Is there any news about the Enforcement directorate’s raid on the company?Has the ED given a clean chit?

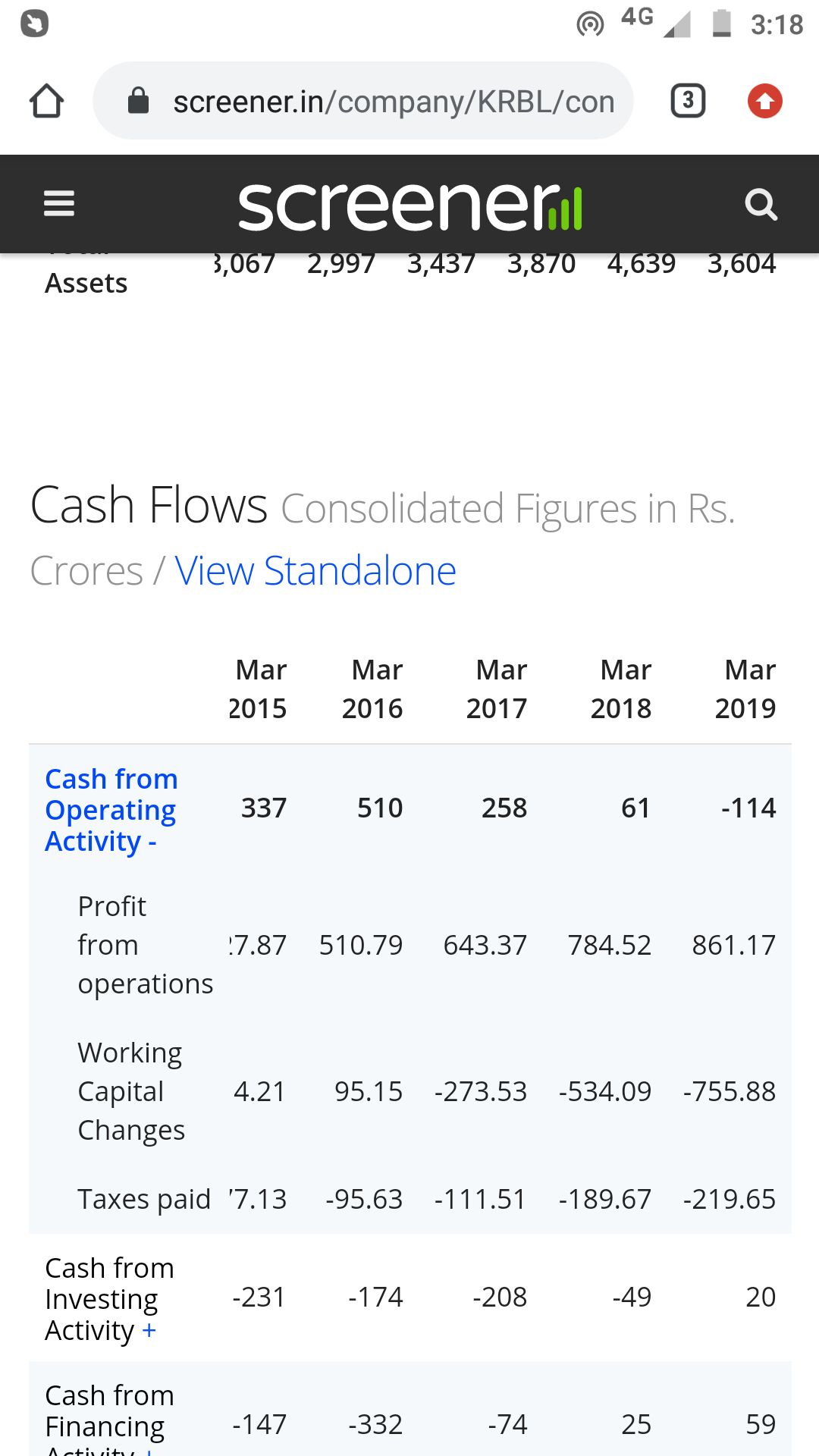

Screener shows CFO is negative in 2019 ending. Due to working capital needs. Could we find these numbers in the AR, and further dissect this lead.

