Hello @raksnair

Unfortunately, account and finance is not my cup of tea. You have better knowhow than me.

Let me request other VP friends for assistance with two queries raised by you.

2 Likes

@Worldlywiseinvestors - I remember you mention about something fishy in KPIT’s balance sheet in your Tata Elxsi video. Since nobody seems to be able to explain these numbers, would really appreciate if you could shed some light on this, perhaps.

1 Like

https://www.bseindia.com/xml-data/corpfiling/AttachLive/836e6efa-26b8-49a8-8610-a989307d9e18.pdf

KPIT to boost investments towards software-defined

vehicle solutions with a specific focus on middleware

1 Like

5 Likes

When is the Q2 Results of KPIT? Screener was showing it on yesterday (30/10/2021).

There was a board meeting on 30/10, and it will be continued on 1/11. KPIT notified the exchanges that the Q2 results will be considered on 1/11.

2 Likes

3 Likes

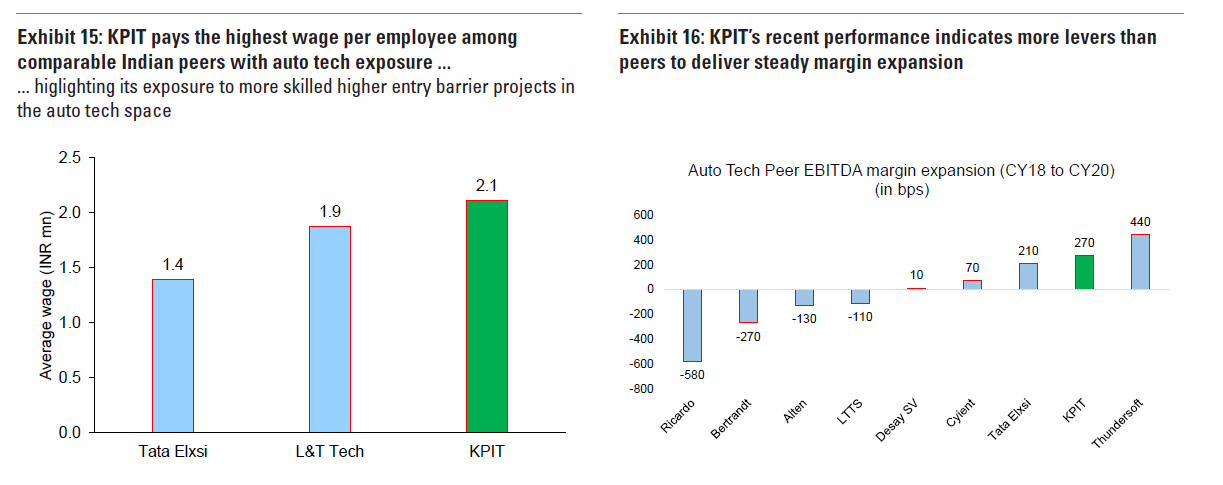

Numbers are very similar to Tata Elixsi in terms of revenue but there is a huge difference when it comes to employee cost. In a previous interview to Bloomberg CEO mentioned additional benefits had been given to employees because of COVID but also in general the employee costs are much higher. Does this protect the company from high attrition rates as well ?

3 Likes

Following are the main reason for low employee cost for Tata Elxsi

-

one of the big Tata Elxsi development Centre is in Kerala Trivandrum. Their they are having big advantage of very low attrition rate due to low living cost and most of the engineers are from KERALA itself.

-

Tata Elxsi is mainly focusing on offshore activity than on-site activity and also keen on 30% margin rules.

-

Tata Elxsi is having advantage of its brand value to keep the employs than KPIT

-

Tata Elxsi don’t have any development centres outside India other than on-site assignments and most of the engineers are on on-site assignments on deputation than recruiting from the on-site location. which will bring down the cost considerably

-

KPIT is mainly located in Pune , bangalore And Munich all are expensive city’s and of course the employee cost will also be higher

10 Likes

C4K configuration tool by KPIT ( Module tweaking, values retained etc.)

