@rupaniamit Want to know your views on the impact of heightened US/Iran tensions on Indian basmati industry and KRBL.

There were already fears for lower demand from Iran. With the tensions escalating, will this lead to temporary supply glut in the market due to demand shortage, resulting in lower prices?

Disclosure: Significantly reduced holding today. Will look for more clarity before re entering

Hi @fundoo - Although I feel I understand KRBL’s business economics but I also know that I am not a basmati industry expert. I will not be able to share my view on the future regarding impact of this geopolitical tension on the basmati industry or KRBL. In fact, personally I would not even take Mr. Anil Mittal’s future view on this topic since its so delicate and sensitive that I believe no one can predict how things will pan out. This reminds me famous quote by Bruce Newberg - “There’s a big difference between probability and outcome. Probable things fail to happen - and improbable things happen - all the time.”

However, I would look at two indicators 1) look at the history and take cues from it to check how things materialized in the past. 2) where are we in the existing basmati cycle today to determine whether to be aggressive with accumulation OR stand back and let market/cycle come to your comfortable price.

Sanctions on Iran or geopolitical issues in the middle east have always been an issue in the past. However, their appetite for basmati has grown year after year and KRBL has flourished with it. Will this continue in the future? I believe so. Currently Iran consumes 3.2mn MT of basmati annually out of which it produces 1.8-1.9mn MT and imports rest. They have no option but to import to cover their short-fall. Pakistan produces about 600k MT. India’s production is 6mn MT. Pakistan doesn’t have capacity to fulfill Iran’s full demand. Iran doesn’t have any option but to come to India. Mr. Mittal has indicated before that worst-case Iran business will go through Dubai or Iraq. So long story short - there can be short-term Iran demand issues given trade bans or US sanctions, but I believe there is a good chance if someone is holding for long-term this event would be a small blip in the bigger scheme of things.

Mr. Mittal has already candidly shared that this year they are expecting good basmati crop which in itself should keep prices in check. On top of this if Iran demand is slow/less - then that will add further pressure to basmati prices.

