Islamic year is 11 days shorter than the solar year. So approximately 1 month advancement every 3 years.

4 Likes

The LT Foods results are out and looks better. When someone (in this thread itself) comparing LT and KRBL the point highlighted is about Debt. In the presentation the DE ratio is brought down to a reasonable level of 1.25. Can we consider this company to get better valuations in next few qtrs ?

Daawat Results.pdf (803.4 KB)

1 Like

I looked at both Daawat and KRBL and decided on this one as the PE valuation is half of KRBL. Both are excellent brands, but my understanding is that Daawat is spending much more on branding than India Gate. On top, KRBL does not own India Gate brand exclusively for all products and the recent issues regarding corporate governance is a big distraction for KRBL. More often than not it has been seen that there is no smoke without fire.

Valuations should definitely close between these two companies (whether it is LT Foods going up or KRBL going down remains to be seen). Last 10 years growth and ROE gives comfort at these levels to hold.

1 Like

Latest Credit Rating report of KRBL.

https://www.icra.in/Rationale/ShowRationaleReport/?Id=72414

Key Points

- The profitability has improved significantly in FY2018 and in the current fiscal on the back of high premium on stock of aged Basmati rice, increased contribution from branded sales,and firming up of average realisations–both in the domestic and export markets.

- The integrated nature of operations of the company’s agri-business segment and contribution from the renewable energy segment inherently boost profit margins.

- The resultant healthy internal accrual generation and limited capex requirements have decreased reliance on external debt to meet funding requirements of the business. This is demonstrated by the steady decline in the percentage of inventory funded through external debt from around 66% as on March 31, 2014 to 47% as on March 31, 2018.

- The inventory, valued at cost, also carries a pricing premium in light of the increase in Basmati rice prices, both in the domestic and international markets.

- Iran, one of the leading importers of Basmati rice from India, intermittently imposes import ban which affects the demand and pricing dynamics. In this fiscal, there is the added risk of trade sanctions onIran by the US, which can impact supply to that country.

- Another growing risk for the industry is the tightening of pesticide residual norms by importing countries. The European Union has already imposed stringent norms with effect from January 1, 2018. Saudi Arabia (another leading Basmati rice importer from India) is also considering the same. These norms can severely impact the demand for Basmati rice from India.

- Paddy prices have firmed up considerably over the past two procurement seasons, resulting in an increase in the cost of inventory.

Regards

Harshit

2 Likes

3 Likes

KRBL Ltd

Highlights of results of Q1 FY19

Financials

- Revenue de-grew by 15 % to744.44 Cr against 878.90 Cr last year same quarter

- Shipment worth Rs 200 Cr are lying at the port and it come in July. It is because of Ramzan Festival going on in the countries in June so there is a holiday of 8-10 days.

- Company achieved EBITDA margin of 24.62 % compare to 23.91 % last year same quarter increased by 71 basis points.

- EBITDA 183.25 Cr

- PBT margin stands at 20.09 % at Rs 149.26 Cr during the quarter compare to 18.45 % at Rs 164.79 Cr last year same quarter. PBT margin increase by 130 basis points

- PAT margin improve by 62 basis point from 12.82 % to 13.44 % in the quarter.

- Company earned a profit of 100 Cr total compare to 109 Cr last year same quarter.

Key Highlights - Price are stable in range of 66-67 Rs for brown rice , 73-74 Rs for white rice

- Market condition is very good due to favorable monsoon and increase price of MSP.

Q&A - Give some brief on the dispute in Iran market ?

o There was a notification from Iran that from 22nd of July Iran will Ban import of Basmati rice . Few days back company get notification from the government that there is no such information from the government of Iran. But due to tension of Trumph Administration there are rumors that any payment after 5th or 6th August might be problematic but still it is not confirm. So it is very difficult to say anything because the last Mail received from Indian Embassy in Iran also say that there is no such notification from Iran for Ban of Importing Rice after 22nd July. Still the bankers are not confirming the trumph administration that how the payments will effected. So therefore shipments are going Regularly . They have slow down because people have doubt in their mind that payments received after 5th Aug what would be the grade of the payment from Iran.

