@atul1082: Thanks for your POV.

The guy has built the institute from scratch and aspires to catapult it in the top league. UK says below in one of his AR letter’s which seems a reasonable point:

@atul1082: Thanks for your POV.

The guy has built the institute from scratch and aspires to catapult it in the top league. UK says below in one of his AR letter’s which seems a reasonable point:

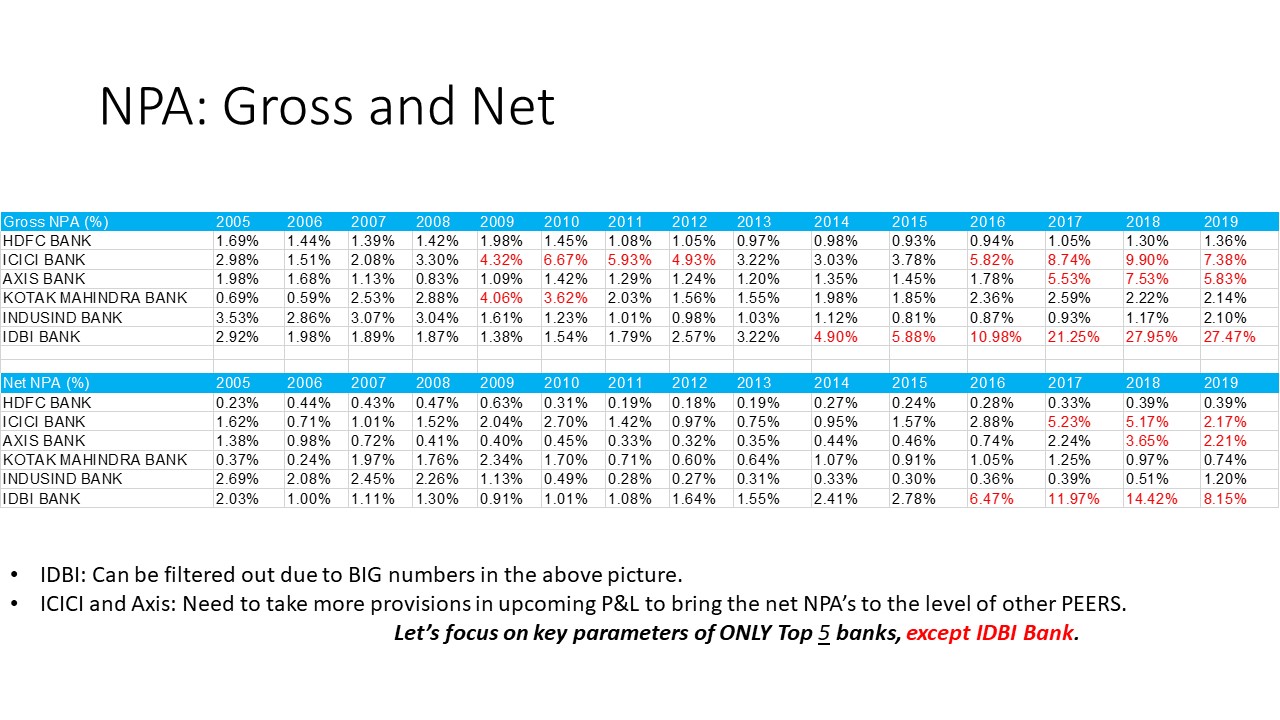

NPA details for top 4 private banks is as below. Besides NPA, I also collected data for write-off and Debt Restructuring.

Source is RBI website- DBIE-RBI : DATABASE OF INDIAN ECONOMY.

