As far as I read, even if Supreme Court rules against Balsharafs, KRBL’s business should not directly be effected since the case has nothing really to do with KRBL’s business. Can anybody following the ED case comment on my assessment ?

Results out -

disappointing numbers from a topline perspective, will have to see the mgmts. commentary.

1 Like

Management had already guided that India business was in slump and export business did phenomenally well. Increase in margins is visible.

Disc. - Invested

1 Like

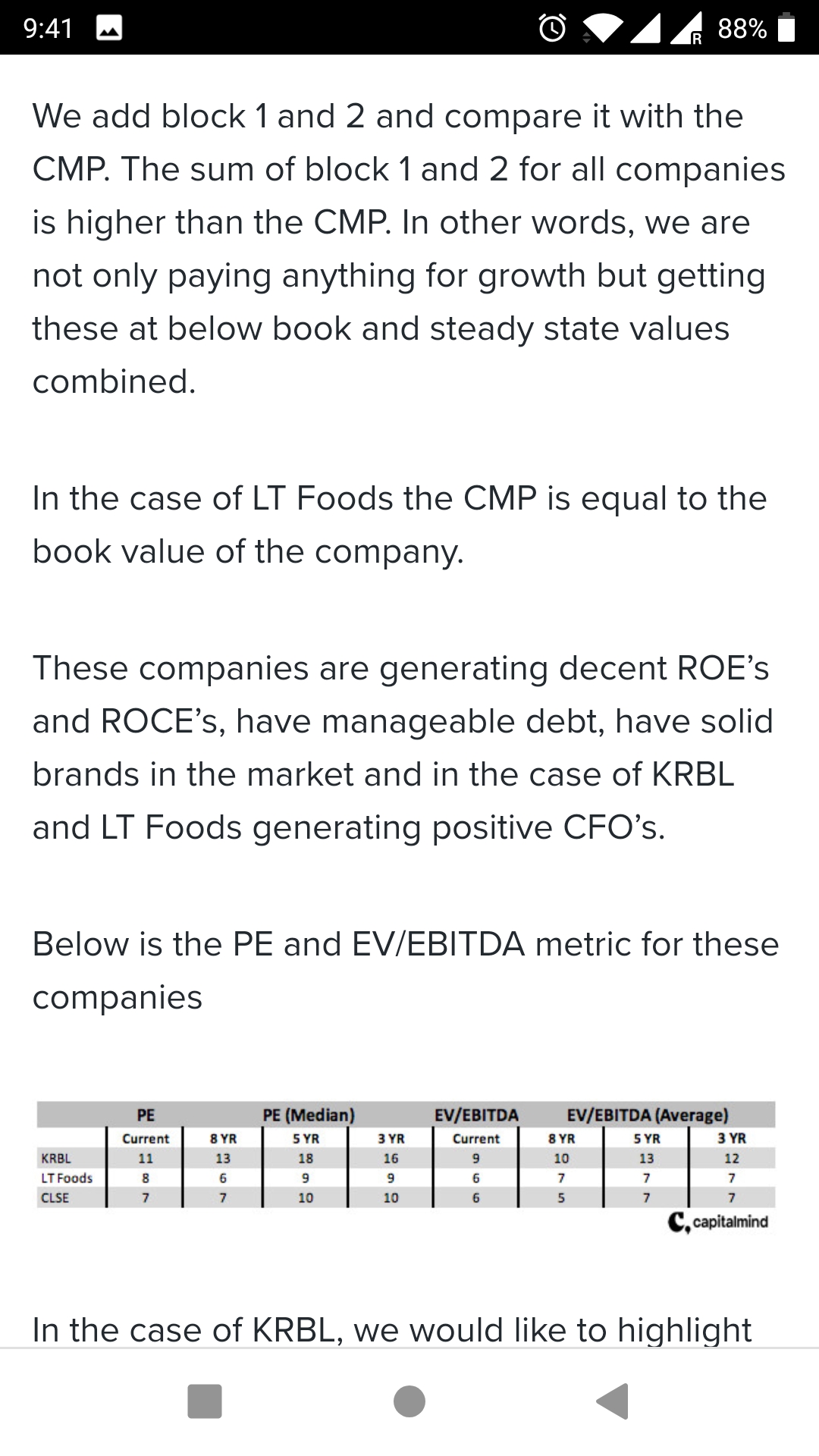

LT Foods:

