looks like an annual ritual ![]()

![]()

![]()

Rs 412 lakhs in June (late batch of last year? why they booked this fee in June while admission happened in March?)

Rs 315.12 lakhs in Dec ( Regular 22-23 batch? Has one time admission fee reduced compared to previous batch?)

I am going through the annual report of KMCH of FY 21-22 and found that the remuneration

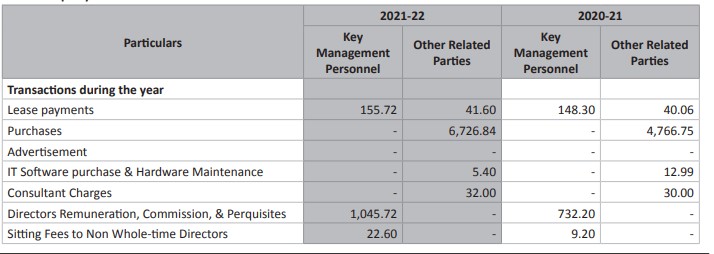

for executive directors was increased by 218.27%. Also, purchases from the related party transactions also increased from FY 21 to FY 22 - 48 to 67 Crores. Is it a cause of concern?

After spending a Day on Kovai Medical What Insight I can Derive

Liked

![]() Net Block 2X

Net Block 2X

![]() Occupancy Bed Rate FY22 48% in FY20 63%

Occupancy Bed Rate FY22 48% in FY20 63%

![]() Growth Led By EPS

Growth Led By EPS

![]() High ROE,ROCE,ROIC,ROIIC

High ROE,ROCE,ROIC,ROIIC

![]() Not Liked

Not Liked

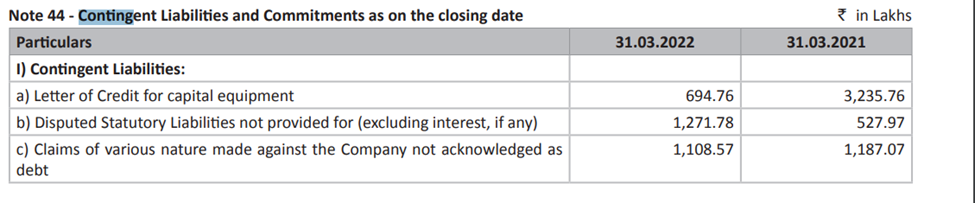

![]() Contingent Lib ~ 10% of NW

Contingent Lib ~ 10% of NW

![]() Investor Friendly

Investor Friendly

![]() Why Dividend

Why Dividend

![]() High Debt

High Debt

![]() Valuation

Valuation

![]() Regional

Regional

What if

Occupancy Rate Back to 63-70%

Debt starts Reducing due to Earning growth

Net Block Starts Yielding

Quarterly Meeting

So Adding Watchlist

I would like to point out a few things

Contingent Liability

Its 5 % of net worth and close to 7 crores is letter of credit.

Debt

Debt of 534 crores is huge if we look at it separately. The company however has cash and cash equivalents of 235 crores as of Sept’22. At the last quarterly run rate the company could be net debt free by the end of next FY. Interest payment is currently huge but can considerably reduce if the company uses cash to pay down debt.

Valuation

The company is available at a trailing EV/EBITDA of 9.18 which I consider cheap for a non cyclical business. Also P/E is 21, is much lesser than other listed hospitals.

Dividend payout is very low and I don’t think its a major issue. It’s true that its a regional player, but I am not worried about that as long as there is steady cash flows. Going forward, I am interested/ concerned to know how the company is going to utilize the cash its generating.

The interest payment is still around 30% of the Net Profits. This is after considering the fact that KMCH regularly Capitalises Interest (Not an issue per se — it’s an acceptable Accounting Principle).

Most of the Capex is behind us, I’d assume. So the next focus should be Debt Reduction. The management has also promised the same in the last AGM. Now we wait for the proof of execution.

