Gensol - Bluesmart story points the role of corporate governance - even in high growth industries like solar, EV, etc.. I would clearly stay away from companies with poor governance..

Two points which seem to be red flags to me

Sustainability of profits and returns on capital

- The operating margins of 30% + are unheard of in Solar EPC. I am not able to fathom how they have been achieving the same

- On the IPP business, their PPAs are at 2.7-2.8/unit - it will be difficult to earn a return on capital of more than 12-14% percent

Further, promoter buying stake of 16% in the subsidiary Sun Drop Energia which is then being used to service orders in the exact same line of business feels unfair to minority shareholders. They could have added the capital in KPI Green directly instead. Unable to understand the rationale.

Lastly, not to mention the over indexation on share price and frequent bonus/split, dividend while equity dilution is happening which seem to be done to boost market perception and share price.

Had invested from 130-140 levels, thinking of exiting.

1 Like

Is it possible that OPM is on the higher side because revenue from IPP has very high margin, so blended margins are higher? Assuming they are capitalizing IPP investments.

It has ~10% institutional holding, vanguard and blackrock , adia and similar. Can we trust them to keep the owner true on corp gov?

disclaimer: invested and 10% of pf. reevaluating post gensol fiasco

1 Like

As far as I know, IPP revenues are insignificant as of the results declared (<10%). Most of the IPP assets are yet to be commissioned and revenue will start flowing post commissioning.

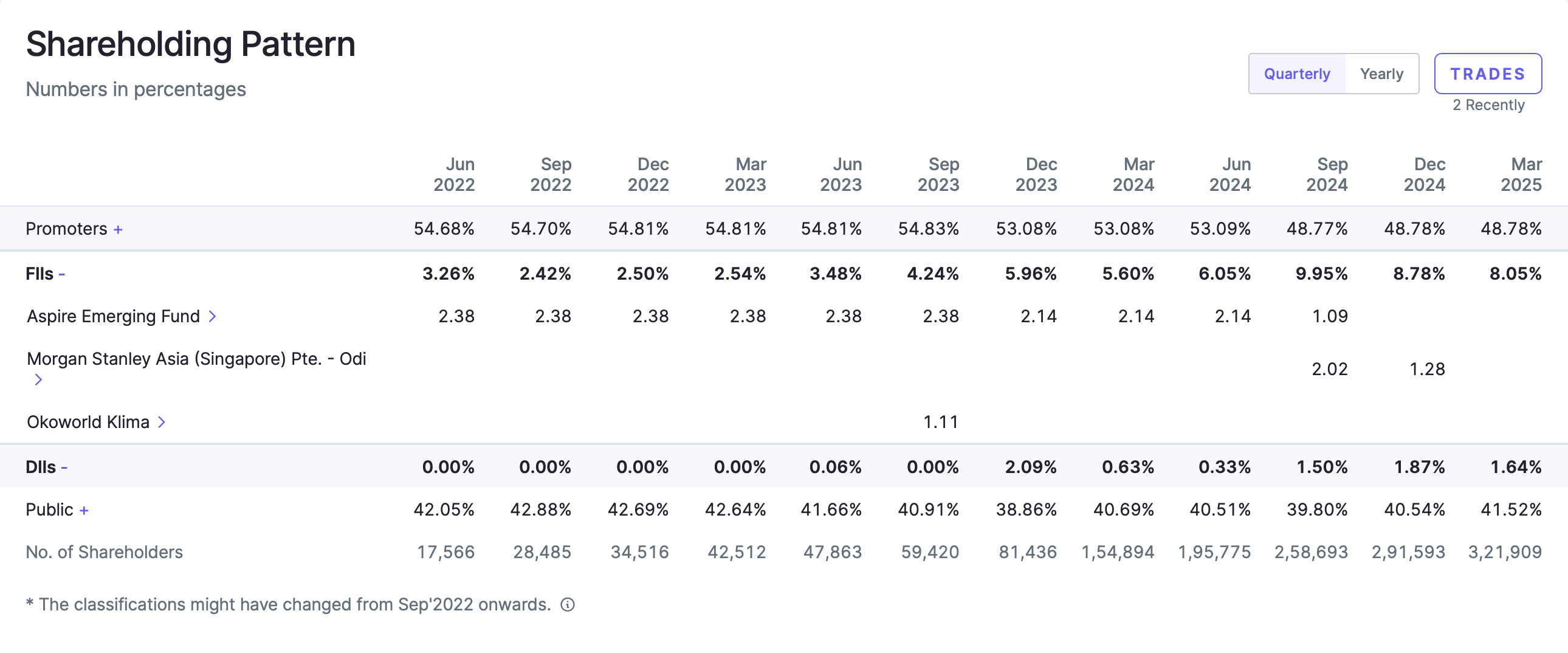

Also, I could not see the institutional holding mentioned as per Mar 2025 shareholding. Please correct if wrong.

