Generic disclosure. But gives a good idea about the major Promoters of KMCH.

1 Like

Sir, How is the result of of Hospital for the year 21-22

There were lots of concerns raised on the foray by the co into the education segment. I feel this qtr shows that it will be profitable and the real nos will show as they complete another term and full strength of students are there.

22 Likes

The medical college foray is a double edged sword—-

Certainly it will provide another revenue stream and perhaps low cost man power, but many paying patients will find it difficult to accept being open to student examination.

How it’s handled can affect the patient perception of hospital.

At least based on my experience, it’s difficult to ride two horses together - Preferred destination for paying patients and medical college.

Moreover, national medical commission enforced reduction in fees for 50% seats will be applicable from this admission. We need to confirm whether there has been a compensatory rise in fees for another 50% seats or not - at least in Gujarat no increase has been allowed for next two years to compensate for loss in revenue.

Regards

2 Likes

agree with you sir , but in my opinion fees reduction last decide state affairs, correct me if i wrong , closely tracking this space.

disc invested no transaction since 6 month

not sebi register

Find relevant news article NMC directs private deemed universities to reduce fee for 50% medical seats | Education News,The Indian Express

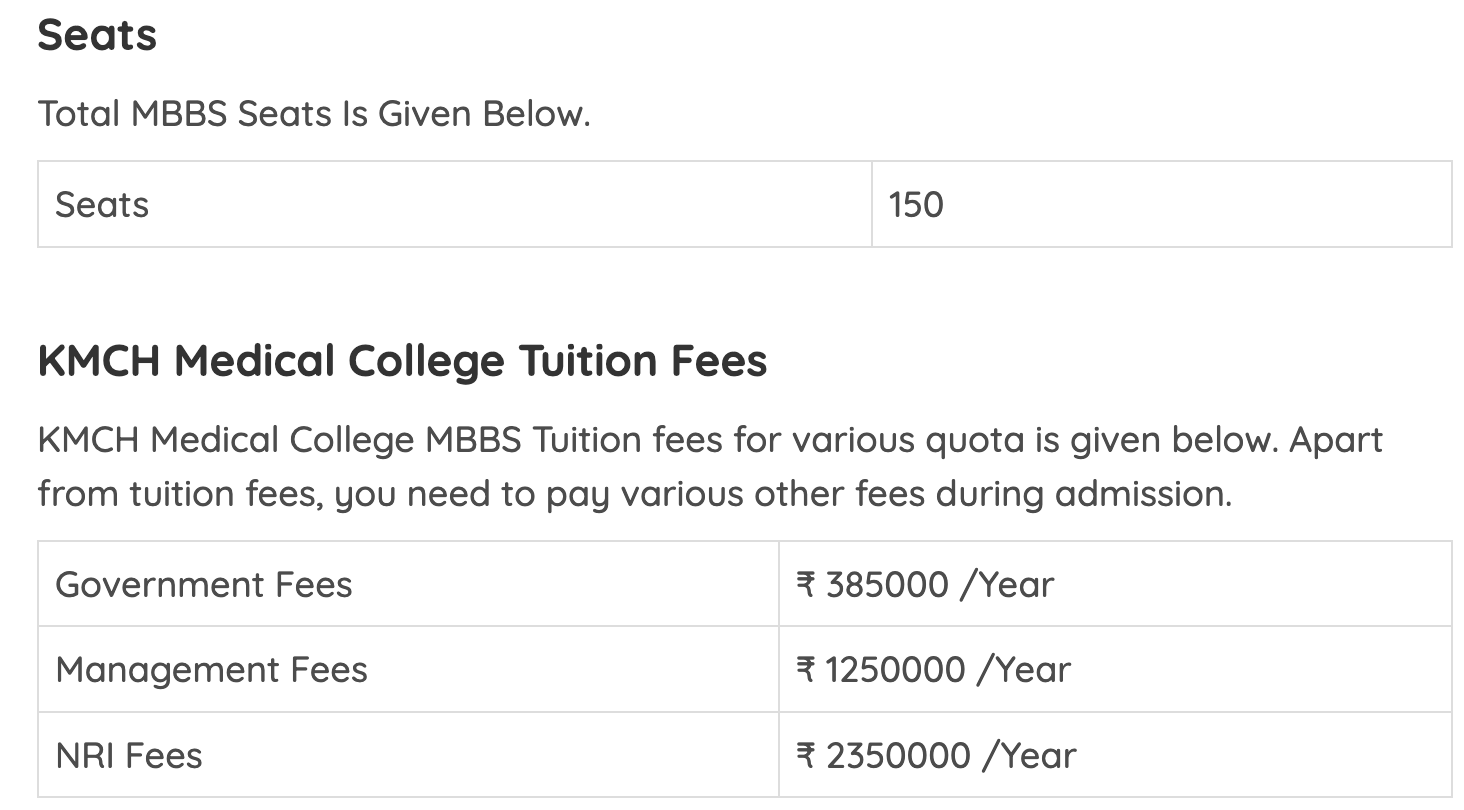

For 21-22 batch below was the fee structure and total fee collection was 12,79,60,000/- (12.79 Cr) from 150 admissions.