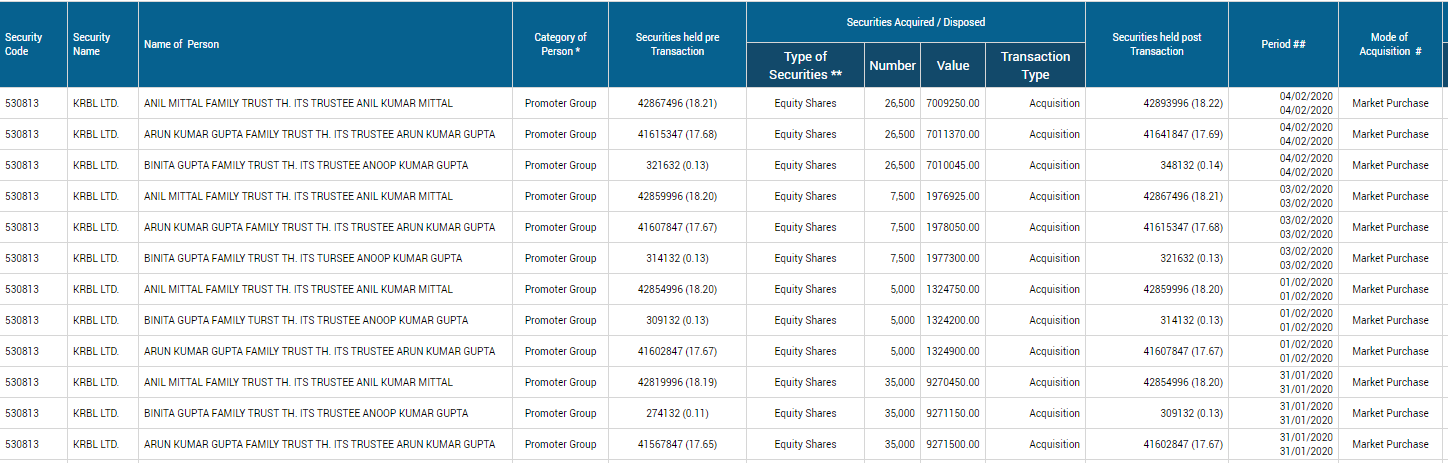

In the bigger scheme of things - recent opportunistic aggressive purchases by promoters of 8.4 lac shares valued roughly at 20cr shows confidence by management that it is truly confident that Tax & ED issues will be resolved in KRBL’s favour and it is bullish in long-term prospects of the business. Mr. Mittal also indicated in one of his interviews that management is mulling over demerging energy business. If this happens, it’s balance-sheet will show the asset-light quality of Agri business plus 30%+ ROIC of Agri business which may lead to re-rating.

Disc: invested for long-term and will be buying at attractive levels. Views will be biased because of ownership and current accumulation in the business.

Rice millers in India face a squeeze on margins as basmati trade to Iran has come to halt, as insurers aren’t ready to provide cover to shipments following the latest escalation in Iran-United States conflict.

Payments were late by five months last year and exporters are not ready to take more risk.

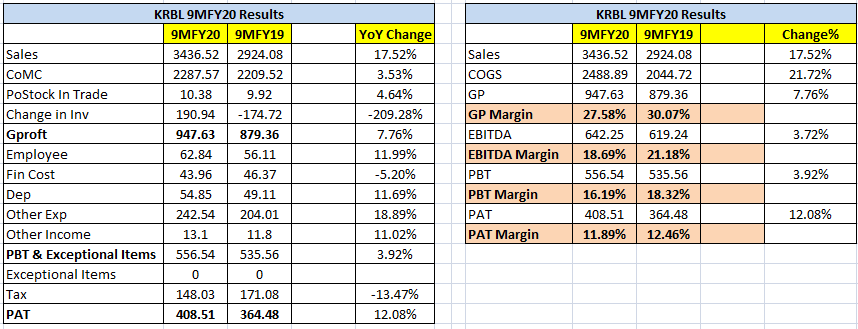

Heartening to see 33.29% increase in exports volume for 9M in challenging export environment.

EBITDA margins have come down from 21.18% to 18.69% with decrease in GM.

Looks like management had to compromise on export realization to bring in 33.29% increase in exports volume.

If there was no corporate rate tax cut, bottom line would have been flat instead of 12.08% increase since PBT is up just 3.92%.

Will be helpful to check how new basmati crop has come out and their procurement so far on tomorrow’s con-call.

PUSA 1121 spot prices per ncdex site has been hovering between 31.5 to 33 in month of January so far which I believe has been on the higher end than what was expected by management per Q1 and Q2 concall.

Will be interesting to see if management continues to do opportunistic purchases in Q4.

Good to see a small victory for ED issue; order dated 17 January 2020, the Appellate Tribunal has restored the possession in favor of the Company, however, such attachment will continue till the conclusion of the matter.

After Q3FY20 results, KRBL management has continued with their creeping acquisitions from the market. They have bought 2.07 lac shares spending total ~5.5cr in last 3-4 trading sessions. Total acquisition of 10.44 lac shares for total ~25.6cr in last 2 months.

