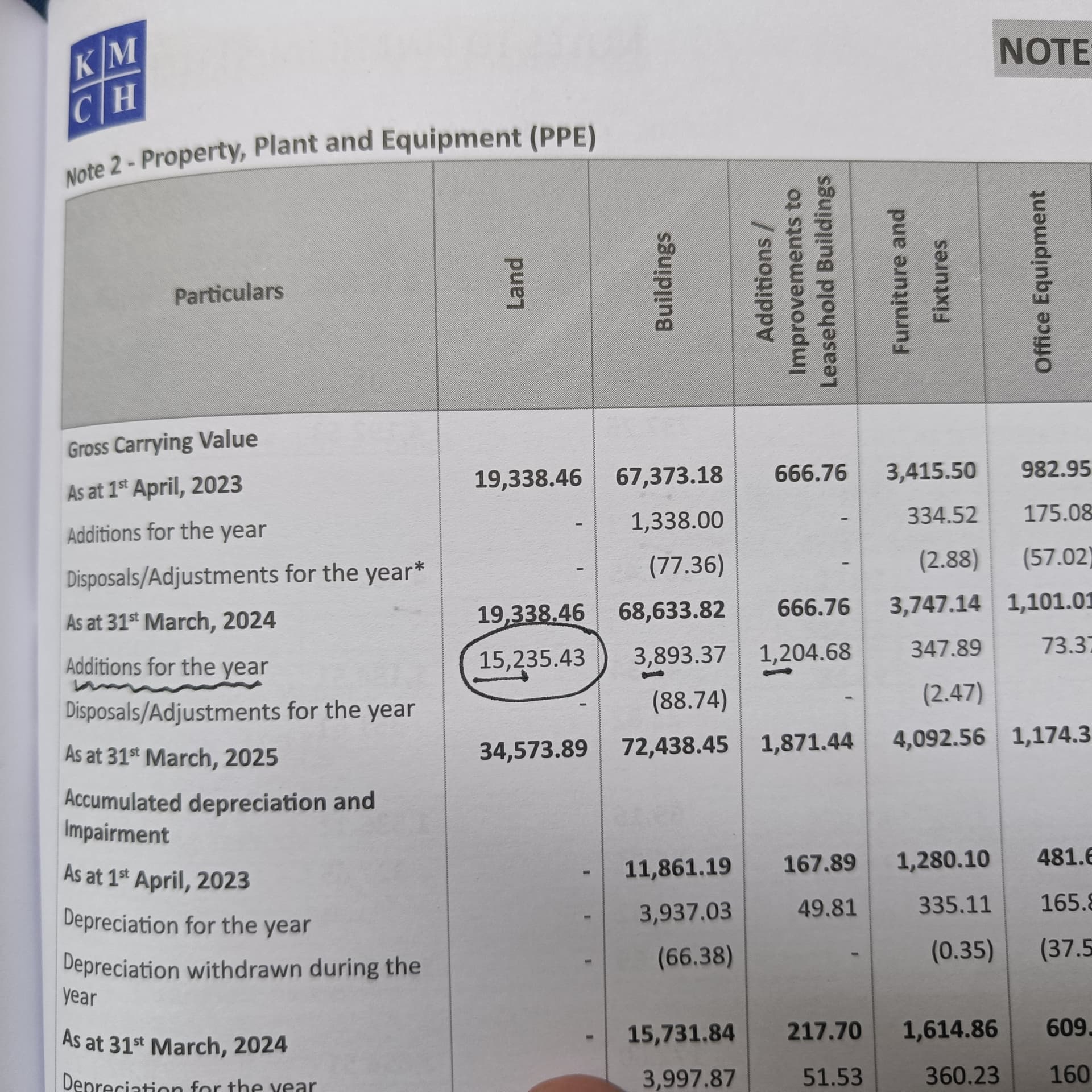

Annual report FY2024-25 shows addition of land of about 150 crores. Does it belong to Chennai hospital? Anyone has any Idea?

