The 1000 MW is by CY25 and not FY25

yes order inflow must increase to have longer visibility.

For IPP to survive, CPP order inflow is must.

Some IPP calculations: 132 cr for (16mw wind+10mw solar), means avg 5 cr / mw.

This hybride can generate 16 x 365 x 24 x 0.25 x 1000 ~ 3.5 cr units from wind , and

10 x 1000 x 4 x 365 ~ 1.4 cr units from solar. Total units = 4.9 cr

At 5.5 rs a unit = 26-27 cr revenue.

If all 132 taken as loan at 9% for 10 years, EMI/yr can be 21 cr.

So basically IPP is more sort of asset generating business and CPP is cash generating business.

CPP is needed to keep IPP going on.

Can you please give a description for the above calculation.

Also, Management has said they charge 10% discount for the IPP rates which will be Rs7/- to Rs 8/- per Unit for IPP.

Reference- https://www.youtube.com/watch?v=rHEj1ye0NPk

Avg 4 units(kwh) can be generated in a day from 1 kw solar capacity.

1 Like

It’s not 7 to 8. They need to cross subsidy charge, transmission charges etc. So realization is only between Rs 4 and 5

May be because of this?

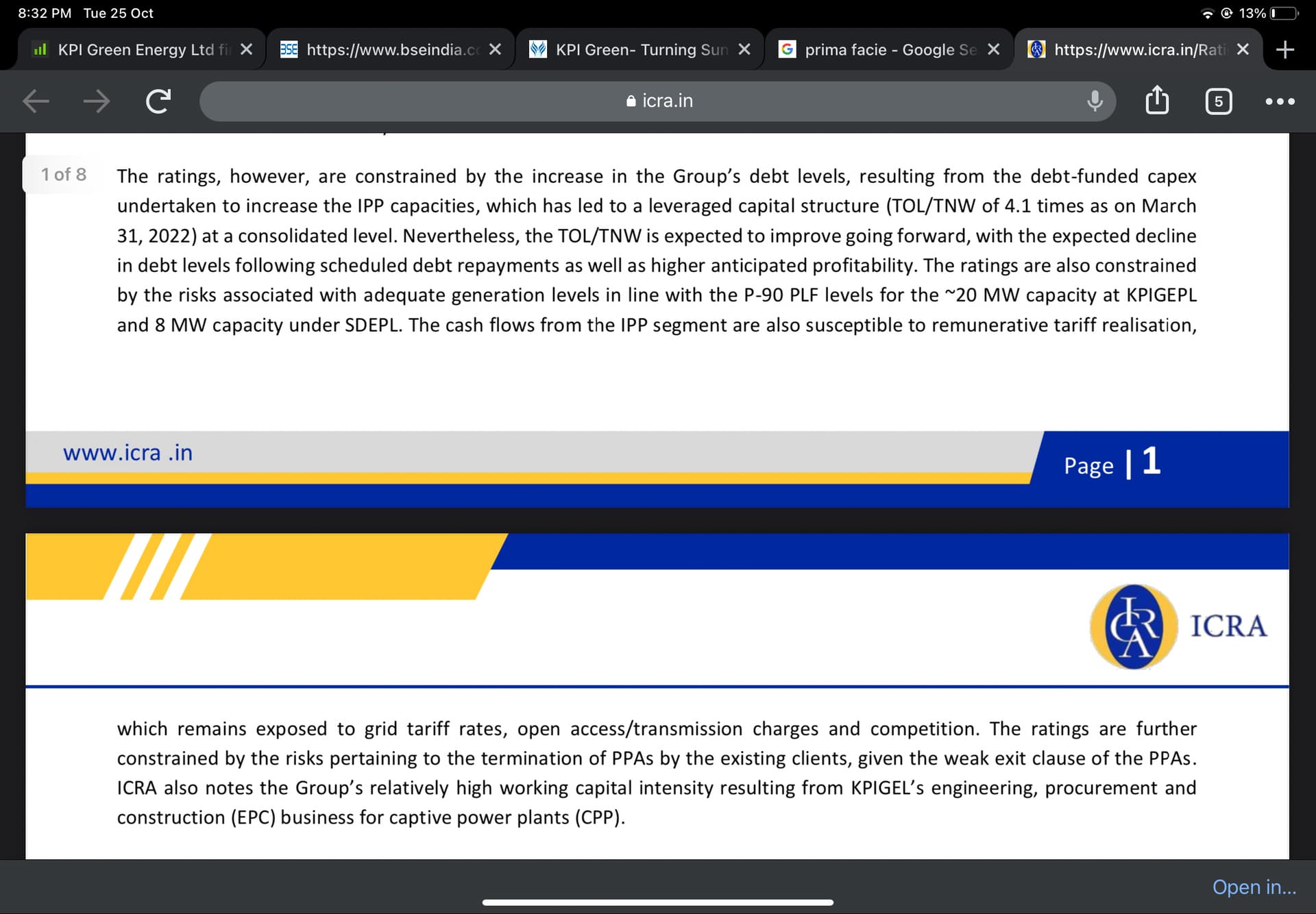

Prima facie, I think it won’t impact kpi’s existing capacity.

KPI’s IPP capacity is tied up with private players and rates seems to be variable

Other companies like sjvn who have signed PPA based on earlier custom duty structure will suffer if the projects are not completed. As cost is going to increase and state discom are not revising up price in the PPA.

3 Likes

Just to be sure, can anyone contact the company and get clarification from them about this? I tried writing to them but no reply yet. Is there anyone who has a direct or indirect connection to reach out to the company’s management?

Seeing the promoter buy from the open market when the stock dropped, I do feel it probably is not gonna affect KPI.