1 Like

As per latest investor presentation, IPP is 13% of the 9MFY25, which is almost 145cr. 9M PBT is ~300 Cr. Assuming 70-80% marging on 145, it can seriously positively impact overall margin. FII + DII is close to 10%.

2 Likes

Perhaps. However, margins have been consistently in the mid thirties which seem high by industry standard.

As far as institutional holding is concerned, institutions have sold part of the shares they acquired in the QIP at prices higher than the CMP.

Hopefully there are no skeletons in the closet and the growth story plays out well. Personally, seems risky to me.

2 Likes

This might be next Gensol, too many shady area’s. Results are always excellent, bonus, split, pledge:joy:![]()

![]()

2 Likes

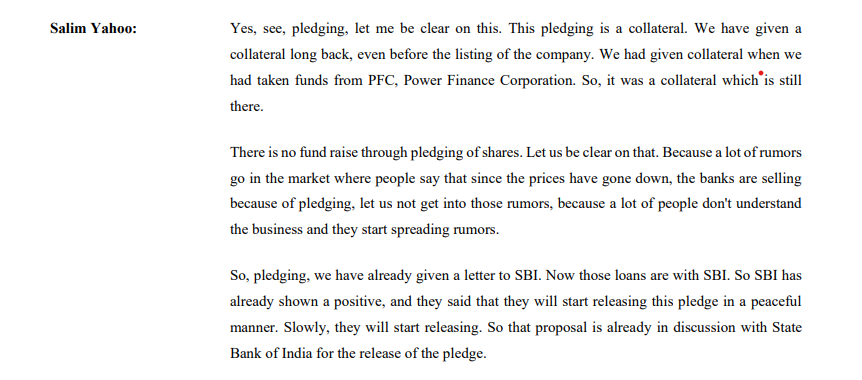

Management’s response on pledge, though it’s not clear why they its a collateral but not for fund raise. Anyways, a key aspect to monitor, if they will be reducing it. Their borrowing has come down significantly, and so is the interest they are paying.

NPTC green, with 2K sales has mcap of 90K and margins of 85 - 90%.

KPI green IPP with 200 sales , by the same yardstick, would have a value of 9K ( the mcap of entire KPI). So there is surely some value there for the IPP business.

Unless it’s an outright fraud, numbers are fudged, etc, etc. at current valuation, it looks like value. It is possible that management might shortchange the investors, here and there.. but then, most corp do that in our market. Hope the management learns from gensol. Planning to hold and keenly monitor.

6 Likes

In the current year the company has generated 24.9 crore units of power in IPP and booked Rs 217 as revenues. This translates in Rs 8.7 per unit of realization. Can anyone share what are the rates charged by the Gujarat Electricity Board. I would presume that the rates will be lower but happy to be corrected.

1 Like

KPI Green has received a Letter of Intent from Gujarat Urja Vikas Nigam Ltd to develop a 150 MW wind power project in Gujarat. This was awarded after a competitive bidding process and a reverse auction where KPI emerged as a successful bidder. Once they get approval from the Gujarat Electricity Regulatory Commission, they will sign a power purchase agreement with GUVNL.

2 Likes

Concall Notes - Aug 2025

KPI Green Energy Limited – Q1 FY26 Earnings Concall (August 6, 2025)

Detailed Analyst Note

- Financial Performance & Growth Trajectory

Record Quarter, Fifth Consecutive All-Time Highs

- Revenue: ₹614 crore, +75% YoY (Q1 FY25: ₹350 crore).

- EBITDA: ₹217 crore, +64% YoY.

- PBT: ₹149 crore, +64% YoY (Q1 FY25: ₹91 crore).

- PAT: ₹111 crore, +68% YoY (Q1 FY25: ₹66 crore).

- EPS: ₹5.28 (+44% YoY).

- Cash Profit: ₹163 crore, +92% YoY.

- EBITDA Margin: 35% (blended; IPP: 75-80%, CPP: ~20%).

“We are pleased to report yet another record-breaking quarter, making our fifth consecutive quarter of highest-ever revenue.” – Salim Yahoo, CFO

Guidance & Outlook

- Management reaffirmed 50-70% topline growth guidance for FY26 and FY27, with confidence of meeting/exceeding it.