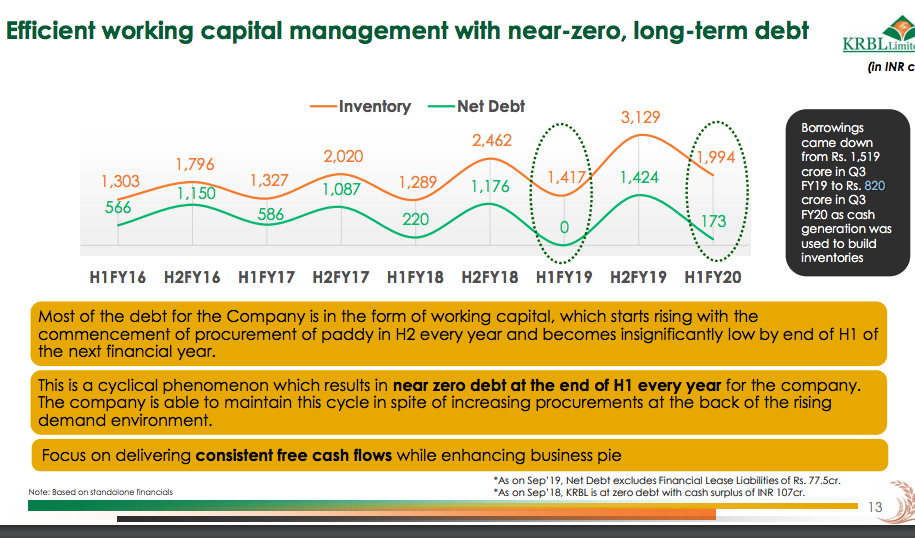

They have procured ~10% more paddy than last year (at 20% lower cost than last year) which is highest level of paddy that they have purchased in their history. KRBL is setting up good platform for better margins in FY22 and FY23.

Yes.people are buying rice left and right. Everyone is stocking due to coronavirus fears at least in US and Iran. Expected higher profits this quarter.

Hi @abhishekshete - thank you for sharing the info with everyone. Is that your opinion or based on any facts?

Can you please share your source of information for everyone stocking basmati rice in Iran and US due to coronavirus fear? I can imagine heavy stocking to happen (especially in Iran), but still it would be good to confirm it via a reliable source. Thanks.

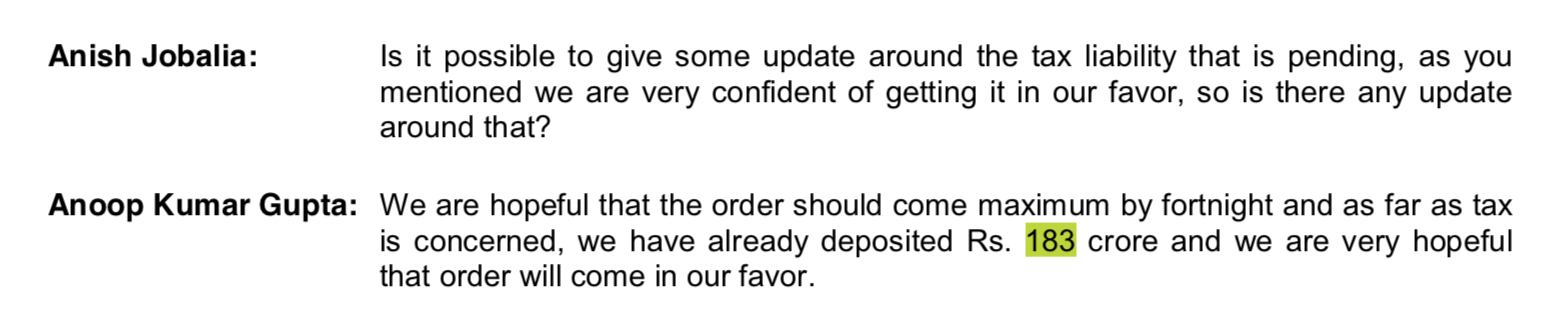

Much awaited outcome in favor of KRBL from IT dept.

As a result, the Income Tax demand got reduced to only Rs.101.46 Crores (including Interest of

Rs.38.93 Crores) as against earlier demand of Rs.1269.20 Crores (including interest of Rs.511 .76Crores).

What about the statement

“The Company is in the process of filing appeals with reference to the balance additions of Rs.181 .09

Crores before the Hon’ble Income Tax Appellate Tribunal (ITAT), New Delhi and is of the view that

these additions are unsustainable in law.” ?

CFO is getting worse due to increasing need for working capital. It is due to the company not able to get the debtors to pay up. Debtor-days is on a rise. I wish this company had more bargaining power.