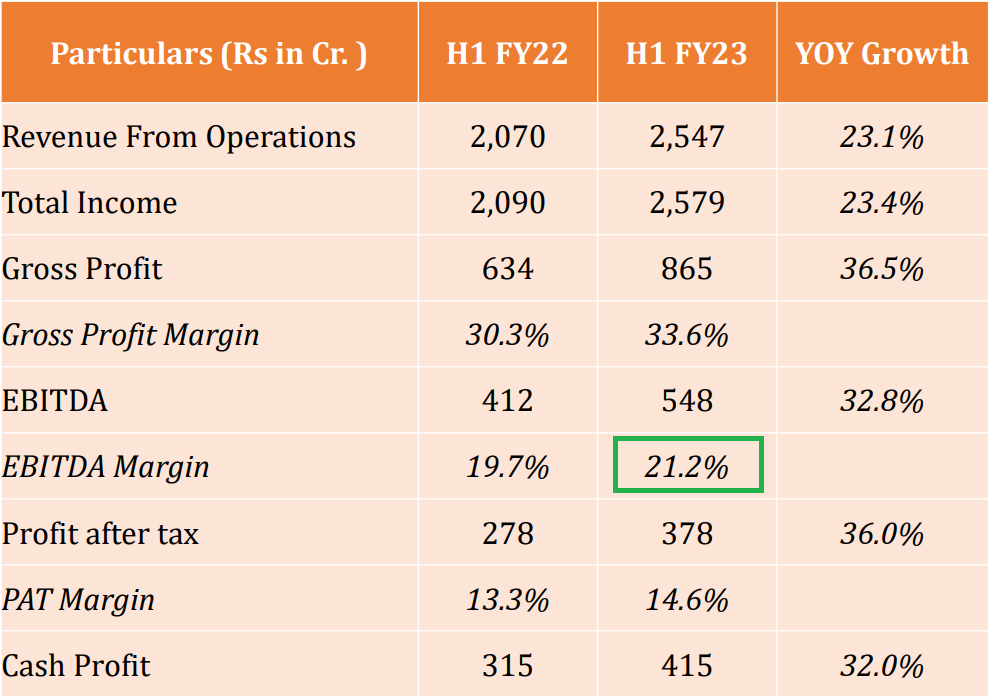

Wonderful set of numbers from KRBL even beating my estimation for Q2FY23. Very Strong growth from Export as mentioned by management in last concall. I won’t be surprise if this counter even cross all time high before Q3FY23 result as Domestic sales should also start contributing more due to Festival seasons.

Key Takeaway from Q2FY23:

- Strong Q2FY23 Gross Profit margin & EBIDTA margin at 34.5% and 22.8% respectively

- Basmati realization increase (42% over Q2FY22) partially offset by 27% increase in rice input cost over the same period, resulting in improvement in Gross Margin.

- Revenue growth witnessed in both Domestic and Export Segments.

- Q2FY23 revenue growth mainly driven by Export Sales – 105% y-o-y growth.

- Total inventory as on 30th Sep’22 is 2,054 Cr

More Details:

Happy Investing,

Karthik

Disc: I am invested in this counter from long time around 20 Rs. So my views can be biased.

7 Likes

KRBL q2 fy 23 investor presentation.

Most eye catching thing besides the earnings growth has been net cash of 1600 crores on balance sheet. An eye popping number in this kind of business where a lot of capital is tied up in inventory because rice needs ageing.

krbl q2 fy 23 presentation.pdf (2.2 MB)

11 Likes

I think large cash accruals in BL would be largely because of IT refund they would had received .

With lined up capex + high paddy procurement expected this year I believe cash would get consumed and by FY end debt would come down marginally compared to last FY