- PAT margin guidance maintained at 16–18%.

- The company expects to maintain strong margins as IPP contribution rises.

- Business Model, Segments, and Revenue Mix

Core Segments

- IPP (Independent Power Producer): Long-term annuity income from power sales (PPA-backed).

- CPP (Captive Power Producer/EPC): EPC and turnkey projects for third-party/captive customers.

Revenue Mix Evolution

- FY25: IPP ~13%, CPP ~87%.

- Q1 FY26: IPP ~10% (lower due to phasing of commissioning).

- Medium-term target: IPP to rise to 17–18% by FY26-end, with a strategic goal of 25% as portfolio scales.

- Long-term ambition: 10 GW portfolio with 25% revenue from IPP, 75% from CPP.

Unit Economics

- CPP: Solar EPC realization ~₹3.25–3.75 crore/MW, wind ~₹7–7.5 crore/MW. Some projects are BOP (Balance of Plant) only, affecting per MW realization.

- IPP: Average realization ~₹3.5–3.6/unit (PPA rates).

- Project Pipeline, Order Book & Execution

Mega Projects Under Execution

- IPP:

- 250 MW Solar (AC, 350 MW DC)

- 370 MW Hybrid (AC, 679 MW DC)

- 150 MW Standalone Wind

- Total execution size: ₹5,000 crore

- Backed by 25-year PPA with GUVNL (“one of the best paymasters”).

- Phased commissioning through Sep 2026; revenue recognition to begin in coming quarters.

- CPP:

- Order book: 1.8 GW (₹4,000+ crore unbilled).

- Milestone-based billing; revenue recognition aligns with execution milestones.

Capacity Snapshot (as of Jun 30, 2025)

- Installed & Upcoming IPP: 1.7 GW

- Installed & Upcoming CPP: 2.3+ GW

- Cumulative Portfolio: 4 GW

- Land Bank: 6,275 acres

- Evacuation Capacity: 3.2 GW (already approved)

- Orders in Hand: >3 GW (including LOI-awaiting capacities)

- Presence: 108 project sites, across multiple discoms and CTUs.

Execution Run-Rate & Seasonality

- Q2 execution may see slight curtailment due to monsoon, but management expects to match previous year’s Q2.

- For FY26, plan to commission at least half of the 1.2 GW IPP under construction.

- Units Generation: Existing 171 MW IPP generated 6.9 crore units in Q1; new 240 MW + 92 MW to add 35 crore units (half-year) post-commissioning.

- Strategic Initiatives & Technology

Key Developments

- LOI from GUVNL for 150 MW wind project, strengthening hybrid pipeline.

- Three MOUs with Delta Electronics India:

- Battery Energy Storage Systems (BESS)

- Green Hydrogen & EV Charging Infrastructure

- Advanced Solar PV Inverters

- BESS (Battery Energy Storage System) Foray:

- Targeting ₹3,000–4,000 crore of BESS tenders (pipeline).

- Focused via subsidiary Sun Drops Energia Pvt Ltd (SDEPL).

- Smaller BESS projects in SDEPL; large utility-scale BESS may be in KPI Green.

- Execution timelines: 18–24 months per project.

- Margin: Will target healthy but competitive margin; BESS seen as a future growth vector (“only BESS can give you RTC and stability in green power”).

Technology Edge

- State-of-the-art OMS, NOC, and robot facilities for project O&M.

- IBM Maximo Renewables for real-time monitoring and performance optimization.

- Solar Panel Robot Cleaning: Currently for internal use (500+ robots installed); potential for commercialization/O&M for third parties in future.

- Industry & Policy Commentary

Sectoral Headwinds/Opportunities

- ISTS Charges: KPI Green is insulated as current projects are under STU/state bidding, not ISTS. No direct impact from sunset of ISTS waiver.

- Transmission/Evacuation: Management claims no bottleneck; have pre-secured 3.2 GW evacuation. Gujarat government planning ₹1 lakh crore investment in transmission infra.

- Land Bank: 6,000+ acres secured, mitigating a key sector risk.

- Execution Risks: Management identifies land and evacuation as key risks, both addressed proactively. “Success rate may be around 95% to 96%.”

Government Policy

- No negative impact anticipated from recent government policy changes.

- 25-year PPAs with GUVNL provide annuity income and counterparty security.

