@SandyG bro how did you get the row for FCF on screener? I don’t see it in the cash flow section of mine…

somebody please do let me know. Thanks!

1 Like

check

and

5 Likes

Market is giving much higher valuation than intrinsic value then promoters will go for additional equity - leading to dilution. and low gearing. KPI is not raising debt as new equity is available at very high valuation.

in such companies, the valuation eventually comes down to realistic levels. but investors who came in during euphoria will lose out.

4 Likes

Good explanation, its time to pay tution fee for lot of new investors in lot of euphoric stocks in various sectors, market will test your temperament now and will segregate wheat & chaff.

1 Like

Extreme churning is happening and will keep continue, its a distribution phase in markets rightnow, we may see further fall of 10-30% in stocks which are quoting at astronomical valuations and analysts will also justify valuations. ![]()

![]()

Either stay away or book profits, staying put will test your conviction.

1 Like

Every one post message once share down by 10-15% and sit on sideline when share increase. The share valuation is high but promotors are buying from market. Big funds like Goldman and bofa have invested. This should be oportunity who missed it earlier. Valuation might be stretched at 1100 but future growth was also immense.

There is lot of competition in solar EPC and this is the reason for sideways to downfall move but the company have moat which is land and it’s IPP Business which will give them annuity and that is high margin business and management guided that it will be IPP devision profit will be higher than its current sales. Company have huge order book and company needs fund for it and that’s why they raise 1000 core. They even raise fund in begining at rs 40 at that time also there were same comments.

Disclosure- invested from very low levels and biased

8 Likes

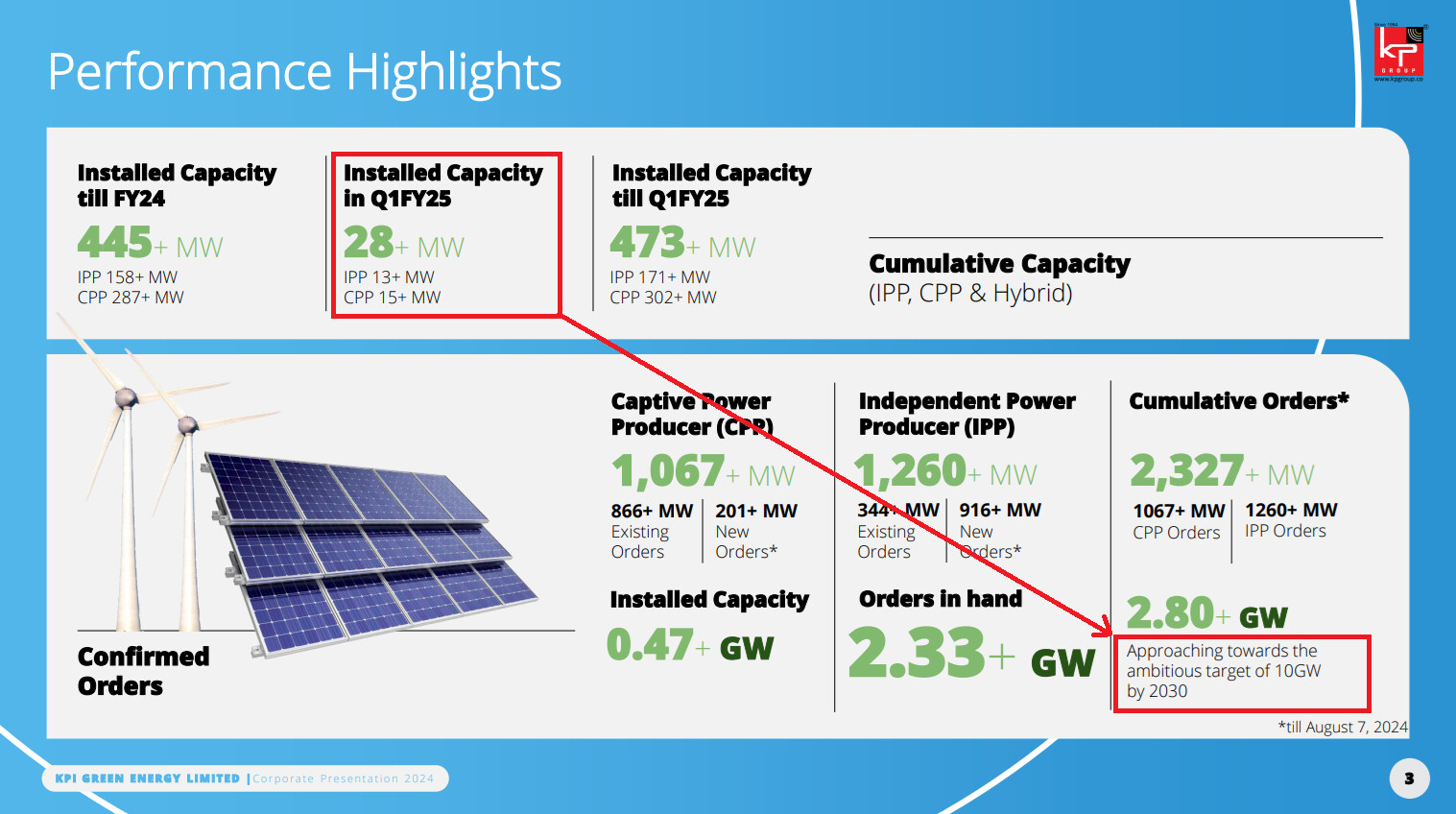

Company is aiming for 10GW by FY30.

