Totally right! Two of them have decent experience (6-8yrs) and public profiles and it seems justified, but the other two don’t. Seems very excessive to me. 60LPA + perks for 4 more people is going to cost us owners ₹2.5Cr+ every year.

1 Like

yeah, Its not just about Rs 2.5 Cr its about their intent and integrity, In future they might look for opportunities to squeeze more of your pocket.

The proposed remuneration of upto Rs. 6.5 mn, for the 2nd generation of promoters is an upward limit, which the company cannot exceed. It is extremely unlikely the company will hand out a 250% increment in a difficult year, given that the salary growth has been in the range of 15-20% over the past 2-3 years for them. In the worst case, even if we assume that the entire sum of Rs. 6.5 mn is paid to them, the members are well qualified, have been associated with the company for a while now. The total family remuneration, including Executive Directors and other office of profits (all inclusive) aggregates to less than 1% of FY20 net profits. In my opinion, there are no concerns on remuneration.

Regards

Shobhit Jaju

3 Likes

1)Very good result by Krbl ,though driven by exports where the margins are far better 2)Huge operating leverage into play bcos of export margin 3)I am assuming India business didn’t do well bcos of Horeca segment which should do well as complete lockdown has been withdrawn ie from full qtr 3 onwards

KRBL qtr 2 ppt 061120.pdf (7.0 MB)

3 Likes

1 Like

In my view KRBL is not a cyclical stocks -their inventory holding is cyclical ,but not the underlying business -if you take a horizon of atleast 6months -1 year ,then the actual consumption of rice (read as offtake ) by consumers will get filled by the company as primary sales to their distributors who in turn would sell to retailers ( secondary sales ) .This way typically a FMCG company operate .If past is an indication of future, their sales ,PAT and share price have compounded @ 11% ,16% and 18% respectively for 10 YEARS which is a very decent compounding .I am expecting the same trend in topline and bottomline (if not more ) and a PE re rating going forward meaning the share price will compound faster ,is my view .

Discl_ my views may be biased because of my holding

8 Likes

Thx for your views. I also expect a PE re-rating is on the horizon. Investors should be able to finally see the strong track record of 20% OPM, 20% RoE, 16% NP CAGR. If a company with such strong brands and commanding market position is available at 10x TTM PE I think it is surely worth a look from a value investing point of view. Main hangovers over the stock are Iran exports, COVID related HoReCa slump - both of which should be addressed shortly (reports of Iran clearing payments and resuming imports). Focus of Health foods, entry into new big markets of USA/Canada are other big positives not yet priced in.

Below chart is courtsey of screener.in and shows how the PE has derated (EPS gone up while price moved down since 2018). Even at current EPS if maintained, median PE implies strong upside.

2 Likes

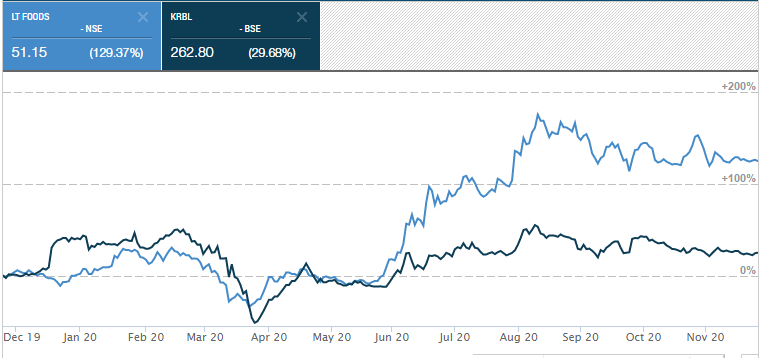

Also massive underperformance vs L T Foods (Daawat brand) over last 1Y (see below chart, c. moneycontrol). Now considering India Gate has ~35% market share and Daawat ~30%, both seem to be strong competitors in the branded rice market. Keeping aside the fact that LT Foods has always traded at a lower PE vs KRBL, it is imp to note that L T Foods’ current PE of 6x is 15% discount to the 5Yr median, while KRBL’s 10x PE is at 44% discount…justified??

2 Likes

Would suggest that you have a look at 5 year profit growth of both companies too before making PE discount comparison.

Past PEs are a very rough benchmark, but LT food profit growth has been much better.

In recent past, LT foods has shown a revenue and profit growth which KRBL has not.

4 Likes

Not sure of what you mean here?. I am comparing the PE discount of the the two companies vs their own history and NOT against each other. What I am intrigued about is why should KRBL trade at 44% discount to its own historical multiple while L T Foods trades at almost its median multiple?

Also, looking at their financials I would rather NOT just see the 5Y growth in profit. More focus point would be the higher profit margins of KRBL vs L T Foods (OPM of 20% vs 11%; NPM of 13% vs 5%), basically KRBL makes 3x more NP on similar revenues vs L T Foods!!

1 Like

Once doubts are raised about company for any issue(ref - Augusta Westland case), it becomes difficult for market to value the company in the same way. Hence historical PE has no value as market starts looking at the stock with some suspicion. I think similar story is playing out at Kaveri Seeds.

8 Likes

KRBL purchase 1718 and 1121 (paddy category) from the market. At the start of the season, they were at 2200 and 2500. Remained around at that level for 15 days before moving up. Now 1718 is at 2861 and 1121 is at 2900 (Jind, Haryana mandi rate). Rough guess bulk of buying happened below or equal to 2500 for 1718 and 2600 for 1121.

17 Likes

Deepender, Where can we find this info?

1 Like

Hi @satishwe, My father runs a shop in Mandi which sells to them. I am not sure if there is any official website which records this.

7 Likes

thx for this insight. As far as I can recall, Co mgmt had said in their Q1 CC that they will be taking advantage of low market prices, seems they did a good job!

1 Like

2 Likes

The company has refuted the above news, https://www.bseindia.com/xml-data/corpfiling/AttachLive/7944cd78-68f7-4608-aebb-4e2e3defd113.pdf

1 Like

Such a big company and just 16cr is the amount in question. I guess it should not impact KRBL materially in the long-term.

Thanks for highlighting this. While the company has denied any wrongdoing (which obviously they will), and also the amount involved in not much, but this does raise some red flags to me. Company’s name getting involved in such central government defense deals which is no-where related to the company’s area of operations does raise concerns on the company’s governance and ethical policies. I feel dumb to have missed out on such crumbs before making observations on attractive valuations in my earlier posts. This episode has taught me a good lesson of not only evaluating a company by the numbers but also by their social and ethical values.

2 Likes