Classic - AUTOSAR configuration tool by KPIT")

3 Likes

Very good insights from Mr Pandit

Key Drivers of Automotive Industry

Clean Vehicles

Connected Vehicles

Safe & Autonomous Driving

Advance assisted Driving

All of these features translate into more electronics that are driven by software than hardware

KPIT to be treated as a partner by OEMs than a vendor

Research by Sapient Labs :

Working on Hydrogen Fuel Cell

Also working on Hydrogen generation by Bio-Mass (Technology , not into production )

2 Likes

Sharing 2 links here on KPIT

1 Like

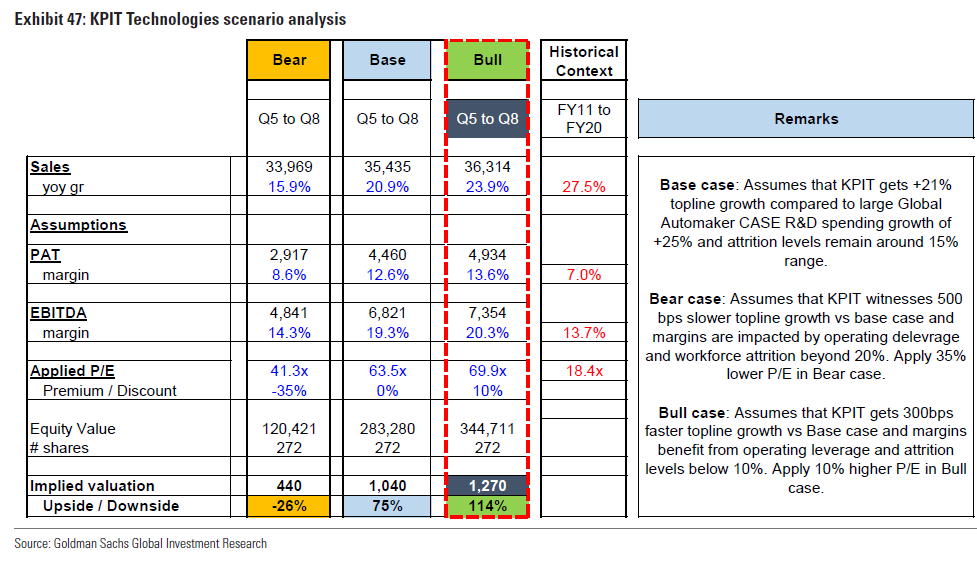

Excellent Report by Goldman Sachs

Latest update from Goldman Sachs

Key Industry Drivers

-

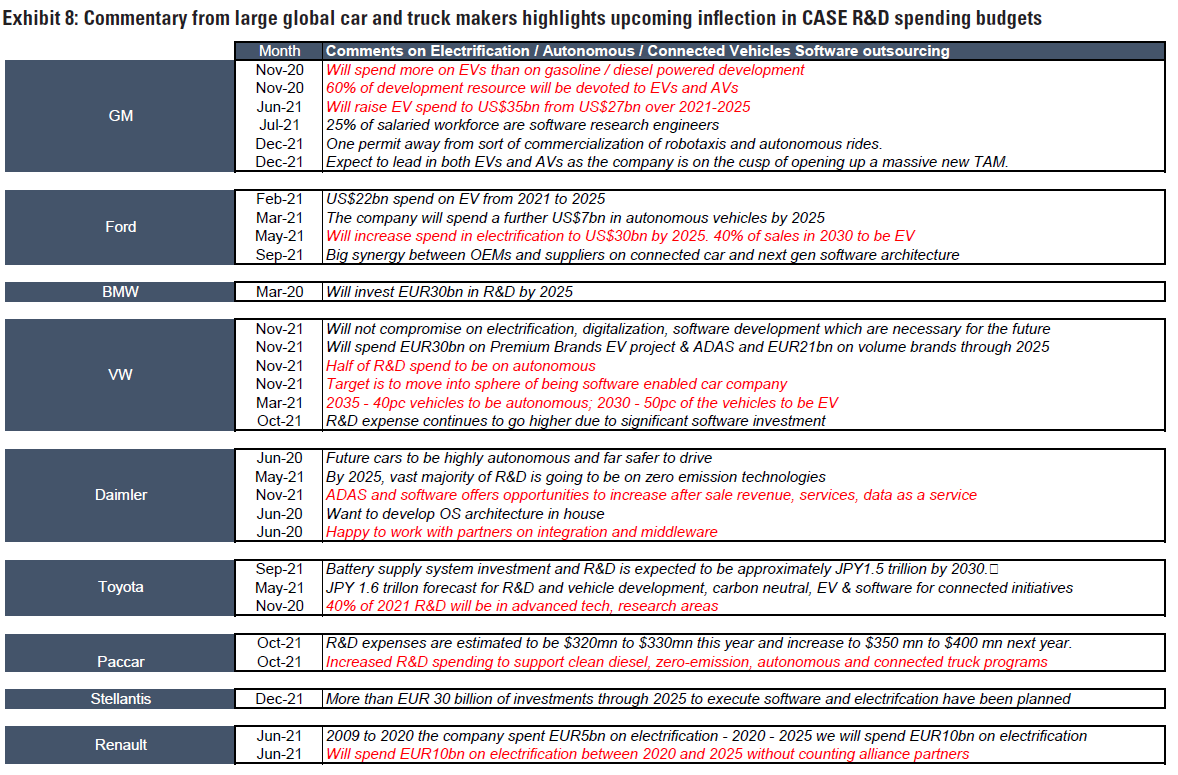

R&D spending on CASE (connected, autonomous, shared, electric) technologies at the top 10 global auto R&D spenders is poised to triple over FY21-FY26 to ~US$61bn

-

Europe’s CY35 ban on ICE vehicle sales has accelerated this shift.