2 Likes

Kovai Medical Center & Hospital (KMCH) disclosed that it acquired land and building of 1.28 acres in Chennai for ~₹121 crore for business operations.

KMCH approved a proposal to purchase ~1.11 acres with building at Sholinganallur, Chennai (S.F. No. 752/1) for up to ₹60 crore (funded via internal accruals and bank loans); the same filing also mentions a lease arrangement for the property

11 Likes

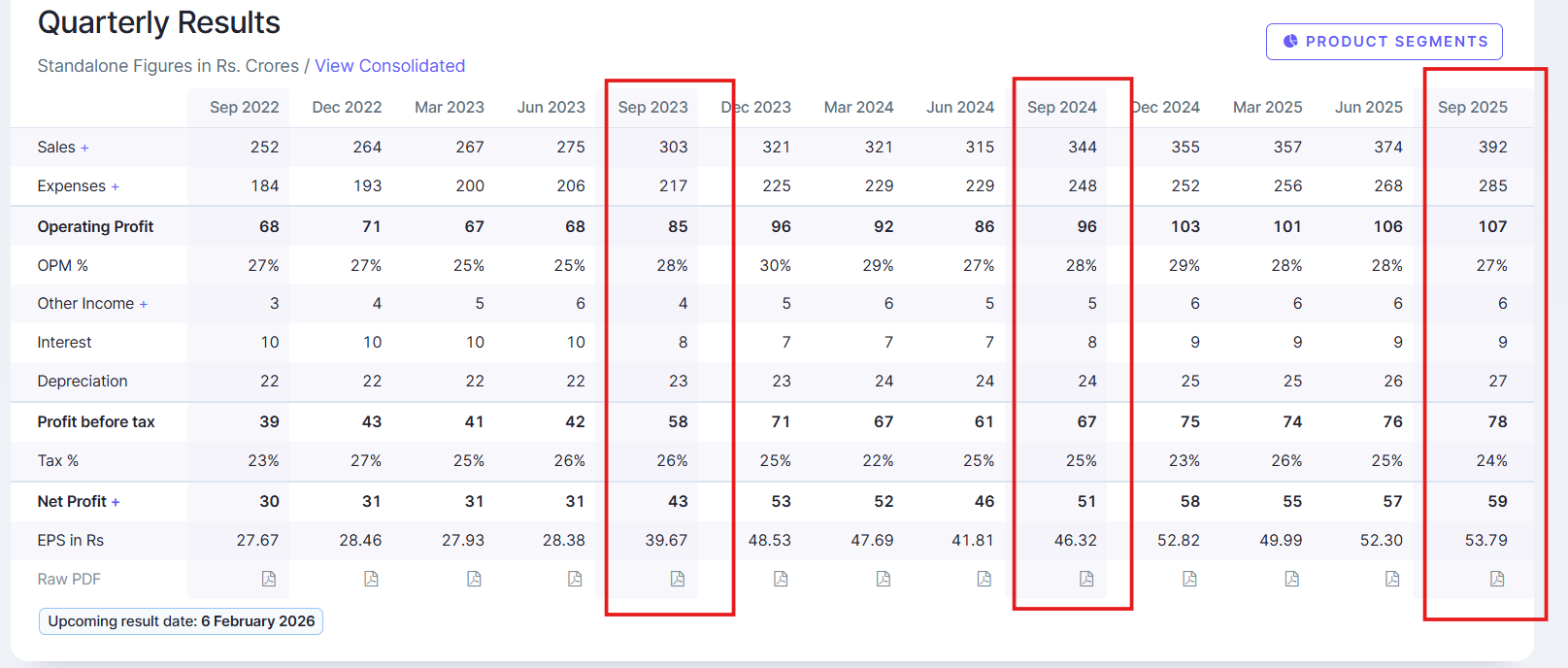

Decent Q2 results by company:

- YOY Revenue grew by 14%, EBITDA by 12% and PAT by 16%

- EBIT of healthcare segment has now reached 88cr, which was hovering around 80cr from last few quarters;

