Not sure weather your queries were answered through mail @Gaurav_Kothari. I attended the AGM and would highlight what I understood. Other participants who attended, request you to give your insights for benefit of all.

Comments from Management:

- Crossed milestone of “Obtaining Veera Carbon Credit”. We are 1st Listed Bio-Diesel company to have this acknowledgement.

- Increased Capacity from 500KLPD to 1500KLPD for Biodiesel. Increased Capaicty from 17KLPD to 210KLPD in Glycerine.

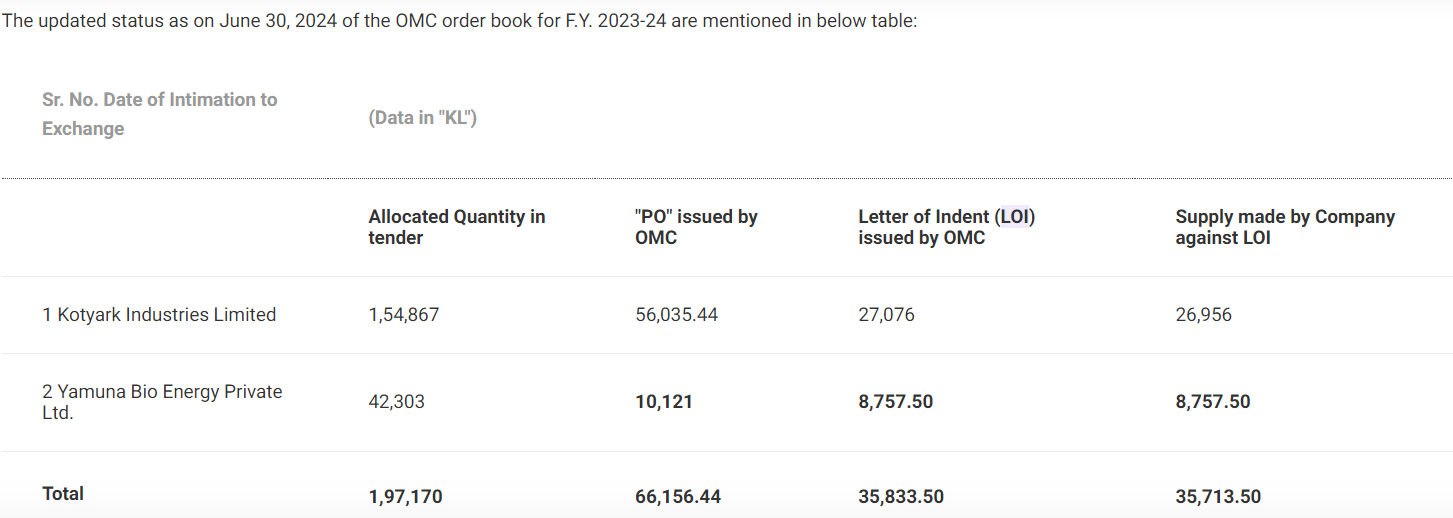

- In FY24, we got LOI for 1.97L but PO of only 35.8K were issued. Historically, it has happened. If PO is not issued within tender timelines than whole LOI is invalid.

- Applied for subsidy with RJ govt, our manufacturing unit is eligible. Once approved, will increase our financial position.

Answers of Q&A:

- All RM we use are sourced locally, RM is non-edible oil. There is ample availability of RM in market.

- There is pricing formula with OMCs: Past 3 months average RM Price + Rs. 15 Processing Charges + Profit. So we are protected with RM price fluctuations.

- We expanded from 500KLPD to 1500KLPD despite being underutilized. Confident of utilizing same… At full utilization level - turnover potential at current price is 5000cr…

- Biodiesel & Ethanol both started in 2005. First big tender for Ethanol was received in 2015 and then it got slow. Ethanol as of today is stabalized. So, similar could happen with Biodiesel.

- No guidance on Revenue, H2 results will come shortly and I can say it has been good year so far. Compared to last year, this year EBIDA margins will be same.

Note: I have posted only short transcript and not done any analysis. Folks with better understanding of company, request you to give valuable insights. I feel, government’s initiative to fast-track the use of Biodiesel would be game changer for Kotyark with exponential growths.

Regards,

Mukul Jain

Disc: Invested

5 Likes

EBDITA will be same or EBIDTA margin?

Corrected. It is EBITDA Margins

1 Like

Thanks for sharing your notes.

Threefold increase in capacity when original capacity is not even 20% utilized. Seems very very bold (if not reckless) decision. I know that based on Govt commentary the requirement for Bio-diesel seems huge in future but with Govt policies there is always a danger of flip-flops, delays, tweaks which can adversely impact whole Business plan.