-

Commercial vehicles CASE R&D spend may have started later, but catching up fast Driver and fuel are key variable costs for CV fleet operators: While the aggregate global market in value terms for medium & heavy commercial vehicles is smaller than passenger vehicles, the commercial vehicle category is especially relevant from an autonomous driving and electrification standpoint. The key variable costs for fleet operators in the CV arena are driver cost and fuel.

Autonomous and electrification to help boost CV fleet owner profitability: Autonomous driving technologies and electrified powertrains help do away with both of these costs and promise a more cost effective and profitable operation to trucking and logistical service operators to start with in the short haul categories for BEV technologies and eventual hydrogen fuel cell powertrain potential for long haul vehicles. Despite a later start, the criticality of these technologies to customer profitability indicate a faster pickup in CASE R&D spending for commercial vehicle manufacturers going forward, albeit off a smaller base than passenger vehicles.

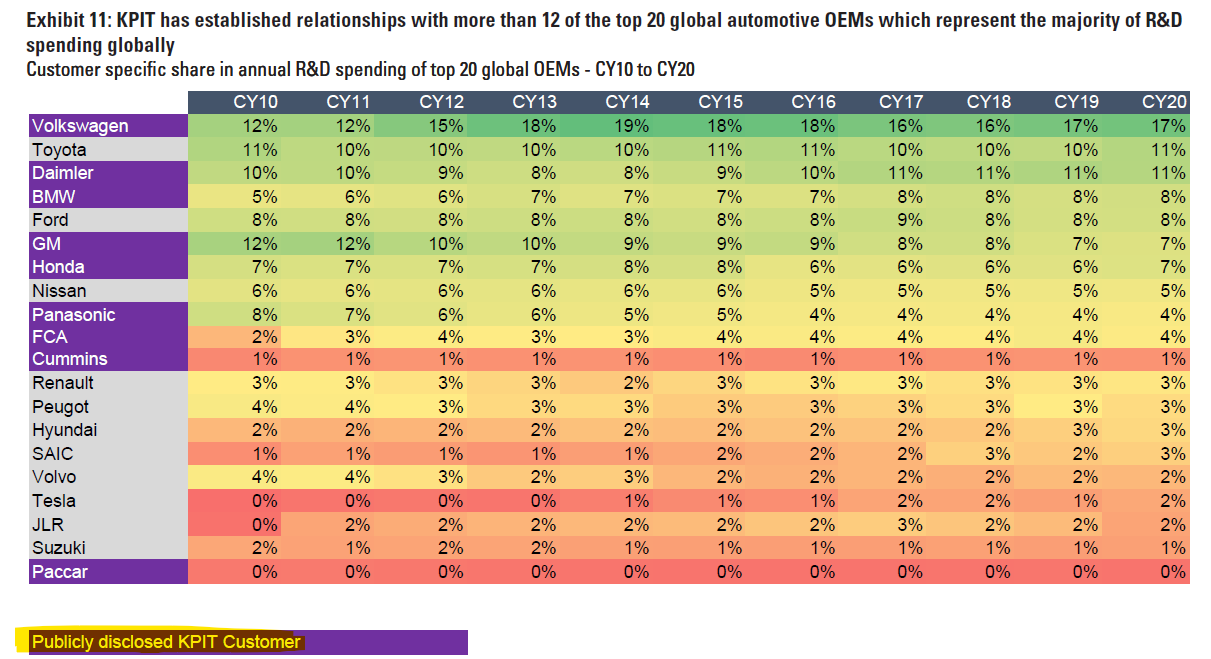

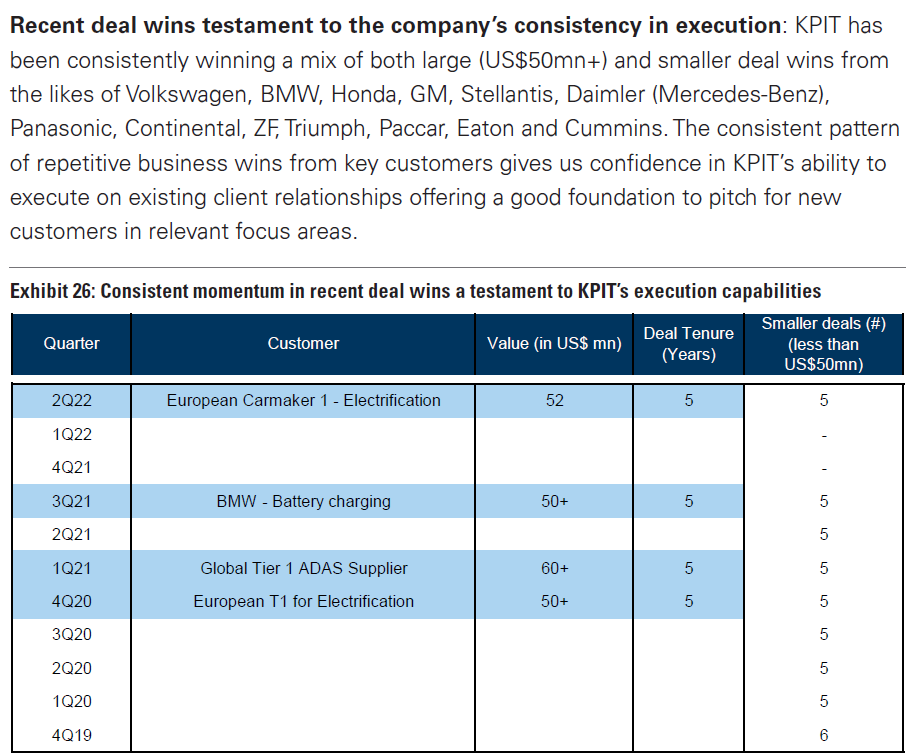

KPIT’s CV vertical well placed to capitalize: With established relationships at truck makers including Volkswagen (SCANIA, MAN, Navistar, Traton brands), Daimler, Paccar and Eaton; KPIT has been winning a lot of its recent deals in the CV arena. Consequently, we expect the company’s CV vertical (~25% of revenue) to grow in the low to mid 20% range annually over FY22 to FY25 vs the passenger vehicles segment (~70%+ of revenue) where we expect ~19% growth.

