Walker chandiok is among the top 5-6 auditors in the country. Grant Thornton is the auditor. In terms of credibility 100 times better than previous one

1 Like

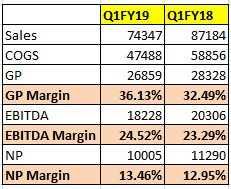

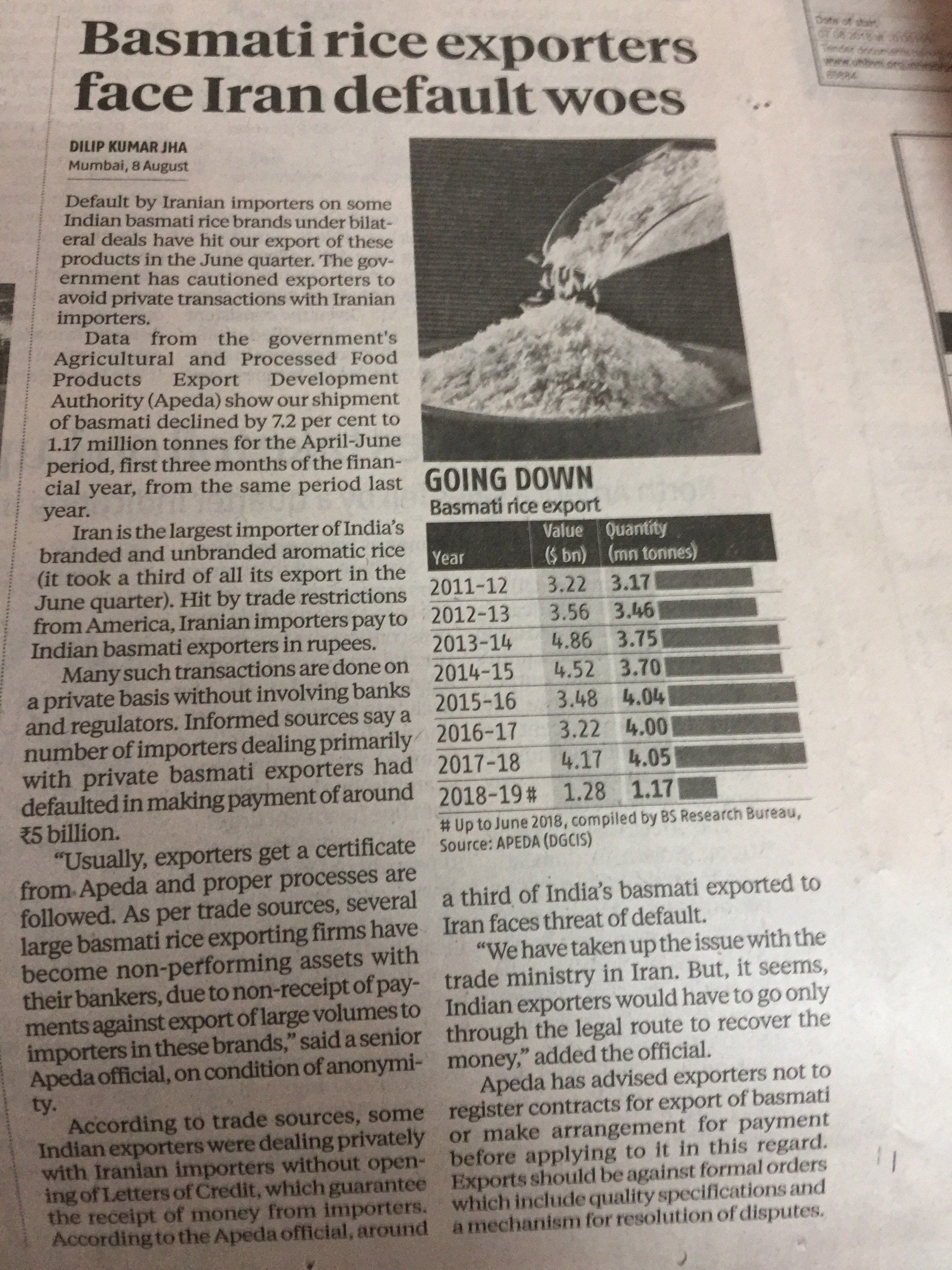

This quarter margins seem to be improving. Exports numbers have been very volatile impacting topline. Looking forward to understand from management reasons for decline in top-line.

Management mentioned on last con-call that they have cut-down on non-branded business and will be focusing only on branded business (which means lower volume but higher realization/value) which should keep EBITDA margins at around 22-23% range. They also mentioned that stock level of aged inventory is low in the industry and KRBL has got maximum aged inventory which should help to keep it’s margins firm. They also mentioned that low cost inventory benefit should continue in FY2019. Post FY19, key item to monitor would be growth in volume and level of realization/margins that management can get.

