As per an email response from the company, the company shares are listed only on BSE but not on NSE. They were traded on NSE as part of a NSE’s marketing strategy. Seems that marketing strategy period for trading of this company shares may be over and company would have to formally list its shares on NSE platform by following the procedure which may also need monetary expenses in form of listing fee etc. As of now company doesn’t have any plans to list its shares on NSE and it seems to be the case that company wants to save some cost. As such it’s not because of any kind of ‘ban’ that they’re not traded on NSE.

Seems like this is a pretty common scenario that I got to know recently. There are many such companies that are listed only on BSE and not on NSE, which explains why NSE might have a marketing strategy to temporarily trade shares that are not listed on it.

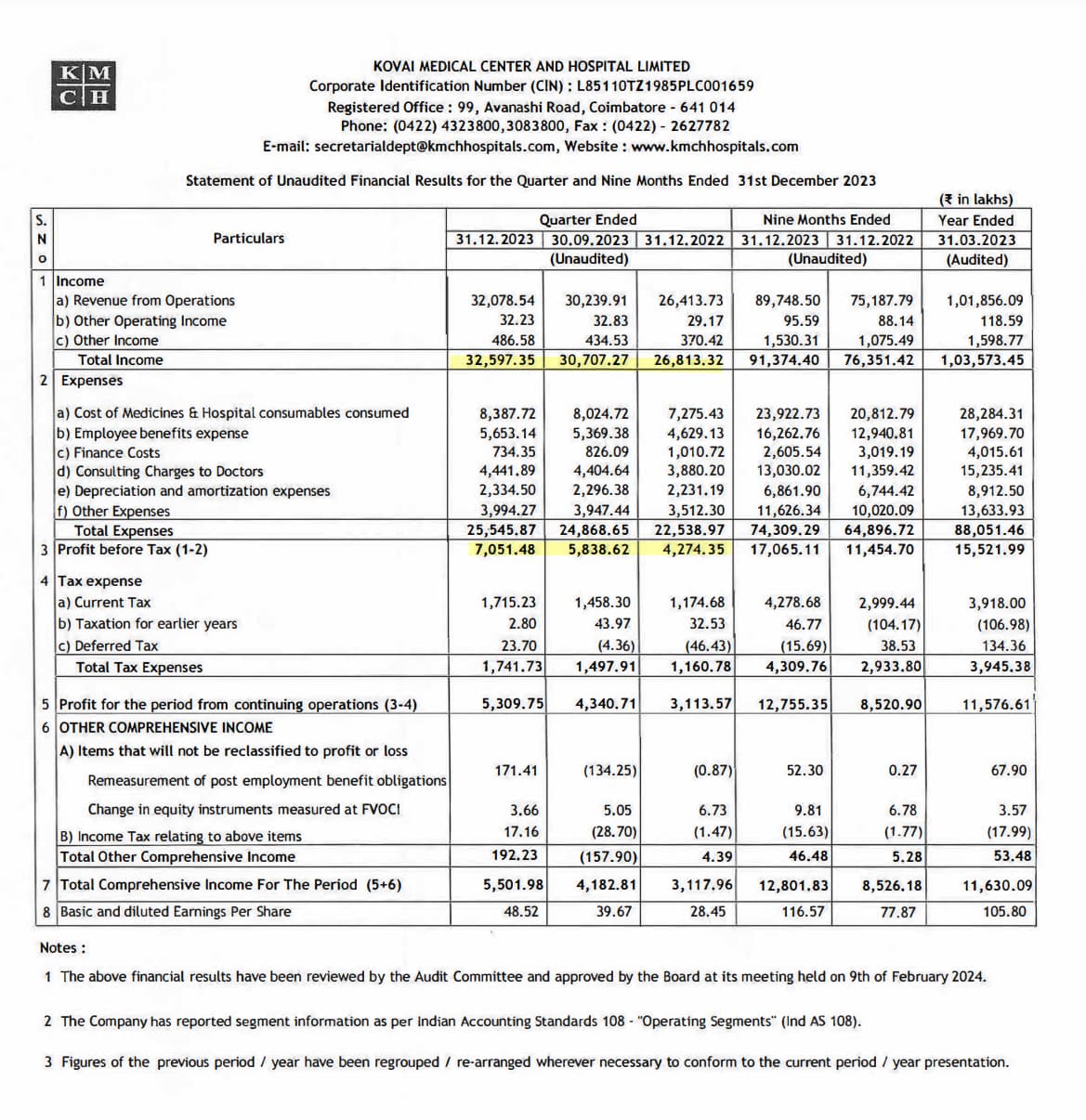

20% increase in Revenues YoY; 11% increase QoQ as well. It looks like business is back to normal at last.

The 38-40% increase in Profits is a little deceiving, since Cash profits have only risen 7-8% (Increased Working Capital and higher Taxes)

But the real kicker for me is the bulk repayment of long term Debt to the extent of Rs. 118 Crores. We can see the immediate impact in Finance Costs reducing from Rs. 36.53 Crores in Mar 2023 to Rs. 15.82 Crores in Sep 2023.