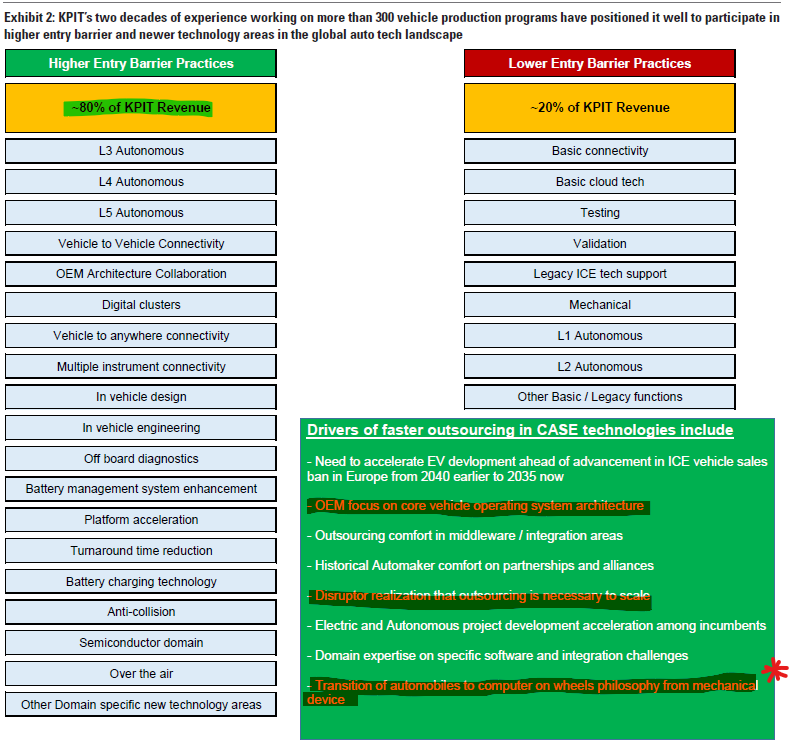

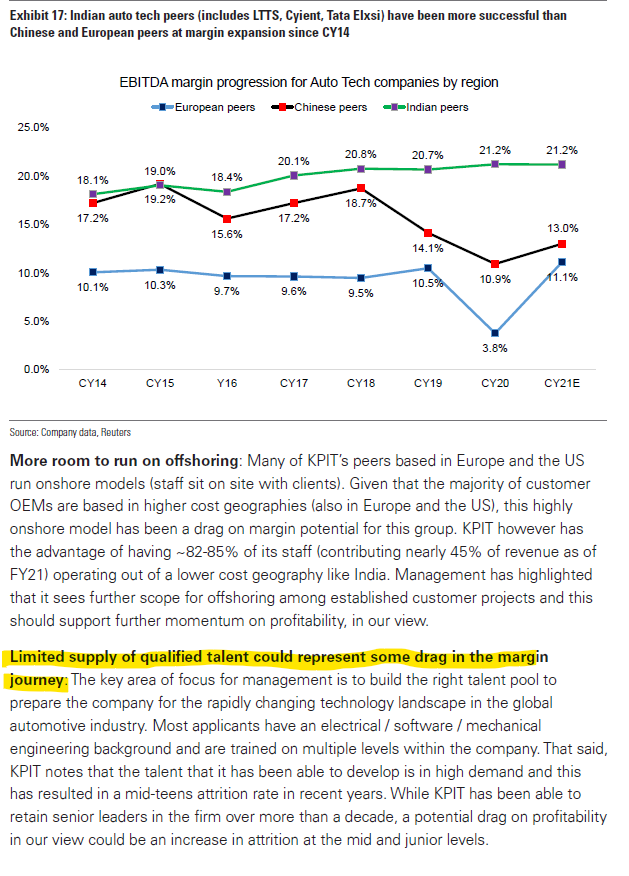

Outsourcing in middleware and integration likely to grow, though core OS architectures may remain in-house: Judging from previous cycles of R&D outsourcing observable in industries like pharmaceuticals (clinical trials outsourcing + drug development related outsourcing), we believe that the non-core parts of technology development are prone to more accelerated outsourcing than the core areas. For perspective, drug manufacturers have consistently tried to shift their focus towards core innovation and drug development and have been increasingly outsourcing non-core functions like clinical trials management and manufacturing to more specialized and scale players to variabilize their costs and extract more operational efficiencies from specialized partners. In this context, only ~15-20% of auto tech functions today are outsourced, though the rate of outsourcing in CASE R&D functions could be slightly higher, in our view. While we are still in the early innings of electrification and autonomous R&D spending, we believe that (1) more supporting functions in the auto tech landscape will be outsourced in the future; and (2) more disruptors looking for a path to operational efficiency will look to outsource parts of their auto tech spending functions; as both sets of companies look to scale their ambitions in electrification and autonomous driving functions. That said, we do not expect a high degree of outsourcing in vehicle operating system architectures which are more core to OEMs’ ability to differentiate the customer experience.

Customers have muscle to invest through the cycle: KPIT’s customers which include many of the top 20 Global OEMs as well as large T1 suppliers, are all longstanding automotive manufacturers with strong balance sheets. These companies understand the importance of investing in new product and powertrain projects through the cycle and many have gone on record through the Covid-19 pandemic, reinforcing their intent to do so. The balance sheet strength and regulatory as well as competitive factors behind the ongoing switch to electric powertrains and autonomous vehicles, give us more confidence that KPIT’s earnings prospects are relatively sticky and less prone to disruption by short term demand variations in the event of demand peaks / trough in the more cyclical global automotive sector.