Disc: invested

1 Like

The reason for fall in exports is mentioned. 200 cr worth goods were stuck at ports and transported in July. Will be interesting Sept quarter results, if 200 cr gets added to regular Sept quarter revenues.

The old inventory is still contributing to profitability. Next year will be the year with higher cost inventory and most likely soft Paddy and soft basmati price.

Disc: invested

Heard this from some friends who are in rice (non-basmati) business in south:

Some dealers ask to pack rice in India-gate packs(non-basmati) which are available outside. The packs may be not look as geniune as original.

A few days back officials had raided, seized & served notices to these guys who are using India Gate trademark to pack their rice un officially. I am not sure whether the raid was conducted only for India Gate brand or also for all other unauthorised use of trademarks. Even the pack vendors who are supplying these bags were raided. But all these is related to non-basmati rice.

3 Likes

A case on Anti-Profiteering (GST) with positive outcome for KRBL

Kumar Gandharv Vs. KRBL Ltd. [(2018)

Facts: The Applicant in this case filed an application that the benefit of reduction in rate of tax on ‘India Gate Basmati Rice’ had not been passed on to the consumers as its maximum retail price had been increased since implementation of GST w.e.f. 01.07.2017 and hence margin of profit had also been increased by respondent. Held: India Gate Basmati Rice sold by respondent was not liable for tax before implementation of GST and after coming into force of CGST Act, 2017, it was levied @5% w.e.f 22.09.2017 with eligibility to avail ITC. It is apparent from the returns filed for the months of September to November 2017 that the ITC available to the respondent as a percentage of the total value of taxable supplies was between 2.69% to 3% whereas GST on the outward supply of Basmati Rice was 5% which was not sufficient to discharge the tax liability. Moreover, in this case rate of tax has been increased from 0% to 5%. Furthermore, there was an increase in the purchase price of paddy in the year 2017 as compared to its price during year 2016 which constitutes the major part of the cost of the product. Therefore, there appears to be no reason for treating the price fixed by respondent as violation of the provisions of the anti-profiteering clause.

Look at devaluation of currency where they are exporting…E.q. Iran

In comodity linked business paying high P/E is dangerous…it is 50% down from peak now It need to go 100% up to reach earlier price!!

2 Likes

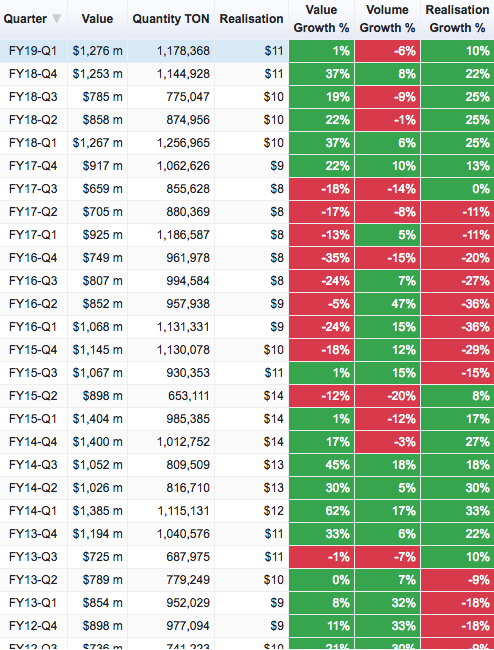

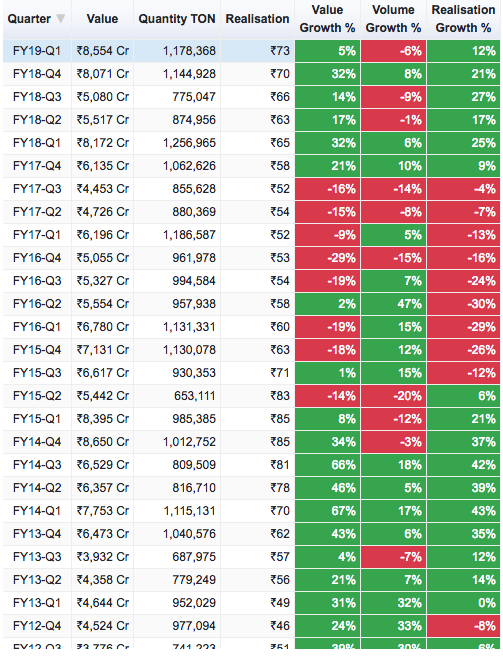

There is a big slump in volume probably due to devaluation of Iranian rial. Here is the export data of Basmati rice to Iran.

