Margins of education segment of Q2FY25 looks lowest in last 8 quarters. Can someone help how to read this?

Education has seasonality, Revenues depend upon admission season.

As per the below snippet from AR, company recognize registration fee on the commencement of semester & course fee on straight line basis (& hence creation of contract liabilities).

Even if we assume some seasonality (and after considering below text on website), Q1 should have higher margins, which is not the case. In my view, H1 margins is the sustainable level of margins and last year was the one-off for some reason, in which case normalization of it will take 2 quarters, which would lead to slower YoY growth in H2

3 Likes

Have read last few years AR and understood that higher revenue and margins in education segment in Q3FY24 & Q4FY24 were probably because there were delays in starting the first batch of 3rd / 4th & 5th year of UG and hence that period had seen overlapping in bookings of few of those batches, which should normalize in next 2 quarters this year. If that’s true, believe Q3FY25 should be flattish quarter YoY. However, there’s some triggers on medium term that will drive growth:

Q4FY25

- As per discussion in AGM, Company is opening up 2,00,000 sq ft building in New OP block in Jan 2025. Reading this with latest AR, I believe this is for neuroscience. No details regarding the bed capacity is provided. Conservatively assuming 150 beds @ 30000 ARPOB and 50% occupancy, this should contribute 80cr annually to revenue. Bed capacity could be higher and of course, if the building is for neuroscience, it could have much higher ARPOB then this estimate

FY26

- This would be first full year of absorbing KMCH institute passed out graduates, this would bring in some efficiencies in employee cost

- As per AR, institute will be starting its first PG batch in FY26. Again just assuming conservatively 30 seats and fees in line with current UG batches, it should contribute 3cr to revenue (usually fees of PGs are atleast 2x the UG batches).

- Company will also add new 100 beds in the space in main center, which got available from shifting hostels and some educational sections in new Neelambur campus. Taking 50% occupancy and ARPOB of 30000, it should contribute ~55cr annually to revenue

FY27

- Will add 2nd batch of PG (with same assumptions as above, it should contribute 3cr to revenue)

- 300 bed Chennai hospital to become operational. Assuming 40000 ARPOB and 40% occupancy in 1st year, it should contribute 175cr to revenue

FY28

- 3rd batch of PG (~3cr of revenue)

- Assuming chennai hospital occupancy reaches 60% and 40000 ARPOB, it should add 88cr to revenue

Net debt

Company had net debt of 131cr at september end. Company would do CAPEX of 300cr for Chennai hospital and assuming would further require 150cr for completing the new building & additional beds in main center and above assumptions hold true, company would be debt free by the end of FY26 & hence savings in interest cost from FY27 onwards. However, to sustain the growth momentum, company would need to announce additional CAPEX in FY26. In AGM, mangement did mentioned that they are evaluating options to setup windmill

Insiderbuying

Promoter is regularly buying from open market every quarter (recently bought few shares this week too), albeit in small quantity, but shows management is positive about the near term / mid term future

Chairman’s speech of AGM 2024: https://www.kmchhospitals.com/wp-content/uploads/2024/08/Chairman-Speech-English.pdf

17 Likes

Hey,

Very insightful estimates. Can you please provide the basis or sources also? Has company mentioned anywhere that Chennai facility will be operational by FY27?

I think this was communicated in AGM, you can find this in Vijay’s post of Aug 2024

1 Like

Healthcare sector related updates from Budget 2025

2 Likes

Source - x.com

5 Likes

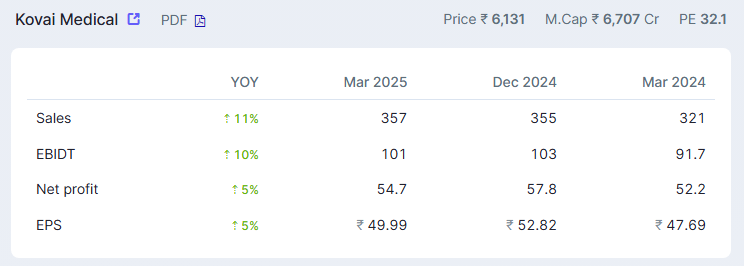

As expected company’s growth has slowed down to 9%. Still trying to guess what would be sustainable level of margins for education segment. Expecting company to return back to 15% growth from Q1FY26

4 Likes

This news initially came on 12th February 2025.