- EBIT from education segment was 5cr, compared to 16cr in Q1. Company book revenue on the commencement of academic period which is usually Q1 & Q3, also, as 1st batch of PG course has also started, expecting higher EBIT in Q3 from education segment

- Cash flow from operations too grew in line at 18%

- CWIP stands at 224cr vs 150cr in Mar’25 - looks like CAPEX for new beds is nearing completion and new beds would become operational in a quarter or two

- Debt of 366cr and cash/bank of 274cr

6 Likes

Hospital sector in general is showing sign of weakness (stock performance wise), might be because some of them are trading at more than 30x EV/EBITDA, hence little scope for further returns. However, Kovai is one of few hospital which is trading at significant discount, at current valuation it’s trading at ~15x EV/EBITDA.

To me at current levels, it’s worth looking into. Immediate triggers:

- Company is adding 100 beds in main campus for Advanced Neuro Center. It will also start new OP block (I expect it to have ~150 beds). Neuro surgeries are generally very complex hence high ARPOB and outpatient patient beds, due to its lower overhead costs, generally have better ROI

- Company is yet to receive approval on PG course; once received it would be further positive (although it’s contribution to overall revenue would be insignificant)

Together with this, company could easily clock 20% growth.

Chennai hospital (400 beds hospital) would likely get started in phase-wise manner, would be growth driver for FY28 & onwards

7 Likes

Don’t we see EVEBITDA its already penning down to 13. One of the lowest in the industry.

Yes, we should see both EV/EBITDA and P/E. Both show that Kovai is available at one of the lowest valuations in the hospital industry. In my view its largely because of geographical concentration as well as information available on the ongoing expansion/timelines / 2-3 year outlook is very limited, which makes tracking it very difficult

2 Likes

I live in Coimbatore and pretty close to KMCH and I thought I will pen my thoughts here.

-

The hospital is the go to critical care center for people in western part of Tamil Nadu - Coimbatore, Erode, Tiruppur.

-

It is renowned to be a multi speciality hospital than a single speciality hospital.

-

The doctors are some of the most experienced specialists. Foot fall is high at the main hospital and at Erode but not sure about the ones at Kovilpalayam and Sulur. Those 2 are pretty small centers.

-

I visited the main campus last September and I had glimpse at new block that is supposed to open soon I believe. It looked ready to go from the outside view. No clue about the beds or timeline in which they are supposed to open.

-

The brand name is good here and hopefully that will sustain and carry them once they complete their capex in Chennai.

-

Their medical college could act as a feeder system in my opinion for the upcoming Chennai campus.

-

They actively advertise about robotic knee replacment surgeries in the city. One such milestone that was advertised here. KMCH performs 1,000 robotic-assisted knee replacement surgeries | Coimbatore News - Times of India

Another recent one that is on advertising hoardings around here in January:

14 Likes

The business is hardly growing at 10% from past 2 years and hence the current valuation, what are the triggers for it to achieve 30% growth YOY?

This is definitely not a screaming buy !

1 Like

Past numbers reflect the capacity constraints they faced. But with the new block inaugurated in Jan '26, it should be better in coming quarters.

But still, expecting a 30% YoY growth with a PE of 25 may be unrealistic. It is a steady compounder and should not be viewed as rocket. ![]()

3 Likes

Thanks for sharing your thoughts here, these are very useful feedbacks to get. Having been a very long-term investor here, I love the consistency in the performance of the company and the reinvestments they keep doing from time to time in business expansion. Also, whenever I read their annual report, I get a very good feel about so many new things that they are doing in the medical field and our amongst the 1st to bring so many new medical solutions to the city and country.