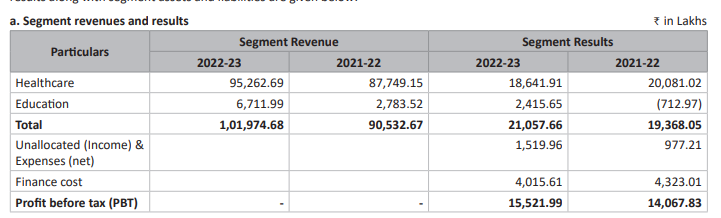

For the HY ending Sep 2023, Education segment has clocked around Rs. 14 Crores in PBT. Annualized, that’s Rs. 28 Crores - which is quite the jump from last year’s Rs. 2 Crores. Per management commentary, this could be peaking out soon. We’ll have to see how much the profits will grow YoY post that. I presume around 10% at least. 15% would be good from IRR perspective (Considering the Rs. 700+ Crores Capex that was made; but some of it was for the additional beds).

If majority of the remaining Rs. 350 Crores (Short and long term) loan is repaid as discussed by the Management, the quarterly savings in Finance costs would be around Rs. 7-8 Crores. Of course, paying off Debt also allows internal profits to accrue faster and build up a war chest for further expansion.

Its finally great to see long term debt coming down. On top of that I was really surprised by the 12 % revenue growth in the Health care segment. I was expecting to see contribution from the 5th year of admissions in this quarter. Hope to see that next quarter. With the final year in, hope to see leverage kicking in and better margins

The total debt as on November 30, 2023, stood at ₹285.45 crore

KMCH is planning to undertake capex in the range of ₹250– 300 crore in the medium term funded through a combination of term debt and internal accruals against which sufficient accruals are expected to be maintained on the back of improving operational parameters. Hence, CARE Ratings anticipate that debt coverage matrix will not moderate and will remain comfortable in the medium term.

In recent years, KMCH has emerged as one of the most successful ‘Multi Organ Transplant Center’

in the rest of Tamil Nadu, leading to an increasing number of referrals from Western Tamil Nadu and Kerala. It is recognized as a forerunner in transplant surgeries as well.

the Medical College, boasting a total of 750 seats, operates at full capacity, with

an average annual fee of ₹14 lakh. CARE Ratings expects that the revenue contribution from the medical college will improve as

the operations progress.

In H1FY24, the ARPOB of the main centre stood at ₹28,479 similarly, ARPOB for the other centres was between around ₹11,000 to ₹19,000, however, for the medical college hospital which added 238 beds in FY23 itself, stood at ₹3,388 which has impacted the overall average ARPOB level from the previous year.

While going through the latest annual report of the company I have found some interesting data about their revenue breakup. We have seen that KMCH since inception has been investing heavily in advanced medical equipment. During FY23, over 20% of revenue came from diagnostic services. I haven’t checked for other hospitals yet, but it is quite large and margin accretive I guess.

Great results. Best ever quarterly revenue at great margins. Operating leverage finally kicking in. Finally seeing the fruits of large capex. Revenue from education segment starting to contribute. Margins close to 52% on the education segment. Good to see interest costs also coming down. It will be interesting to see how the management utilize the cash they are generating.

Yes, both the top and bottom lines have performed better than expected. This quarter’s margin improvement may be attributable to both the education and healthcare segments equally. This also suggests that the education sector had a disproportionate impact.

However, now that the fifth batch has entered, the education segment may not increase significantly in the next years. The only other levers in this segment are fee revision by the state government and the addition of MD seats (what does it take to obtain this permission?).

In Healthcare segment both the hospital’ number are given together. Difficult to know which part has improved. Given the numbers in the attachment, medical college bed occupancy and uses of other facilities is good now. But seems average stay days has to reduce. We cannot expect medical college bed to earn much but it being new facility there should be scope for further improvement (in additional to inflation) from here onward for few years.

I have no idea how much volume a 150 seats medical college should be doing? I am assuming it would take some more time to optimally utilise facilities.

I think I did mistake in previous post, is one more year’ (6th year = 5th to 5.5 the year) fee due from 1st batch student, correct?

I would be interested understanding how availability of internship batch (4.5 to 5.5 year) may affect medical college hospital operations?

Not sure how healthy it will be for a hospital to run a medical school for profitability. A medical school will attract talented doctors who like teaching and will also allow young and newly qualified doctors to train during internship which is mutually beneficial. Teaching experience is also a valuable experience on a doctor’s resume. I wonder if the reason for opening the medical college is more for the above reasons than profit.

Also, Coimbatore is a lovely city with lots of decent colleges, less traffic than other major cities, good weather throughout the year except maybe the summer making it an ideal city for these doctors to settle down in.

Actually having both a medical college and hospital will allow them to offer other Post graduate courses.

As per regulations:

The Medical Institutions that have been granted permission to start Postgraduate Courses in broad specialties under Section 9.3 of these Regulations shall have the following facilities.

(a) The Institute shall have an hospital with minimum 400 beds.

(b) The Hospital, in addition to clinical specialties shall have full fledged Departments of Bio-chemistry, Pathology, Microbiology and Radiology/ Imaging including CT scan and MRI facilities.

(c) The Hospital should have been running for at least two years prior on the date of application to seek permission to start the postgraduate course

Source: https://www.nmc.org.in/MCIRest/open/getDocument?path=/Documents/Public/Portal/LatestNews/final%20PGMER%20draft.pdf

internship the interns have to be paid a stipend may not be source of income in final year

teaching collage does not mean quality of the patient care will go down

young doctors will observe and do manual and clerical work only

if patient request only senior doctors are allowed near them

patient must consent for examination

high five patient are not bothered

this will reduce work for senior doctors

without knowing how much seats have been filled not exactly sure how much revenue they can increase

there is a regulatory risk of the government capping fees and the institution getting black other wise it is completely solid

former mbbs intern at psg medical collage Coimbatore

disclosure invested since 2020