- I am not sure how fee is charged for the 4.5- 5.5th year students when they are in residency program?

- Does residency program enhance patient serving capacity of the Medical Collage?

- Looks like revenue from AHS courses is not significant.

- As per new norms, will adding 80 more beds allow them to seek permission to add another 50 seats?

The requirement for the number of beds in a medical college hospital has been reduced from 530 to 430 for a 100-seat college, and from 930 to 830 for a 200-seat college, according to the new regulations notified.

7 Likes

Its always good to read the annual report of Kovai. They have had a really good track record of consistent growth and scale up from a single location.

Other highlight is the several firsts that they keep doing in the medical field. It seems the management is quite focused on bringing new machines/technologies and doctor talent to offer the best of healthcare to the public.

Given the superior profitability that this co generates, I feel the stock has never got the due valuations.

Looking forward to attend the AGM to get more insights.

Ayush

Disc: same as before. Invested in family and client acs.

26 Likes

Thanks @ayushmit in advance for attending AGM, looking forward for your notes.

Have certain queries, pl see if possible to take them up:

1. Medical Tourism:

Whatever little Foreign exchange earning company has is from Fee for Education (ref. page 18 of 2021-22’s AR), this means Zero earning from Medical tourism, while same has been identified as Opportunity in SWOT analysis.

My queries:

i. What initiatives company is taking to initiate it’s entry in medical tourism ?

ii. One o the key consideration foreign patients have is international accreditation of the hospital i.e. by JCI. KMCH is only NABH accredited, what’s their plan to get JCI accreditation ?

2. Number of Beds

Page 1 of AR 22 informs opening of hospital within college adding 750 beds, Page 37 informs that KMCH is now 2250 beds hospital, while Page 40 informs bed capacity of 1854 (against 1629 last year).

Query :

i. What is the current bed capacity of KMCH & what is foreseen to be by end of FY23 ?

ii. If possible to get : What’s the breakup among Multi-specialty, ICU & Emergency

3. Succession:

Please observe : how Dr. Arun N Palaniswami is taking over the organisation.

Thanks

Charanjeev

Disc: Invested

3 Likes

Totally agree @ayushmit sir, when you sir posted AR20 annual reoprt with all highlight and mark, it almost ready to eat type dish but someone had to read it also , very easily connected to this story , may be some circle of comepetence , thanks for guidance , happy teachers days ,

disc old investement, top 5 holdings.

4 Likes

Please share the AGM notes. Didn’t able to attend the meeting this time. Thank you.

1 Like

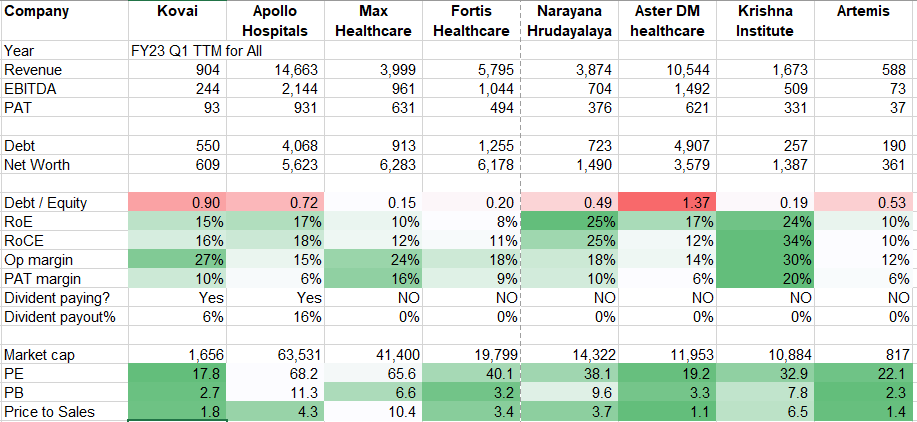

Valuations may not improve unless the company expands geographically IMO.