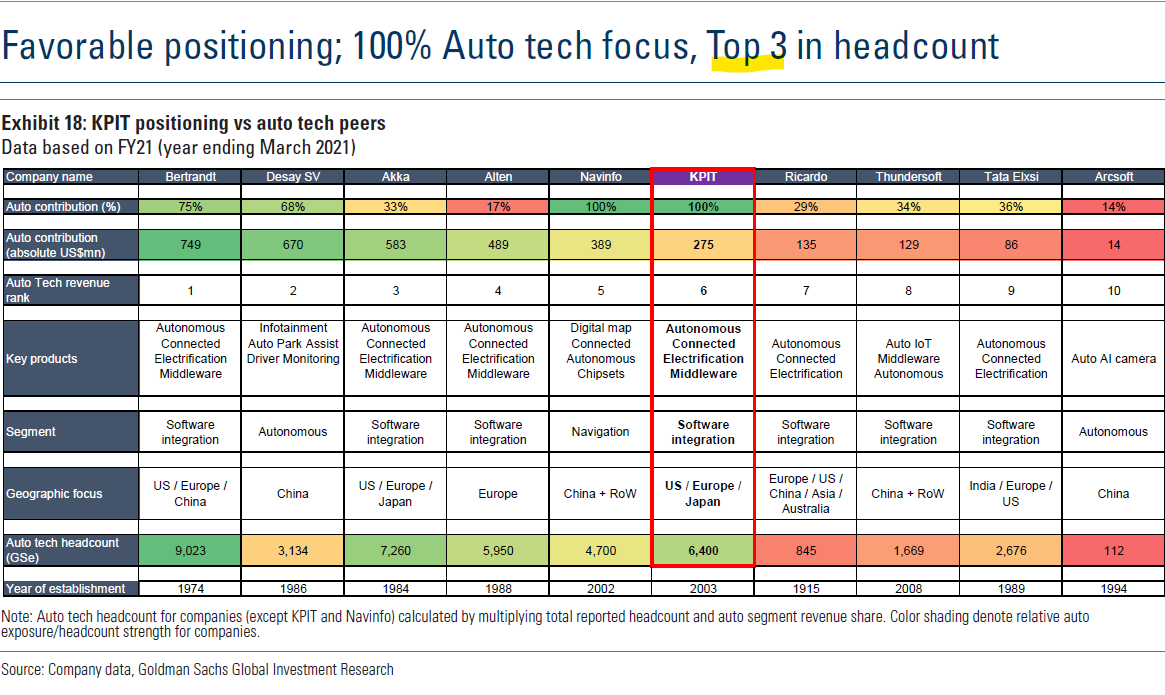

KPIT Strengths

- KPIT is uniquely positioned as a 100% automotive software integrator helping large OEMs accelerate their R&D projects in CASE related production platforms. We believe KPIT’s expertise in

(1) high entry barrier areas like L3-L5 autonomous driving, vehicle to anywhere connectivity, digital clusters and battery management system enhancement; combined with

(2) a strong talent pool (3rd largest auto tech talent pool globally), position it well to gain wallet share in the rapidly growing CASE R&D arena.

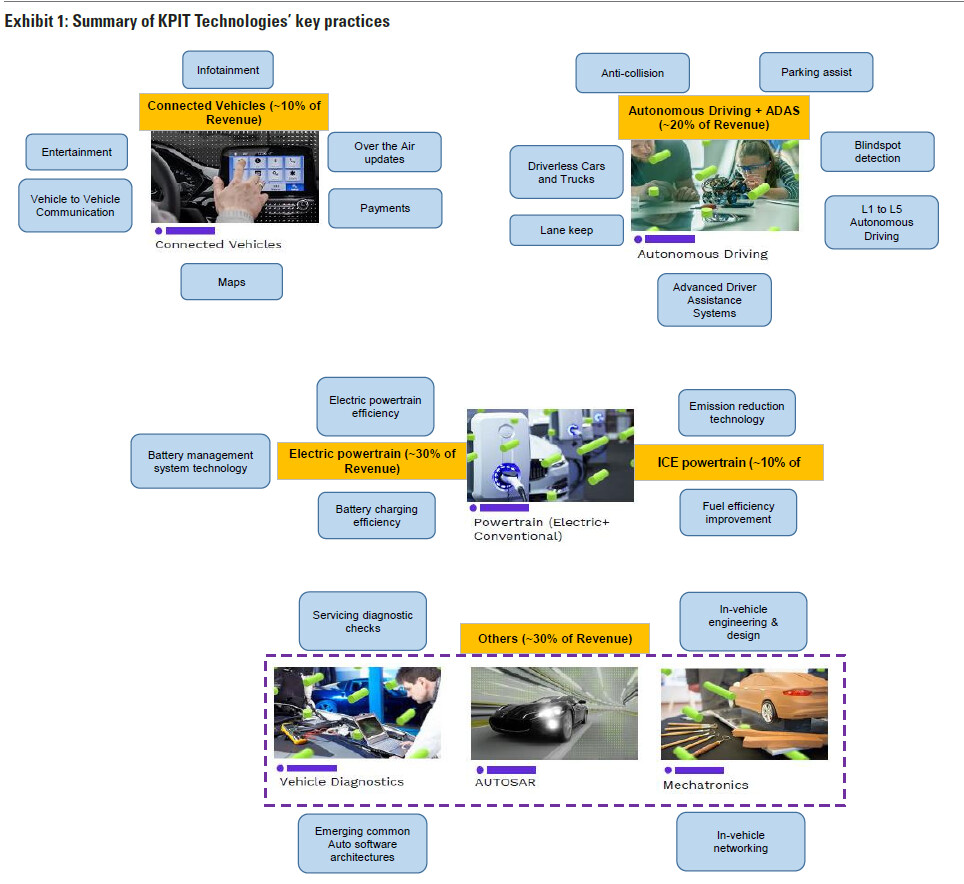

Broad range of services: In comparison to some peers which are exclusively focused on segments like autonomous or navigation, KPIT offers a broad range of CASE solutions to customers including Infotainment, electrification, autonomous, mobility solutions, vehicle diagnostics and other middleware solutions.