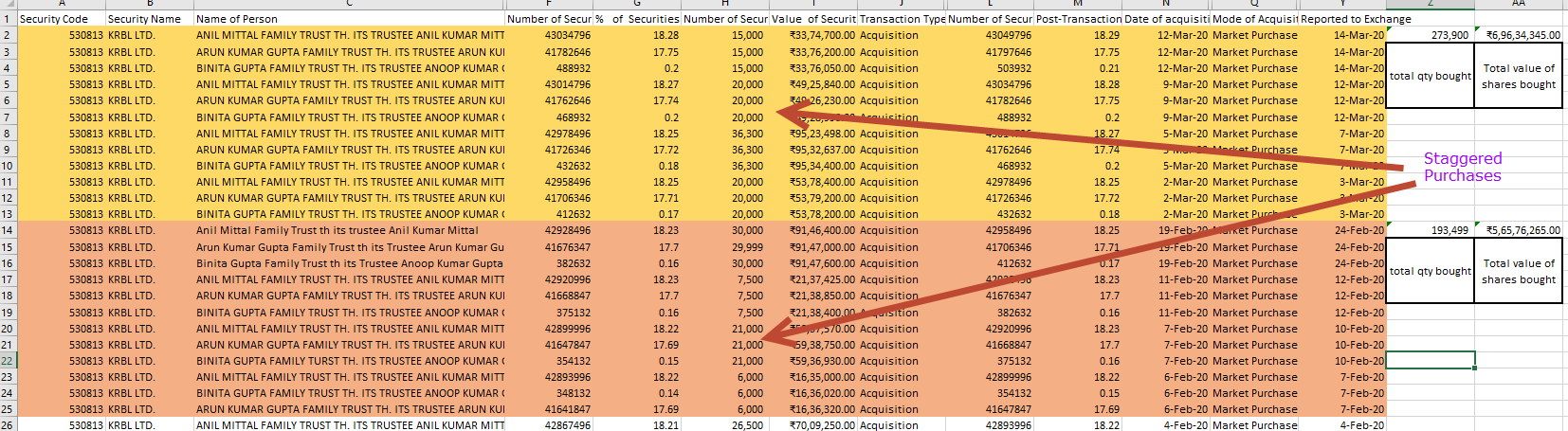

Since this date, Feb 4th, the promoters have been constantly buying in a staggered manner.

Bought back 12.62 Crores worth of stocks. Total quantity acquired - 4,67,399 Shares!!

Disclosure: invested & no trx in the last 30 days. Please do your own diligence before taking any actions.

2 Likes

Hi Ganesh, thxs for this info. Any idea how much export is to Iran and is that Banned or still continued.

The interview was deferred as per the intimation by the Company to BSE

Hi Kartiks, can you share link to the video?

Regards

Krishna

1 Like

No the interview was deferred. Pls check the bse announcement section.