KRBL:

Q1FY21 Q4FY20 Q1FY20

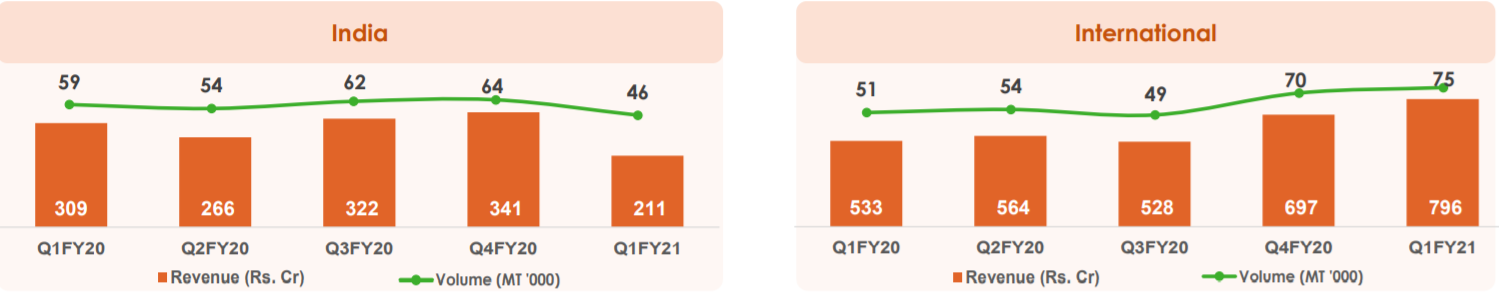

The domestic business: the fall % is same between LT Foods & KRBL. The export segment, LT Food did well compared to KRBL YoY.

LT Foods is diversifying into Ready To Cook Basmati rice, organic staples etc. Not sure why KRBL is not interested in this segment. The Ready to Cook Basmati would probably give tough competition to Maggi, Yippee etc.

Disc: Invested in KRBL

1 Like

If i am not mistaken, the KRBL Board has given in principal approval to demerge the power / energy business. At least they have started the ball rolling and has appointed KPMG for evaluating this hive-off. Hopefully, we can expect the demerger to happen, however, it would be really helpful to understand the timeframe by which the management is expecting to complete the demerger? I am expecting some clarity in the ensuing concall. Needless to add, the hive-off would be improve the ROCE and may help the standalone consumer/ rice business to fetch higher valuation.

I’m also expecting clarity in terms what happened in the gone quarter for KRBL to record lower sales / pbt vis-a-vis DAAWAT / LT Foods’ stellar results. In the concall, hopefully the management might be questioned on all these fronts, as KRBL being the market leader and how can it post such dismal numbers when your competitors have posted excellent results

Having said that, we should not forget the margin expansion that happened this quarter for KRBL. We need to see, is this one-off or something which can be assumed on a going forward basis as the basamati rices are seeing a demand / price uptick

Disclosure: Invested in both KRBL and LT Foods for a while

3 Likes

Just finished the conference call:

- Fall in sales of 350 crore this qtr because of labour issues at the Kandla port, which should be compensated in the coming qtr

- Why this didn’t impact competition - They use rice containers (somehow different trade)

- Horeca segment sales stay impacted and will be normalized only after Covid19(Hotel/Restaurant/Marriages activity)

- Energy business might be set as a separate subsidiary (this would take its own due course of time and will happen only if KRBL can transfer power contracts to new subsidiary without any renegotiation with govt, current rates are lower than executed contracts). No plan to sell.

On a high level:

Guidance of 5k crore stays(may be 100-200 cr lower)

