6 Likes

1 Like

Naval Ravikant, Angel Investor and Philosopher also says on similar lines: Take accountability and attach your name with the idea.

1 Like

2 Likes

Quote from above article:

Chandna said that Kotak Mahindra Bank has now “pressed the accelerator” on unsecured products and is confident that credit cards as a product will continue to stay, although form factors may change due to technology developments and changes in consumer behaviour.

.

“The idea of individuals wanting a credit line will stay. They may or may not use the plastic. That does not matter. The application has already gone digital. The card business is here to stay and is something we are invested in,” he said.

.

Going forward, Kotak Mahindra Bank also plans to invest more in Buy Now Pay Later (BNPL) given the potential in that area.

Interesting!!

3 Likes

Lots of acquisitions and minority stake purchases in various fintechs in the news from KMB over the last several months. Would be interesting to note how this “conservative” bank is planning to disrupt in the face of change in banking industry.

Invested. One of my core holdings.

1 Like

Mint: Kotak Prime acquires passenger vehicle financing portfolio of Ford Credit.

1 Like

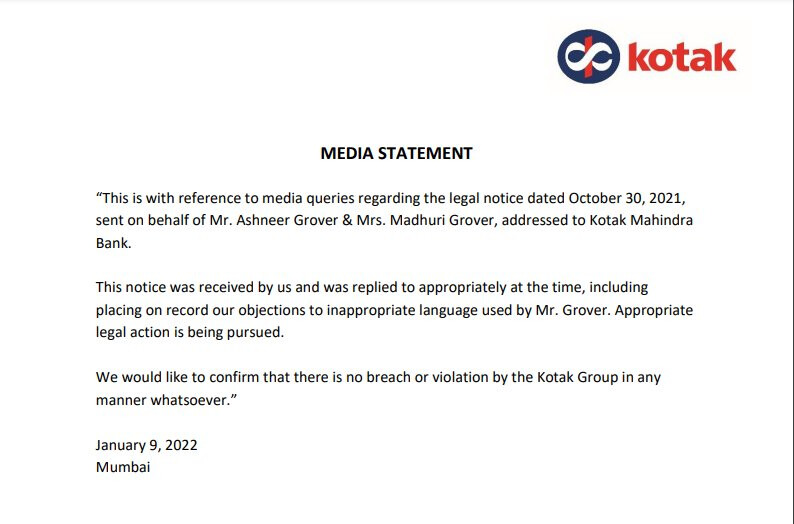

Maybe to defend its Image?

They must have wanted to establish that they didn’t do anything wrong with respect to IPO financing or faulty promises to HNI clients about allocation.

1 Like

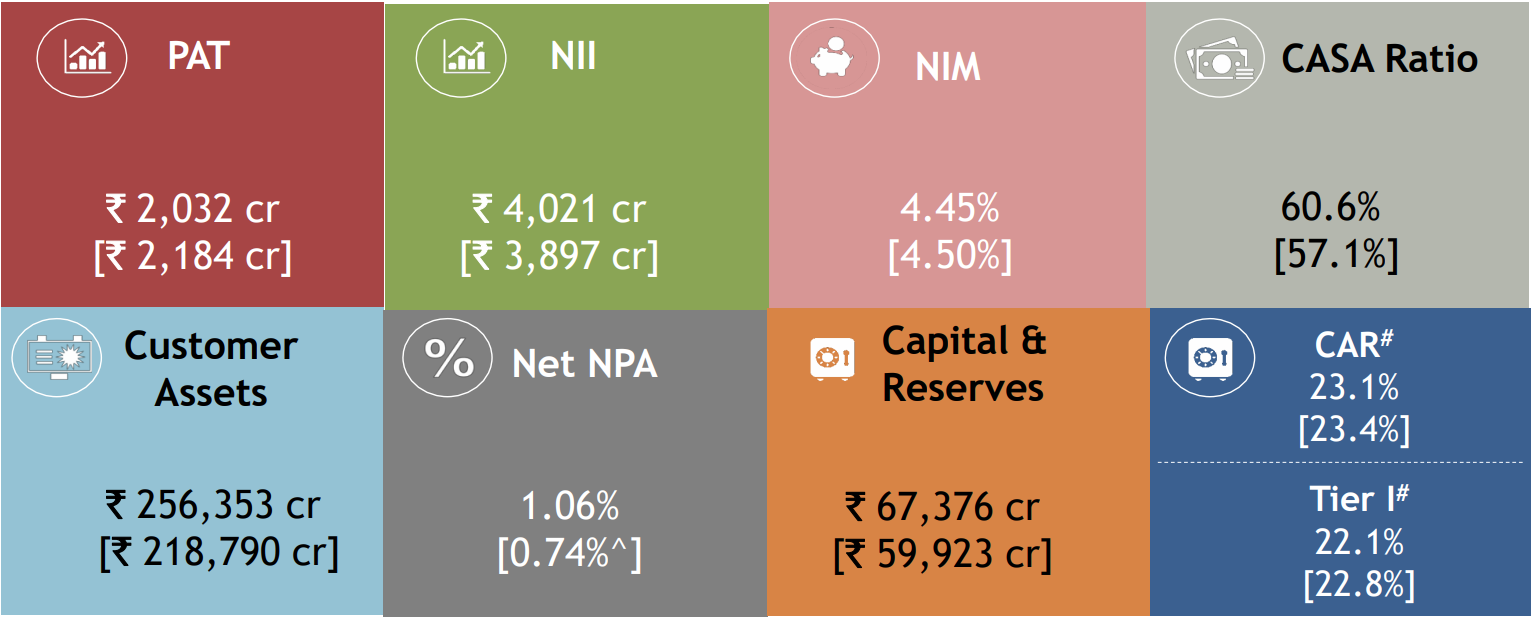

Q3FY22 Results

Consol Q3FY22 highlights:

Consol PAT at Rs. 3,403 cr up 31% YoY

Subs & associates:37% of Consol PAT

Major Subs PAT:Kotak Securities–Rs. 270 cr, Kotak Prime–Rs. 254 cr, Kotak Life Insurance–Rs. 247 cr, Kotak AMC & TC–Rs. 149 cr

Assets under mgt/advisory ~Rs. 386,465 cr up 23% YoY

Bank Q3FY22 highlights:

PAT at Rs. 2,131 cr up 15% YoY

NII at Rs. 4,334 cr up 12% YoY

NIM at 4.62%

Net Total Income at Rs. 5,698 cr up 10% YoY

CAR as per Basel III, incl unaudited profits, as at Dec 31, 2021 was 23.3% & Tier I ratio was 22.4 %

Deposits:

CASA ratio as at Dec 31, 2021 at 59.9%

Avg CA for 9MFY22 Rs. 49,417 cr

Avg SA for 9MFY22 Rs. 119,645 cr

TD Sweep for 9MFY22 Rs. 23,429 cr

Advances & Asset Quality:

Customer Assets (Advances + Credit Substitutes) Rs. 274,569 cr up 20% YoY

Advances at Rs. 252,935 cr up 18% YoY

NNPA at 0.79%

Credit cost for Q3FY22 on advances was 35 bps (annualized) (excl reversal of Covid provision); (63 bps for Q2FY22)

Investor Presentation

Financials

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0c26a2d2-cd69-4010-893e-c8fe67c4f85f.pdf

8 Likes

4Quarter2022

Investor Presentation

Financials & Earnings Update

https://www.bseindia.com/xml-data/corpfiling/AttachLive/7b80c0ef-ced9-47c2-b2ca-d3350be19745.pdf

4 Likes

8385f70e-32bc-4e29-83e3-df47a10b6f4a.pdf (2.0 MB)

Kotak 118 investor presentation

Interesting data of digital initiative

For good measure the official bank spokesperson was cited stating, Jay’s progress “will continue to be based on merit.”

.

The media and the attendees were oblivious to the elephant in the room, namely, how was a 32-year old with an MBA degree from Harvard University and a mere three years of work experience was selected as a business co-head in a bank valued at $48.7 billion.

.

The critical issue in Jay Kotak’s appointment as co-head of the 811 initiative is what criteria were selected to determine Jay’s suitability for the post. One understands that new digital ventures are set-up in banks as incubators and are staffed by youngsters but there is no explanation to KMB stakeholders why Jay was the most suitable candidate amongst many youngsters for the post, apart from having Kotak as his last name.

In the old private sector banks – those established prior to 1991 – there is one instance of a bank selecting a son with a time lag to replace the father, as was the case with City Union Bank (market valuation of US$ 1.3 billion) and its current CEO, N. Kamakodi.

1 Like

KMB is one of my core holdings. In the past UK have indicated that his successors would be a professional rather than from family.

However these new developments are concerning and does not augur well from the governance point of view.

Though the entire thing is a conjecture as of now. It may very well go the NRN way of Infosys.

But as an investor deeply deeply concerned.

2 Likes

The calculations of the bank showed that it took 4.5 years to break even after the acquisition of a customer at the end of march 2022.

Just read this report by Ambit Capital - https://www.bqprime.com/business/kotak-mahindra-banks-industry-best-casa-ratio-tells-half-truth-says-ambit-capital

Can someone shed more light on their “Bull Case Scenario” for Kotak Mahindra bank? Particularly interested in Loan Growth and NIMs going forward.

Interested and evaluating a position.

3 Likes

Monetary Penalties Levied by SEBI on KMAMC (Kotak Mahindra Asset Management Company Limited) and KMTC (Kotak Mahindra Trustee Company)

Name, Monetary Penalty, SEBI Order Dated.

1 KMAMC Rs 5 mn August 27, 2021

2 Kotak Mahindra Trustee Company Ltd. Rs 4 mn June 30, 2022

3 Nilesh Shah, managing director, KMAMC Rs 3 mn June 30, 2022

4 Lakshmi Iyer, chief investment officer, KMAMC Rs 2.5 mn June 30, 2022

5 Deepak Agrawal, fund manager, vice-president KMAMC Rs 2 mn June 30, 2022

6 Jolly Bhatt, compliance officer, KMAMC Rs 1 mn June 30, 2022

7 Abhishek Bisen, fund manager, KMAMC Rs 1.5 mn June 30, 2022

8 Gaurang Shah, director, KMAMC Rs 2 mn June 30, 2022

Source: SEBI

1 Like