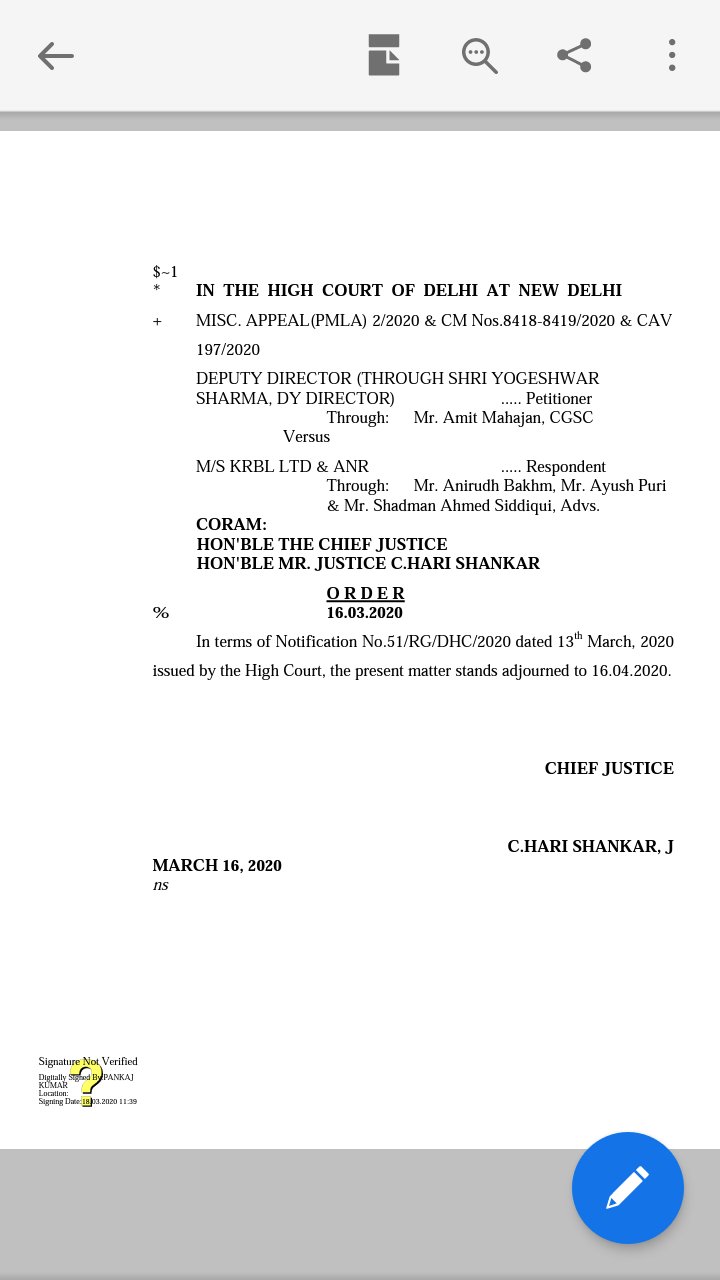

I did find this on twitter relating to pmla matter. Cant find more details.

1 Like

1 Like

Anil Kumar Goel - Pledged shares sold by Lenders on 26-03-2020

2 Likes

It’s actually bad market situation for such small cap companies. Just 0.54% stake offloaded and price collapsed so much (assuming the fall was due to this). What will happen if he/lender decides to sell remaining stake of 4.5% to improve liquidity condition or further pledge being invoked?

As per mgmt interview 50% of his holding had been sold. 10% o of it was due to pledge. So yes the 50% sale led to such carnage.

2 Likes

Over and above there r no of corporate governance issues - one or other keep coming and management keep defending…Share is in clear downtrend since ED issue … Mohnish Pabrai is a lucky guy…

1 Like

Please highlight corporate governance issue.

Also have a look at this - on ED issue:

I recently invested during this pledge sale(reasons below):

- In India hardly you get brands at 4-5PE (now 6.7)

- Market leader + Dividend Paying + Promoter buying + No pledge

- No corona impact on industry so far - some +ve impact seen in shops because of hoarding

- Recent Income Tax assessment in favour

- ED case against company is only 15cr - but could remain on investors mind till settled

- 10-15% volume growth, management has target of 8k cr revenues in 4-5 years, inherent ROEs of 35% and can be seen if renewable power business is demerged

It has been well debated in this forum that it can’t be valued at FMCG multiple of 40-50 but nothing stops it to reclaim 15PE in next few years

2 Likes

Completely agree with ur above points but Why the pledge holder of mr.goel sold their holding ?

When mr.goel has enough stock to pledge more if need arise or the prices goes beyond their point?

If i am not wrong mr.goel holds some 10% of the company and out of that only 5% is pledged!

Than what makes lender so uncomfortable ?

Disc. Not invested

Last years numbers were a precarious, and this year the situation is not being assuaged. A number which I find important is Net Cash From Operations. It must be in line with Net Income, otherwise I see too much risk in growth.

In 2017

Net Income 5376

Net CFO 2587

Diff: 2789

This diversion is big, but since the growth is good one is willing to give it a chance.

Then In 2018

Net Income 6550

Net CFO 417

Diff: 6133

A good time to get out of this stock. This shows that the goods are being Invoiced, but payment is not being collected. This is really bad. In front of this, no other numbers matter to me.