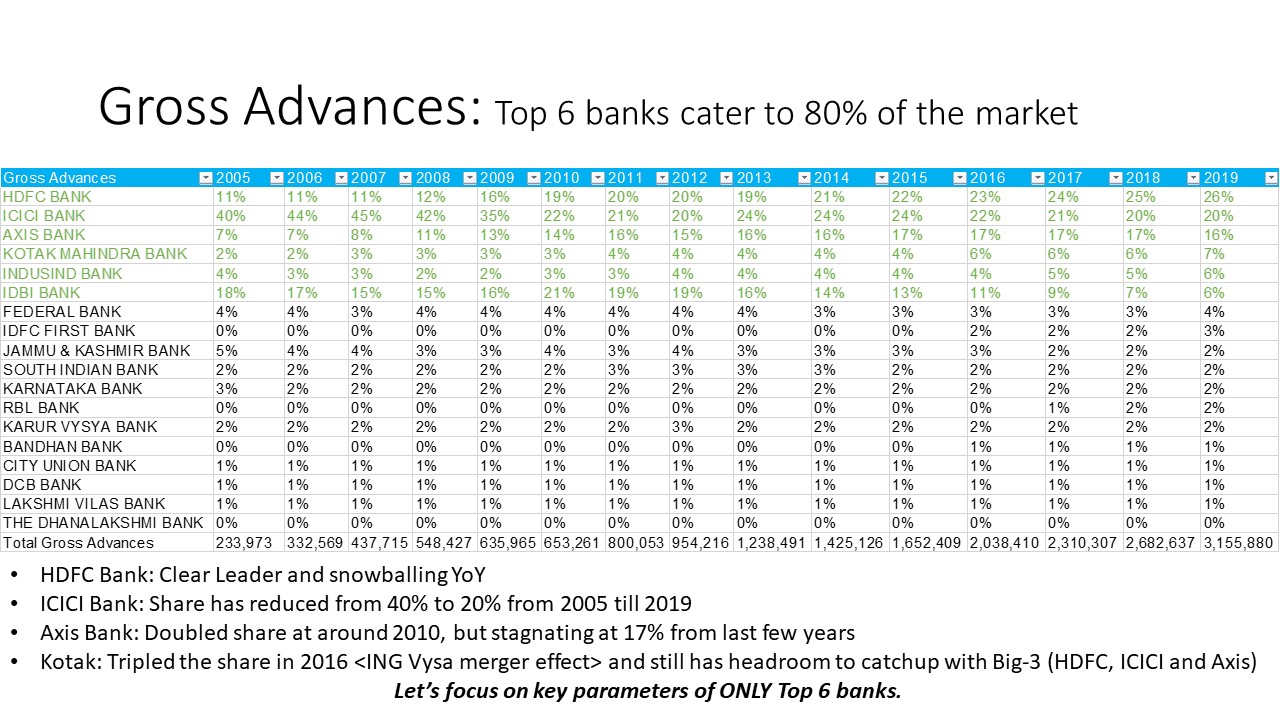

I did more data crunching and sharing with all for comments/feedback. Started with 18 Private Sector banks and filtered to focus on 6 using the below logic-

