Indeed, that is the rationale behind checking ValuePickr. Does the stock have any issues? Because KPI Green is the only stock in my portfolio that is red today.

If there was no 5% circuit, then KPI green would have fallen much more than 5% yesterday. That is the only reason. Otherwise maybe kpi would have fallen 15-20% yesterday and recovered 10% today like Waaree

1 Like

Stocks typically trend sideways after a bonus or stock split.

During a 10X journey, there will inevitably be times when support levels are breached. Initially benefiting from the PM Suryoday Yojana, the sector is now facing headwinds due to increased import duties and declining overall prices, which are tightening margins.

Renewable energy is not a theme that typically attracts significant investor interest in terms of higher allocation, so it may be best to wait for the upcoming results and budget announcements. If there are positive developments regarding solar energy initiatives, the stock may recover; otherwise, only strong earnings can prevent further decline.

4 Likes

I think the reason is more related to the stance taken by Mr. Trump about the Renewable Energy. Trump is very aggressive to make America Great Again.

All Renewable projects are halted, restriction put on the import and i think subsidies also doubtfull now. So overall sector has got the hit. All the renewable share are down 30-40-50%.

Now my take is on the move from Modi Ji. Budget will show if we tilt according to US or we take our stance and allocate good for Renewable.

If Indian Govt shows backing then i think the sector should recover, may be not completely but atleast should Stable.

Also with this company my Bet is on Promoter not on the company. so All finger Crossed

2 Likes

Please correct me if I am wrong.

Waaree, Insolation, Websol etc all these panel or solar module manufacturing companies are the most affected ones right? If US stops buying modules/panels from these players, it is a risk for them. However all these manufacturers are on expansion spree, prices of modules/panels will only go down, be it domestic or international which is would be helpful for KPI Green or other Solar EPC.

Because Renewable energy is cheaper, regardless of what Trump says Renew adoption (hence orders) keeps growing. We even saw Coal India giving large order 1300Cr to KPI Green, so i don’t expect slowdown in Renewable energy order inflow.

As some people on twitter are saying, may be promoter pledge is key concern. I don’t what is the price at which the Margin call gets triggered. I don’t know if it already breached.

4 Likes

I have the same opinion that with Trump policies might impact solar pv/modules manufacturers business and therefore the overcapacity should lead to price fall for these which should ideally be favourable to players like KPI green.

However an another view is that all these might impact the future PPA tariffs as the cost of energy production would go down which should bring down the future annuity cash flows for IPP business of KPI green.

Management should bring clarity on the impact of these decisions on IPP business PPA tariffs.

1 Like

If module costs decrease, then both EPC and IPP constructions will become cheaper for KPI Green. KPI is also shielded against any fall in solar EPC due to their IPP business. This makes them safer than Waaree Renewables according to me and the lower PE multiple than Waaree by so much adds icing to the cake.

The one risk to KPI is on a technological aspect related to IPP as any improved efficiency could mean existing solar sites becoming of less value. I am bullish on KPI Green at current levels.

Disc - Invested

3 Likes

Definitely the cost of project for IPP business comes down. In my view this happens to entire EPC industry. Therefore at Industry level the PPA tariffs bidding will become more competitive leading to fall in realization per unit (which is anyway low )and therefore loss in revenue from IPP business from future agreements.

Invested.

2 Likes

Yes, if IPP PPAs price points are revised/renegotiated, the revenue potential (& margins) will take a hit. But the fall in module prices will offset that. I am assuming Margins will be more or less stay where they are or may be fall a bit.

My biggest worry is competition, the likes of NTPC Green & Adani Green. I feel ultimately it will boil down to who procures Land, Modules/Panels and PPAs at the least cost.

- Adani Green is exempt from restriction of buying from Indian module manufacturers ALMM thing, which means at the moment, they can buy cheaper Chinese modules.

- They have the humongous land bank, Adani Green is scaling to 50 GW, so you can guess who is going to be cost leader

Although players like KPI Green and Oriana have IPP particularly in Khavda, I read somewhere that these 25 year PPAs can switch with 1 year or 6 month notice.Guess who will they switch to.

