I have made this remark on the basis of FY21 because that time revenue is increasing but TR were also increasing. Moreover CFO is negative with high WC. In FY22 they have performed well which is clearly visible in their CFO ( From -27 CR to +102 CR) and as you said receivable had also decreased.

But inventory is pilling up ( 40 CR to 107 CR) almost more double. But the reason is they are pilling up inventory can be seen as a proxy for their revenue growth.

My bet is on Promoter farukh Patel ji his clear buying form open market when share price is hammering after Q4 is giving clear signal to me.

it appears that KPI green has bagged more orders but not declared the same. in the last credit rating report , they had 84MW orders. right now in the latest analyst coverage by Batlivala securities, they have orderbook of 120MW worth 580 cr. This is really splendid growth.

Farukhbhai Patel ji covered by " CEO Magazine".

Attaching some main points from the interview

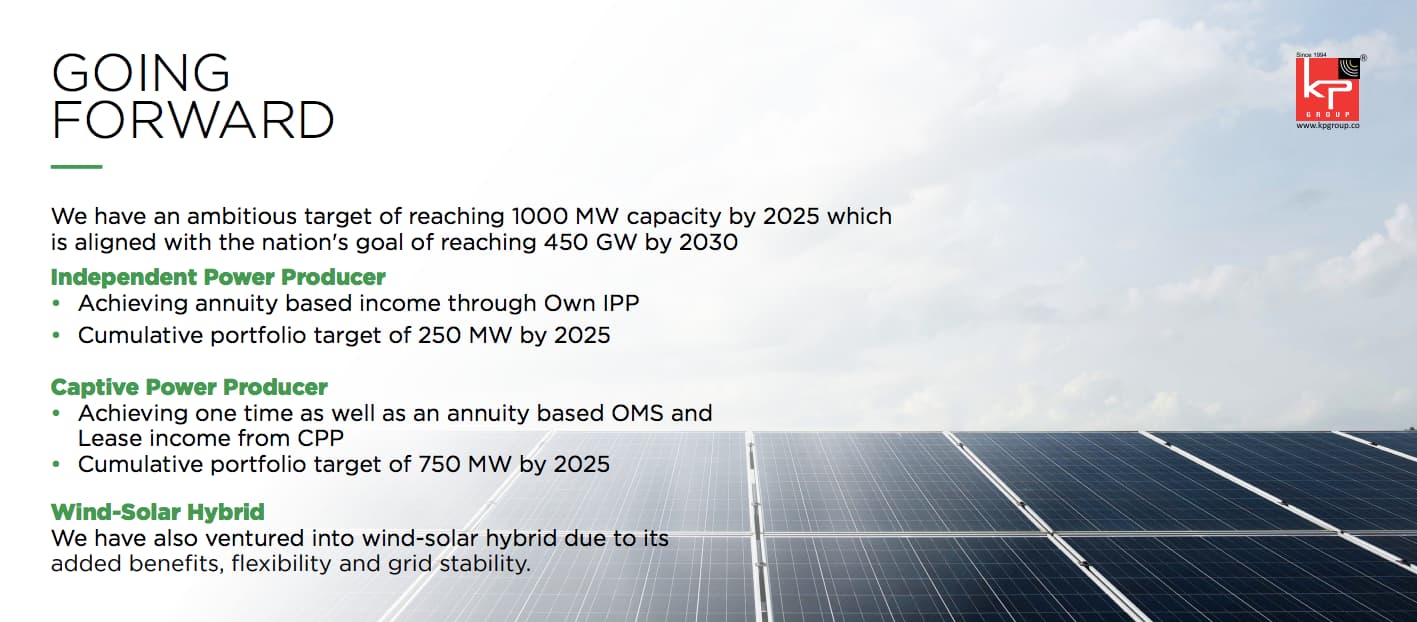

The KP group has set the ambitious target for their each entity.

The sheer number of projects currently running and in the pipeline for KP Group hasn’t stopped Faruk from hitting projections and setting bigger goals for the future. “Regarding KPI Green Energy, we jumped from 49 megawatts to 100 megawatts in IPP, and nine megawatts to 65 megawatts in CPP last year,” he says. “We have another 162 megawatts in the pipeline so we’ll cross 300 megawatts in March 2023.

He maintains a strong bond with vendors and suppliers by following three key rules.

First, their payment should be on time. Second, the clarity and quality of materials should be very particular. Third, employees must respond immediately to their queries,” he says.