Among the 6, IDBI was filtered out due to huge NPA % as shown below -

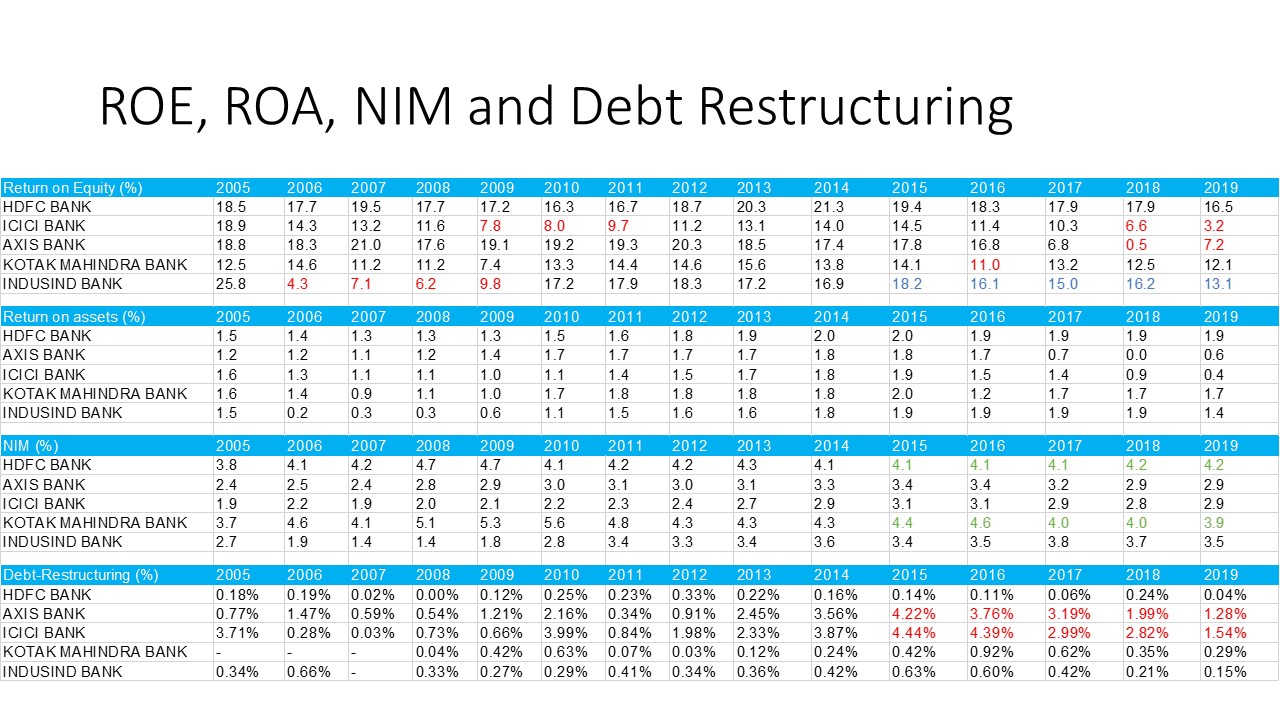

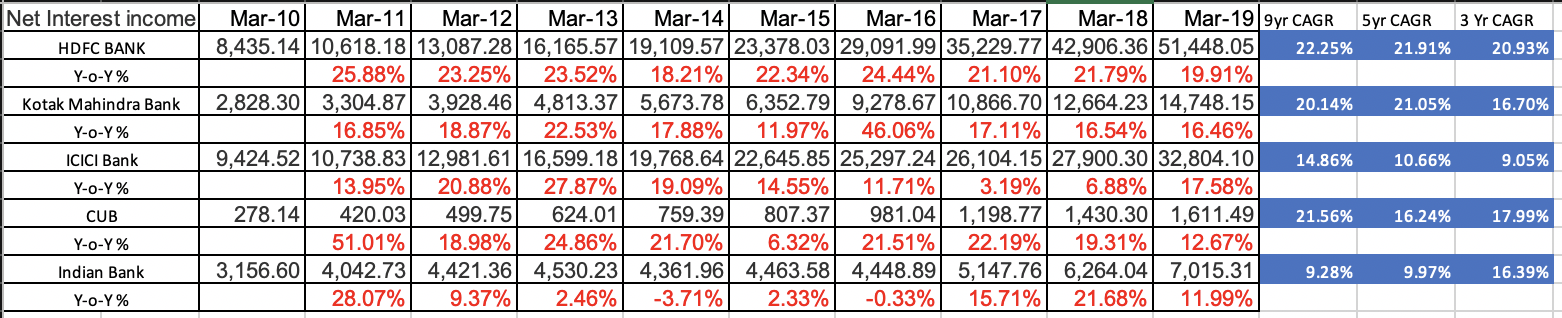

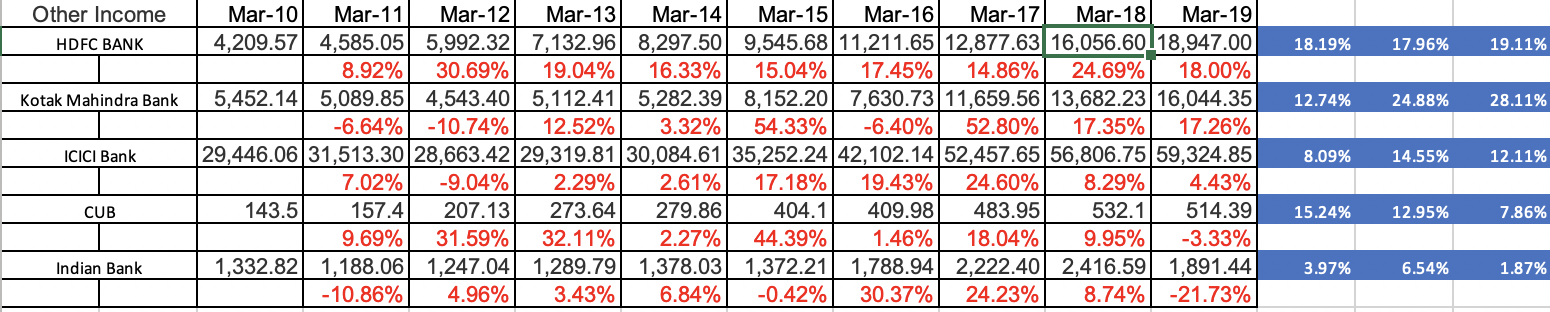

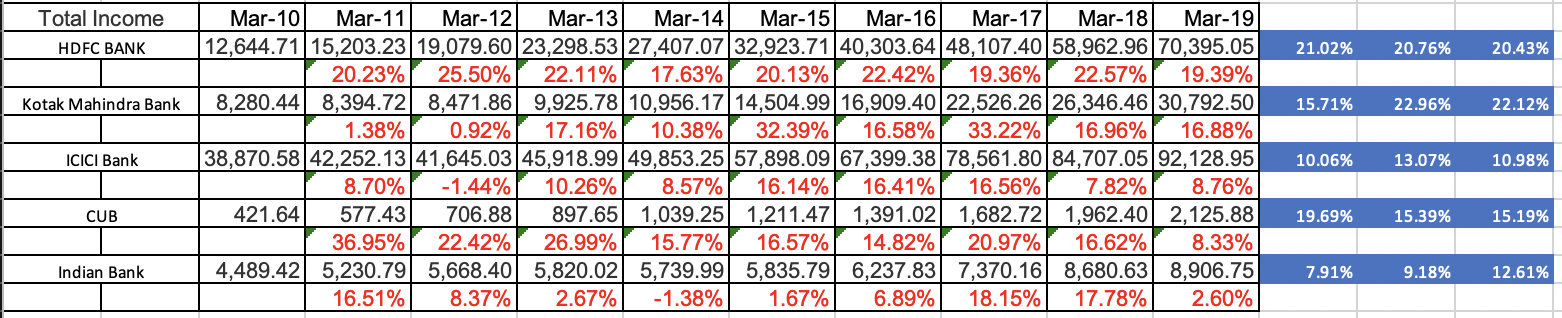

In the last 5 banks, a comparative look-refer below picture- at ROE, ROA, NIM and Debt Restructuring makes one thing clear that AXIS and ICICI can be studied further if one has an approach to investing with the basic tenet as ‘Reversal to Mean’ while other 3 - HDFC, Kotak, and Indusind- can be studied for consistency and long term play.