o Every year in month of August September in Iran there is a Ban because they have to safeguard their own farmer because there is harvesting in September. So in September-October there is no export to Iran.

o There are two items which cannot be stop from export one is essential commodities like Rice and other is medicine . Iran have an alternative arrangement where Iran cannot stop it. Their total consumption of rice is 3.2 Mn ton and they use to grow 2 Mn ton . 1.2 Mn ton they import. Now because of their own problem they have defecated to 1.5 Mn ton. So there has to be some concession and relaxation as far as the food is concern. - What is company total exposure to Iran ?

o Just 4-5 % from last 5 year - Is there any issue of payment from Iran ?

o Yes there was an issue and that issue belonging to one particular private trade. Huge payment of 10-12 exporters are hold up in Iran and Indian government and association helping to get out of it . otherwise payments are coming normal and goods are going. Its only one Party who get a very big chunk of money around 4 months back that amount was around 700-800 Cr rupees. KRBL has no exposure toward it. In last 20 years company have seen a Bad Debt in Export as well as Domestic. - Kindly brief on the Europe has tightened the Import Duty on pesticides issue ?

o Company use to export around 350-325 ton of rice out of which 50,000 ton are use as traditional basmati rice and 275 Mn ton use as Usaa basmati rice. Now there is a problem as there is a fungicide known as Triseclozone and that they have reduce from 0.01 to 0.001. So because of that the Export to Europe from January till now is hardly 25-30,000 tons. So for that concern company had do lot of hardwork to educate them not to use certain pesticide which can create a problem of triseclozone. Company will solve this issue by atleast 50 % in coming quarter. Last year company had exported 25-30,000 tons of brown rice and this year it is hardly 500 tons. Company had lost 25000 ton but instead of that company had exported 12000 ton of Traditional Basmati to Europe. So company had net quantum loss of about 10-12,000 tons from January upto now. - Give Brief on China that agree for importing rice ?

o China is very difficult to predict and China has approved 12 rice meal in India for import and KRBL is one of them. Starting of import was going to start by 31st of July which has now be postponed to 15-16th August. Company is hopeful of some business to be commence. - What is the trend of the basmati rice prices ?

o Barkoil-1121 :- Prices in the beginning started with 58-59 Rs they shoot up to 73-74 Rs. Today they are at 60-65 Rs and now they are stabilized toward 65-66 Rs. But there will be a pressure on Basmati rice coming in next quarter but these prices could sustain because government has recently announce MSP of 200 rs for Non-Basmati Rice. So it has no effect on the Basmati rice also. So prices have sustain themselves at 66-67 . There is hardly any carry forward. If a order come in market for 100 thousand ton than this prices may jump to 72 so there is hardly any stock that can restrain the prices . Prices can go up but cannot come down.

o Rains are very good , sowing are very good . Company is expecting price of 28-30 rs because of increase of 2 Rs in MSP in non-basmati rice. That is the price of new paddy . Company will be able to do better over last year - Can company give some volume outlook for next 2-3 years ? Adani has gone and bought the Bhusan brand so the trade between India and Iran of a million ton that get impacted by Adani which is 25 % quantity in portal ?

o That Brand is purchase by Wilmar not by Adani . Wilmar is a partner of Adani as far as the Oil is concerned but this does not give assurance that they will buy rice also from Adani. Yes company is first discuss with Adani but they are also talking to 3-4 other players because they told Adani that 50 % they can buy on production and 50 % on the trading base. So things are not clear

o Wilmar has purchase this brand from Mosin and Mosin has sold this brand because he has already executed a dozens of people in India and people have still to receive big money from Mosin . As far as Mosin brand is concerned they have been in the market from quite long and their system of sale is not feasible . They use to buy goods at 1000 $ and sell them again in 1000 $ because they have decided not to pay to the Indian market. So they were spoiler of other brand in Iran market. So it is very early to discuss the strategy of Wilmar.