Now Look, in 2019

Net Income 7330

Net CFO -1144

Diff: 8474

Normally, one would say that the growth is good, even in such bad times, by looking at the Net Income growth from: Net Income 5376 to 6550 to 7330.

But, I think the situation has gone out of hand. Surely, the promoters are doing something fishy, like selling goods to its own entity and siphoning off the funds. In fact, if you look at the Debtor list, there will be a few entities where the Trade Receivables will be unusually large.

5 Likes

@jamit05 KRBL unlike their competitors tend to store rice for about 2 years so that the product is seasoned. I remember reading that management tends to procure rice when the prices are down and hold back from purchasing when prices go up.

Exports are always around 40 to 50% of sales. Considering the geo-political situation in middle east, these might have had an impact on receivables and debtor days.

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Inventory | 834.83 | 787.9 | 781.27 | 1208.5 | 1237.73 | 1260.29 | 1690.02 | 1859.67 | 1795.66 | 2019.96 | 2462.72 | 3129.39 | 3073 |

| Trade receivables | 180.81 | 70.67 | 135.08 | 148 | 229.16 | 194.72 | 287.26 | 339.98 | 154.46 | 230.02 | 246.68 | 397.29 | 315.37 |

| Debtor Days | 66 | 20 | 31 | 35 | 52 | 35 | 36 | 39 | 17 | 27 | 28 | 35 | |

| OPM | 14% | 16% | 13% | 15% | 14% | 14% | 15% | 17% | 13% | 20% | 24% | 21% | 19% |

| Taxes paid | -10.36 | -25.76 | -27.1 | -30.49 | -18.43 | -56.04 | -69.32 | -77.13 | -95.63 | -111.51 | -189.67 | -219.65 |

Also take a look at this report from a fellow valuepickr.

Edit: Added historical inventory, receivables, etc., Also referenced a slide from their latest investor presentation.

2 Likes

Is it possible to deliver goods and not to collect money ?

That is a reasonable thing to say.

I have read that about krbl’s style of working.

Still there is a doubt, that, if this is something which this company has to do every year then that amount under the heading of inventory should be perpetually blocked.

Nonetheless, let’s look at the past few years’ cash flow statements and see if something is discernible.

@Kuldeepjadeja, Yes it is one way of siphoning money. For me, if a company is not increasing it’s Net Cash Flow along with it’s Net Income, then it’s a big red flag.

1 Like

OCF not matching Net Income is a valid concern for any business and not just KRBL. KRBL is a unique business with some Business Intricacies that one need to be aware of to better understand the business. These intricacies are like 1) Basmati procurement period 2) Aging Process 3) Inventory increase and decrease season 4) Underlying basmati pricing cycle 5) etc. Each investor in KRBL should have a good grasp on all these important intricacies.

Now let me try to address your OCF not matching with NI concern. Basmati is grown only once a year. Paddy procurement period is limited between Oct-Dec. And KRBL ages its paddy for mostly 2 years because aged basmati is premium product because of its taste, flavour, and aroma. Hence KRBL commands better margins compared to other peers. So in b/s of March you are going to see increase in inventory because of paddy that was procured in Oct-Dec. If you see their b/s that they share end of September every year, you will notice drastic decrease in inventory where older aged basmati is being sold and new basmati is again procured in Oct-Dec increasing your inventory (see how inventory moves in screenshot that @madhug has shared above). In order to grow they have to increase volume and hence their inventory goes up every year. Hence, increase in inventory puts pressure on their OCF. If they were to release their annual statements in September instead of March, Cash Flows would have looked very different.

I presented my understanding of KRBL’s business at 2019 VP Annual Goa meet. Please look at the presentation to better understand the business. An Attempt to Better Understand KRBL Ltd._Amit Rupani.pdf (889.6 KB) If any questions, please feel free to reach out.

Without understanding the nature of the business and calling promoters shiponing money without backing with any proof/evidence, is a very harsh statement towards promoters, imho.

Disc: invested and my views will be biased. I’ve added to existing position last week.

19 Likes