I guess all hospitals are probably busy but recently I had to go there and they were packed with no room for patient’s attendants even, if they are admitted to an ICU. They are one of the expensive options in Coimbatore so I guess they have a good team of doctors and good facilities to be a better option for the patients here in spite of their higher rates.

any observations on the college?

how is that shaping?

as of my knowledge seats are full as a student of medicine i can provide a few insights

the seats get filled depending on your reputation and if your hospital has good patient inflows and it is not fully depended on other near by collages as students from all over the state and india get admitted in the collage

financially some one can explain what is going on in here because i have less idea on that

the main threats are here management getting black money and government control over the pricing of medical collage seats

i have visited the hospital several times and it has one of the finest reputations and the best doctors but will it translate into profits and stock returns we have to wait and see

very valid point on black money but recently all medicall college administers are very smart they take all charges in cheque, trackking this space closely , invested and biased no transaction in last 30 days

valid point it is difficult to cheat neet system for examination

The Board of Directors recommended a final dividend of INR 5 per Equity share and a special dividend of INR 5 per Equity Share (of face value of INR 10/ each) for the year 2022-23, subject to the approval of the shareholders in Annual General Meeting.

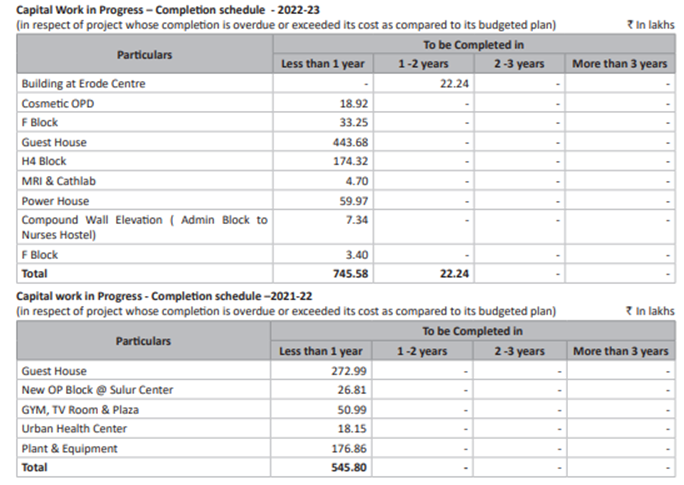

Good set of results except for borrowings not going down much. As against Sept balance sheet debt has gone down by 23 crores. Its good to see cash conversion cycle becoming negative again in the current financial year. The company is currently having a CWIP of 23 crores. Will love to know more about the capex. Will have to most probably wait till AGM to know about it. We could see registration for next batch of medical college in June quarter. Overall, results were mostly on expected lines.

-

Remuneration increased for Mr. Arun by 210% because that year he was given 1% commission for the first time, so that’s okay for me.

-

Yes, related party transaction is issue as it’s majorly supply of hospital consumables, the company should buy those materials directly to enhance minority incestors’ confidence.

I have been following Kovai and so far I have really liked the business. Some of the things I like about Kovai are the negative working Capital, cheap valuation for a hospital and the stable margins. Debt has been the major concern so far. The shares of the hospital are not very liquid. Its very difficult to buy even a small amount of shares. Debt is no more an issue as the medical college is functioning well and all the seats are filled up every year. Free cash flow can easily service the debt. Debt is also reasonably priced.( around 7.4% as per AR 22, must be at MCLR). There was some interest capitalisation but as per AR 22 the amount of interest capitalised in FY 21 -22 is 60.84 lakhs against 5004.15 lakhs in the previous year. So capitalisation of interests would have significantly decreased. Company doesn’t have much institutional followers. It is good to see promoters buying ( though not much). But my concern is with the cash flow. It will be great if anyone has any idea. As per the cash flow statement they have spent 127 crores in the last FY on purchase of fixed assets.

Does anyone has any idea on this? Is this maintenance capex? Or should we wait till AR to get clarity on this. There is a CWIP of 23 crores in the balance sheet.

I would really like to know more about its cash flow.

Discl: Invested.

Mostly, they have to buy ~40-50 crore of medical equipments every year, to keep up with the latest technology.

I was really happy about the growth in revenue and profit in the last few quarters but was concerned about the cash flow and the very slow reduction in debt. So I was going through the AR to understand the cash out flow better.

.