20 Likes

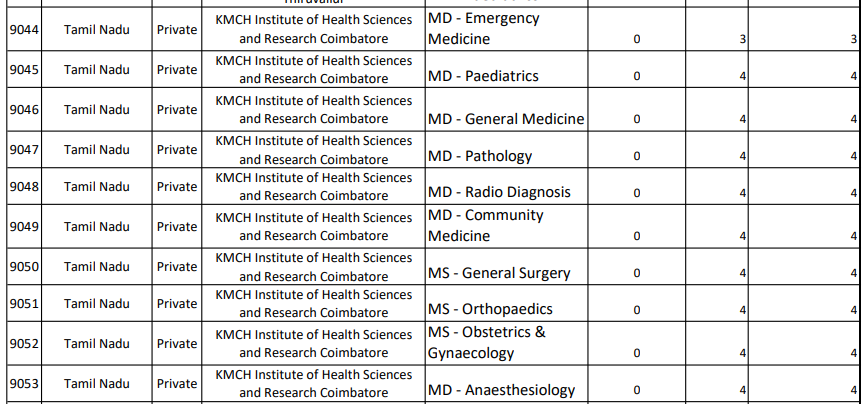

Seems like KMCH has got approval for 39 PG course seats. Can anyone confirm if this is correct?

4 Likes

Decent results:

- Revenue grew by 15% YOY; EBITDA grew by 13% YOY; PAT grew by 13% YOY

- Healthcare EBIT grew by 10% (seems largely due to annual price increase, as there were no new bed additions during the quarter)

- Education EBIT grew by 36%

- Company has announced 300 bed brownfield expansion at Sulur for CAPEX of 300cr (timeline- 3 years)

- Also announced 300 bed hospital at children hospital at main campus for CAPEX of 300cr (timeline- 3 years)

FY27 revenue growth would be driven by the recently launched Neuroscience, OPD block and PG Institute; Beyond that, growth will be driven by the opening of Chennai Hospital & recently announced Sulur Hospital and Children’s Hospital. By the end of 3 years, Kovai’s total beds would increase from 2000 to 3000.

9 Likes

Any idea if the new block is operational already or by when it will be operational and whats the bed addition in this new block ?

Many large pharma in India are launching Generic GLP-1 shortly. From the US market, it is clear that Bariatric, Cardio, Orthopaedic are affected most by GLP-1. Many Indian hospital stocks have high exposure to Cardiology and Orthopaedic.

Has anyone calculated what is the impact on Kovai and other hospital stocks cause of these generic weight loss drugs?

Is there study on affect of GLP-1 on Bariatric, Cardio, Orthopaedic from other market?

1 Like

there is no study as such. But US hospitals reported 20% reduction in bariatric surgery volumes. For Cardiology and orthopaedic,high acuity inpatient cases remain stable, while routine procedures are rapidly moving to outpatient settings. For orthopaedic, volumes will rise in short term as more patients become eligible for knee/hip replacement as weight drops. But it is predicted by 2030, the growth rates will take a hit for cardiology and orthopaedic as weight loss drugs are mass adopted. So terminal growth rates may take a hit.

I have sent emails to Kovai, KIMS, medanta, Yatharth, Narayana Hrudayalaya, Fortis, Max Health investor relations asking what is the affect and what is their strategy. No one has replied yet.