I am bullish from short to medium term (1 to 2 years, till these orders in hand get executed), but long term I exactly don’t know how it pans out.

I have entered at 370 price, given that it is debt free and has good revenue visibility for atleast 6 to 18 months. They seem to be on track for 1500 Cr revenue , assuming 15 or 16 full year EPS. If they walk the talk, 40 - 60% growth FY26 EPS is 24. So it is less than 15 PE for next year. Plus, Mr. Faruk said no more equity dilution for next 2 years.

So if market agrees on giving 20 PE FY26, 33% upside.

Please let me know if there are any major flaws in these assumptions, happy to be corrected.

5 Likes

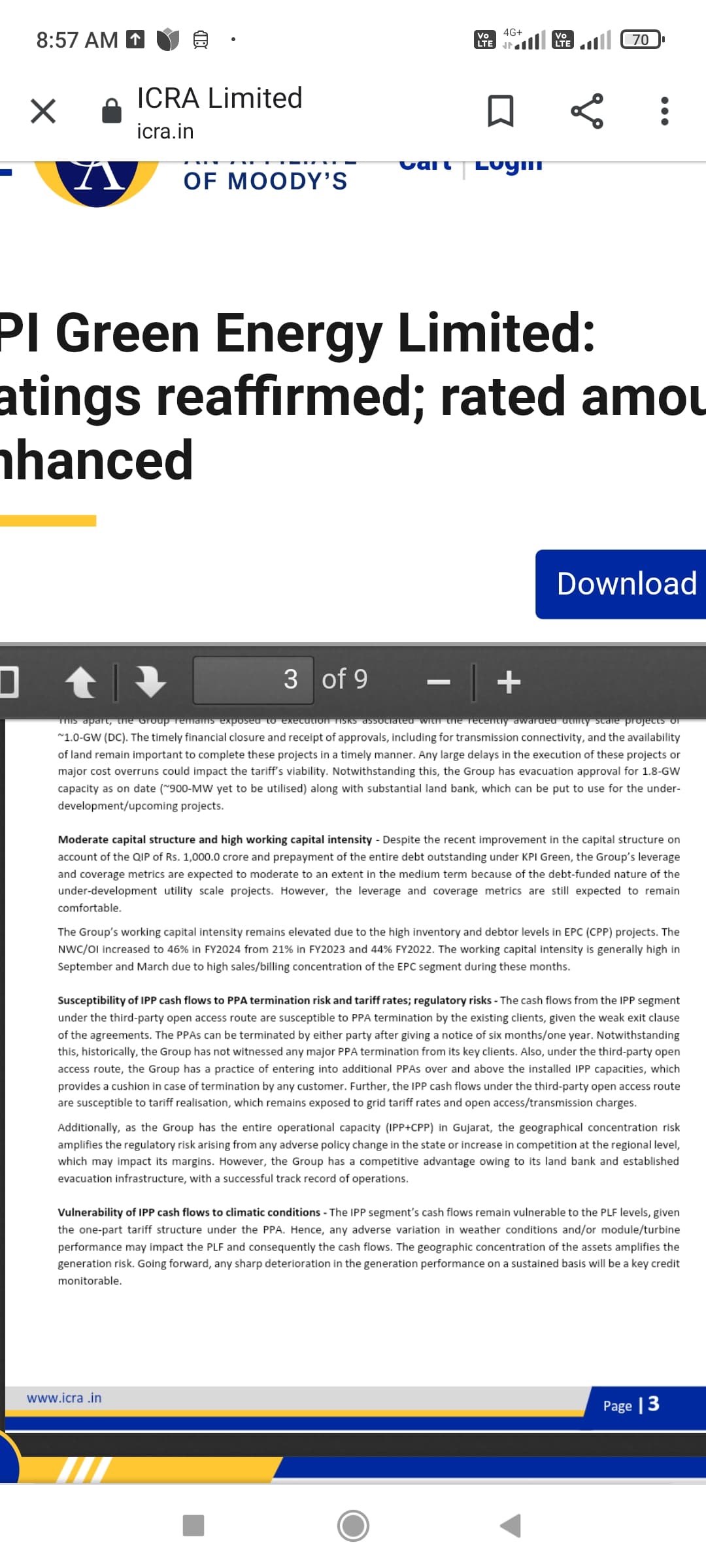

Yes. As per the credit report the PPAs are vulnerable to weak clauses . So it all depends on how the overall discoms & consumers react to these decisions leading to uncertainty. Probably that is why market reacted with so much fall.