For each material, KP Group has five suppliers at any given time to maintain the quality of products. “We have around 237 items and a minimum of 1,000 suppliers and vendors, out of which, around 25–30 suppliers are key to the running of the business,” he says.

All the active projects, as well as those in the pipeline, contribute to KP Group’s top line. According to Faruk, together, KPI Green Energy, KP Energy and KP Buildcon will command a revenue close to US$600 million by 2025.

also CNBC interviewed the founder today, i think its first time he was on CNBC. he didn’t give a no but did say that revenue will be 2-3 times every year till 2025 and they will definitely reach 1000 MW.

Rough Calculation -

So if we take conservatively 2X rev every year from FY22 then by FY25 total Rev will be 1800cr

if we assume NPM =20%, bottom line will be 360cr… If we assign conservative multiple of 30X then Mcap will be approx 11000cr by FY25…Thats 6-7X in 3 years

(please correct me if something is wrong)

this is right. the sector is growing without doubt. and is one of the fastest growing sectors. both solar and wind have huge potential in gujarat state and the target which co needs can be done in gujarat itself without venturing outside. the only caveat is execution risk which going by the track record of the co is achievable i would say. and if the co does more revenue in FY24 then the valuation can peak in that year also without waiting for FY25 to happen.

one may be concerned with increasing debt but cashflows from ops are robust and more than sufficient to take care of the debt repayments. also co is focusing on CPP segment which is asset light.

at this point its more a question of how can the co. go wrong. that is the biggest risk imo. the sector, the growth, the potential are all there.