Geographic focus on US and Europe an advantage given faster electrification in these markets: KPIT earns ~80% of its revenue from Europe and the US. Our global autos team is of the view that EV penetration will pickup fastest in Europe and then the US / China over 2020 to 2030. We believe the company’s headstart in having established strong client relationships with large customers in these two geographies will help accelerate medium term growth.

Next gen companies on KPIT’s radar include disruptors + chipmakers + Big tech + 5G Telecom

KPIT’s experience in accelerating development of electrification and autonomous driving programs at a broad range of automakers have given it the requisite domain knowledge and expertise to now offer potentially nicher and more specialized offerings to disruptors in this space, in our view. KPIT has highlighted that it is in the process of studying the requirements of the disruptor set including companies like Lucid, NIO, Rivian, Tesla as well as tech giants like Microsoft, Apple, Amazon among a broader group of close to 10 newer age companies interested in the mobility and autonomous space. Additionally, KPIT notes that it is also working closely with semiconductor companies to help them sharpen hardware-to-software integration with core automotive OEM clients. Given that autonomous technology would need to be supported by a strong 5G connectivity backbone, we believe that telecom companies too over time would become more interested in the CASE technology landscape.

Triggers

(1) potential addition of semiconductor and EV disruptor companies to the client base

(2) further inflection in CASE R&D spending to support rising EV sales ratio targets

(3) margin potential led by increasing share of work in newer technology areas

Catalysts

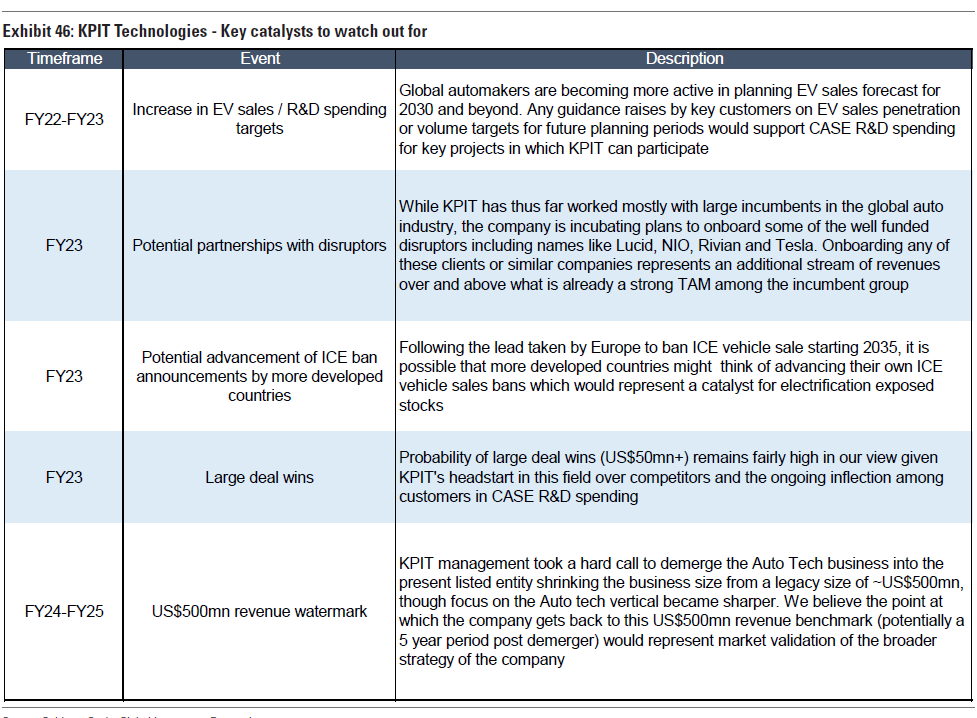

Going forward, we see the following events as potential key catalysts for the stock; (1) Potential above consensus growth in EV sales momentum in various parts of the globe as decorbonization and electrification themes gain momentum; (2) Evolution of partnerships with EV disruptors from the current pilot stage to more full fledged projects as disruptors look to scale profitably; (3) Further regulatory updates incentivising EV and autonomous vehicle platforms in more countries; (4) Deal wins in excess of US$50mn with specific customers tend to boost medium term revenue visibility for a company of KPIT’s present size; (5) Pace of progress in lead up to US$500mn revenue watermark which was revenue level of the company pre-demerger in 2019.

Key Risks

(1) Attrition in skilled talent pool;

(2) Slowdown in auto tech outsourcing;

(3) Vendor consolidation by OEMs;

(4) Revival in onshoring;

(5) Obsolescence of domain expertise; and (6) INR appreciation.