- Subsidiary Structure, IPO Plans & Capital Allocation

Subsidiary Structure

- Multiple subsidiaries/SPVs for ring-fencing project risks, in line with industry practice (e.g., Adani Green, Mahindra Renewables).

- Sun Drops Energia Pvt Ltd (SDEPL): 100% subsidiary (now minority pre-IPO investors), to be listed; KPI to retain >51% post-IPO.

- KPIG Energia: For 35–100 MW projects.

- K Park & Miyani: For specific plant/connectivity.

- Reason: Different customer sets, project sizes, and resource needs.

IPO of Subsidiary

- SDEPL IPO planned; DRHP in preparation.

- No direct allotment to KPI Green shareholders; open market dilution (25%).

- SDEPL to be the vehicle for BESS and smaller projects.

Capital Structure & Debt

- Current D/E: 0.5:1

- Post-NCD (₹700 crore): Will not exceed 2:1; industry peers at 5–7x.

- No immediate equity dilution planned; profitability to support net worth.

- Green Bonds: Rated AA+ (CRISIL), likely pricing ~8.8%.

- Margins, Unit Economics & Financials

Margin Profile

- IPP: EBITDA margin 75–80%, PAT margin 15–20%.

- CPP: EBITDA margin ~20%.

- Blended: EBITDA margin 30–35%, PAT margin guided at 16–18%.

- Margin volatility across quarters due to milestone-based billing (service component higher margin, supply component lower).

Cost Escalation/Design Changes

- ICRA noted ₹700 crore cost increase in one IPP project; management clarified this is due to design change (tracker to fixed structure, higher AC-DC ratio), not escalation.

- “IRR will slightly improve” due to higher PLF and revenue.

- Order Pipeline, Bidding Success & Growth Visibility

Order Pipeline

- CPP: 1.8 GW/₹4,000 crore in hand; pipeline robust with further tenders.

- IPP: ₹5,000 crore under execution; 1.2 GW to be commissioned by Sep 2026.

- BESS: ₹3,000–4,000 crore tenders targeted (Maharashtra, Gujarat, Rajasthan, Andhra Pradesh).

- Overall pipeline: ₹8,000–9,000 crore (solar/wind/hybrid + BESS).

Bidding Success

- Hit rate in tenders: 80–90%.

- Expectation of more large orders in coming quarters (including CIL, SJVN, GUVNL).

- Corporate Governance, Disclosures & Investor Relations

Pledged Shares

- SBI loan repaid; pledge release process underway, pending SBI board approval (expected by next quarter).

Investor Suggestions

- Management receptive to feedback: will enhance PPTs with quarterly capacity additions, segmental revenue, group/subsidiary structure, and clarify group-level targets vs. company-specific ones.

- Promoter holding stable at ~48.7%; no dilution planned in next 2–3 years.

Shareholding

- FII holding strong (Vanguard, Blackrock, etc.); DII focus to increase, especially with green bond issuance.

- Risks, Challenges & Mitigants

Key Risks Identified

- Execution (Land & Evacuation): Both proactively addressed (large land bank, pre-approved evacuation).

- Government Delays: Acknowledged as industry-wide, but not seen as major risk due to project structuring and counterparty (GUVNL).

- Project Design Changes: Managed through technical flexibility; cost increases offset by higher output and revenue.

- BESS Business: New segment; margin and execution risk acknowledged, but strong technology partnership (Delta) and initial focus on smaller projects to mitigate.

- Other Notable Points

O&M and Robot Cleaning

- 500+ robots deployed for internal O&M; future commercialization possible.

Evacuation/Transmission

- 3.2 GW evacuation already secured; Gujarat government and central government investing heavily in grid infra.

Workforce

- 800–900 employees, including 560 in KPI Green; focus on professionalization and hiring to support growth.

International Expansion

- Under discussion; no concrete disclosures yet.

- Management Tone & Outlook

Highly Optimistic and Confident

- Management repeatedly emphasized robust execution, strong order book, and risk mitigants.

- Confident of maintaining growth rates and margins, scaling up IPP share, and leveraging new growth vectors (BESS, green hydrogen).

- “I give you the promise that you will be very happy in next con-call more than this quarter and that is my promise to you people and we are doing the work…” – Dr. Faruk Patel

Conclusion

KPI Green Energy continues to deliver industry-leading growth, with a robust order book, strong execution capabilities, and disciplined capital allocation. The company is aggressively scaling its IPP business, entering BESS, and leveraging technology partnerships. Risks around execution and policy are proactively managed, and financial guidance is reiterated with confidence. The management’s tone is highly optimistic, underpinned by strong operational visibility and sector tailwinds.

