My notes from the Concall(please excuse any mistakes on my part):

Government package very meaningful,will help a lot but need to wait for the details.

Covid is here to stay for next 12-15 months.

Lockdown has an exponential cost on the economy,getting out of lockdown very tricky.

Kotak Bank has a 1.Strong balance sheet. & 2.Trusted deposit franchise.

Lending pegged on:

1.Sector

2.Avoiding companies with high fixed operating costs.

3.Avoiding businesses with High leverage.

Even after the rate drop,still at SB rates that are higher than peers.

Despite drop in rates have seen improvement in saving account numbers in April.

Adding 14000 customer accounts per day in May through digital channel.

Opened 44 lac accounts in whole of last fiscal year.

Cost of deposits for last FY:5.2%

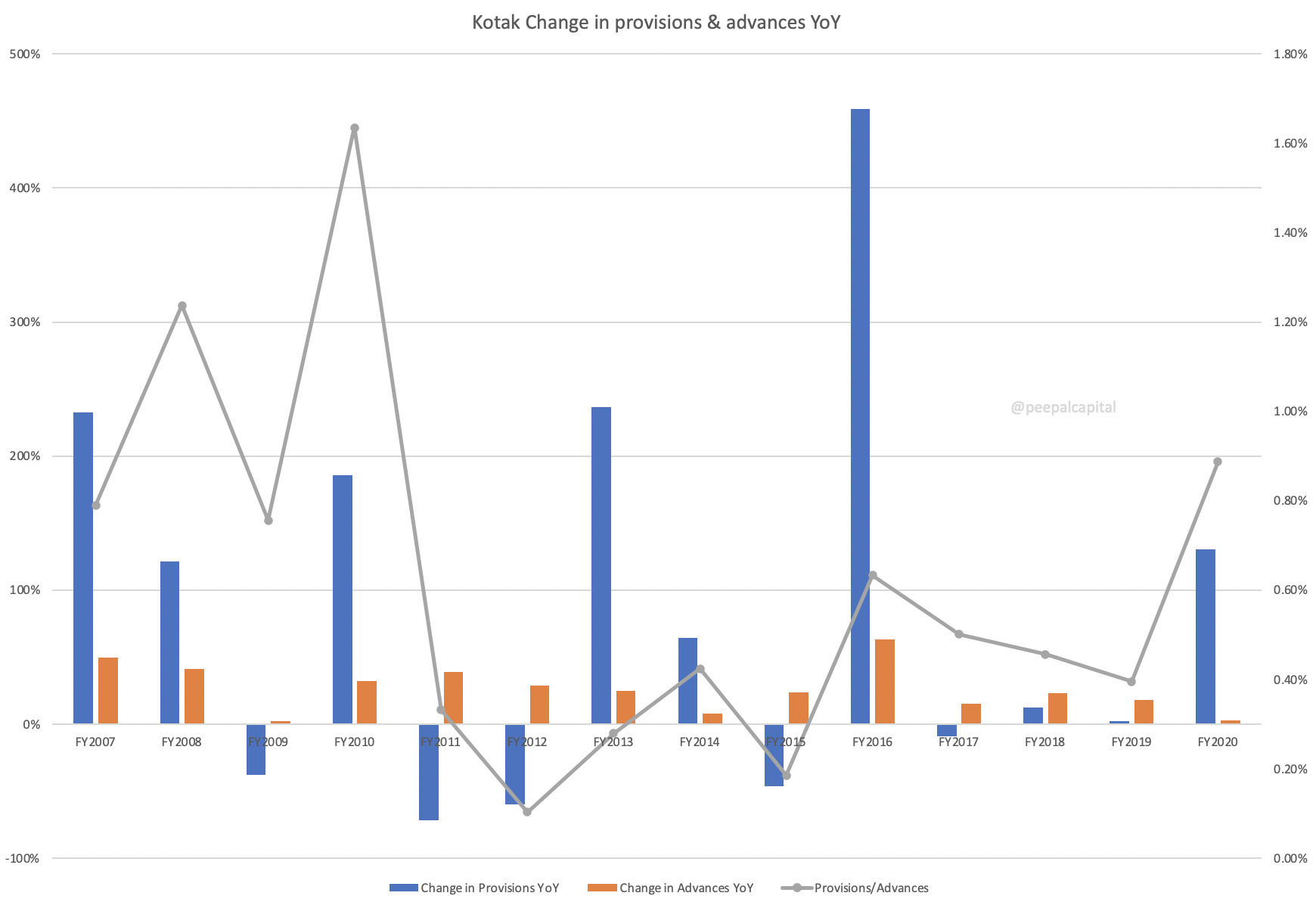

SMA2 outstanding is 274 Cr.

SMA2 includes accounts that are only above 5 Crores.

Have taken 650 Cr. Covid provisions.

Moratorium is 26% by value as of April 30,numbers increasing as the lockdown extends and more customers wanting extension.

Credit utilization has come down but customers want to conserve cash in uncertain environment.

Significant changing the credit underwriting metrics in the post Covid world.

Spending on digital & technology will go up,brands will become more important.

Non credit risk business(Advisory,Wealth management & Asset management,Securities) will see higher focus.

Will lend only if the risk adjusted return makes sense,not after topline growth.

Fund raise via selling of up to 6.5 Cr shares soon to reduce promoter stake.

Worried about unsecured lending even to salaried customers.

Consolidation can happen through mortality or through combination.

At a policy level do not have a clear exit policy for entities in financial sector.