1 Like

Hi Everyone,

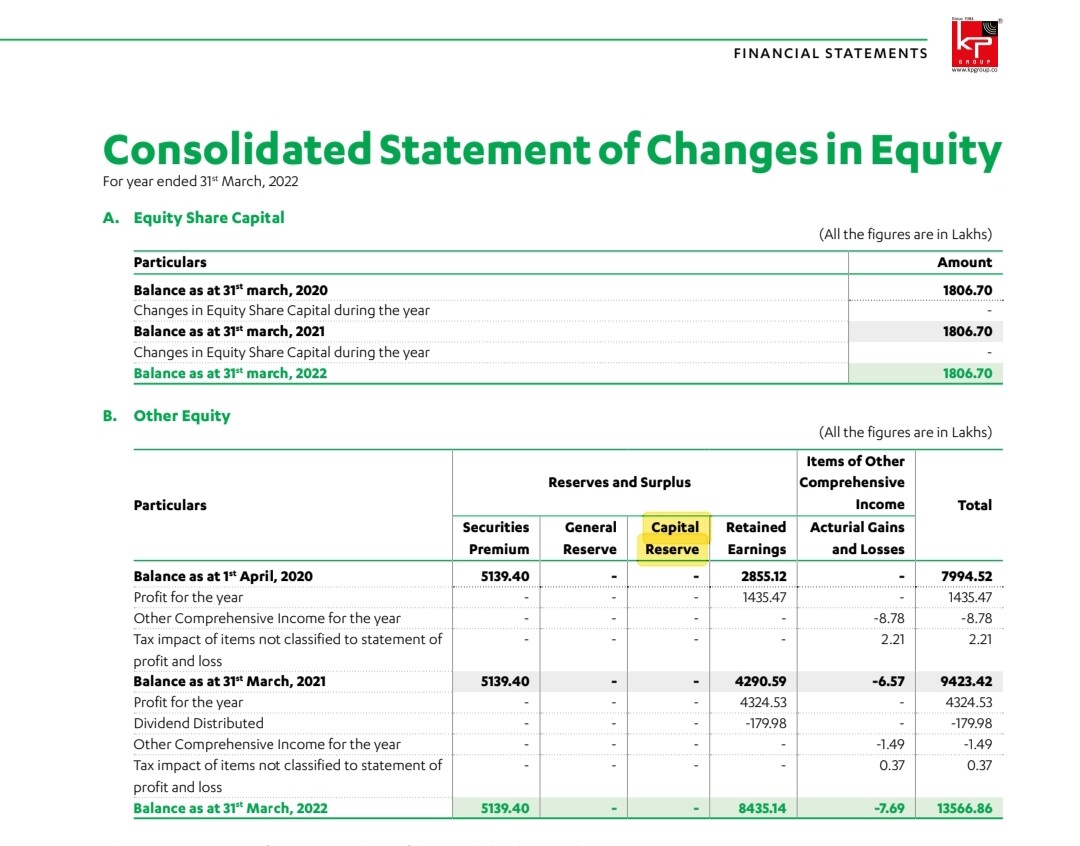

What do you all think, is it wise decision for the company to declare bonus shares considering debt and capex ?

What’s the link of bonus shares to debt or capex?

1 Like

Bonus shares will be issues through reserves… Which could be used to repay debt… and do more capex?

Bonus is just a free share given to shareholders it doesn’t impact cash flow of a company. Only reserves get distributed.

Bonus can be declared from three reserves

- Capital reserve

- Securities premium reserve

- General reserve

In case of KPI Green they had not created capital reserve so the bonus shall be distributed from Securities premium and general reserve if SPR is not sufficient.

Hence saying that reserve can be used for debt and capex has no use as company act,2013 provided certain restrictions on reserves.

Hope your doubt is cleared now.

5 Likes

Hello Everyone,

Does anyone know what is long term vision of the company, it is not mentioned in their Annual reports.

Is KPI Green willing to operate only in Gujarat? Or does the company have expansion plans to other state like Rajasthan … etc…?

1 Like

@tejaspdongre , there are management interviews in this thread. pls listen to them.

1 Like

I have been following KPI GREEN for the last six months, patel did not mention anything regarding expansions in other states…

So i had to highlight … and ask if anyone has a clue regarding this ?

They have land asset in Gujarat and transmission lines plus approval too.

Makes no sense to expand to other states.

2 Likes

Gujarat has good policy when it comes to establishing renewables infrastructure and also enabling the ecosystem right from allowing private players to create solar and wind power projects and transmitting that electricity back to grid. Because of this I don’t think Kpi green will expand in other states.

These are my views and I am may be wrong.

3 Likes

Mr. Faruk Patel during his AGM of KP energy did mentioned that they are planning to enter into Kerala state for their wind business. This might open up opportunity for kpi green in future.

Also Mr. Patel have mentioned multiple times in the past that Gujarat state has huge potential for the business as all the power heavy consuming industries (textile, chemicals etc) are setup in Gujarat. Hence considering the size of the company, they can continue to de well in near to medium term without having any need to enter into other geographies.

6 Likes

It was Karnataka I think and not Kerala

1 Like

Is KPI Green’s current valuation justifiable?

Company is unable to brag orders above 1 or 2 MW… max is 10 MW…

Can it be a prominent player in the solar industry or just 2/3 players will dominate the solar market…

Patel’s vision to cross 1000 mW in the next 2 years… with just 1 or 2 MW majority orders seems tough? or even if he reaches the 1000 Mw mark… has the market already discounted it?

what do you guys think about it?

Thanks in advance ![]()

1 Like