3 Likes

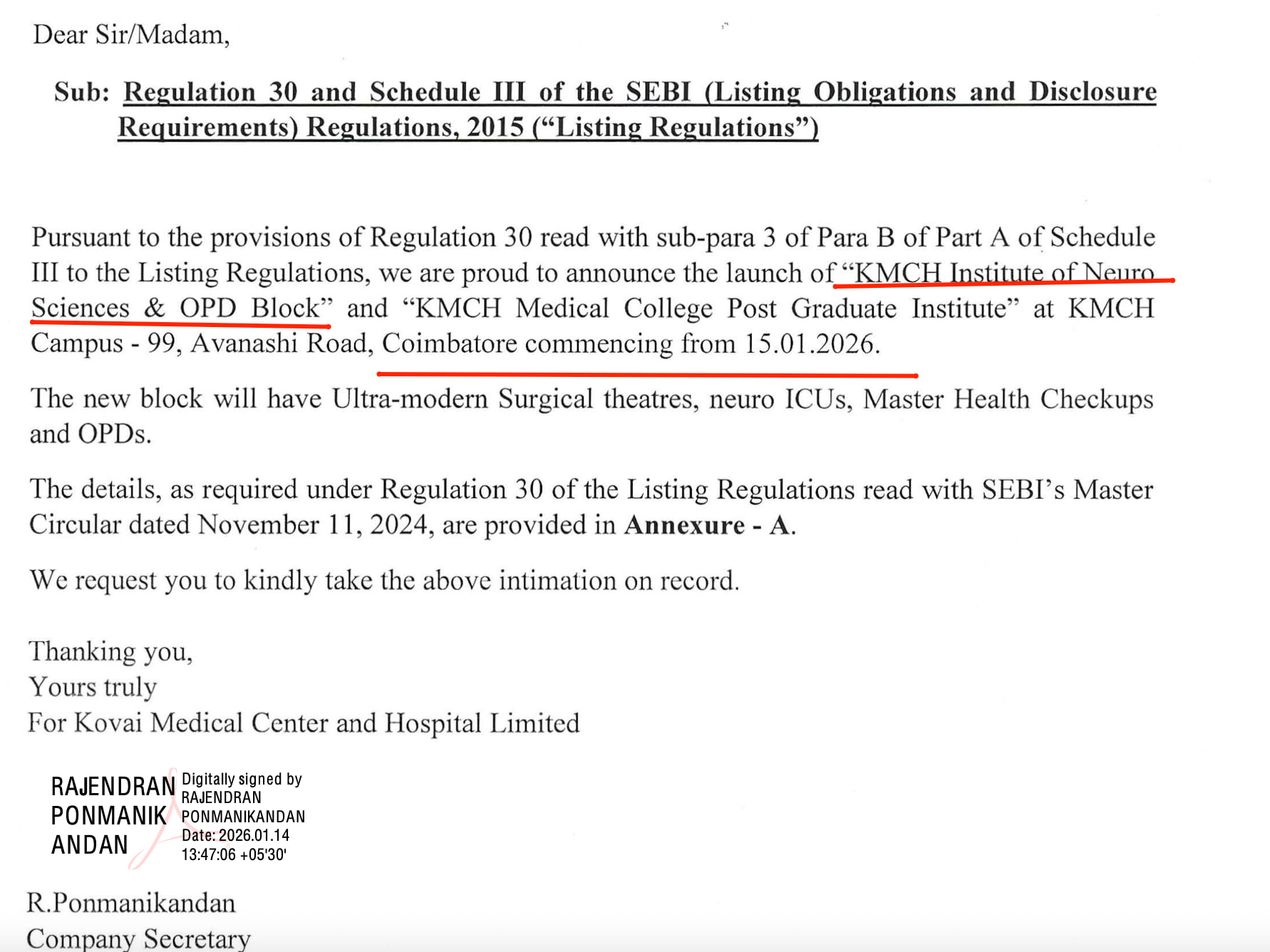

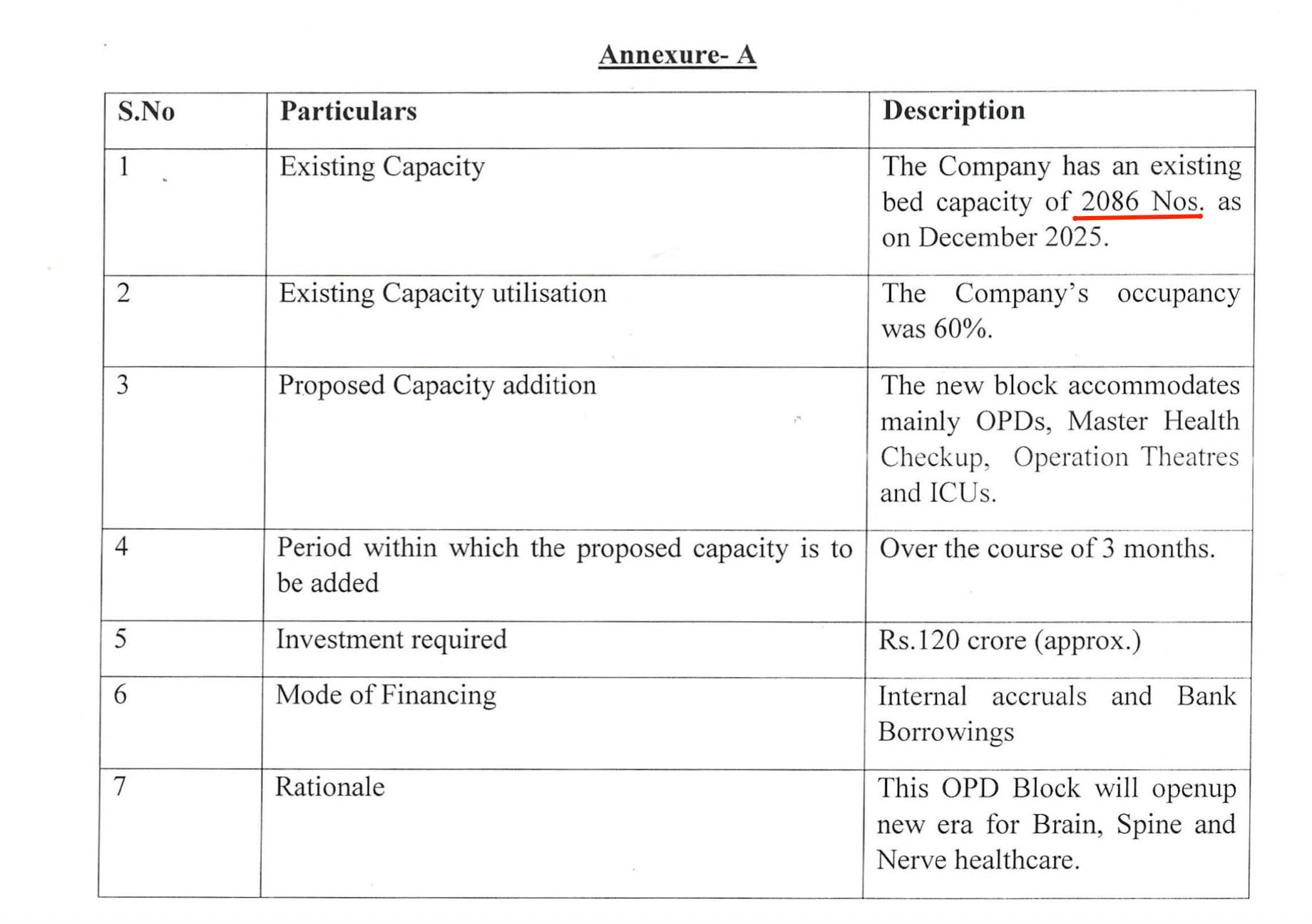

New block launched on 15.1.26. I am not sure about the exact number of beds added in this block. MD had mentioned that 100 new beds will be added in the last annual report.

In the Annexure, they have mentioned proposed capacity addition is going to be added within next 3 months. So I am not sure if this new block will have meaningful revenue impact in the ongoing Q4 quarter.

https://www.bseindia.com/xml-data/corpfiling/AttachHis/6b7c4d90-07a6-4265-869d-cfba37046e41.pdf

4 Likes

Does the medical college give KMCH an addition to the regional moat it seems to have? Colleges will attract doctors who enjoy teaching new doctors and also new graduates who will want to settle down in Coimbatore and practice their vocation. This seems like a good development for the hospital. As a shareholder, I wouldn’t mind if the company only makes reasonable profits required for development and to provide cutting edge treatment as I understand that medicine shouldn’t be solely driven by profit motive.

1 Like

New block became operational from today

7 Likes

Thanks for sharing the detail.

Though hospital is doing good and there are no glaring issues in fundamentals, stock price has been depreciating for the last 6 months inch by inch.

Can there be any reason for this fall? I wish promotor buys, but they haven’t bought recently as well. Is there anything we are missing?

1 Like