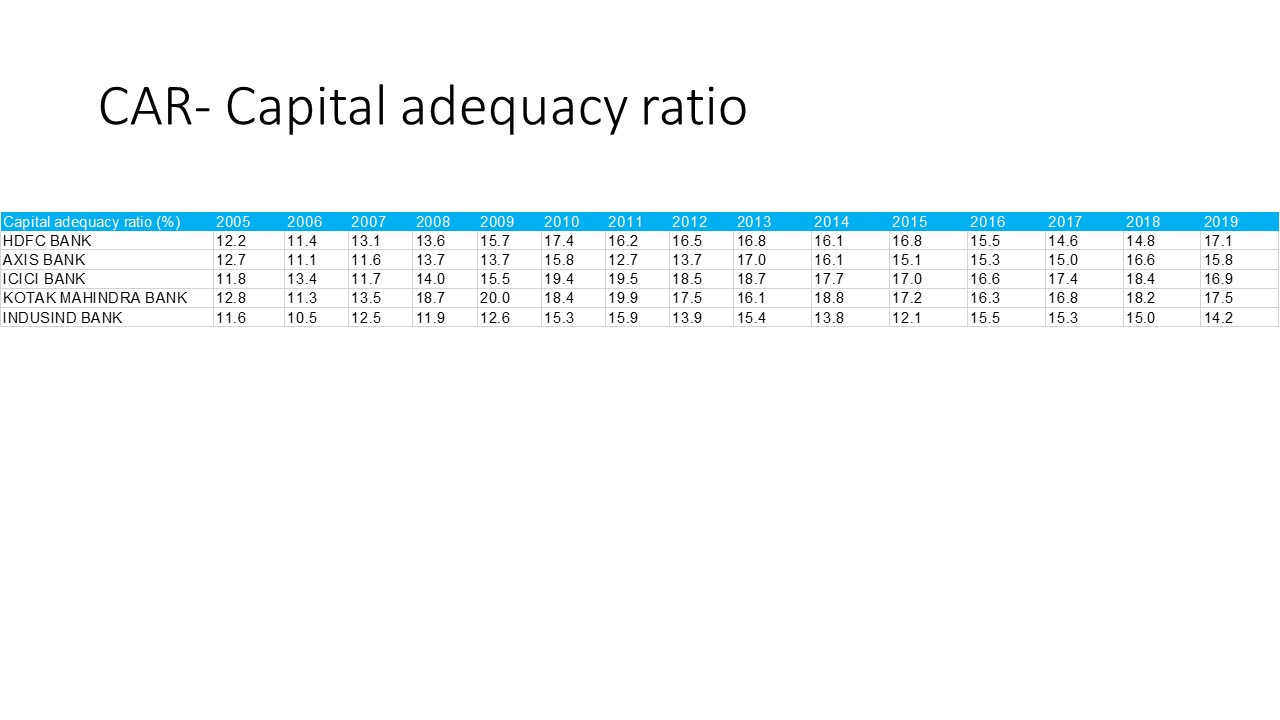

Finally, the CAR of all the banks looks as shown below-

And the deep dive still continues…

Few more thoughts-

KMB’s earnings are suppressed.

KMB’s ROE is suppressed.

Other Key Aspects:

Is that the reason market has always valued KMB so highly?

Disc: Not invested. However, impressed. Still working to find the bear case. Do help ![]()

@atul1082 & @PRSAUDAG:

RBI and Kotak Saga- An interesting read-

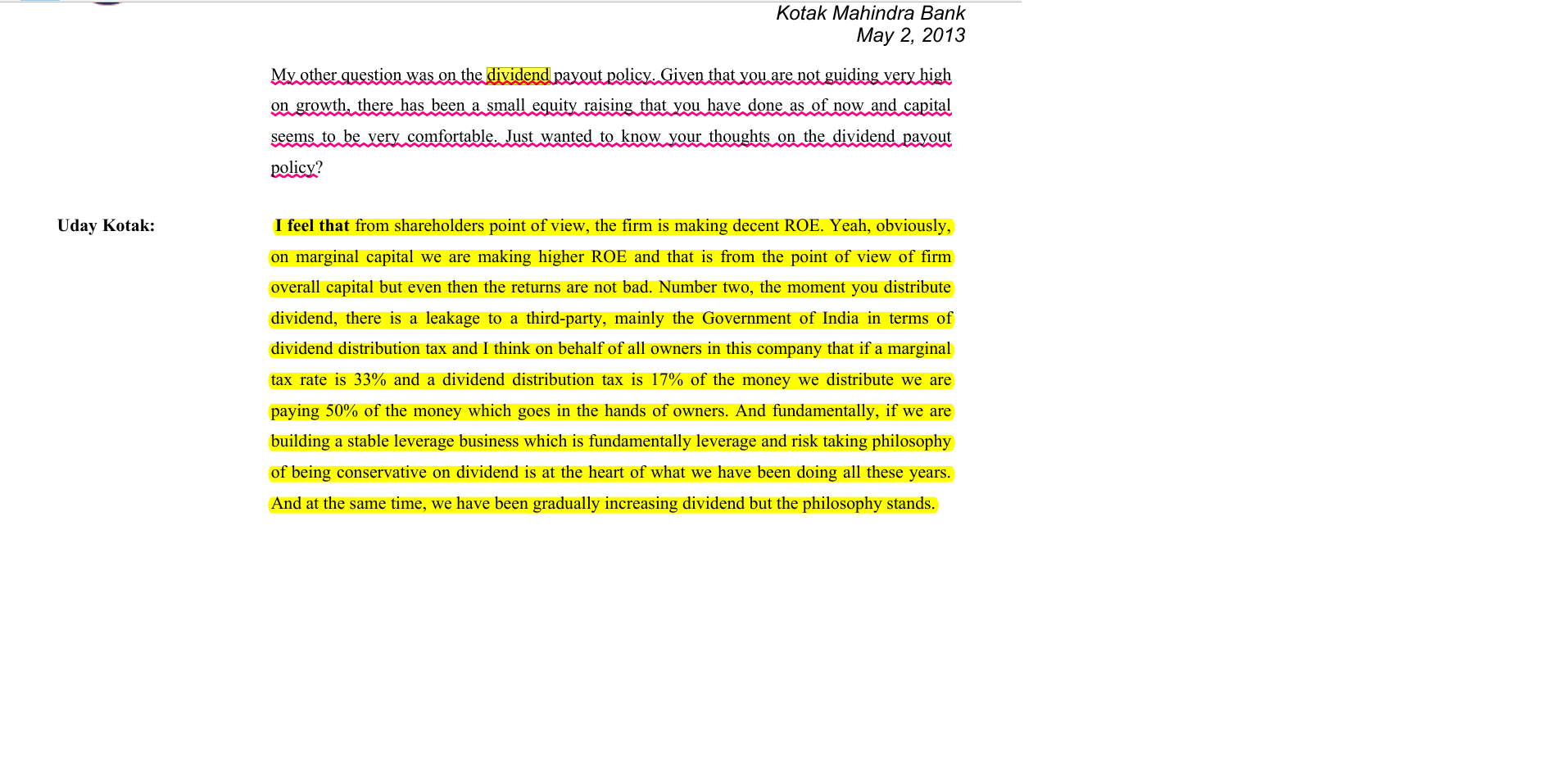

@Hao-ming: UK’s view on Dividend-

For us all, Evolution, Adaptation and Survival story of KMB:

Disc: Still Learning about the business. No investment in KMB.

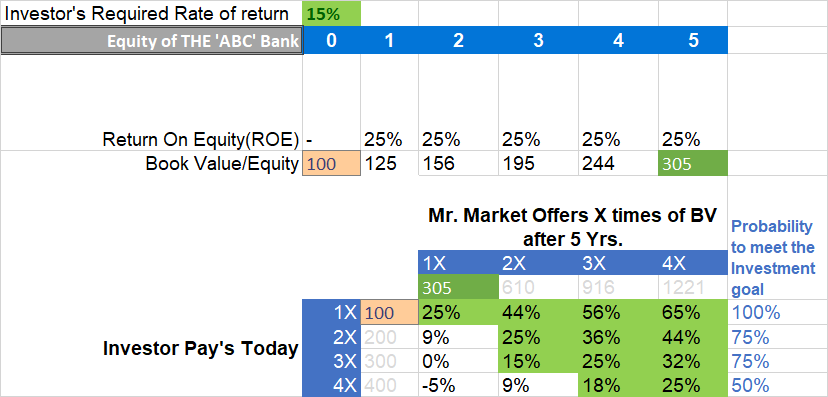

As per my thesis, KMB has the potential to grow at a rate of 25% for the next 5 years. Why?

Valuation aspect for an Investor who aspires to earn 15% from his positions looks as below:

If an investor buys the equity at a P/B ranging from 1 ~3, he/she is most likely ( 75% to 100% chances) able to earn his/her expected IRR.

Disc: Waiting for Mr. Market to push the offer in my Sweet Spot before I swing the bat.

Following guiding philosophies of the business leader- UK- caught my attention while exploring various interviews, AR’s and Conference Calls as they point to the INFINITE Game plan.

There were talks about Uday Kotak reducing the promoter holding to 26% to comply RBI rules. This one is new though, they have come up with FPO and QIP to issue new shares. What are your thoughts? Will this dilute the equity?

As mentioned earlier, UK’s stock ownership in the business is almost 30% but must be reduced to 26% by Aug-2020 as per RBI’s directive.The announcement seems to be the step in that direction.

QIP does lead to Equity Dilution. 15%+ new equity will be issued by the company in case only QIP is done in order to bring down promoters stake from 30% to 26%. Raising money via QIP is preferred as the same is faster, reliable and less cumbersome. Money goes to the company.

FPO: Considering the purpose of the exercise, I understand that it will be of Non-Dilutive nature. Promoter will sell his existing 4% shares to other shareholders. Money goes to the seller/promoter.

Let’s wait and watch. Rest time will tell.

