In this topic, KPI Green- Turning Sunshine Into Cashflows. We have been monitoring the company’s performance, and it would be wonderful to share insights with fellow members on its strengths, weaknesses, and long-term outlook.

KPI Green Energy Limited (KPIGREEN) reported its fifth consecutive record quarter in Q1 FY26, driven by robust execution across Independent Power Producer (IPP) and Captive Power Producer (CPP) businesses. Topline grew 73% YoY to ₹603 crores, EBITDA by 64% to ₹217 crores, and PAT by 68% to ₹111 crores, with EPS up 44% to ₹5.28. Cash profit jumped 92% to ₹163 crores, reflecting good cash generation. Management has pegged PAT margins of 15-20% and topline growth of 50-70% in FY26, reflecting optimism for continued momentum.

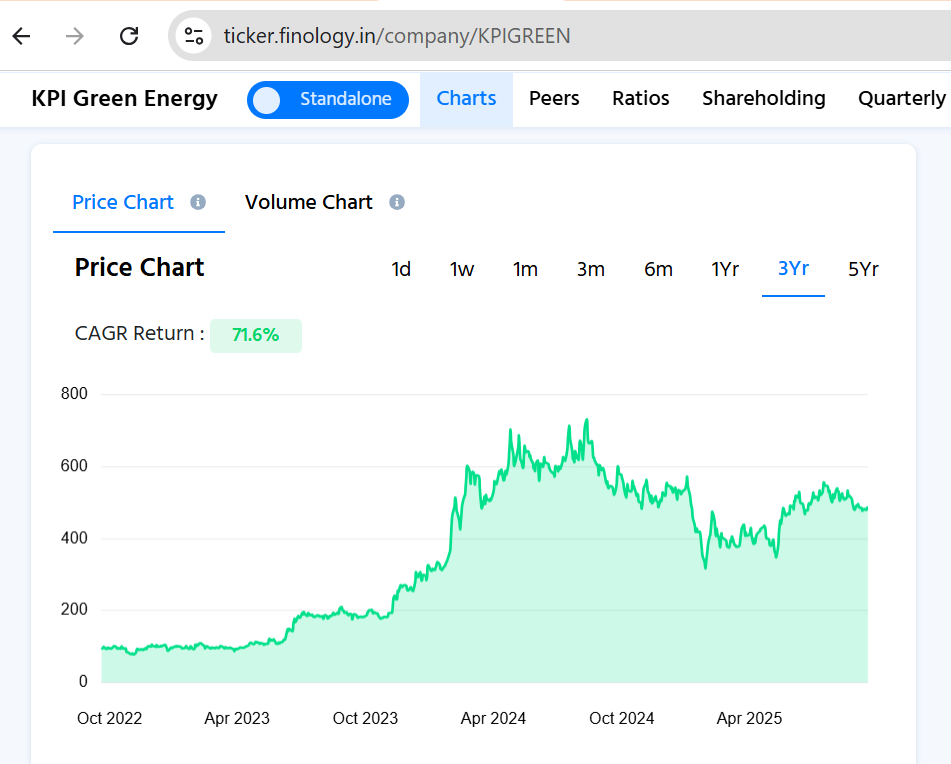

Over the last year, the stock has declined by 10.6%, indicating near-term weakness or a correction following its steep rise. This can be due to profit booking, sectoral issues, or general macroeconomic influences. But from a 3-year perspective, the stock has posted an excellent return of +71.6%, indicating robust creation of wealth and highlighting the advantages reaped by medium-term investors during the growth cycle of the company. Over a 5-year horizon, the stock has returned an impressive +128.7%, fully doubling the wealth of the investor. This strongly suggests that, for all the short-term fluctuations, the firm’s strong fundamentals and potential for long-term growth have not been compromised.

The operational strengths of the company consist of a 4+ GW portfolio comprising 1.7 GW IPP and 2.3 GW CPP, an order book of more than 3 GW (₹4,000 crores of CPP alone), a large land bank of 6,275+ acres, and more than 3.2 GW of sanctioned evacuation capacity. High-value projects under implementation - solar, wind, and hybrid of ₹5,000 crores are supported by 25-year PPAs with GUVNL. KPI Green is also expanding through collaborations in BESS, hydrogen, and EV charging with Delta Electronics, and is preparing its subsidiary, Sun Drops Energia, for an IPO. The mix of revenue is anticipated to change gradually from CPP dominance (90% during Q1 FY26) to IPP, with the long-term vision of 25% IPP contribution, enhancing profitability.

Looking to the future, the firm is venturing into offshore wind, floating solar, and green hydrogen while being financially prudent at a debt-to-equity ratio of 0.5:1 and zero near-term equity dilution. Project cost escalation and seasonal execution declines are risks that remain under control. With institutional investors from around the world, such as Vanguard, BlackRock, and Goldman Sachs, supporting the firm, KPI Green is a technology-focused renewable energy company poised to meet its 10+ GW goal by 2030.

Would appreciate hearing members’ opinions:-

-

Can KPI continue its 50–70% topline growth in the future?

-

How will margins and profitability be affected by the CPP-to-IPP revenue mix change?

-

Are BESS, hydrogen, and offshore wind genuine growth drivers or mere optional plays?

-

With international institutions put on the line, does that minimise valuation risk or must prudence prevail?