When we try to translate that into equal quarterly growth the estimated annual growth (in terms of installed capacity) comes out as approx. 76.33% per annum.

| Expected Annual Growth | 76.33% | |

|---|---|---|

| Expected Annual Growth / 4 | 19.08% | |

| Quarterly Installed Capacity (MW) | Total Installed Capacity (MW) | |

| Q1 2025 | 28 | 473 |

| Q2 2025 | 33.3 | 506.3 |

| Q3 2025 | 39.7 | 546.0 |

| Q4 2025 | 47.3 | 593.3 |

| Q1 2026 | 56.3 | 649.6 |

| Q2 2026 | 67.0 | 716.7 |

| Q3 2026 | 79.8 | 796.5 |

| Q4 2026 | 95.1 | 891.6 |

| Q1 2027 | 113.2 | 1004.8 |

| Q2 2027 | 134.8 | 1139.7 |

| Q3 2027 | 160.6 | 1300.2 |

| Q4 2027 | 191.2 | 1491.4 |

| Q1 2028 | 227.7 | 1719.1 |

| Q2 2028 | 271.1 | 1990.2 |

| Q3 2028 | 322.9 | 2313.1 |

| Q4 2028 | 384.5 | 2697.6 |

| Q1 2029 | 457.9 | 3155.5 |

| Q2 2029 | 545.2 | 3700.7 |

| Q3 2029 | 649.3 | 4349.9 |

| Q4 2029 | 773.2 | 5123.1 |

| Q1 2030 | 920.7 | 6043.8 |

| Q2 2030 | 1096.4 | 7140.2 |

| Q3 2030 | 1305.6 | 8445.8 |

| Q4 2030 | 1554.8 | 10000.5 |

Now, even if we assume that due to rising competition, the margins of EPC players will shrink going forward; its still seems to be an impressive growth story. Lets keep on tracking QoQ.

Disclosure: Invested from decent valuations and biased.

7 Likes

I would like to add equity dilution for fund raise which would dilute EPS, still from 76% Annual growth even with dilution seems a very good bet with credible management and good players enterred via QIP

3 Likes

The group has been making confusing announcements - Publicly they always say 10GW as a group (KPI Green Energy, KPI energy and KP Green Engineering). This document says only for KPI Green.

1 Like

I think the management’s credibility is questioned here:

2 Likes

Disc: invested

4 Likes

Agree… sector is right… but many such equity buy/sell transactions being done to favor promoters… these transactions are as per the SEBI guidelines of pricing etc… but current valuation is too high. investors coming in now… will surely be at risk of loss…

2 Likes

Another subsidiary Sun Drops Energia Private Limited where promoter has taken stake… they dont even mention at what price… etc… most likely will list this company also at huge premium… again retail shareholders being shortchanged…

5 Likes

Results look solid enough by most parameters. Top-line 75% up and PAT 100% up for H1 FY25.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c73fa056-6ac5-4b80-b35c-d1a628604d88.pdf

4 Likes

pl compare with trailing quarter… then you will know why KPI is falling.

https://www.screener.in/company/KPIGREEN/consolidated/#quarters

Even in sequential terms, top-line and net profits have seen slight growth and are at record high levels.

Passing orders on to related entities is the company’s stated stated policy, is it not? It is how costs are controlled and timeline/ execution is ensured at better than industry standards. As long as KPI Green’s eventual results/ margins are not significantly impacted, it does not seem like a problem for shareholders.

Please note that I am a novice investor and looking to learn.

2 Likes

I am finding the company grossly undervalued right now. It’s P/E is at 44, less than half of Waaree renewables. PEG ratio lesser than 0.5. Great order book which is higher than last quarter and best ever quarter. Agreed company has debt but their interest coverage ratio seems to be decent.

5 Likes

Q2 is a monsoon quarter and hence not comparable to Q1

Company’s debt has come down by 600cr in Sep qtr. equity raised 1,000 cr.

company is replacing debt with equity?? does it mean valuation is high…

3 Likes

While KPI’s cost of equity is more than its cost of debt. I would look at it favourably. One major difference between Waaree ren and KPI is their debt. Waaree has virtually none. A lower debt can ease investor concerns and help in the rerating. Going forward, this will also help the bottom line. This quarter itself it was 23 Cr. 23*0.75=17.75 Cr addition to PAT

2 Likes