I am not a registered Sebi analyst. No buy selling recommend…

5 Likes

Kpi green to raise 3200Cr from SBI via loans

2 Likes

Very well researched video / he has raised significant red flags. Check yourself before taking a call.

Summary:

- The cash flow from operations has been volatile, and the company has been funding capital expenditures through debt and equity dilution [08:23].

- Equity capital and borrowings have been increasing, which means existing shareholders’ stakes are being diluted [15:30].

Concerns about corporate governance and related party transactions, including:

2 Likes

I don’t know what to believe, ICRA & CRISIL both are giving an AA+(CE) Stable rating for now so my stance will be cautious but not as negative. Nonetheless, thanks for sharing the risk, will try to manage the risk with lower allocation.

Credit rating agencies evaluate companies primarily from a lender’s lens—focusing on debt repayment capacity via metrics like liquidity, growth, and leverage. They don’t necessarily assess governance or shareholder alignment.

Recent red flags like property purchases and royalty payments to promoters suggest a pattern: capital being extracted in ways that don’t benefit minority shareholders. While the business may continue to perform, these governance signals raise enough concern for me to step aside.

Plenty of cleaner stories out there—no need to carry unnecessary baggage.

2 Likes

In this topic, KPI Green- Turning Sunshine Into Cashflows. We have been monitoring the company’s performance, and it would be wonderful to share insights with fellow members on its strengths, weaknesses, and long-term outlook.

KPI Green Energy Limited (KPIGREEN) reported its fifth consecutive record quarter in Q1 FY26, driven by robust execution across Independent Power Producer (IPP) and Captive Power Producer (CPP) businesses. Topline grew 73% YoY to ₹603 crores, EBITDA by 64% to ₹217 crores, and PAT by 68% to ₹111 crores, with EPS up 44% to ₹5.28. Cash profit jumped 92% to ₹163 crores, reflecting good cash generation. Management has pegged PAT margins of 15-20% and topline growth of 50-70% in FY26, reflecting optimism for continued momentum.

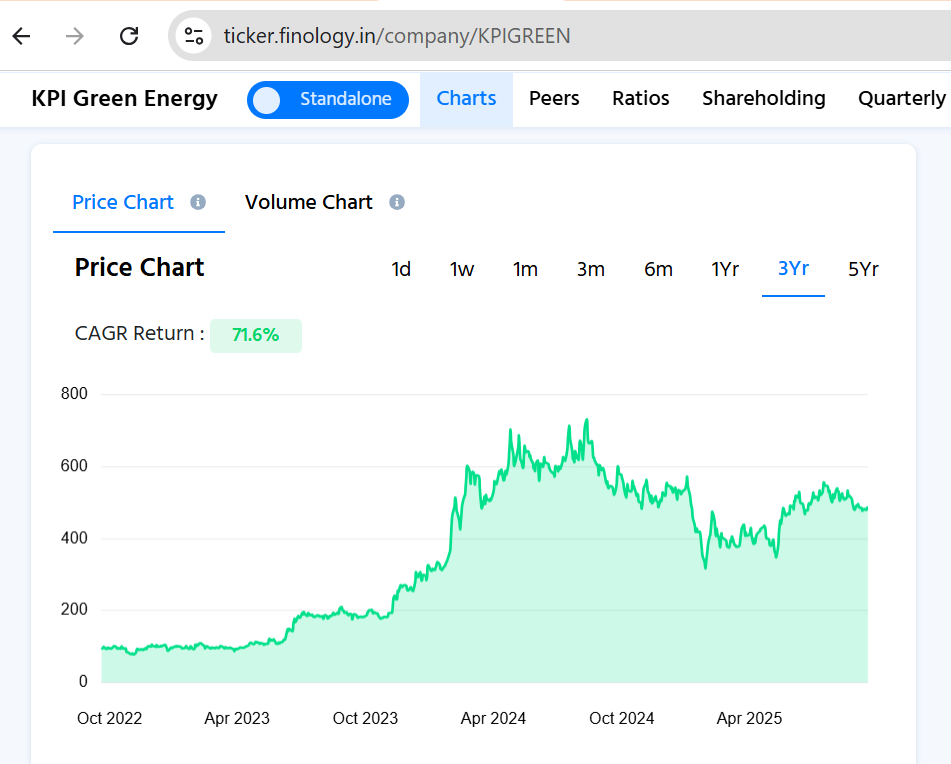

Over the last year, the stock has declined by 10.6%, indicating near-term weakness or a correction following its steep rise. This can be due to profit booking, sectoral issues, or general macroeconomic influences. But from a 3-year perspective, the stock has posted an excellent return of +71.6%, indicating robust creation of wealth and highlighting the advantages reaped by medium-term investors during the growth cycle of the company. Over a 5-year horizon, the stock has returned an impressive +128.7%, fully doubling the wealth of the investor. This strongly suggests that, for all the short-term fluctuations, the firm’s strong fundamentals and potential for long-term growth have not been compromised.