o Mosin use to buy around 200 thousand ton of rice from India whereas wilmar has come and say that in first year they will go for 100 thousand. So this is not going to impact the Indian Basmati market because the total market size of Iran is around 1 Mn to 1.1 Mn. - What is the realization difference between Basmati and Usa ?

o Company have three major varieties which are been exported out of India . One is traditional variety which is Dyeing which use to be 100 % export in 1990-1995 because of their yield per acre of 9-10 quintal compare to Usa which is 15 quintal compare to 1121 which is 3 quintal compare to 1509 which is 25 quintal which is dyeing and farmer don’t get surprise because of double or other variety of basmati rice. There is a export but that is also not more than 5-6 % of total export from India Major export more than 50 % is 1121 that is the majority of export.

o Company grown rice of 6 Mn ton out of that rice 4 million ton is alone 1121 and remaining is Usa , Sugandha, 1509 other. Last year people get very good price of 1509 Punjab has reduce its cultivation of 1121 and has gone to 1509 . Overall this year the production would be 6 Mn ton plus of Basmati Rice.

o As far as International market is concerned it is about 6 % there have to be jump . It all depend upon what is the reaction of China because if China start definitely it will become market of 300-400 thousand ton may be from 3-4 years from now because today they are buying a big quantity of Thai Rice. In the very first year company should export around 50,000 ton subsequently it will increase to 3-4 times in China .

o Now another problem is there is a disturbance in all middle east country . A country like Iraq they use to buy 400 thousand ton of Rice but payment is a problem from Iraq. Yaman is also having disturbance. Now in Opaque countries such as Liberia , Algeria, Syria. Lebonon there is a big Demand now if everything goes well and all sanctioned get removed then India can export 25 % more than the current level. But every time there is some restriction that made figure back to 4 million only. - What will be the impact of new companies coming in the market ?

o Because of GST many companies has been removed from the market and now only two brands exist mainly India-Gate and Dawwat. Adani has got a 4 % share , Kohinoor has got a 3-4 % share. India-Gate and Dawwat hold more than 60 % of market share. Other brand do not any market abroad.

o There were total 3000 rice meals on GT road from Delhi to Amritsar out of them 300 were for Basmati rice. Now they got register under small scale sector because government want to promote rice for export as a niche product and those people got money and money from Government from 1995 to 2008. So that result in many of people start trading and they vanish the market . Reason was Paddy comes for three month and total paddy purchase has to be done in three months. Now company have a program of 2 years to buy and sell and decide price because of brand value and other people decide it on speculation so they are not sure whether they will be able to liquidate the stock or what is going to happen that’s why whole industry has gone into bad shape. KRBL have very good control on the business and consistency of doing right things and company have good limits. Now the market will stabilize and don’t run in a roller coaster manner that is the advantage. - How management will increase the volume from 450 thousand ton to 1 million ton and also the market share ?

o Company backend is very strong , marketing is very strong , company have to only look toward marketing the brand. In next 5-7 year company will plan to take it to 1 Mn ton. - How much of rice inventory go back due to any of reason like fungus etc ?

o Nothing has gone back. - Is there any litigation on the company or promoter ?

o No - What were the volumes for the quarter ?

o In domestic market company had done 70645 Mt ton compare to 68170 MT ton last year. In value term company did 379.57 Cr compare to 352.07 Cr last year so average realization for domestic has increase from 51,646 Rs per MT ton to 53,729 Rs per MT ton.

o In export market company had done 29,016 MT ton compare to 54,383 MT ton last year in value term it is 268.05 Cr compare to 439 Cr last year . Realization has increased from 80,724 Rs MT ton to 92,380 Rs MT ton last year. Only difference come is because of goods were lying at the port .

o In power company revenue has increase from 37 Cr to 38 Cr.

o Rice brand oil sale has increase to almost double.

o Seed business is also doing better. - Did company is on track to achieve 10-15 % growth in volume in the financial year ?

o Yes company is targeting 10 % volume growth. - Why inventory days has gone up sharply ?

o It gone up in value terms because cost of raw material procured in 2017-18 were higher. From 25 Rs in 2016-17 it gone to 32 Rs in 2017-18. - What is the company plan to expand in non-basmati and non-rice segment ?

