KPI Green Energy Ltd. (formerly KPI Global) is a Gujarat-based company engaged in the solar power infrastructure and generation business. They have two main verticals- Captive Power Producer (CPP) and Independent Power Producer (IPP).

Brief description of both verticals:

Captive Power Producer-

As a Captive Power Producer, KPI develops, transfers operates and maintains grid-connected solar power projects for CPP customers and generates revenue by selling these projects to CPP customers for their captive use requirements. The CPP Business is also carried out at plans located in Sudi, Bhimpura, Kurchan, Muler, Ochchan, Jhanor, Bhensali, Vagra and Vedcha villages of Bharuch district, Gujarat. KPI develops solar power projects on behalf of CPP customers by entering into a turnkey agreement enabling CPP customers to not only use a common pool of grid-connected land to establish and generate solar power, but also provide ready-made common infrastructures to evacuate power, using our transmission line from solar plants to the nearest GETCO Substation.

KPI also provides Operation & Maintenance Services (OMS) by entering into a separate OMS Agreement for 25 years with CPP clients ensuring a long-term annuity source of revenue.

Margins in this segment range from 40-45%

Independent Power Producer (IPP)-

Under IPP Segment, KPI develops and maintains grid-connected solar power projects as IPP and generates revenue by selling power units generated from our solar plants through Power Purchase Agreements (PPAs) with reputed business houses. The IPP Business is currently carried out from plants located at Sudi, Samiyala, Tanchha, Bhimpura, Kurchan, Muler and Vedcha villages of Bharuch district, Gujarat.

Margins in this segment are generally 70%+

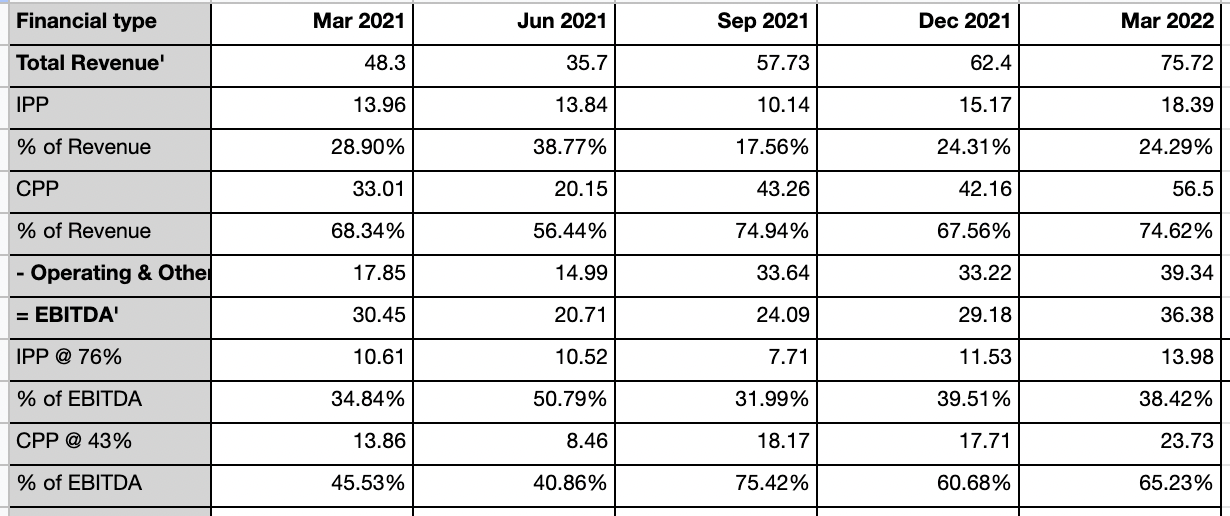

IPP has been a major focus area for the company due to its margin accretive nature which can be seen in its growth over the past six years-

Source- FY22 Investor Presentation

While the CPP segment is majorly topline accretive, the IPP segment is bottomline accretive. The same can be seen here-

Even while IPP makes a <30% proportion of total revenue, it accounts for a significantly higher proportion of EBITDA.

The margin figures for specific segments have been taken from this TV interview as the company consolidates both segments in its reporting.

What I like-

- Solar Power Generation as an industry has significant policy tailwinds in India. Aggregate capacity at the national level has gone up more than 20x in 6 years, with a target to further take it up to 300 GW (~6x that of current capacity). Budgetary allocations have been made for the same. The central government’s incentives can be found here. However, at the state level, the impact of policy may not be directly beneficial due to the introduction of banking charges of Rs. 1.5/unit, the overall policy thrust is towards encouraging captive use by industries.

- As companies look to score better on ESG metrics and reduce costs, they will look to reduce dependence on thermal power plants and look at captive RE sources.

- The promoter, Mr Faruk Patel has been working in the infrastructure and logistics space for almost 30 years.

- The most important factor for any infrastructure company is execution, and execution has been top-notch for KPI. In FY22 alone, the company added 51MW+ capacity in IPP. To put that into context- in H1FY21, the company had a 43MW IPP Portfolio with another 43MW underway.

- Robust order book- in the CPP segment, the company has an order book of 83MW+. To put that into context- since it has started operating, KPI Global has executed an aggregate capacity of ~65MW.

- Strong client base with long-term Power Purchase Agreements (15-20+ years) for IPP with companies like L&T, UPL, Cadila, etc as clients.

When I first bought, the company traded at roughly 4x trailing EBITDA albeit with a smaller execution record. It currently trades at 10x FY22 EBITDA (and a ~15x EV/EBITDA). However, management guidance is for 1000 cr revenue by FY2025- which at FY2022 Margins means 400 crores in EBITDA, valuing the company currently at <3x FY2025 EBITDA.

While I don’t normally take management guidance at face value- I have reason to be confident here due to their past track record. The present valuation even after a significant run-up allows enough margin of safety.

Concerns/Risks-

- Debt Levels- the company’s debt to equity is at 2. While cash accruals are expected to cover repayments and there have been interest savings on account of refinancing of loans, further expansion is expected to be met via internal accruals and borrowings.

- Despite the large debt component, the company regularly pays dividends even though there may be better uses for the cash. However, one may find a little solace in the fact that the dividend money is used by the promoter to buy stock from the open market. (The company paid Rs.1.8cr as dividend in FY22 with an additional Rs.3.6cr of dividends announced in May)

- IPP Margins from the new capacities are likely to take a hit due to an introduction of Banking charges at Rs. 1.5/unit. Average realisation per unit in IPP has too come down from Rs. 6.06 in FY21 to Rs. 5.03 in FY22.

- The industry as a whole suffers from the possibility of lower production and thus lower realisations due to climatic conditions, which is amplified for KPI as the company’s client base, as well as production, is concentrated in Gujarat.

- The company does not host conference calls and there is no analyst coverage and thus our ability to reasonably forecast earnings is constrained.

Disclosure: Invested from 120-130 levels.

My gratitude to @chins for encouraging me to write here and for recommending the thread title.

Looking forward to hearing everyone’s thoughts!