The deal with Pathpartner is done at 2x sales. It seems reasonably priced.

However, pathpartner also have product/services in the non-automobile area. Don’t know what KPIT will do about it?

Awaiting more information… Do fw if anyone come across.

The deal with Pathpartner is done at 2x sales. It seems reasonably priced.

However, pathpartner also have product/services in the non-automobile area. Don’t know what KPIT will do about it?

Awaiting more information… Do fw if anyone come across.

I have invested in both KPIT and LTTS.

LTTS Ceo mentioned Autonomous and connected vehicles many times post Q1 result commentary. He indicated this as a big growth area for LTTS in the coming years.

Expecting good results of KPIT.

Please note that this expectation may be priced IN.

Disc: As indicated above.

Q1 FY 22 results

Good results.

Conf call is not on the Youtube channel of trendlyne.

You may access it from here

https://drive.google.com/file/d/1eUzRrbGvzm8oC7IEGaCA_z0WxsEQGgic/view

Takeaways:

Attrition is at 20% in H1 which will be under control in H2

Given good increment but that won’t affect margin

Captured 2 china new-age clients (2 out of 4 new age EV players)

The wage hike will be effective in Q2

1000 employee plan for the addition

We are larger than typical IT companies (as ex Accenture) in a domain we work

The work we do with OEM is very important for them as well; hence we get desirable attention.

Fix project is increasing, that is good for our margin, utility and also more competitive.

Pardon mistakes as it’s hard to listen without captions.

Disc: Invested

@Rafi_Syed - Q was there in concall.

The division was separated from KPIT, as it was decided that KPIT will have focused efforts on software. As per management, KPIT has ZERO involvement, not capital nor manpower.

However, in future, if any gain then the majority of those gains will flow to KPIT through a separate royalty arrangement.

