They have always had higher debt levels. When their stock price was around Rs 150, I stayed away from the stock thinking I don’t want to invest in a leveraged balance sheet. My mistake.

2 Likes

This stock is in my core portfolio since last 10 years from 160 level. It started elliptical upward journey within 1 yr since then. unlss 2-3 years consolidation 2018-21. When I looked at valuation with peers and possibility of rerating I decided to hold. Though returnwise it is not outperformed other bets in PF, but steady 17x in 10 years is not bad defensive bet either.

5 Likes

Wondering what is the probability of a bigger hospital chain/group acquiring KMCH? It will be pretty expensive for acquiring the infrastructure as well as the doctors and staff to compete with KMCH in Coimbatore. The medical college is probably a good source of junior doctors and nursing staff. Other big hospitals in Coimbatore are as follows but in no particular order:

- PSG Hospitals

- Ramakrishna

- GKNM

- KG

- Royal Care (Newer player)

KMCH is expensive but seems like a safe option always. KMCH is also a little far from the city centre. It’s around a 45 minute drive whereas KG Hospitals, Ramakrishna, PSG, and GKNM are very close to the city centre.

KMCH City Centre, which is in a very convenient location in the city, though not that crowded it is very well maintained and provides services such as dialysis and other services. The city centre is multi storied and provides an option for not so serious patients I guess. However, I am not sure if the city centre is a profit driver. Might need to dig deeper into the annual reports to see if they provide the contribution of the city centre. It might just help in directing more patients to their main campus.

KMCH main campus on the other hand is super crowded. Compared to KMCH, PSG Hospitals comparable in terms of size seems not so crowded. It might be because PSG is more spread out in terms of its buildings but not sure. Even PSG has a medical college and is much older than KMCH and is just as well known in Coimbatore but maybe cheaper. PSG is not a public limited company.

3 Likes

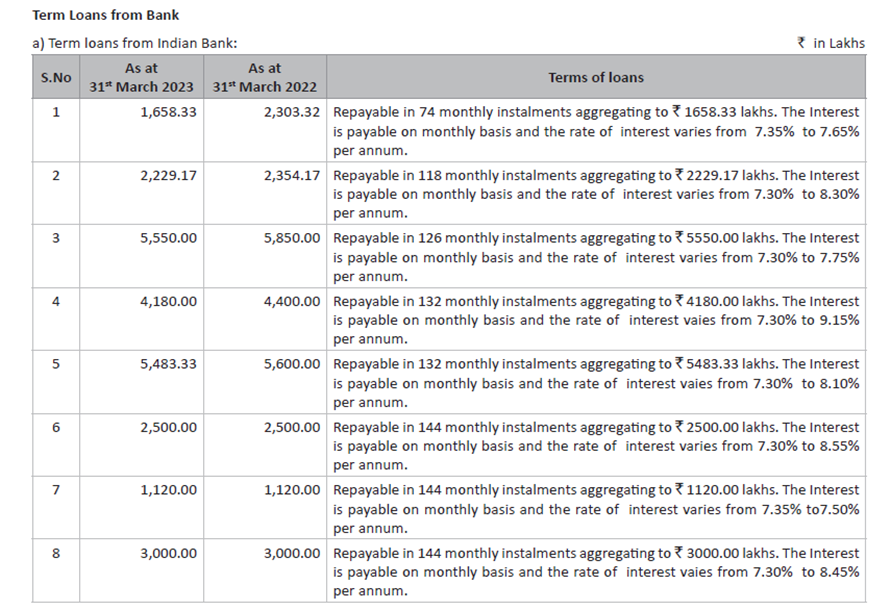

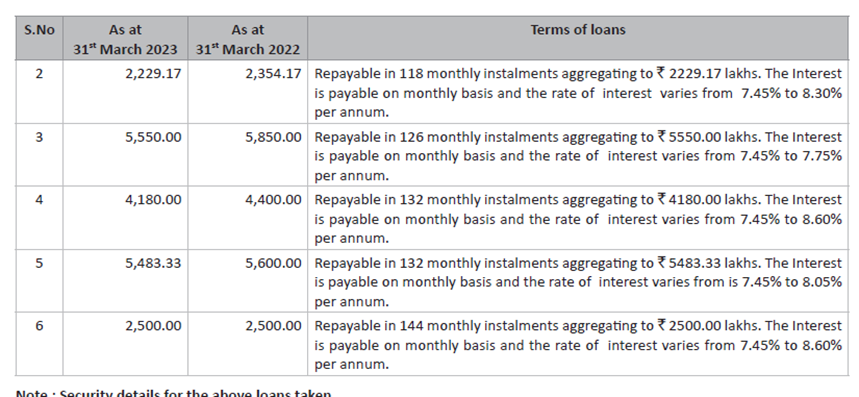

They have given a good picture of the debt in the AR.

I think most of the loans are at MCLR 1 year rate.