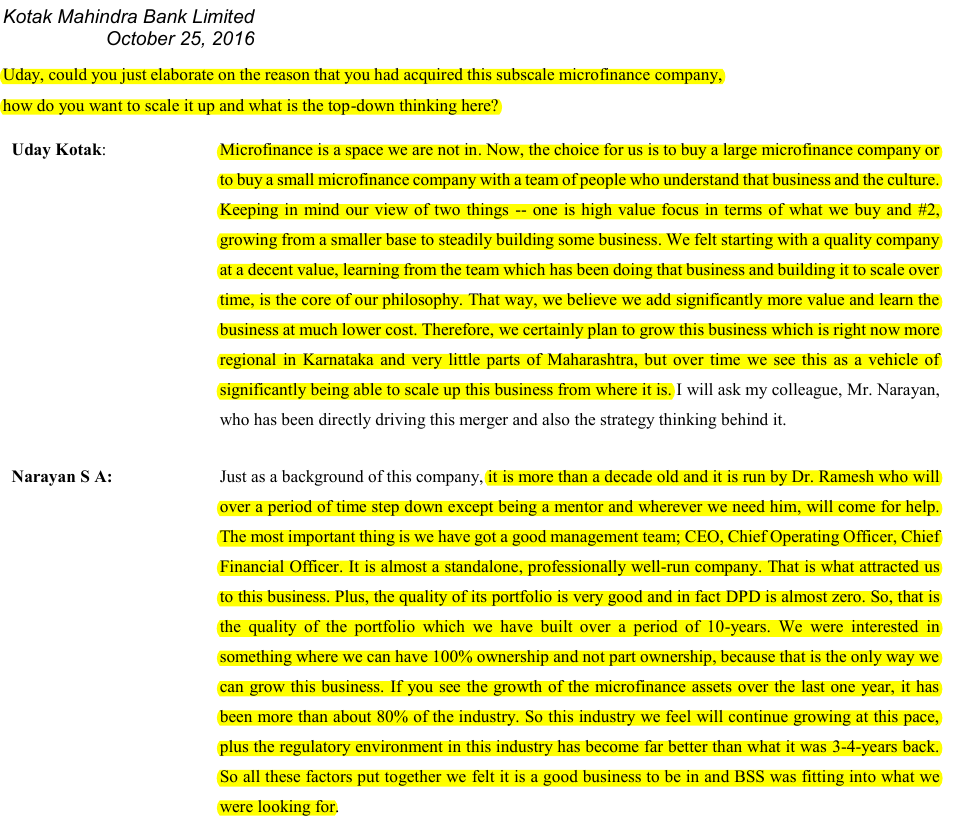

Kotak also worried about Microfinance exposure

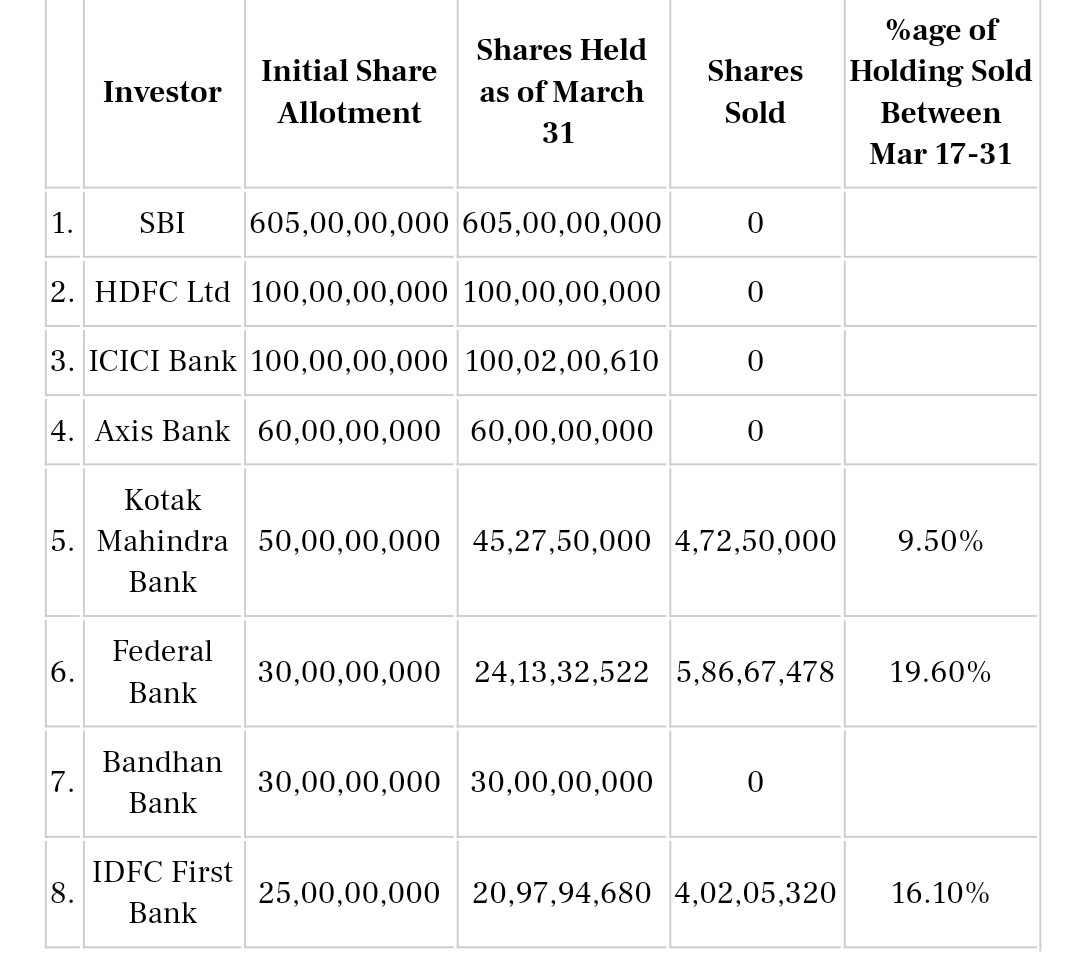

So Kotak seems to have sold 9.50% of the shares they were allotted at Rs 10 within the first 15 days. Selling price has to be around Rs 30 which was the market price around that time.

Meanwhile Yes Bank is now seeking to raise more capital to support its balance sheet.

Nothing illegal I suppose but is it ethical in the strictest sense of the word?

If yes then why didn’t the other banks also sell.

Disc- No investment in Kotak

^^“Yes Bank shares traded at anywhere between a low of Rs 22 and a high of Rs 87 between March 17 and March 31. Simply put, this means the three banks that sold stake during this period could have made anywhere between 2X to 8X gains on their investment of Rs 10 per share.”

Your figure of RS 87/- seems incorrect. PL recheck

It was intraday high (18/03/2020)

Can kotak sustain such high p/b given that growth is a question mark - additionally the ROE on the bank has historically been low (sub 15% for past 5 years). Quality should ideally be backed by good return ratios as well (for comparison hdfc bank has roe of 18% for past 5 years) while both have similar sales growth ~20% for past 5 years

Hdfc bank trades at 3x pb, while kotak trades at 4x

UBS too recently downgraded the stock to sell

Please go through this post:

Apart from this,RoE is lower for Kotak because they have lower leverage,if you look at the RoA(return on assets) that is around the 2% mark with HDFC bank being a shade lower.

On growth,that is not a Kotak specific issue,you will see that across the sector,however very few have the capacity to suffer and thus have the ability to not only survive but thrive when the environment improves a few quarters down the line.

Given what I’ve observed about KMB since posting this and also gotten a somewhat better understanding of how KMB is being run in the past few months, below factors helps me understand the valuation difference with HDFCB