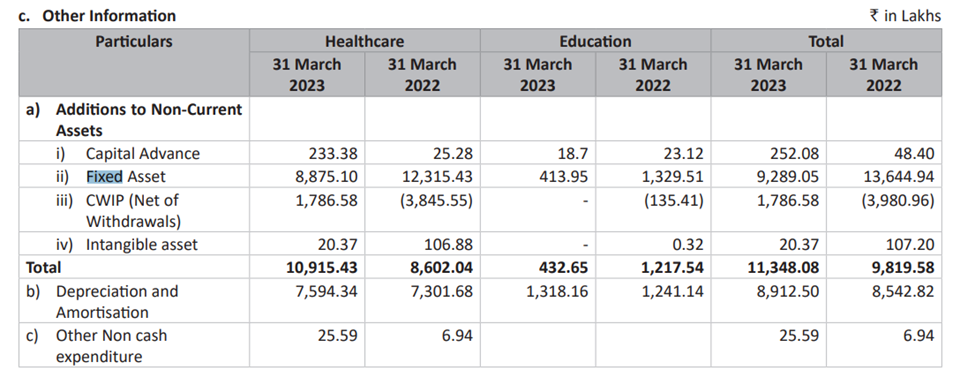

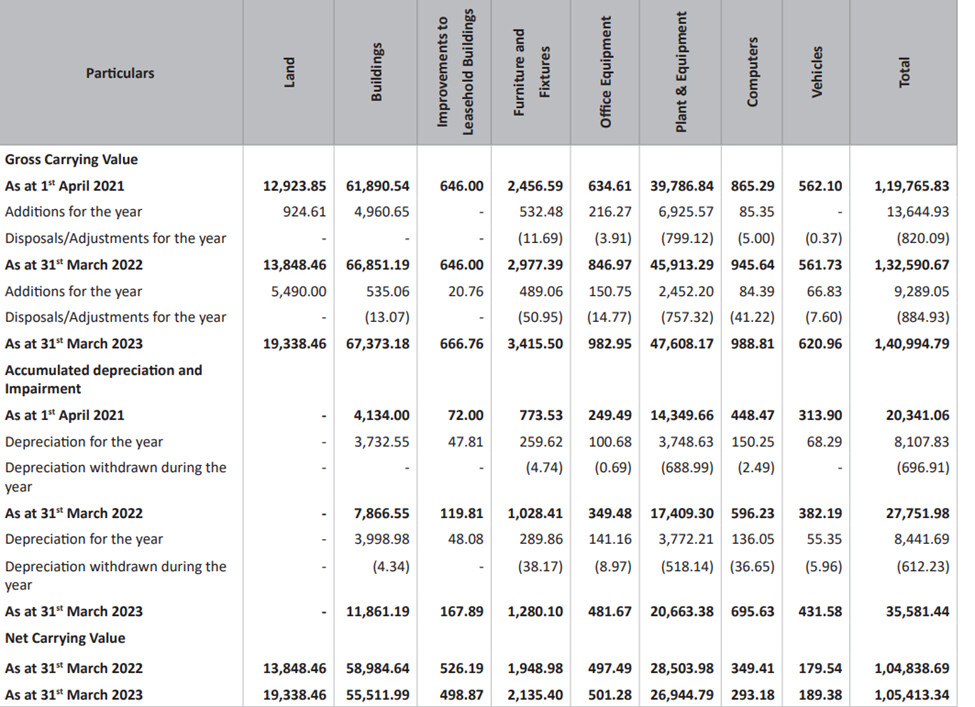

There is significant addition to land, plant and equipment.

54.90 crores were spent on land and 24.52 crores on plant and equipment. Out of which 19.57 crores were spent on purchase of medical equipment alone. Land was purchased in an auction.

Interest capitalized is NIL this year.

Going forward, I think the investment in medical equipment will be high as the chairman has indicated in his speech about having cath labs and MRI scanners at its various satellite centers. Investment in equipment and technology absorption is a good thing and can be revenue accretive. It will be good to know how they intend to use the land. I am not going into CWIP as it is already mentioned in the previous post( mostly buildings).

KMCH has always been into importing the latest medical tech. In fact, that’s one of their major selling points / differentiators. People living in the Coimbatore and surrounding regions will attest to that. It’s even been referenced in past ARs and even in the Chairman’s interview (It should be found in this thread somewhere, posted by me).

My concern still lies with the laggard pace at which Debt is being paid off. It wouldn’t be so bad if we are somehow able to estimate the exact cost of debt. That’s a bit difficult, since KMCH capitalizes their interest. If we get some hint of it from the management, it will help us understand if it’s good leverage or bad leverage. Hopefully it’s good.