However in my view the current price should factor in all these realization risks. It should show some stability at current level.

1 Like

Websol sells its cells in domestic market now in DCR. They are selling 92% of their production in domestic market so USA impact should not be much but taking markets into consideration, its the ripple effect in all cell companies.

Disc - Exited KPI and Websol both

2 Likes

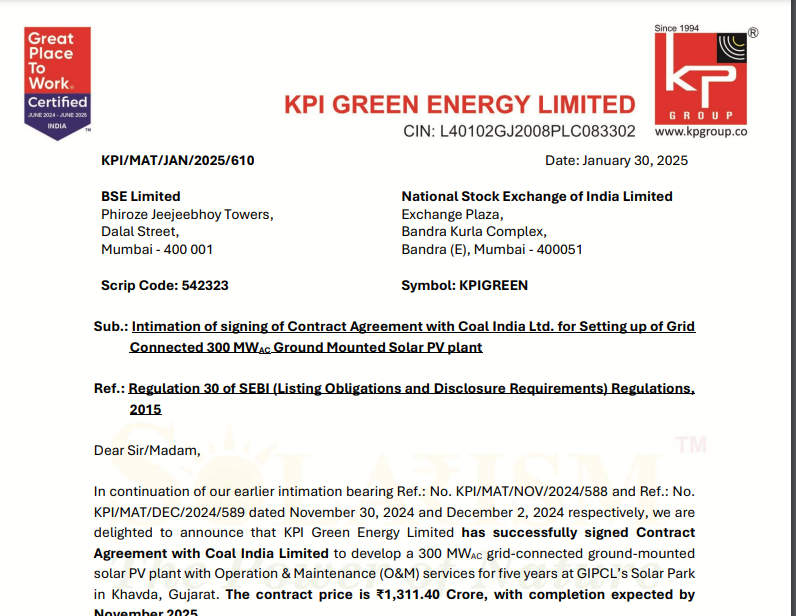

KPI Green Energy Limited has successfully signed Contract Agreement with Coal India Limited to develop a 300 MWAC grid-connected ground-mounted solar PV plant with Operation & Maintenance (O&M) services for five years at GIPCL’s Solar Park in Khavda, Gujarat.

The contract price is ₹1,311.40 Crore, with completion expected by November 2025.

2 Likes

while they have got a large contract… the question is how much margin are they making on this… and is these are fixed costs contract then what is the risk involved in increase in costs…

all in all the solar business has become very competitive and will not be as high margin as it has been in the past.

Also with INR depreciating will the project costs go up as most of the equipment are imported… modules are only fabricated in India.

3 Likes

Assuming O&M at 2L/MW/year - the O&M value would be ~18cr. EPC value ~1290cr, ~4.3cr/MW.

If they manage their costs well, as they have been doing so far, they can manage it in ~3.5-3.6cr/MW as per the current industry trends (this does not factor in domestic content requirement for cells which increases the cost 20-25L per MW min). It’s roughly an EBITDA of 15-20%. Which is lower than their ~35% EBITDA today.

However, they have been making this EBITDA consistently and we do not really know the past revenue/MW they realised as they typically only disclosed the capacity which was awarded.

Discl: invested and biased

4 Likes

The biggest risk in this company is Corporate Governance. even if there is profit in the business if it does not come to the minority shareholders whats the point. So many issues have been pointed out by many people in this forum… and one can always find out independently…

KPI is a average return high risk company for me…

QIP at such a high price and then correction of 50% from there itself raises a lot of doubt… are the large institutions like MS stupid… or there is something with retail investors are missing…