Ebidta should stay higher - inline with current qtr

16 Likes

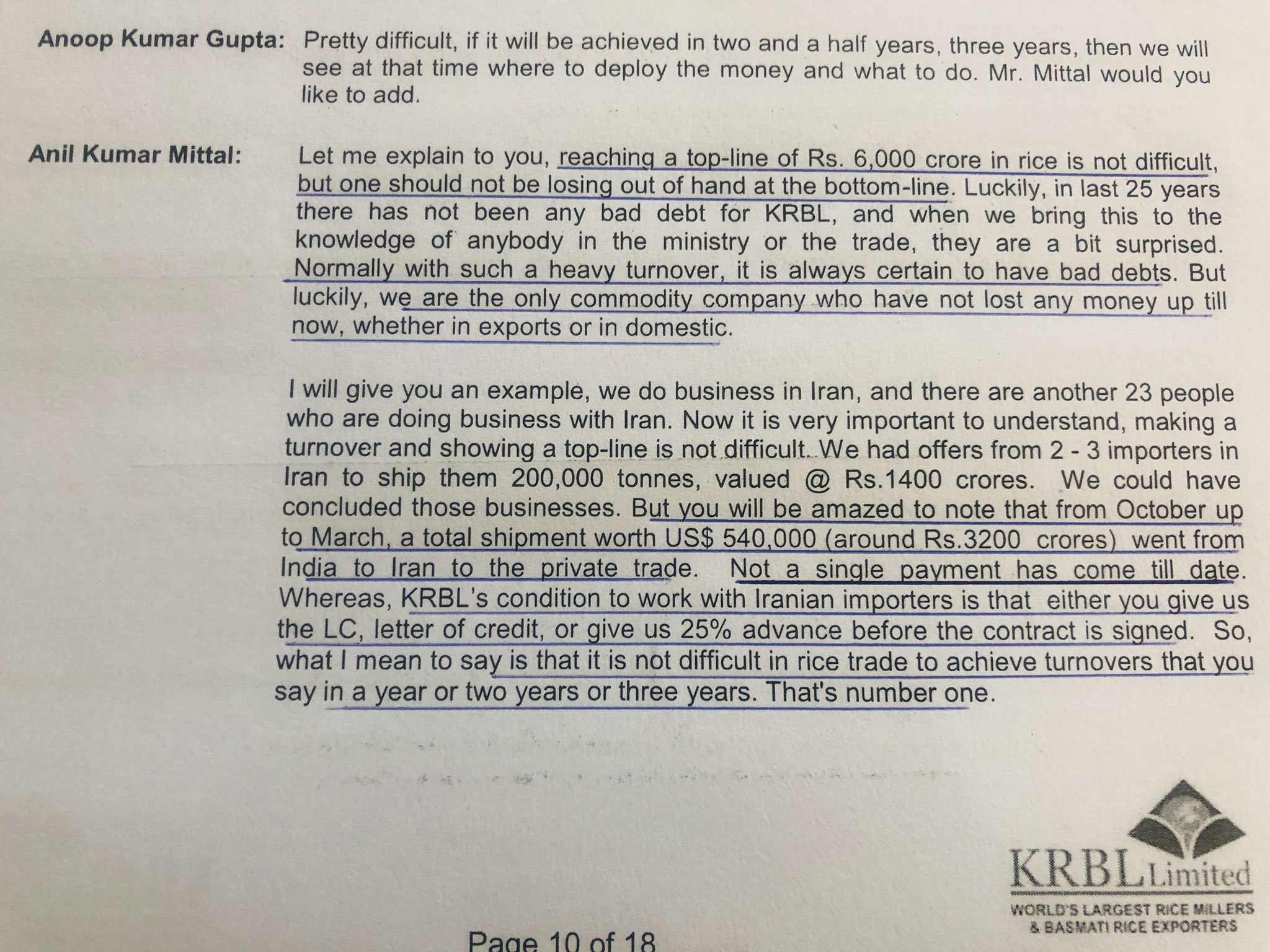

USD 540,000 is definitely not Rs 3200 cr. Error in transcribing?

1 Like

I think USD 540000 is wrong as the figure appears too low for Iran import from India for 6 months

Recent media coverage, talks of growth split of expected mid-term target of 8kcr:

- Focus on increasing market share in USA and Europe

- Domestic focus with launch of non-basmati rice(regional) and rice atta, idli rava, ragi flour, millet and gram flour

- Higher contribution from healthier rice segment

(Disc - Invested)

2 Likes

Q1FY21 call. Notes re-organized

-

Higher gross margin and reduced WC borrowing. Q1FY20 debt was 690cr, q1FY21 at 268cr

-

Took advantage of low cost paddy, higher volume inventory yoy.

-

We estimate that traditional Basmati rice prices will increase yoy by minimum 10% to 15%. Internal estimate basmati production would be lower by 15% - 20% this year. Higher sowing of 1509 compared to 1121/ Traditional /Pusa Basmati. the consumption and the demand of 1121 is more than 1509. So we feel that 1509 prices will come down by 10%-15% over this year or the prices of 1121 will increase by 15%-20% this year. If the estimates that I’ve discussed are correct, which we will come to know by end of August or first week of September.

