Total consumption of coal will reach a record high of more than 8.5 billion metric tons this year, and then start a long, slow decline, according to the International Energy Agency.

Read more at:

Total consumption of coal will reach a record high of more than 8.5 billion metric tons this year, and then start a long, slow decline, according to the International Energy Agency.

Read more at:

QIP completed at 1183… and well know funds have taken a stake… This bull market will ignore all the CG issues… and that’s going on in all the companies till date

Small caps are always plagued with CG issues. Till the time there is an effort to consolidate & ramp up all renewable energy business under a single head , such related party transactions take back seats in Bull market unless there is a cash consideration involved.

Talks about growing at the same rate till 2030.

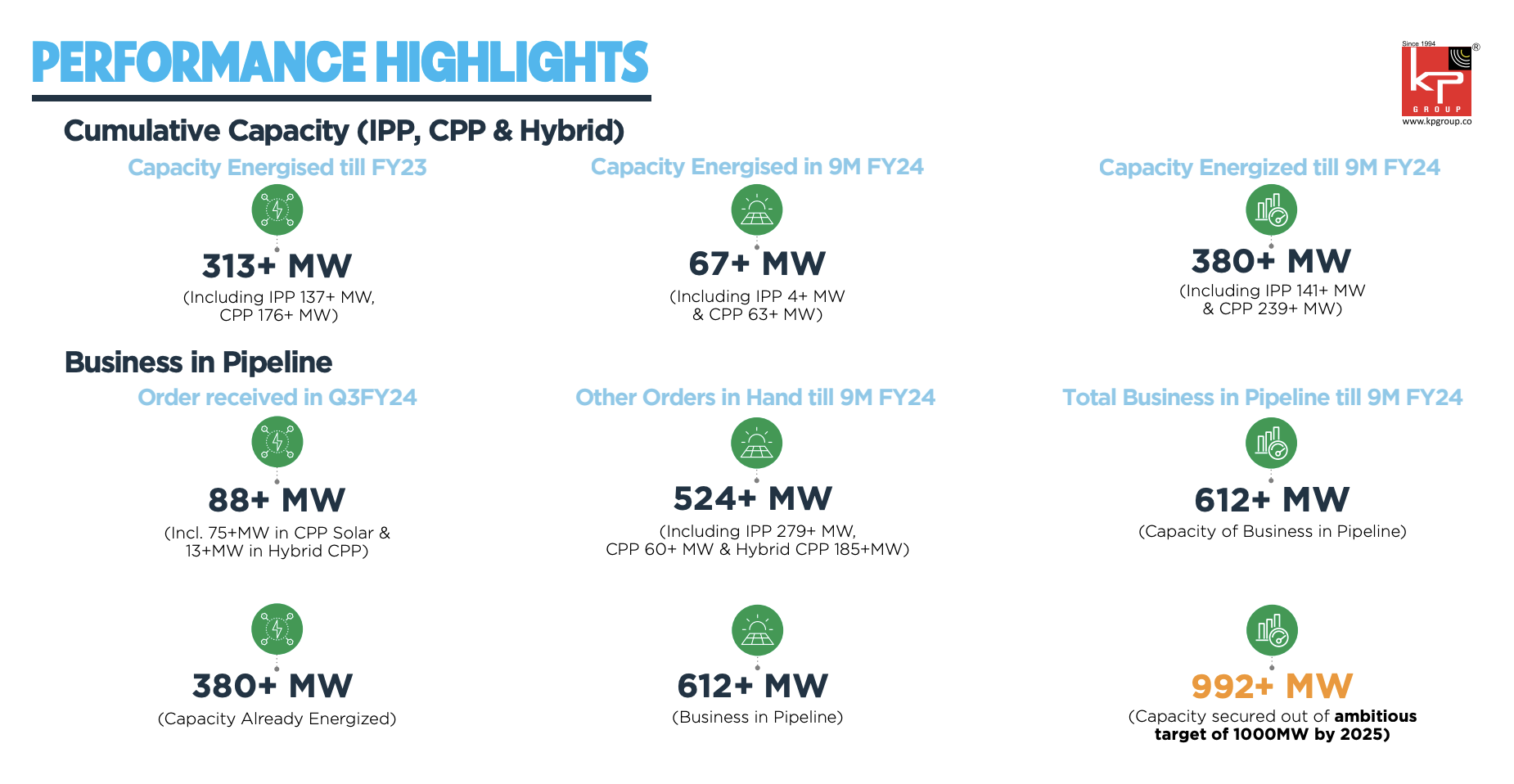

Company has an order book of 992 MW already. Planning to execute 1000 MW by 2025.