o Company have entered Kinovva segments , still market is in developing stage and in next 2-3 years company will grab good market share .

o Company is dealing in High quality Non-Basmati Rice like Jeera Rice, Kolam Rice , which are sold at 100 rs plus and getting good response from South India . - Within export kindly give the break-up of Basmati and realization ?

o 25,237 Mt ton of Basmati at a total value of 248.71 Cr and 3,379 Mt ton of Non-Basmati at total value of 19.34 Cr. Average realization of Basmati has increased from 81,651 Rs to 98550 Rs per Mt ton . Basmati was 52,912 Mt ton value is 432.06 Cr last year .

o Volume growth is due to consumer brand sold more in GT. - What was the rice inventory at the end of Q1 and the costing ?

o Paddy inventory of 1,64,281 Mt ton at average price of 31,299 Rs per MT ton

o Rice company have 3,47,402 Mt ton at average price of 45,436 Rs per metric ton. - What are the challenge company getting in expanding the market share in Kinnova ?

o Market size is very small approx 1000 to 1200 ton where company keep the MRP at 800-900 Rs per Kg and now company have reduce the price to 400-450 rs per Kg. Company have now reached to 10-15 % of market share and company can go to 30 % of market share and if company go to 30 % also than also company will grow to 300-400 ton of Kinnova market in India. So market has to grow and company is doing lot of social media for Kinnova and it will take 3-4 year to develop a market. - Does company foresee any investment in power sector ?

o No because IRR doesn’t come as per expectation. - Is there any impact of GST on the company ?

o No company pass all the GST to consumer and it is positive for the company.

5 Likes

The GST issue is given too much importance Atleast in Rice(basmati/non basmati). I had some friends in non basmati rice & they say they didn’t saw a single small unit who got closed due to GST. Every body moved to GST, just that some companies took time. Actually in rice, the branded guys are at loss as they had to pay 5%GST, although which eventually passed to customer. But if anybody says an advantage of GST, it’s simply a PR gimmick.

2 Likes

A Comparative test for Branded Basmati Rice from Consumeraffairs.nic.in website but the test is done by some NGObasmati-ilovepdf-compressed.pdf (2.9 MB)

1 Like

This test does not seems to be comparison of apples to apples . Premium quality of, Golden harvest, Lalquila and Patanjali compared with Local quality of India Gate- Tibar, where as export quality of India gate is Classic.

For it looks biased.

I am invested in KRBL and my opinion may be biased.

3 Likes

Like others, I also got puzzled with valuation difference between top 2 players. But looks there is a lot of justification to it hidden in numbers. Noting my observations:

- Prima facie, operating profit difference between LT(10-11%) and KRBL (20%+) - looks liked a main driver. But digging further got me further clues.

- Rice is all about ageing like wine - so inventory outstanding days is key - LT 178 days and KRBL 330 days. The difference is close to double - India Gate is really aged and not just branded like that.

- I wanted to further understand the causes of difference in profitability. So went on digging in P&L from AR 2018. Paddy cost for LT is 37% of sales and for KRBL is 48% sales. Rice is 43% of sales for LT Vs 20% for KRBL. This shows LT is more reliant on trading in rice rather than buying paddy and processing it, ageing it. This was further concluded when I bought Daawat Rozana Mogra - Basmati Rice 5 kg - INR 65/kg - which turned out to be a broken rice. I will email customer care to see the response.

- Apart from above, further into P&L - there is major difference in employee costs. LT is 137 Cr Vs KRBL 77Cr for almost similar level of sales.

- Further, expenses like freight in total are 112 Cr for LT vs 76 Cr KRBL - this may substantiate the trading point discussed above.

- Lastly, advertising and selling expenses are way to higher in LT vs KRBL.

- Lastly return ratios, capital gearing ratios are all favourable to KRBL than LT. KRBL may sound like a compounding machine with 20%+ ROE and looking sales vs debt growth.