Some interesting slides

- Add to Asia ex-Japan Conviction List

13 Likes

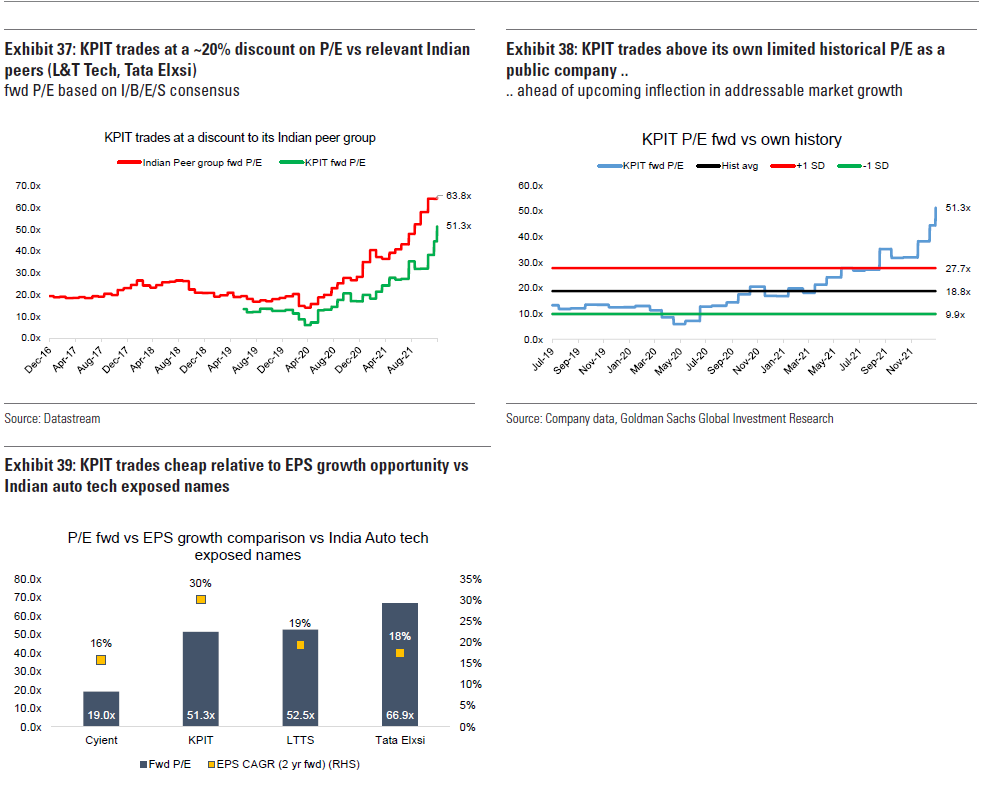

KPIT - What a a re-rating! I admire these Indian tech firms even more now. I have been tracking KPIT, although not very closely, since almost an year and what a story I have missed because of few factors like - Sector concentration risk may present sharp downside in case of any adverse situation arising, various metrics not as good as say a Tata Elxsi, not the best of promoters in technology space, lack of engineering ecosystem like an L&T or Tata promoted LTTS & Tata Elxsi… (invested in both)

As alternative I did invest in some Foreign MNC IT companies (OFSS - although not services company but still had huge scope of growth as Saas products, cloud offerings and what not) which lacked growth by huge huge margin in last few years.

One big learning - In India, invest in India…invest in top notch and as well as growing Indian promoters rather than Foreign MNC if you seek growth and re-ratings. Foreign MNCs are already valued to perfection and in most of them their promoters lack the zeal to go on to the next level. They are more of a sustainability investing rather than a creation…and what a company KPIT has created for the next leg of growth in EV automotive space…

Disc: Not invested in KPIT but tracking. Invested in LTTS, Tata Elxsi & OFSS named above. Not a buy/sell recommendation, only thoughts on business and admiration of the transformation in KPIT that I have observed in last year or so. I maybe wrong in my assessments above and KPIT or any other stock price movement may go either side, but the business is certainly taking right decisions & execution…

12 Likes

Hi Rafi

Thanks for sharing. How can we get access to GS research reports?

Thanks in advance.

actually they have tied up with dSPACE GmbH ( kind of middleware) along with Microsoft Azure (cloud) in almost 1 or 1.5 month back, this news & goldman report results in this rally , also last month cop21 summit the buses were used there by Alexander Denis which runs of kpit’s software, it’s a service provider to the disruptor, so can imagine the capabilities it has, the management has been extremely focused & believes in innovation & budding talent ,'Kpit sparkle ’ every year the get many budding talent those who are highly belief in innovation not copy pasting code like other IT co

5 Likes