Kovai is at 2x of revenue . recently a pvt hospital was traded at 200 crore valuation and 4x sales valuation. Even on /bed Kovai is cheaper . The other one was Artemis which has now 1.5 sales. I do see rerating opportunity on basis of rather than expanding geographically vs not doing mindless expansion. the biggest positive is the medical collage and i believe completing 1st batch there would be one good trigger.

hospital stocks are in trend. almost all pharma fund has exposure of 15-20% in hospital stocks . Kovai is one of bargain available at present.

7 Likes

The problem with KMCH is that they have ‘potential’ to expand, but we are yet to see clear evidence that they can scale the hub-and-spoke model to a completely new city. From Apollo’s or NH’s history, we know that operating a Brownfield Hospital produces decent Cashflows and Returns, but wealth is built in expanding and operating Greenfield Projects sucessfully (Apollo’s especially a good comparison to make).

Personally, I am happy that they chose to build a Medical College instead of a Hospital in Chennai. And I’m not saying KMCH can’t build a sucessful Greenfield Hospital. I’m just saying that they haven’t shown any evidence of the same. I’ll be happy to see them setup smaller operations in other cities like Trichy or Madurai too, just to experience expanding on a new market.

And maybe that is going to happen in the future too. I just feel like that’s one of the things they’re yet to prove as of now.

17 Likes

The CFO has resigned. Is it something negative?

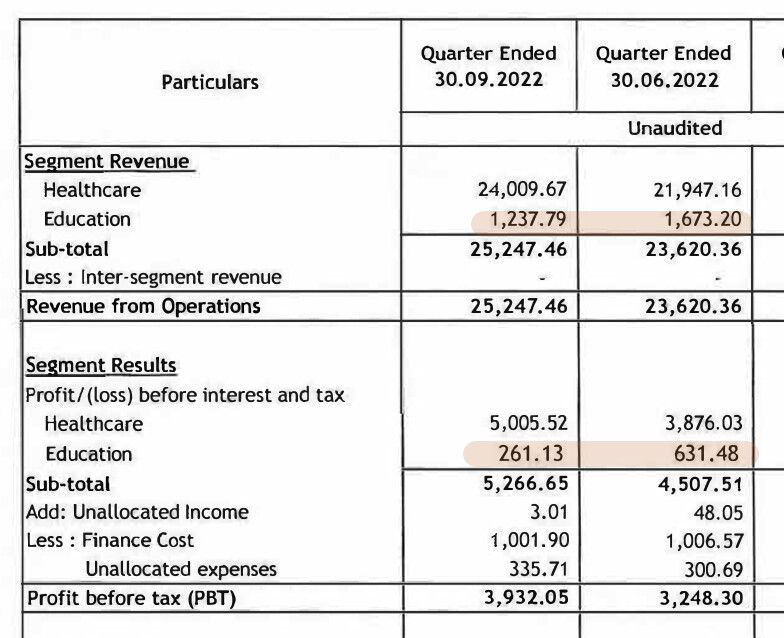

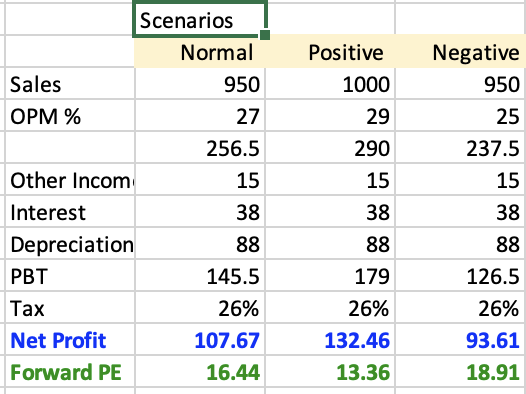

4th batch took admission this year. This years’ education profit may touch 14-15 Cr compared to 7Cr loss in previous year. Next year (2024) it should reach to ~20Cr profit with 5th year fee.

2024 estimation scenarios, (I have not gone at extreme on either side)

Question would be how much of this year’ sale is because of pent-up demand or elevated concerns after Wuhan virus or enhanced operations, how much of it would sustain in next year?