2 Likes

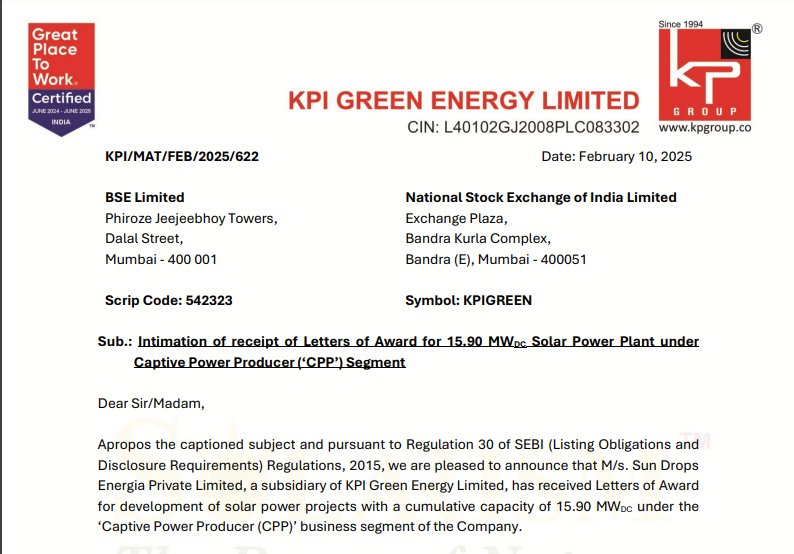

KPI GREEN | WINS ORDER

M/s. Sun Drops Energia Private Limited, a subsidiary of KPI Green Energy Limited, has received Letters of Award for development of solar power projects with a cumulative capacity of 15.90 MWDC under the ‘Captive Power Producer (CPP)’ business segment of the Company

The projects are tentatively scheduled to be completed in the financial year 2025-26, in various tranches as per the terms of the orders.

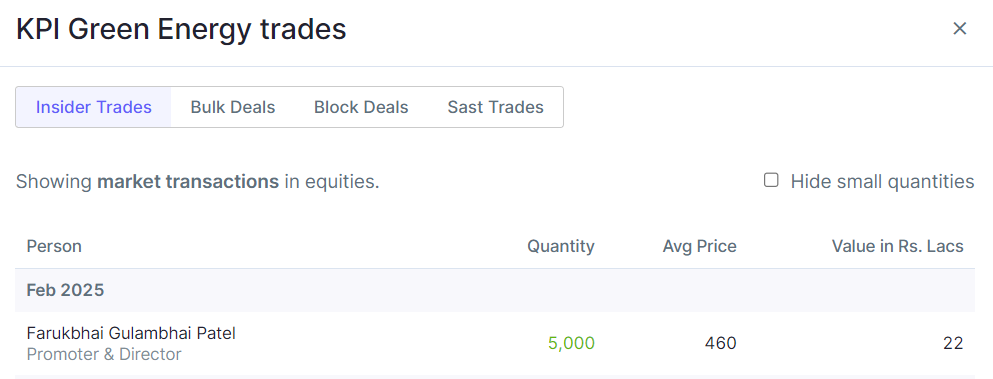

KPI Green | Promoter Purchase

Farukbhai Gulambhai Patel (Promoter) bought 5000 shares of INR 22.977L - Rs. 459.55/sh

3 Likes

he has also converted loans to company (Sundrop) into equity a few months back… and the price was also not disclosed !!

Most of the value in this group… buy way of stake, land sale, loans, etc is being captured by promoters.

one big risk investors are overlooking is performance of solar cells over long run and also variation in generation which can happen. also the quality of panels being put up…

4 Likes

While the criticism continues, the company is doing what it has to, focus on work and execution:

Another MOU with the MP Government:

8 Likes

More order flow: Receipt of new orders for 13.80 MW Solar Power Plant under Captive

Power Producer (‘CPP’) Segment

KPI green is down 40% from QIP price.. even Morgan Stanley which was the biggest investor in QIP is reducing stake at a loss !!

inspite of all announcements stock is declining.. Share price of any company with Corp governance concerns will be subdued… only high risk investors will invest in such companies.

Does anybody know the life of the solar plants they are putting up.. quality of panels, etc.. even in investor calls these points are not raised.. when markets are bullish every fundamental question is ignored.

whom is the land being bought from - promoter entities? or like in Sundrop, loans for land purchase being converted in equity at low price..

2 Likes