Hi Ankit,

Is it mentioned anywhere ? Even in Sept 2019 and Dec 2019 they had similar high values for lease.

Hi Ankit,

Is it mentioned anywhere ? Even in Sept 2019 and Dec 2019 they had similar high values for lease.

Please check the link which i shared . All details related to Early Lease Termination is mentioned.

Is this something alarming ?

|Date|Person|Buy / Sell|Transaction Type|No. of Shares|Price

®|Value

| (R Lakhs) |

|---|

| 17-Mar-2021 | KPIT Technologies Employees Welfare Trust | Sell | ESOP | 3,400 | 157.20 | 5.34 |

| 15-Mar-2021 | KPIT Technologies Employees Welfare Trust | Sell | ESOP | 8,500 | 152.50 | 12.96 |

| 10-Mar-2021 | Kishor Patil | Market Sale | 10-Mar-21 | – | 159.65 | – |

| 04-Mar-2021 | KPIT Technologies Employees Welfare Trust | ESOP | 5-Mar-21 | – | 140.30 | – |

| 15-Feb-2021 | KPIT Technologies Employees Welfare Trust | Sell | ESOP | 28,500 | 134.35 | 38.29 |

Kishore Patil sold his pledged shares. Not alarming

Q4FY21 and FY21 results seem to be in line with management commentary. The investor update is available here.

My main takeaways are:

KPIT is currently at P/S of 2.62, whereas other companies of similar size like Tata Elsxi and LTTS are at P/S of 24.2 and 5.05 respectively. Will KPIT be able to achieve similar P/S levels? I am hoping so … but would welcome other views.

Discl: Invested, second-highest allocation in PF.

P/S - Is this the right metric to look at tech firms? Can you elaborate on this metric that you are using to compare and what makes Tata Elxsi to trade at significantly higher P/S. Looks like there would be huge difference in Profit margins between the two…

Thank you @Investor_No_1 for pointing this out. Indeed, NPM of Tata Elxsi is close to 20% whereas NPM of KPIT is only ~7% at present.

With regard to P/S, I heard in a webinar that P/S is a good metric to compare companies since sales cannot be easily ‘adjusted/tweaked’. It is a good metric as long as we compare companies in the same sector. I am unable to see why this is not useful for tech companies. I am new to investing and might be wrong. Please correct me if I am wrong.

So a difference of around 3X NPM but P/S difference of 9X…between Tata Elxsi and KPIT…

well P/S, I do look when comparing FMCG firms, it also forms important metrics for FMCG acquisitions. The idea would be that brands/acquiring company can work on margins as long as sales are good and keep increasing.

In case of tech firms, the main cost is employees, so I would not have expect a 3X margin difference and it looks unusual and not sustainable…what would be a usual margin profile for a normal IT services (say a TCS, Infy, LTI) and engineering tech (KPIT, LTTS, Tata Elxsi)…would make us understand which one is way off the mark and either not sustainable over very long term (if very high than median) or a red flag (if much below median - some may take it as opportunity if they trust the red flag is temporary and can be corrected)

Since Employee costs are high in case of Tech firms . I mainly look for Onshore/Offshore staff ratio. More offshore improves overall margin. While i may be wrong with this understanding because Company charges high for onsite work. If they can charge as per Onsite and still somehow compete the work Offshore Margins will improve. This is what happened due to covid and Margins improved for almost all IT companies(Providing no off event)

Patil asked him how they heard about KPIT. Apparently the client had asked tcs(if I’m not mistaken) who was their most feared client. And tcs replied KPIT. So the client came to KPIT.”

Reference video I found from youtube: Success Story from Pune: Ravi Pandit of KPIT Technologies - YouTube. I found interesting, hence posting.

Disc: Invested from lower level and added few weeks back.

Is there any reason for the current rally in KPIT ? I tried to find news/announcements but couldn’t find anything?

No specific news is there, from numbers - seems DII and FII increasing stakes (KPIT Technologies Ltd financial results and price chart - Screener). The stock got added in some theme based fund (as example small case fund of electric vehicle).

Disc: Holding and added on upward - recently added between 190-200 level.

From past few days it’s one way upward… Waiting for 50dma level to add second tranche “if” it comes there…But EV theme is not letting it come down

How unique is the technology that the company possesses? Can the reason for the lower margins, compared to other firms like Tata Elxsi, be the higher competition the company faces in its field?

Escapenet ( the European Patents Office) has the records for the patents filed by the company. One may also go through the USPTO site, for patents filed by the company in the US. Searching for TTL/“lane detection” in the USPTO site, will give the lists of patents filed by all companies with “lane detection” in the title. One can cross search the database with KPIT’s patent titles to see, how many companies have filed for similar technologies. I searched for the above and a large number of companies including Magna Electronics, Ford, etc. come up who have filed for patents with some sort of lane detection technology. While this may be a one off case, where large number of companies have developed this tech and the application and performance of the technology may differ, from one vendor to another. But it does raise the question on competition in the car software industry.

Disc- not invested, tracking

Hello,

What could we attribute to be the reason for Tata elexi getting higher margins ? What kind of value addition is Tata elexi giving which KPIT is unable to replicate ? Even Tata elexi upto 2014 was in similar OPMs as KPIT, it was since then the OPM started increasing substantially. If we compare Tata elexi and KPIT in screener, the major difference is other costs mentioned in KPIT expenses? What does this other cost include?

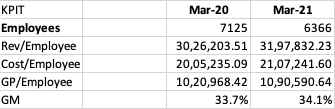

It seems Tata Elxsi is making higher margins due to lower employee expenses. KPIT has been able to generate more revenue/employee. KPIT did open a new technology centre in Munich for 700+ employees, which could explain the increase in cost/employee from FY20 to FY21. I’m not sure abt the reason for the higher employee cost- Tata bigger brand, KPIT paying more to retain existing talent…

Hello,

Interesting data. Which source are u using to collect these data ?

In screener both KPIT and TAta elexi has similar cost for employees but KPIT has additional 15% expense mentioned as others. Does KPIT employ more employees outside India compared to Tata elexi? if so that could explain higher employee costs.

Hey,

Got the data from screener download and AR.

Not sure about the employee locations

Kpit acquired PathPartner Technology.

Co. commentary on the same:-

-Strengthen KPIT’s software integration capabilities and help deliver

complex software solutions for new-age vehicle architectures.

Disc: Invested from lower levels.