Looking at above points, the valuation difference looks convincing and appropriate. Feel free to highlight points I missed. (Disc - not holding either).DaawatLT vs IndiaGate KRBL.xlsx (11.0 KB)

18 Likes

Rozana from daawat is actually a category for broken rice only. It is also divided into 3 sub categories: Super, Gold, and Mogra. All three has different sizes of broken grain, and are also priced accordingly.

Auditors resigned

2 Likes

Pl read th press release - Walker Chandiok ( Also Partners for Grant Thortan India ) are statutory auditors now…

1 Like

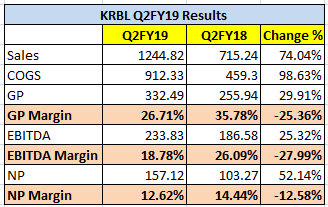

Earlier today KRBL posted the Q2 2018-19 results. Good set of numbers.

Here are the highlights

1-Revenue grew from 716.268 crores to 1250.39 crores registering growth of 74.5% yoy. Revenue in the last quarter was 744.44 crores.

2-PBT grew from 156.84 crores to 221.82 crores registering growth of 41.4%. PBT in the last quarter was 149.26 crores.

3-PAT grew from 103.27 crores to 157.27 crores registering growth of 52.3%. PAT in the last quarter was 100.09 cores.

4-EPS for the quarter stood at 6.68. EPS for the half year of 2018-19 stood at 10.93. Last year full year EPS was 18.46.

For more details please check out the results here https://beta.bseindia.com/xml-data/corpfiling/AttachLive/ed0597db-2390-485c-9ad6-a1b61553b98b.pdf

Cheers,

Krishna

Pretty good results.

Rev up 74% (1250 cr vs 716 cr YoY)

PBT up 44% (222 cr vs 157 YoY)

Agri Revenue up 76.6% (1194 cr vs 676 cr YoY)

Power Revenue up (69 cr vs 52 cr YoY)

PBT Agri up 29.5% (184 cr vs 142 cr YoY)

PBT Power up 40.7% (38 cr vs 27 cr YoY )

Domestic Agri Revenue up 47% (558 cr vs 380 cr YoY)

Export Agri Revenue up 114% (635 cr vs 296 cr YoY)

Exports Seems to have contributed primarily. Domestic, Power too contributed.

Finance costs 92 lakhs vs 13.91 crores (YoY). (Need to understand whether is some kind of adjustment of forex gains into finance costs; Balance sheet indicates Short term Borrowings are down to 115 cr from 1164 cr Six months back; 208 cr Year back)

Receivables stable YoY at 253 cr (vs 246 vr six month back; 261 cr Year back). Payables down to 56 cr (vs 115 cr Six months back & 84 cr and Year back).

Got to listen to concall to understand this Export performance is sustainable or not in coming quarters.

Discl: Invested

1 Like

Last quarter management mentioned that a cargo (worth approx 150-200cr) for Middle East was lying at the port and they weren’t able to ship it by end of Q1. The sale for this cargo is included in Q2 result and hence export numbers are inflated. Need to understand realization trend and value of existing inventory.

Margins were under pressure for Q2FY19 as perhaps benefit of lower cost inventory is not left anymore:

3 Likes

Video version:

Text version:

Very silly interview to replace important conference call. Not much useful info other than management were aggressive in increasing sales so had to sacrifice margins. H2 would be close to H1. No answer to investigation part of question. Iran seems to be planning to buy rice using rupee. No benefit of dollar appreciation due to 80% of dollar revenues are hedged.

Reading between the lines, looks like they have reduced the prices to compete with new players like Adani-wilmer, Patanjali etc…

Disc: Invested

1 Like

While I broadly agree with your analysis, there is a ~7-8% increase in realizations (both domestic and exports). Further, another positive is the ~35% increase in domestic volumes. Though, one may argue that it has come at the expense of margins. Giving the link of the presentation uploaded by the company on website.

Regards

SJ

5 Likes

Wasn’t the share sell to Pabrai funds ? So if ED follows the order, does that mean the buyer will have to take delivery ? And at what price ? Nothing to do with KRBL, just curious to understand how this will unfold.

1 Like