This data in USD terms where you can see exports YoY to Iran is down from $523m to $459m. This is because of volume drop from 514230 MT to 425372 MT. The volume drop is higher than drop in value - Thankfully the firm export prices at $11/kg (Rs.73/kg) has helped the numbers a bit. These are overall export numbers for Iran and sort of reflect KRBL’s trend.

If you see overall numbers for all countries, the growth is flat for the first time in 6 quarters.

In INR terms though, there is a 5% growth, thanks to rupee depreciation in Q1, FY18.

3 Likes

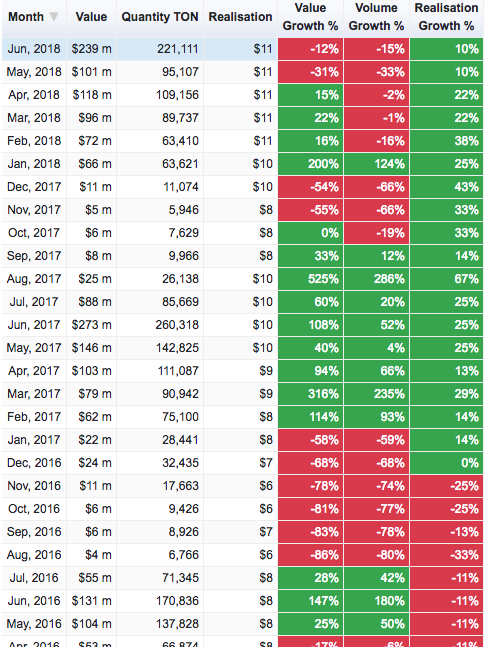

Thanks for data. Data is upto Q1…is it March or June?

Please note that in March Qtr Iranians currency was comparatively strong but presently it is too much down

KRBL

| 5 Years: | 14.06% |

|---|---|

| 3 Years: | 2.66% |

| TTM: | -5.43% |

LT Food

| 5 Years: | 18.24% |

|---|---|

| 3 Years: | 9.93% |

| TTM: | 11.62% |

Just want to compare both. Sales of LT foods are growing. And also available at less PE @ 12. Both stock has corrected more that 50%.

Considering the so much smoke in KRBL, Does any one think LT is more attractive? Is there any benifit to LT due to these allegations?

Can someone shed more light as i am newbee…after going through whole thread LT sound a good investment as both stocks have corrected…and LT seems less risky?

3 Likes

You should compare debt levels also. LT Foods is swimming in debt

1 Like

KRBL Ltd FY18 Annual Report Notes

Company performed poorly in the domestic market but showed good growth in the export markets. Company launched several products in organised branded market, specially in the lower price range segment to give competition to the unorganised basmati segment. Following are the highlights from AR2018.

- Consolidated revenues grew by 3% to `3264 cr. on account of better price realization of rice both in domestic & international market and higher income from Power, Furfural oil & Glucose Business.

- Highest ever EBITDA of `792 cr. , an increase of 21% over 2016-17. EBITDA Margin stands at 24% as against 21% in 2016-17. Gross margins were the main driver for good operational performance.

- Highest ever Profit before Tax of `655 cr. , an increase of 22% over 2016-17.

- Highest ever Profit after Tax of `434 cr. , an increase of 9% over 2016-17. PAT Margin stands at 13%.

- KRBL has four rice processing/grading plants which are based in Delhi, Punjab, Haryana and Uttar Pradesh. The Company also has a modern packaging and foodgrain warehousing facility at Alipur and Barota units.

- Company’s energy portfolio of 146.94 MW consist of 114.35 MW in Wind Power Projects, 15.00 MW in the Solar Power Projects and 17.55 MW in the Bio Mass Projects.

- The total sales for the financial year 2017-18 from agri division was

3,122.81 Crores, as against3049.65 Crores in the previous fiscal. Rice sales accounted to 91.39% of total revenue from operations. Export sales grew by 19.14% in comparison to the previous year. Middle East region accounted for 25.77% of the Company’s total revenues. - The Company reported export sales of Rice for

1,299.90 Crores in the 2017-18, an increase of 20.16% from1,081.80 Crores in the corresponding period of previous fiscal year. It derived around 40% revenue from the international market with strong presence in Gulf Cooperation Council (GCC) countries apart from other countries like Australia, USA, UK, Singapore, South Korea, Germany etc. Ventured into new markets like Europe, especially Netherlands, Belgium, Sweden, Guadeloupe, Germany. - KRBL’s sales from domestic rice business was to the tune of

1667 Crores in 2017-18, compared to1822 Crores in the previous fiscal. - The average selling price for branded Basmati rice was up by about 30% in 2017-18, compared to the previous year. Imposition of GST was one of the reasons for the price increase, besides other market factors.

- The sales in bulk packaging segment in FY2017-18 grew by 6 % in value terms as compared to last financial year. Some of the Company’s prominent institutional buyers in this segment include Taj Group of Hotels, The Leela and ITC Hotels.