-

Guidance: Q2 will have a jump. Maybe 50-100cr or 5% more because of shipment delay in Q1. So, we will end up the year by 5%. We’ll try our best to do Rs.5,000 crore

-

Domestic- Lower realizations. Muted HoReCa. Retail mix towards lower priced SKUs. lower varieties, which is Mogra, mini Mogra, they sold more than the higher varieties. Highest ever consumer pack volumes, growth of 30% yoy

-

On hard questioning of Daawat doing better- " Competitor shipment was all containerized. And our shipment is break bulk. So, the break bulk shipment was a big hassle in COVID. There was no hassle in containerized shipment and why you say that Rs.350 crore carry forward will not be better, definitely our second Q2 would be better by Rs.350 crore. I’m expecting Q2 to be practically 2x of Q1 " That means Rs.1,400 crore? It will be astonishing good numbers. “Good number, but Rs.350 crore will be definitely carry forward and whatever we are doing in a quarter so, we are doing better than quarter one. So naturally, our numbers would be quite great in quarter two”

-

Right now there are no functions, whereas there is a lot of consumption of basmati rice in marriages, in functions, in parties, in restaurants, in catering, and this has nothing to do with restaurants. You can’t say that we’ll make up, that will make up only for KRBL, I can tell you one thing, because of our strong brand. Otherwise, HoReCa segment will have a big dent on other rice millers, rice exporters and rice traders. You see one of our brands is very famous in HoReCa segment. It has a big market, and that is Unity, that brand is suffering a lot. HoReCa was 35% of domestic sales in FY20

-

Normally we do 500cr per Q. Q1 was 350cr.

-

Covid impact on others: Small players and small brands: they are not there at all. Small brands, if you talk, those who are selling with retailers and people have opted not to buy loose rice. So that has really dented those small players because the sale of loose rice is really less compared to previous pre-COVID and post-COVID.

-

-

Exports- Revenue hit because 34,000- 35,000 tons of cargo was supposed to be shipped in May- June. Shipped in July -August.

-

entered the mainstream market in Canada after long and concerted efforts. Will also will enter USA mainstream market. Confident that these two markets will bring good jump for KRBL.

-

Saudi Arabia weak for last 2-3 years. now working to improve. India rice market increasing

-

Iran is a huge market for India for export of about 1.3 – 1.4 million tons of basmati. We are all confused as to what would be the fate of Iran. Routing Iran business through Dubai- No, we will not do that business because according to us, that is not a legal way of doing a business and we will not involve ourselves into any illegality.

-

we have to grow more and more pesticide-free paddy to ensure exports into Europe, USA and Middle East since within next 3-4 years we believe all countries will have the norms for pesticide-free materials.

-

-

basmati rice is normally sold between $1,100 to $2,400. In domestic, even the broken rice is sold, which is about Rs.40, Rs.45, then comes Rs.80, then Rs.90, then Rs.140. So there is a big range, there’s a big product mix pattern as far as basmati is concerned. Since most of the sales were taking place in the primary segment, the average sale price increased from Rs.85 to Rs.101 a kilo in exports and same was the case in domestic market. It will be our utmost endeavor to maintain this EBITDA and profit margins. But as our top line increases, we have to go and look at those sales, which are at $1,200, $1,300 in the range of Rs.80, Rs.90 also. That is also there, but margin of profit is different than the sale price and we will try our level best to maintain this EBITDA what we have shown now

-

Demerger of power- If we are able to get the PPAs transferred, then we will definitely go ahead with it. If at any case they want to renegotiate the price on PPA, we will not do it. …You see, the book value we have taken accelerated depreciation throughout and as per the income tax, the value of the asset is practically zero. If we sell the asset, then it will attract a 25% state tax. Suppose I sell the asset at Rs.800 crore, so it will attract Rs.200 crore as tax only

-

Health/immunity trend: The sale of brown rice has gone up, and we have started a promotion along with 1 kg of brown rice, you take 200 gram of Quinoa. So we are promoting a lot of health products. we are more and more concentrating on healthier products now. In exports, we have come out with Rice Bran oil with Amaranth, with Chia Seed, with Flax Seed. So we are creating a full health basket, especially in the export market and we are very positive on it

-

Quinoa- pre-COVID we sales 7- 8 tons a month. Currently 12-14 tons

-

We have launched idli rava, and during COVID period, the sales were also good. But we are not looking at heat-and-eat segment, but we are looking at certain other SKUs, which are more on health side. Definitely, you will see in next six months, there are some more launches, but definitely on the health side

-

-

Regional rice- after COVID we are going to set up units especially in South India and West Bengal to supply directly from those units to save on logistics / distribution cost. So, we’ll plan big for that investment

-

No plan for buyback. still not discussed within ourselves.