KPI Green Energy Limited Bags An Order For Development Of 305Mwac Solar Power Projects Being Part Of Wind-Solar Hybrid Power Project From Aditya Birla Renewables Subsidiary Limited And ABREL (RJ) Projects Limited.

This is very big order since till now they have just completed only 380MW of solar project.

This is still trading at only 70 pe while waarre and other solar epc are now closed to 140.

Can anyone confirm why there is so much gap in valuation.

Its debt…as per screener data kpi debt to equity is 2.58 which on higher side given its asset Heavy model. On the other side waaare is almost debt free company .

Also market discounting it behalf of foreword PE of only 57 if we calculate based on last eps which is 30.

Hope that help .or is there bubble .

I don’t know I’m still learning.

Disclaimer.Invested from1350 levels.

KPI is IPP Producer as well where they are giving the electricity to user on per unit basis which will give them good future cash flow in future as well when there is no solar contract and its high margin as well. So debt is higher due to that factor. Further after raising equity there debt to equity will go down to less than 1

Source - Rupeevest (Right to Left)

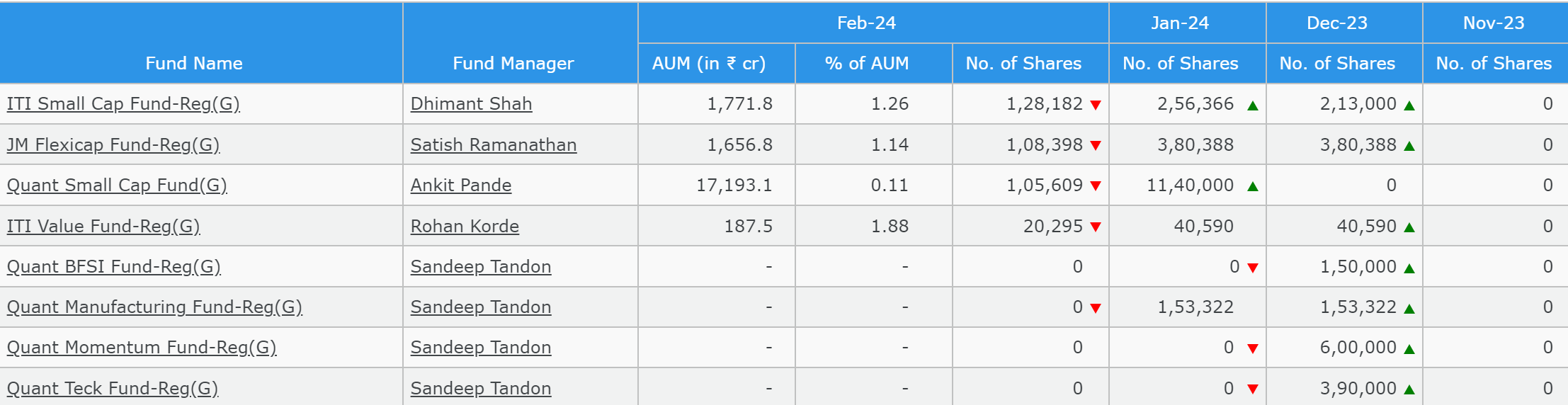

Quant small cap sold 10.35L shares to retail investors and Quant manufacturing fund took a 100% exit.

Sharing the latest numbers & Leadership’s perspective on current numbers & upcoming trajectory:

Fy24 Numbers - Investors presentation: https://nsearchives.nseindia.com/corporate/KPIGREEN_25042024214116_KPI_Investor_Presentation_to_exchnage_signed.pdf

Future trajectory: https://www.youtube.com/watch?v=fTQ7ClxmlBA

Disc: Invested in KPI Green, Would like to consider KPI Green Engineering with some rationalization to price

Why KPI green is falling for last 2 days., didn’t find anything significant.

decline in QnQ revenue/ eBITDA + market expectation were higher growth

The amount of orders pending to be executed in huge. Total Business in the pipeline is 1.23GW. if the company executes the orders with the same efficiency that it has done in the past then it has the potential to grow further.