- At 195 MT/hour, KRBL has the largest rice milling capacity in the world.

- Its flagship Basmati Rice brand India Gate commanded a 35% market share (in branded Basmati rice segment in value terms), the highest market share for any company in the sector in the combined urban and rural areas in 2017-18, an increase of 3% from the previous fiscal.

- While the overall industry growth in this segment stood at 16.5% in volume terms and 21.3% in value terms, KRBL has achieved a 27.6% growth in volume terms and 36.9% growth in value terms in the consumer pack segment in the fiscal.

- The Company has launched India Gate Jeera Rice brand in the southern region market in 2017-18, which has been well received by consumers in that market, going by the sales figures in the first year of its launch.

- Launched India Gate Sprouted Brown Rice. filed for patent on the manufacturing process of the product.

- Due to high inventory company had very little CFO of Rs. 41.66 cr.

- rice being a highly price sensitive item, absence of GST on loose rice being sold could be a dampener in the acceleration of growth rate in branded rice segment.

- India’s rice exports surged 18% from a year ago to a record of 12.7 million tonnes in 2017-18 and accounted for more than 25% of the global rice exports.

- The surge in the country’s rice exports was mainly on good demand for non Basmati rice from Bangladesh, Benin and Sri Lanka.

- The surge in exports came riding on the back of an increase in domestic rice production, which was expected to touch a record 111.01 million tonnes in 2017-18, up by 1.2% from the previous year’s level.

- To give impetus to rural economy, the Union Cabinet, in its meeting held on 4th July 2018, has increased the Minimum Support Prices (MSPs) of all “Kharif Crops” including that of Non Basmati Paddy from

1,550/- per quintal to1,750/- per quintal. This may lead to higher area under irrigation for Non Basmati Paddy, and may result in the increase in prices of Basmati Paddy also. - Rice production in 2018-19 is forecasted at 493 million tonnes, up from 486 million tonnes in 2017-18. Rice consumption also is forecasted higher, at 493 million tonnes, as against 487 million tonnes in 2017-18.

- The major export markets for Indian rice are the Middle East, Africa, the EU and the US.

- Basmati rice, cultivated in some selected areas spread over from UP to Kashmir, with Uttarakhand and Himachal Pradesh including, constitutes only a small portion of India’s total rice production, around 6% by volume. However, in terms of value, Basmati rice exports account for about 60% of the country’s total rice exports.

- The introduction of higher yielding PUSA Basmati 1121 variety in 2003 and shorter duration semi-dwarf PUSA Basmati 1509 variety in 2013 has supported strong growth in Basmati rice production in the last two decades. The new variety is being increasingly adopted by farmers due to shorter growth cycle, lower irrigation requirements, and higher yields compared to other traditional varieties.

Regards

Harshit

12 Likes

Harshit -

Thank you for your through review on the annual report. Did you find any guidance on why the company sales were only 3% up even with the strong export growth? Does management discussion speak of reasons for not showing expected 10-15% growth in revenue in domestic market? Also - I was wondering if you came across any guidance for future revenue growth.

Thank you in advance

Abhishek

Hi.

Management did not gave any guidance for future. Focus was more on launching more products in the organised segment, going forward that will remain the focus area for domestic market.

Sales growth was tepid due to degrowth in domestic segment, GST on organised segment and cheaper products from unorganised players was given the reason for degrowth.

Regards

Harshit

Is the reason given by management is true or reason is default from Iran? As per an article, export has hit in June qtr due to default

I might be wrong but my assessment goes like this. It seems the revenue hit is more due to Ramzan shifted by one month (The management mentioned it in the concall too about this). The importers in gulf countries buy more a month or two before Ramzan. So, the preponement of Ramzan by month (it seems every year Ramzan gets preponed by a month) shifted some revenue to previous quarter. The current quarter was bit tepid as exports don’t buy much during Ramzan month.

The 200 cr worth goods getting stuck at port might be routine thing and management might have used it as excuse. It might be partially true up to may be 50 cr or so [this is purely my guess].

Management is still closely monitoring Iran situation, so no specific guidance on that. They clearly stated that they have no amount involved in the Iran default. They also said they do very less business with Iran (about 5% of revenues).

The management was not very forthcoming in their answers to either augusta westland (they deny it in a single line) or about not owning the India Gare brand for non basmati stuff.

Clearly it is headwinds time for KRBL (augusta, auditor, pesticide issues (this might blow big), raw material prices (increase in rice MSP causing paddy procurement price never going below 25 rs), GST, iran sanctions etc

Discl: Invested

1 Like

I liked your candid reply. I agree with you that Management is not transparent, the answers they were giving on concall was not convincing.

2 Likes