Disclosure: Invested

5 Likes

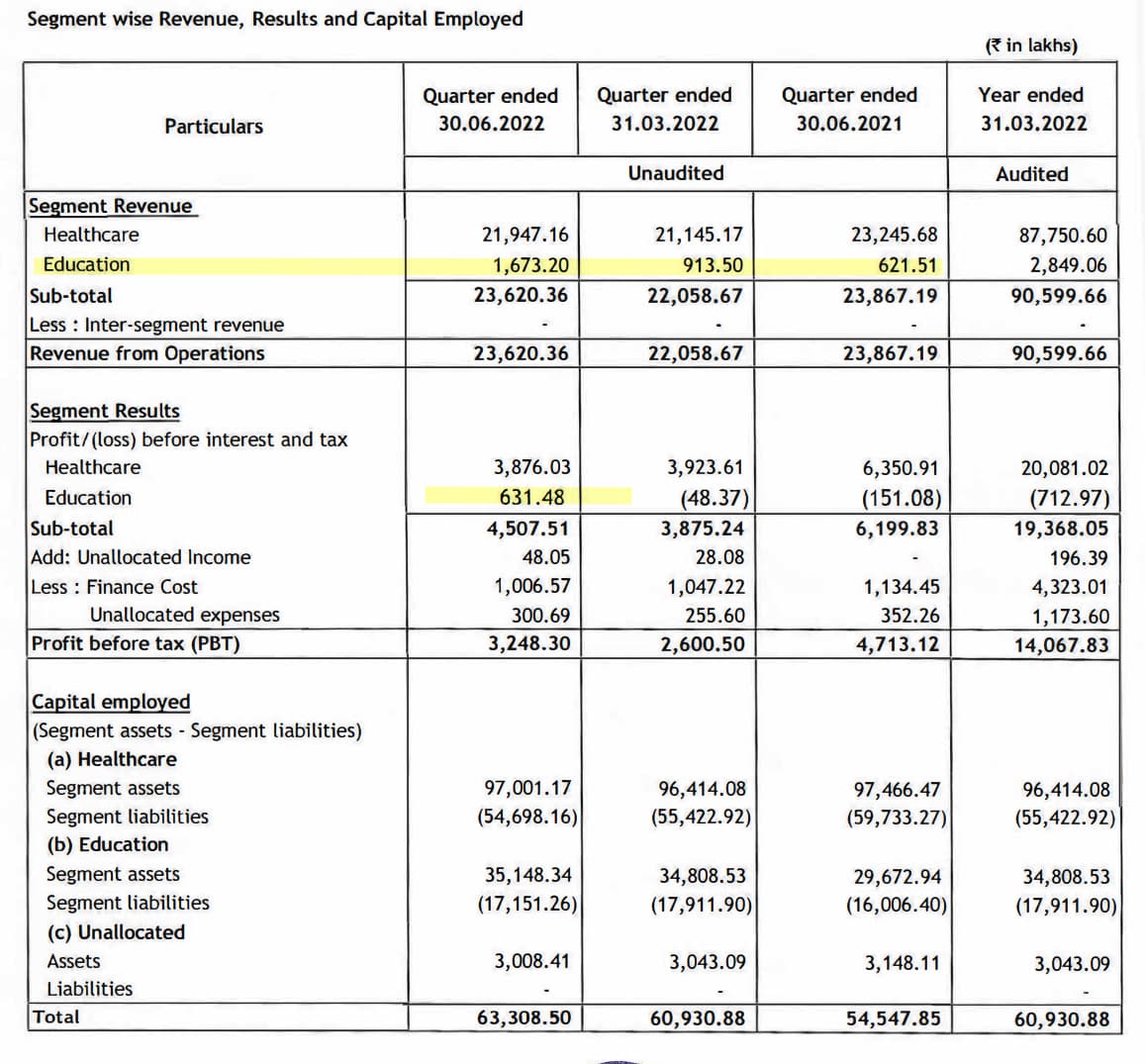

Q3 Results are out:

Total Revenue: 264 crores ( vs Q2 Revenue - 252 crores and Q3 FY21 - 229 crores)

- Hospital Revenue: 246 crores

- Education Revenue: 18 crores

EBIDTA Margins at 27% (vs Q2 - 27%, Q3 FY 21- 28%)

PAT - 31 crores (vs Q2 PAT - 30 crores and Q3 FY 21 PAT - 26 crores)

3 Likes

Good results.

As expected Education segment is adding more and more to topline and bottomline.

3 Likes

The hospital seems to have completed all its capex for the new medical college and the new 750 bed hospital was opened in Oct’21. From now on it will be just minimal capex. As of sept’22 the CWIP is 9 crores. The medical college has completed the 4th-year intake and has started showing profits. The hospital is having 230 crores cash equivalents in its balance sheet as of Sept’22. The hospital may end up with around 320 crores in the current FY and net debt free by the end of the next FY at the current run rate. There will be one more additional batch in the next FY. It needs to be seen whether the management decides to pay down the debt considering the high-interest rates. I believe the benefits of large capex taken may be visible from next year with medical college reaching full utilization. We may see many metrics improving with free cash flow improving considerably. Also it will be interesting to see how they utilize the cash on the balance sheet

10 Likes