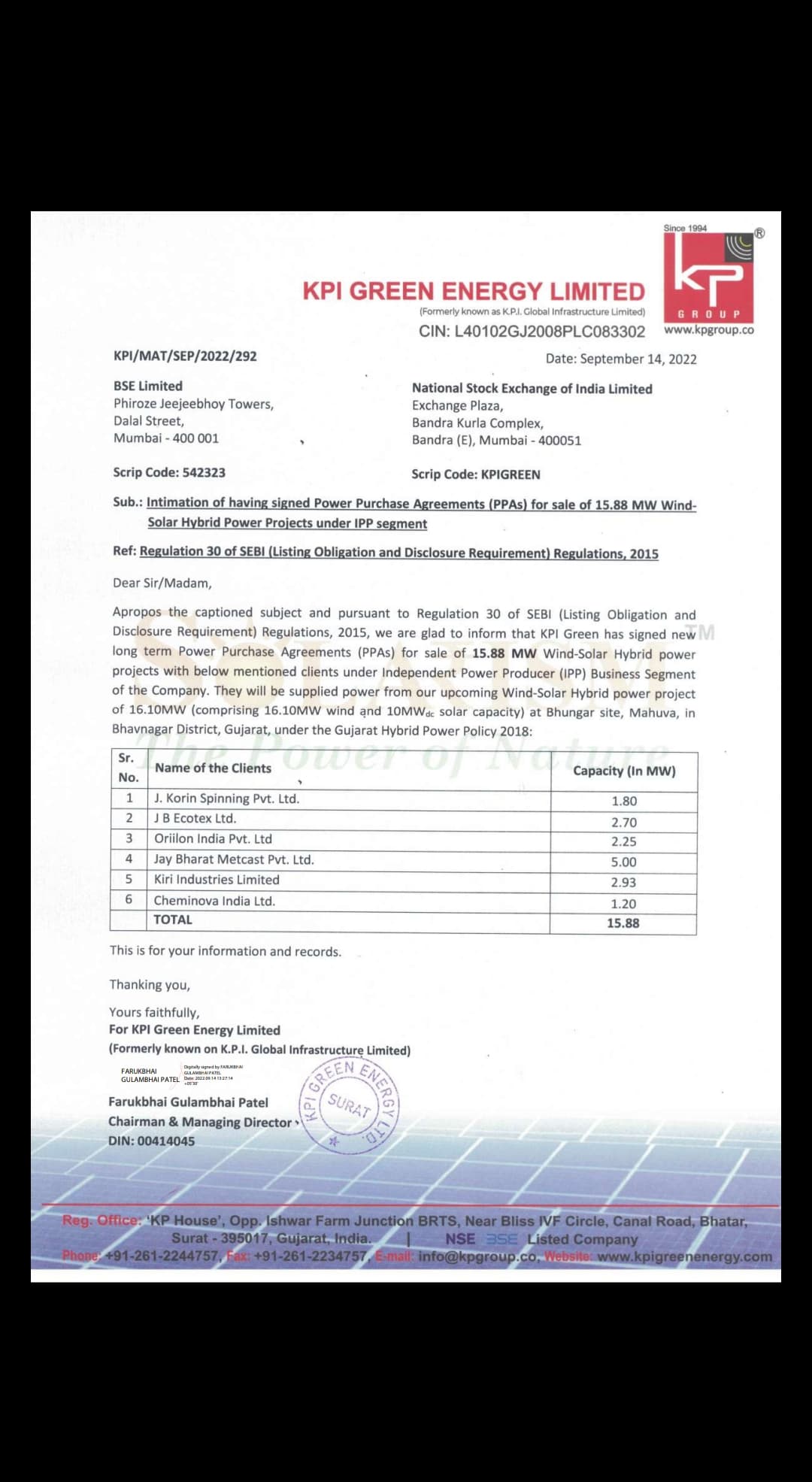

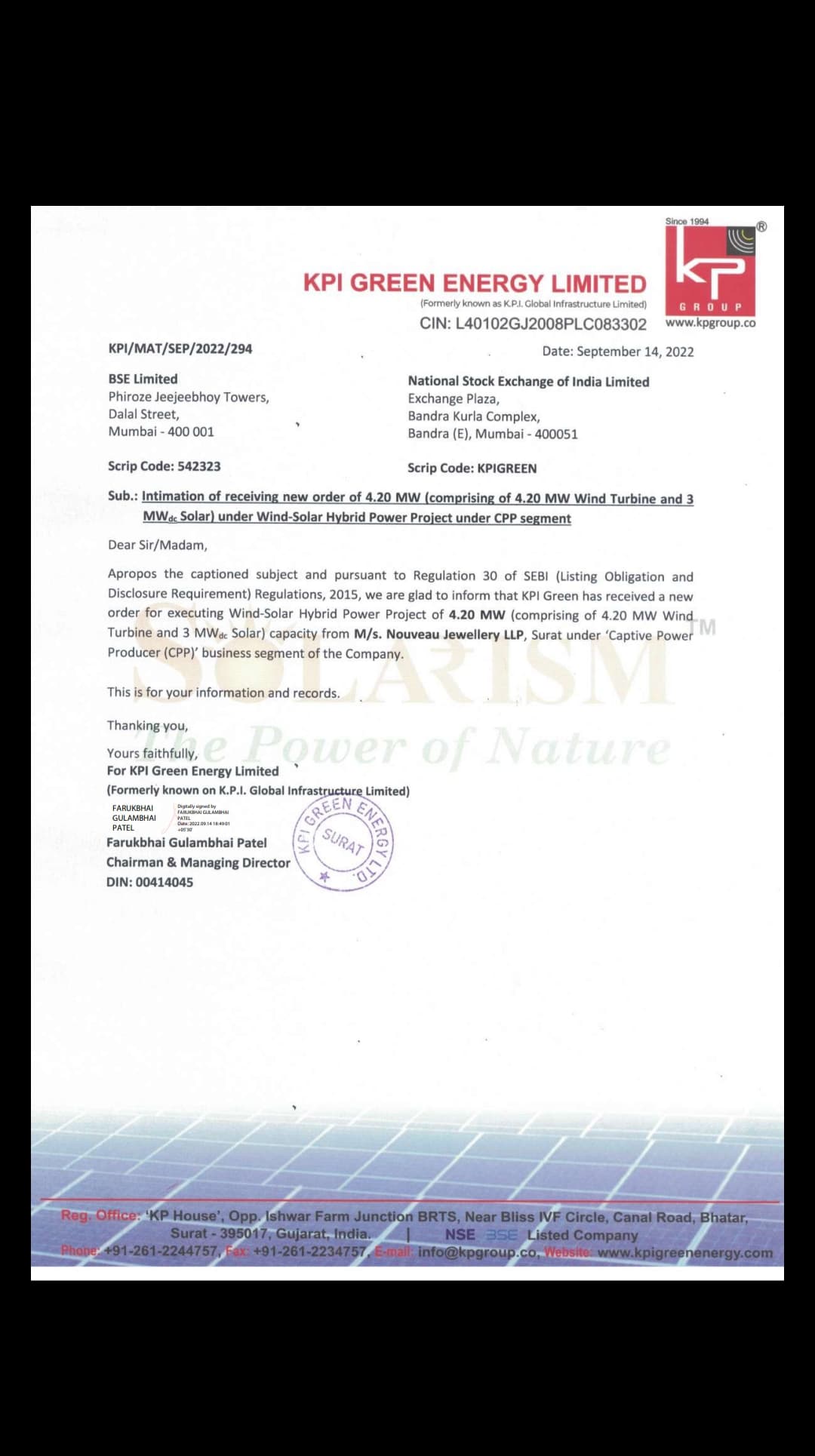

Two big order after a long time.