Substantial hidden profits with lower savings account interest rate (something which was mentioned earlier as well but KMB has aggressively reduced SB interest from 5-6% to 3.75-4.5% in 2-3 months)

Stable Leadership for next 10 years - Uday Kotak is around 60 years old and still has 10 years to go before reaching RBI age limit for MDs/CEO. HDFC Bank’s new MD/CEO announcement is imminent and it can drastically change (up/down both) market’s views on the bank

Conservative lending and debt / equity - KMB is levered 5x whereas HDFCB is levered 7x, in economic downturns like the current one - this should definitely help the bank cope better with upcoming stress.

Their conservativeness is somewhat borne out with below as well:

On a personal note, I hold about 10 different credit cards and Kotak Mahindra was the first to send this message (3rd April) and actually hardly any other banks have shown this:

“Considering the current environment, as a preventive measure, we have temporarily suspended the Cash Withdrawal, Personal Loan on Credit Card and Balance Transfer facilities with immediate effect on your Kotak Credit Card”

Disc: Invested in KMB

In the results of Kotak Bank i saw their AUM. In that 42% of it was in Debt MF. is that a cause of concern given recent franklin episode. Though their NNPA is comfortable. But what if some of this 42% is in short term or Ultra short term Debt .IS not there a chance of Increase in NPA.

while Going further i saw their major portion of profit comes from Corporate/Wholesale banking(40% revenue,70% profit) again given covid-19 situation if big ticket project go haywire then definitely there will be pain in coming quarters.

In cash flow statement i observed decrease in Advances by 50%. may be conservative approach due to Covid-19.

As of now i am very much comfortable with NPA and performance.

I might be wrong in my analysis being a novice. do enlighten me.

Disclaimer: Invested