-

Potential higher cash flows- we will increase our inventory since our marketing and brand which is 2 years old, 1.5 years old, our volumes will go up. So naturally, inventory has to go up

14 Likes

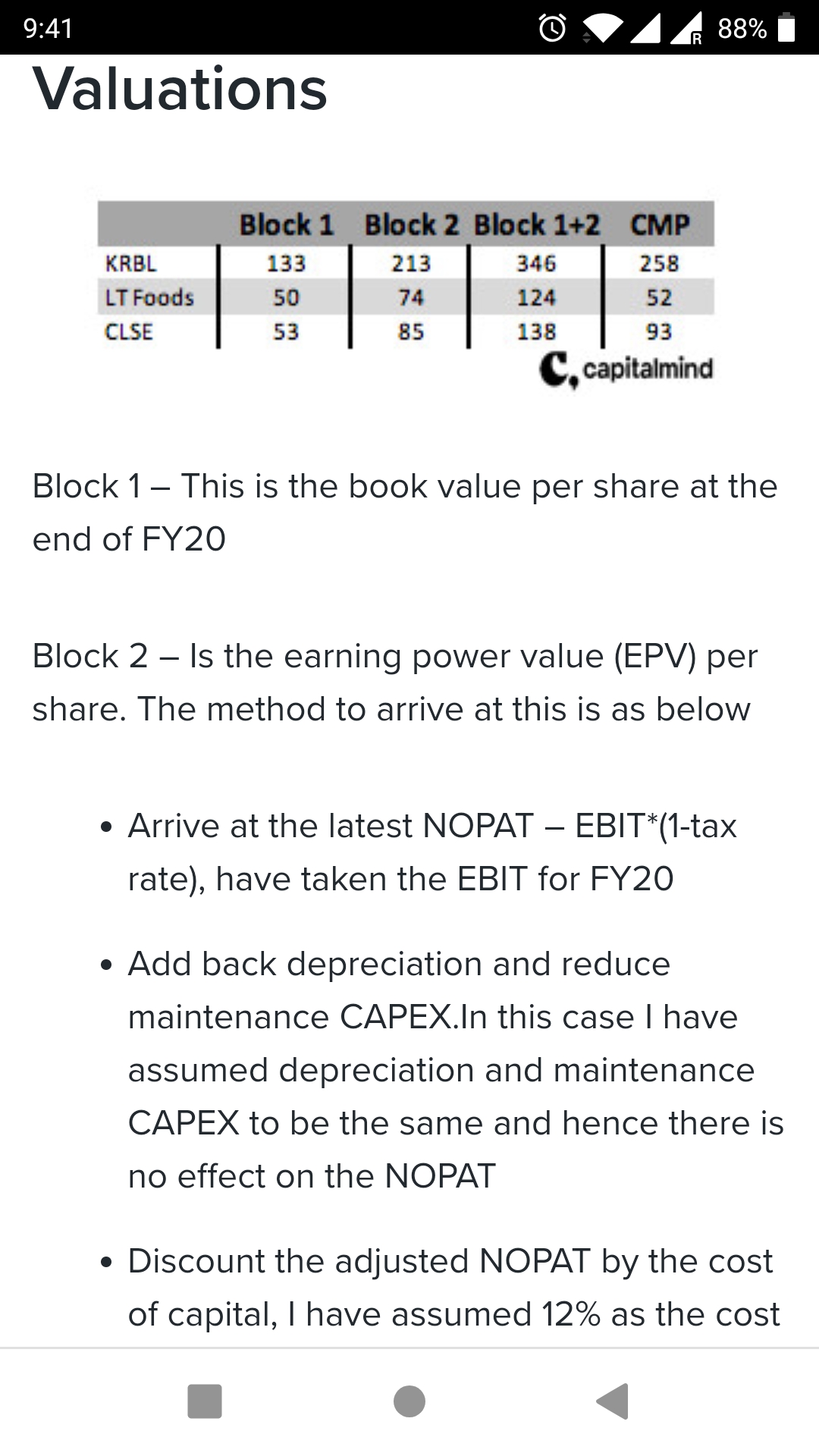

Capitalmind has come up with a simple and detailed article on listen players in basmanti rice category.