The Share is down maybe because of the expectation of QoQ growth is not met. But IMO the company’s future looks bright as the requirement of green energy is all sectors in must and KPI green is poised to take this benefit being the early entrant in the field.

The company should do concalls so the retails investors can have more transparency about the operations and future aspirations of the company.

Disc. Holding from lower levels.

1 mw epc cost is 3 to 5 cr as per reference and 5ooo modules included in per mw as per rough calculations from tata power

as per 1.2 gw is pending of which 868 is cpp it means 868*4 = 3472cr revenue per mw potential in cpp and in ipp is how much any idea

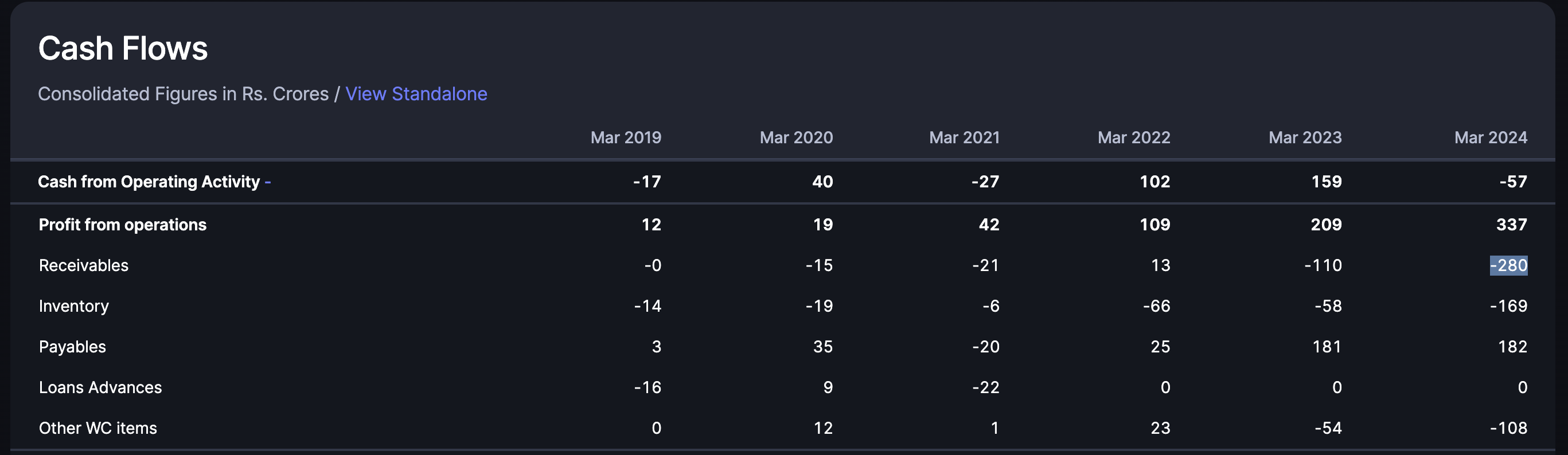

does anybody know why kpi this year in 2024 reported negative cashflow

calculate the peg then u will see the magic

I too had the same question.

According to this interview: it looks like the billing timeline for larger clients is different, leading to inventory days increasing.

However, I see a significant increase in the receivables as well:

Not sure why this is the case and is my concern as well.

Today there was an announcement from the group, where the promoter is being alloted shares of subsidary: bse filing.

I personally am not liking the corporate structure of the company. As pointed out earlier in this thread. Too many related parties and subsidaries.

This is one of the worst companies i have seen in CG. Reasons for this statement -

Only good thing about the company - Its in sunrise sector.

But i feel existing shareholders might have a hard time to make money from here in this counter.

Amtek was a similar case study. Amtek auto, Castex, MFL, ACIL, OCL, etc. went down (4-5 lac group) and had same things.

FCF is sum of cash flow from operating activities and investing activities which tells how much money the company needs to raise to sustain its normal operations/ growth plans (generally -ve in growth companies)

This money is raised through debt or issuing equity which can be seen under financing activities.