The operational strengths of the company consist of a 4+ GW portfolio comprising 1.7 GW IPP and 2.3 GW CPP, an order book of more than 3 GW (₹4,000 crores of CPP alone), a large land bank of 6,275+ acres, and more than 3.2 GW of sanctioned evacuation capacity. High-value projects under implementation - solar, wind, and hybrid of ₹5,000 crores are supported by 25-year PPAs with GUVNL. KPI Green is also expanding through collaborations in BESS, hydrogen, and EV charging with Delta Electronics, and is preparing its subsidiary, Sun Drops Energia, for an IPO. The mix of revenue is anticipated to change gradually from CPP dominance (90% during Q1 FY26) to IPP, with the long-term vision of 25% IPP contribution, enhancing profitability.

Looking to the future, the firm is venturing into offshore wind, floating solar, and green hydrogen while being financially prudent at a debt-to-equity ratio of 0.5:1 and zero near-term equity dilution. Project cost escalation and seasonal execution declines are risks that remain under control. With institutional investors from around the world, such as Vanguard, BlackRock, and Goldman Sachs, supporting the firm, KPI Green is a technology-focused renewable energy company poised to meet its 10+ GW goal by 2030.

Would appreciate hearing members’ opinions:-

-

Can KPI continue its 50–70% topline growth in the future?

-

How will margins and profitability be affected by the CPP-to-IPP revenue mix change?

-

Are BESS, hydrogen, and offshore wind genuine growth drivers or mere optional plays?

-

With international institutions put on the line, does that minimise valuation risk or must prudence prevail?

4 Likes

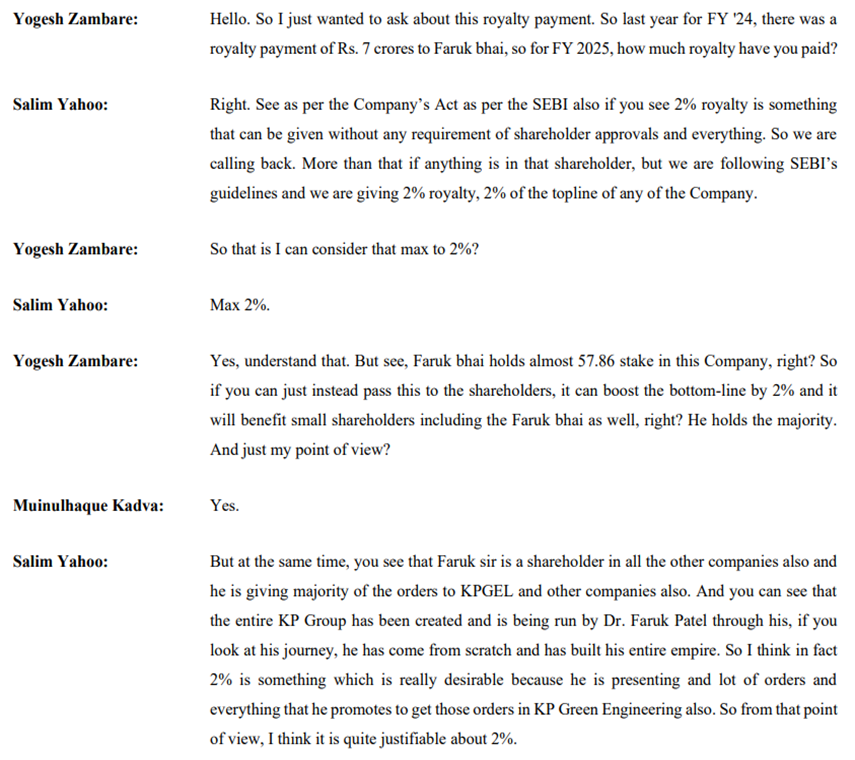

Maruti used to pay ~6% royality now around 3.5. HUL pays something similar, even the Tata companies pay it. It’s legal, so that’s that.

6 Likes

Why stock is falling so much even they are performing good from financials standpoint. Any thoughts ?