One for sale of 15.88 Mw wind - solar hybrid power project from 6 different clients under IPP segment and one for sale of 4.29 Mw wind - solar hybrid power project under CPP segment.

One good point to note from AGM is they have evacuation capacity of around 600MW getting in place which will help them scale. This is very much required as one cannot just add the sites on solar but need to get the electricity out of Solar project as well. Looks like the company is planning and working on all angles to achieve the target of 1000MW by 2025.

I have two basic question regarding the pricing power how much does company earns for 1MW supplied?.And the capacity mentioned in the presentation whether they represent Annual or monthly?

In a recent interview with the MD, he mentioned the company’s target is to reach 1000MW by FY27. Did they just extend their target from FY25 end to FY27? Or am I missing something? If this is correct it will have an impact on growth rates significantly. Or they are just being conservative?!

I am also surprised. I think it’s a miscommunication here. If you hear the video they also say, that this will we will add 300 MW whereas he wanted to say this year we will be cumulative 300 MW. But I agree we should get the clarification as earlier it was 1000 MW by FY2025

Yes he clearly mentioned 2027, and I think thats good as this is asset heavy business IMO.

What co is doing, if you hear interview carefully, he says LAND is everything- very importamt component for them. Both for IPP and CPP, they are using land.

1 MW = 3.5-4 acre land = 6.5 bigha = 1.5-2 cr (20-25 lakh/ bigha land rate in villages where co is working - my assumption)

1 MW ex land development cost is = 30000*1000 = 3 cr

So if you see co is getting immense benefits of having land in place.

I think co is having land till 500 MW cummulative capacities.

Then co needs to add land to grow further and cost will go up.

Old annuity income will help co to great extent in future.

Now lets take asset payback currently = 3 -3.5 years as co is having land bank.

Post 500 mw, that payback will increase to 5.5-6 years. Not good, not that bad either.

Some positive points from interview:

Accelarated depreciation in IPP is helping to save tax and save cash for future growth.

860 MW evacuation in place

100 cr annuity revenue will increase to 300 cr in 2026-27.

co is now getting lower interest loans as size is getting bigger day by day

Biggest risk is gov policies.

Just sharing some long term views and I am holding from lower levels

I too feel its miscommunication cause they mentioned 1000MW by 2025 in their AR, their recent AGM as well as interview given to CNBC one month back…Everywhere they said 1000MW by 2025

Good set of Q2 nos. Important to note that almost all the revenue came from CPP segment. 38MW of CPP orders energized in Q2. Out of 160 cr consolidated revenue, 14.5 cr was from IPP and 145.5 cr from CPP. This brings revenue of 1MW CPP to close to 4 cr.

Also crucial that 77MW of CPP orders and 9MW of hybrid orders are in hand. Bulk of this will be executed in next 6 months which will ensure that co reaches or exceeds 500 cr revenue for FY23.

So one should ask what is next for the company. BY FY23 end, they will have energised close to 100 MW in IPP and 184 MW in CPP segment.

the company aims to increase CPP total capacity to 750 MW by FY25. This will mean that they execute 550MW in FY24+FY25 or a total revenue of 2200 cr.

Remember FY22 CPP revenue will be 300 cr about. So the 2200 cr split could be 800+1400 or 700+1500 cr. either ways it means significant jump in the scale of operations.

The CPP is an asset light model and while IPP brings annuity revenue, it is capital intensive and the interest cost of 44 cr per FY is already substantial. Think the co. also recognises that and is focusing much more on CPP than IPP.

they have also got 9MW of solar+wind hybrid orders which should mean more revenue per MW than solar alone.

Will be very interesting to see how the co. shapes in FY24.

| 14th AGM | 29/9/22")

| Proceeding of 13th AGM | 30/9/21")