1 Like

Small cap index has fallen 26% from top, Mid cap index has fallen 21% from top, Nifty 50 has fallen 16% from top. Compared to this, Kovai has fallen 23% from top

1 Like

Wow, amazing ..

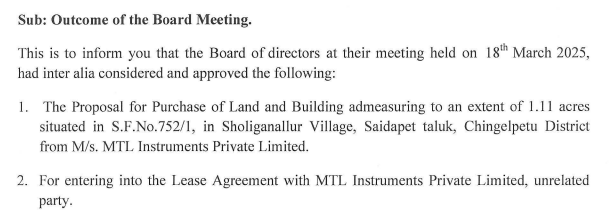

This property looks to be the next to Saravana store they bought last year, and developing now. Google showing it as permanently closed. There is another small property behind this one, lease may be for the second building.

Disclosure: Invested

5 Likes

Earnings for the quarter increased by 11% & PAT by 5% due to higher depreciation & interest YoY.

These were also impacted by lower bottom line from education segment as last year higher on account of income from overlapping batches

Expecting new beds to get added & PG batch to get started this quarter which will drive the growth for next few quarters, post which Chennai hospital will get started & give the boost. Will get to know more on their plans in AGM

5 Likes

Kovai Hospital.pdf (240.3 KB)

Annual Report Page 40-43 for the understand Hospital and other business matrix.

Massage from MD ( Page 1 of Annual report) relevant portion on growth as under

The year 2024-25 was a very good year for us. We have achieved a 12% growth compared to 2023-24. The profit margin was 15%. Our Board has recommended 100% dividend. Congratulations. Our Hospital is a 2000 bed hospital. We will

add another 100 beds in the main campus. In addition we are planning a 300-400 bed hospital in Chennai. The OP block will be ready for operation by this year end.

We take pride in our commitment to clinical excellence and delivering exceptional patient care. Over the past year, our hospital has taken significant strides in strengthening clinical excellence, expanding capacity, and embracing innovation. With increasing expectations from patients and other stakeholders, we have invested in advanced medical technologies, digital health platforms, and continuous staff training to ensure we remain at the forefront of quality healthcare delivery.

12 Likes

Good results, mainly driven by growth in education segments. Any idea if they have started PG courses, cant find anything on this in FY25 annual report

Growth will gain more legs post Q3FY26 when new beds (of more ARPOB) will become operational.

6 Likes

Hi All , I am attending KMCH AGM , any one planning to attend the physical AGM of Kovai Medical happening this Friday , 22nd ? Pls DM me

1 Like

AGM Notes.

- No guidance given both on topline & margins

- Chennai expansion will take minimum of 3 years and maximum of 5 years to get inaugurated

- Post graduation courses will start from this September onwards

- Chennai expansion will have 400 beds

- No plans to aggressively grow pan India , will concentrate on South

- Do not have additional land in Chennai other than 2.35 acres where the new facility is planned

- Planning to have a pediatric block in current Coimbatore facility

- No plans to grow the pharmacy segment , it’s only to service the hospital business

- Management emphasized on the point that they are a conservative management

31 Likes

Although Kovai has few near term triggers like PG course, opening of new OP block, addition of 100 beds in main center, growth has decelerated. Timelines for opening of new block got postponed by Jan 2025 to Jan 2026 & Chennai hospital is taking longer for construction. While the industry is on growth spree (organic/inorganic), is there any major trigger for Kovai in next 3 years, till the time chennai hospital become operational? Well this is already reflected in current valuation, as company is available at 30x P/E compared to median P/E of top 15 hospital > 65x

2 Likes