Seems nothing significant…

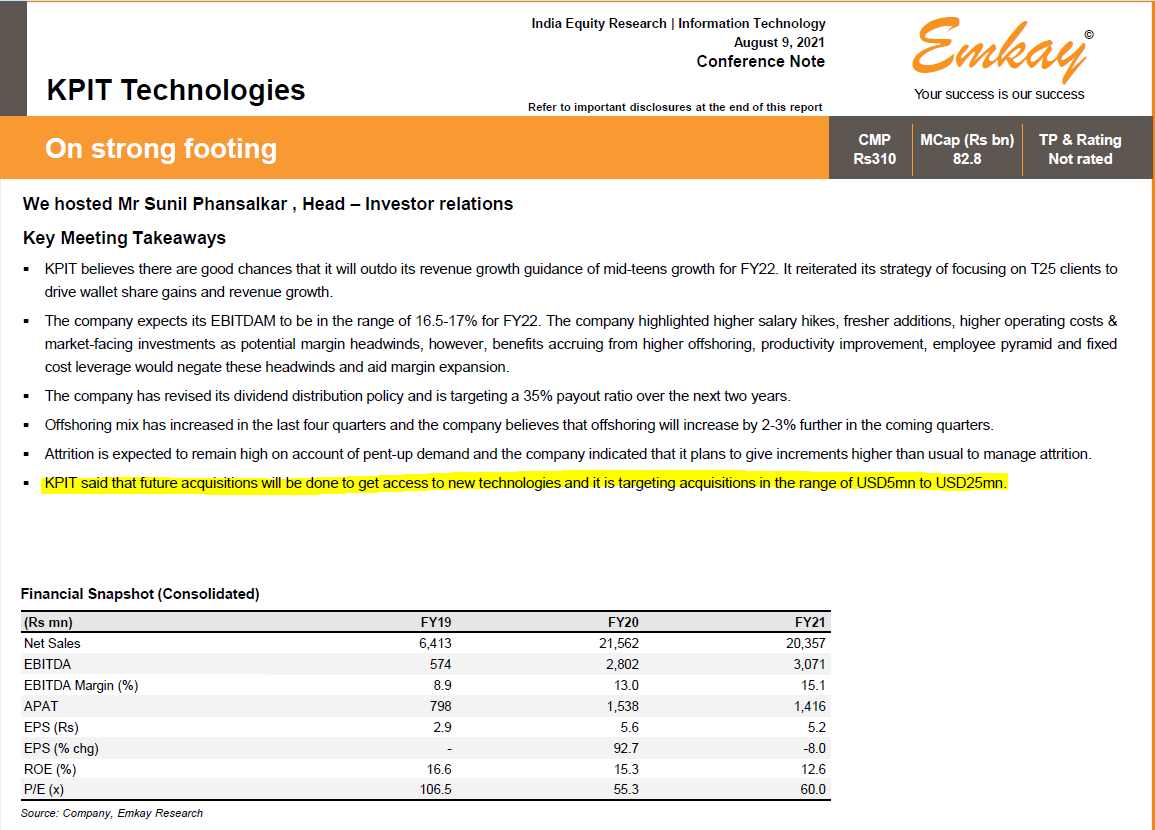

A few key takeaways from the recent concall:

Growth est. to be mid-teens for FY22 (Growth of mid-teens is organic growth, any additional deal wins or acquisitions (like Pathpartner) are not included in that)

EBITDA guidance for 16.5 - 17% for FY22

Focus on T25 for growth - mining these clients more - Mentioned that they could potentially 2X, 3X size of the company if they can utilize the spend of these clients well.

Plans to look at acquisition opportunities also, but very carefully so there will be no dilution with acquisitions

Plan to focus on passenger cars and commercial vehicles, not looking at 2 wheelers for now

PathPartner acquired to strengthen positioning as software integrator at a lower level i.e. semi-conductor level (to get access to semi-conductor technology and expertise, which the company believes is a key reason). Pathpartner will be integrated not operated independently.

Doing more fixed price projects - est. to be in the same range as now - fixed price projects helps them to be more competitive - also more margin accretive

Discl. Tracking position

Does anyone have an idea why KPIT is added in ASM list (Stage 1) by NSE ?

Also, does anyone knows or can share any resource that provides information on co-relation if any between any company being added to ASM list and it’s Circuit Limit being reduced (Ex from 20% to 5% etc)

From last Q presentation: Sentient Labs Pvt Ltd is a research and development focused company funded by Proficient, one of the promoter entities of KPIT. From the beginning of the year 2020-21, Sentient took over the further development of the above hardware-led research activities. Sentient would now be actively seeking different models for monetization, including bringing a majority investment from operating or financial investors. Sentient along with the new investors will decide on the appropriate way forward, either as a complete product licensing or outright sale to third parties or other monetization opportunities. The new majority investor or operating partner along with Sentient will explore appropriate options for building an independent management team, along with new investors…

This is behind paywall, if anyone has access please summarize .

Acquisition areas for long-term growth

KPIT is keen on acquisitions in areas like semiconductor and e-commerce to get better insights into how it can create value in those areas for its automobile customers

Other Points

Changing dynamics(around 18 new EV launches are expected in the US next year) and higher growth for the tech-driven solutions continues to increase

OEMs were used to buying software but now as the software itself is becoming the key differentiator, automakers are looking at doing their own software architecture

Within autonomous vehicles, most companies are not investing in full autonomy but advance level assistance features

KPIT is also keeping an eye on the next big disruptors, the company is engaging with them because it does not want to be blindsided by their success

It’s an 8 month old video, though not shared here, video wrt hydrogen fuel, where we stand and KPIT involvement.

@Deven - is this about Sentient Labs? This article suggests so.

There seems to be an expense item of 8.4Cr to Sentient Labs in the 2020-21 Annual Report. So the management saying there is zero capital involvement seems incorrect.

Please do correct me, if I am understanding this wrong. New to the exciting world of Annual Reports and Concalls!

Yes @Deven these 2 pages mention an 8.73Cr “reimbursement of expenses”.

Also, I was curious if you could find an explanation to the huge % of “Misc expenses” in their statements, especially compared to a peer like Tata Elxsi.

For KPIT, this figure at 28.9Cr forms around 20% of their “other expenses”, 4% of “total expenses” and 30% of PAT.

For Tata Elxsi, this figure forms just 0.5% of “other expenses” at 1Cr.

While the space they are working in seems pretty interesting, these weird observations in their Annual Report is making me circumspect.