If you are not subscribed, can use 14 days trial period and read. Still pasting couple of snap shots from the article for ease of ref.

12 Likes

1 Like

AGM notes:

- Prefer to be a zero debt company

- Mandi tax: Landmark act. 60-70cr benefit, half of that will be passed to the farmer

- Shipments to Iran stopped, impact 1mnT exports expected instead of 1.4mnT

- Saudi import increased from 900k to 1.2mn

- Saudi Market share lost over the years happened because the previous distributors has financial troubles, locating a new one may take 2-3months

- Health foods margins are ~60% but not much impact on top line…may be 200cr in a few years

- Good growth expected in US/Canada

- Dent in HoReCa was expected to be 40% for FY21, now HoReCa dent expect expected is 20%

- Expect procurement price to be cheaper by 15% this year, so KRBL will buy more this year. Inventories should go up.

- Plan for non-basmati: Aggressive in regional, but covid has impacted plans. In 3-4yrs 1kcrore revenues expected and company would sell high margin aged rice. Aging cost is the lowest for KRBL.

- European exports: This year higher pesticide free rice is expected, thanks to punjab ban on exports. Will be back in Europe. Aged rice to export to Europe will start reflecting in Q3/Q4 numbers

- Use of cash flows in future: 6,000 cr to inventory needed for 8kcr. Next year either dividednd would increase or buyback. Dividends should increase going forward.

- Future Ebidta margin: Recent EBIDTA margins are higher and not sustainable in the long run

- Q2 performance: Much better than Q1

- Management would look to market to investor community.

- Forex appreciation impact: Cover 80-85% against dollar in normal times but doing 100% now

- Idli rice: Doing well, should grow to 50-100cr in next 2-3yrs

- No-Capex needed to reach 8kcr, have inbuilt milling capacity

28 Likes

1 Like

Was going through the AR and observed that the second generation have been offered gigantic pay cheques this year. To my mind, not the best decision in COVID year.

1 Like

The paychecks overall for promoters/mgmt have been relatively quite low compared to other companies of same size, pedigree and profitability.

If you are referring to 22 lacs in 2019 to 26 lacs in 2020 then it doesnt appear too high in itself or as a hike. Plus company did well last yr ie 2019-20 so even hike is justified on a low base. I doubt if you will find many similar companies with 2nd gen being paid so low!!

Or did u see something else?

Rgds

RR

1 Like

The salary for second generation (4 kids of the promoter families) has been revised to 60 lacs from 26 lacs with effect from April 1, 2020. This decision, especially in the COVID circumstances, didn’t send the right message across to me at least.

1 Like

Yes…you are right they do look excessive. I couldnt find this in the AR but just checked that these resolutions were passed recently in the AGM.

We only have info available regarding their salaries but we don’t have any info regarding their real and actual contribution and its importance to the business as well as their skills and competence. Maybe there was some misalignment. So it is possible that these were part of some “salary corrections” and maybe they were overdue…as their salaries did appear quite low till last year!! And maybe their contribution in the company is increasing a lot…and maybe they are being groomed for higher responsibilities.

But yes, these are just rationalizing arguments and might not be rational…and maybe the truth is that promoters indeed are using their position to help their sons. But if it was so then we must ask the question as to why did the promoters not increase their own salaries excessively for so many years??

Also one promoter’s son has 15 yrs experience and others mostly 8 yrs. But their salaries seem to be similar. Is that fair?

So this subject of salaries of promoter’s sons is not easy and has to be taken wrt many considerations like roles, responsibilities, real contribution, future readiness, parity within and outside, etc.

So yes, I agree with you, when seen in isolation, the hikes do look excessive and the mgmt should have given more details to justify this.

But as an investor does this bother me to make me revisit my investment decision? Clearly no, as the positives far outweigh these and many other negatives.

Rgds

RR

1 Like