The current part of borrowings is 25 crores which is the minimum expected repayment next year.

Interest capitalised is NIL in the current FY against 60 lacs last year as per the AR.

Interest capitalised was 50 crores in 20-21.

![]()

Last year they paid an interest 43 crores which is huge considering net profit of 105 crores. They have a cash of 249 crores as of Mar’23. It would be great to see some reduction in debt unless they have some new plans.

5 Likes

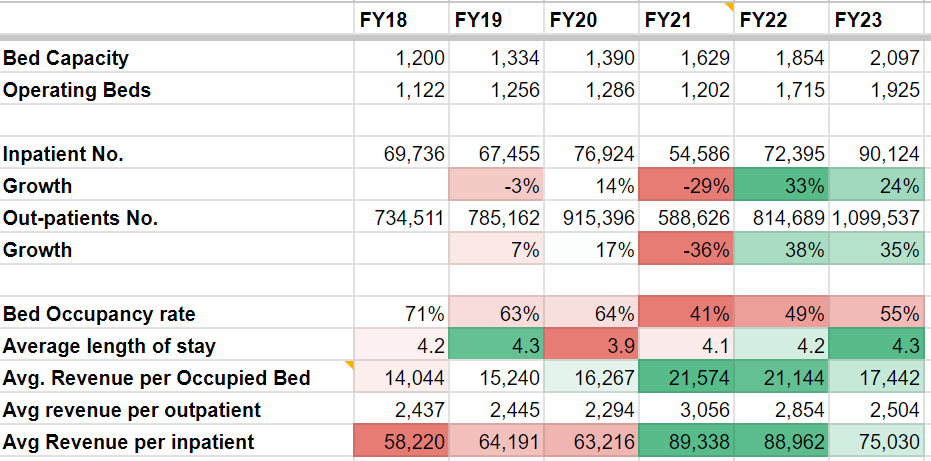

Massive growth of about 25-30% in the no of patients coming to the hospital. However, the aveg revenue per bed has fallen as the rates would be lower at the medical college vs the main hospital. But I think as the medical college gets stabilized and gets more reputed, perhaps this will also see revision in prices and profitability might improve with time.

Interesting to see acquisition of large land. We need to see if they are coming up with a new hospital and where.

Ayush

Disc: same as before

26 Likes

Does these figures (for beds/visitors) in XL include Medical college ? If it were so, the beds would have grown more than the 2000 odd that we are seeing.

Medical college has " 750 general beds including 50 ICU beds, 30 emergency beds and 16 operation theatres" by itself.

PSG is a trust based hospital and as per medical collage requirement’s it is run not as per corporate

since it is a trust it is main moto is well fare of the people although i am highly skeptical of it

in medical collage system the doctors are paid based on their experience although some amount of pay by the amount of work is there i am highly skeptical as only established doctors can benefit in short environment may not be conductive for a highly skilled doctor as they are more than happy with the tuition fees for collage and not much about the earnings of a doctor the earnings of a doctor will result in retention of talent

as far as medical collage is in concerned both psg and kmch is more or less equal and based on the huge demand there is no threat

however because of medical collage bed revenue in kmch may go down as they have maintain minimum occupancy ratio so they are forced to admit low paying patients

bed occupancy in kmch should be improved to at least 75 %

i can tell the only viable competitor is royal care hospitals

KG ,Ramakrishna ,GKNM are viable competitors but not a threat

views are personal

student of psg batch 2014 mbbs now doing hospital administrations course

5 Likes

Q1 FY 24 results are out.

Revenue:

- 274 crores (Q4 FY 23 - 267 crores and Q1 FY 23 - 236 crores)

out of which:

- Health care revenue - ~256 crores

- Medical College revenue - ~18 crores

Net Profit:

- 31 crores (Q4 FY 23 - 30.5 crores, Q1 FY 23 - 24 crores)

Not much reduction in either interest costs(~10 crores) (or) depriciation( ~22 crores) compared to Q4/Q1 FY 23

5 Likes

Thankful for the detailed analysis and notes mentioned above. Had done a small analysis on various hospitals during Yatharth’s IPO.

Considering the run-up of various hospitals, Kovai is the only one that seems reasonably priced. Indraprastha is stuck in legal issues considering their agreement with Delhi govt. for providing free-of-cost treatment in lieu of lease of hospital land.