I am invested in BCL Industries, which is building a 75KLPD Bio-diesel plant along with paddy straw-based power plant, total capex for that is around Rs 140 cr (no land cost included). Assuming that just the bio-diesel plant costs around 90 cr and power plant Rs 50, then Kotyark would need around Rs. 1200 cr (assuming they already have the land) for the additional 1000 KLPD bio-diesel capacity. (Very rough figures)

I am not invested in Kotyark, just started analyzing it today so I may be missing some obvious points. I tried searching online but couldn’t find some info, can someone who is invested/researched, please help me by answering some questions:

- What was the total capex outlay? How did they fund such a huge capex? What was the mix of Equity and Debt?

- Any idea about the debt levels? How much additional debt was taken to fund the expansion and how much is the interest cost?

- This year many of their LOI lapsed, will it impact their ability to service their debt as the Cash flow will be very little compared to the Capex outlay?

Thanks.

3 Likes

H1 Results :- https://nsearchives.nseindia.com/corporate/KOTYARK_29102024163750_Reg30.pdf

![]() Revenue:arrow_up:36%: ₹197cr (H1’25) Vs ₹145cr (H2 ‘24)

Revenue:arrow_up:36%: ₹197cr (H1’25) Vs ₹145cr (H2 ‘24)

![]() PAT:arrow_up:56%: ₹17.8cr (H1’25) Vs ₹11.4cr (H2 ‘24)

PAT:arrow_up:56%: ₹17.8cr (H1’25) Vs ₹11.4cr (H2 ‘24)

![]() EPS has gone from 11.6 to 17.4 per share

EPS has gone from 11.6 to 17.4 per share

![]() Dividend of ₹7.5 per share announced

Dividend of ₹7.5 per share announced

![]() Looking to migrate to main board

Looking to migrate to main board

Govt. Pushing ethanol to blend with diesel instead of biodiesel!

Will it affect Biodiesel industry?

Indian Oil advocates integrating biodiesel processing within existing refineries to meet 5% biodiesel blending target

If OMCs make their own Processing plants of Biodiesel then who will procure Biodiesel from private players like kotyark?

Will it drawdown sales of kotyark?

1 Like

New SME IPO coming in for the biodiesel space - https://www.youtube.com/watch?v=k5pkjzAWxOA&pp=ygUScmFqcHV0YW5hIHNtZW1pdHJh - Very good insights provided by the management about the biodiesel space, the size of opportunity, tender open timings(entire years tenders open up in October), competitors…

AGM is also filled with a lot of information- Video Transcript of 08th AGM 27.09.2024.mp4 - Google Drive

Also, Order worth about 564 Cr to Kotyark for next year (for tenders opened in Oct) - https://nsearchives.nseindia.com/corporate/KOTYARK_20112024193449_Reg30_OMCTender.pdf

4 Likes

Thanks for that.

Rajputana biodiesel is listing at 14 PE and may have a lower base effect for a slightly better growth and optionality of getting into other related bueinesses like CBG.

Ultimately commodity businesses like these dont deserve higher Terminal PE, even when market expects kotyark to register 70-80% growth again in running fiscal year.?

Just sharing thoughts on valuation.

Disclosure : invested in kotyark.

3 Likes

Sir where do you get this 600cr number, Asper IEA- 5% biodiesel blending by 2030, approximately 4.5 billion liters of biodiesel capacity per year is required(Source-International Energy Agency). Currently, Iia’s biodiesel production capacity is about 1.3 billion liters per year.

I posted this comment amid hype around this stock last year. This is what has happened today.

Unfortunately for retail unscrupulous management never discloses such issues during bull market. Bear market is when retail investor is struck by twin blows of market correction and business headwinds getting exposed leading to further selling.

1 Like

Kotyark Industries is one of the best players in this segment . However, the main issue lies with the product’s QC. While Kotyark follows a strict QC procedure but other small players don’t have good QC control. As a result OMCs are facing many Qc related issues while blending Biodiesel with diesel which is hampering their image in the market . So as a result it has been stopped by the OMCS and they are selling pure diesel only as of now.

1 Like

They might be the best player but whether Kotyark is a good stock is questionable. Any small company (with no bargaining or pricing power) that operates in a very niche segment, doing business with mainly government customers who themselves operate in a heavily regulated industry, can’t be trusted to be a good investment barring bull market when everything runs.

1 Like

Finally a small good news compared to the earlier disappointment.

KOTYARK_16042025202328_LOI.pdf (462.9 KB)

What was the need to give preferential allotment of 10 lakh shares (2022 and 2024 when they had good cash flows?

I can see the company is decent but the management must be trustworthy and transparent to an extent atleast.

1 Like