Note: Data is from early Aug for other hospitals

The only issues I can see are:

- The company doesn’t seem to have geographical expansion plans. It’s a good stable business that appears to be undervalued but no amazing story

- Medical college is impacting PAT margins and the company has high interest costs

- Lack of institutional interest and low market vol. depth

- The Google reviews (not sure how reliable they are) are not favourable. Usually they’re above 4 for major hospitals in most cities, see Royal Care is 4.3. This might impact patient inflow

- Lack of medical tourism, which is a very high margin business for most hospitals. They don’t have MTQUA certification (only NABH) which Sri Ramakrishna Hospital in Coimbatore has

- From annual report, their Inpatient nos. increased 25% while revenue only increased 5% (decrease in ARPOB) which they need to pass on

Pros:

- Promoter holding has increased this quarter

- Cheaper valuation (P/E, EV to EBITDA, CFO to EBITDA) compared to other hospitals (see KIMS) considering the no. of beds and strong brand image (as per their AGM and comments from people above)

- Most of Coimbatore population is in urban areas and it is growing at 2.65% rate per annum (same as Delhi)

- In Tamil Nadu, IPD per 1000 is double that of India, implying people are more inclined towards hospitalization services in the state

Happy to get feedback, insights from other people

Disc: Invested and averaging down

3 Likes

Google reviews are probably not that reliable in this case. Royal care probably does a better job of getting their patients to leave a review than KMCH. The number of reviews seem to be relatively too few to make the average rating reliable.

1 Like

The google rating is 3.3 from 1380 reviews, not insignificant, whereas Royal Care is 4.3 from ~600 reviews. This is a primary organic information source for a lot of new customers aside from word of mouth.

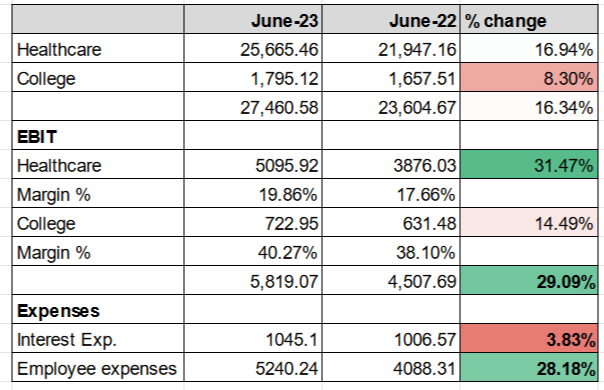

I was going through their Q1 FY’24 financials:

I think the AGM is on 25th Aug. If someone is planning on going and ask the below questions or knows the answers and can shed some light:

- There has been a healthy growth in EBIT (30%), then why have they not paid off the debt (see interest expense). Are they planning on using the money for some expansion plans?

- Employee costs have gone up 30% YoY basis. Aside from appraisals, what is the reason for it?

Edit: Same case for KIMS and KMC, are 30% hikes standard in hospitals ?

? - Any specific plans to scale up the occupancy of the medical college and the hospital to 75%?

- What is strategic view of the hospital to attract medical tourists, are they going for MTQUA certification or tying up with intermediaries?

- Has there been any institutional interest in the hospital stock in past half-year?

- Why is the customer rating so low if the hospital boasts of a stellar reputation, should they not address the issue?

6 Likes

To add on my 2 cents :

- What’s the plan to expand medical college from current 150 to 250 seats ? We know, this would be long term but that’s when operating leverage shall kick in

- What’s the succession planning of top leadership ?

2 Likes

all the promoters family are involved so succession will not be a problem

1 Like

Promoter group bought 16000 shares yesterday.

This is second time promoters are buying the shares in the span of 2 months.

2 Likes

It is a off market buying…they didnt buy in open market…i doubt if they paid current price for the share

4 Likes

Chairman’s speech for today’s AGM: https://www.kmchhospitals.com/wp-content/uploads/2023/08/Chairman-speech-English.pdf

Improvements/Existing status:

- Main Hospital: 100 additional beds were added during medical college expansion and pulmonary medicine dept was added (lung transplant facility now available)

- College: All 600 seats (incl. NRI) occupied along with allied health and Diploma -Diplomate N.B seats.

College is also providing free-of-cost services to poor patients and overall, daily run rate is more than 1000 outpatients and 500 inpatients

New initiatives:

- At present we are building a new specialty Center. It will have all new versions of treatment modalities and equipment. The project cost may be around 200 crores → More operating margin and/or higher revenue?

- 63 Cr spent for buying land & building (edit): Next year, allied health sciences and hospital to be shifted to new campus.

P.s. where do I get link for their AGM’s virtual conferencing?

6 Likes

-

basically 63Cr spent on almost ready to use facility (not just land), correct?

-

one more batch to join (to see peak in fee revenue)

-

100 beds were added in main hospital + 200Cr other investment to complete

Disclosure: Invested

5 Likes

Any timeline or updates on debt repayment?

1 Like

Can someone please share the notes of the AGM of the Q&A section

Kovai has experienced the biggest activity in the last year, with 59,000 shares traded on the BSE today and 90% delivery. Part of this could be because of the fact that shares are temporarily banned on the NSE platform (for unknown reasons)… still average trading volumes seems higher even on on combined (NSE+BSE) basis. Further, share closed up at 5%…

Any technical analyst tracking this stock, please guide how to interpret this.

2 Likes