Kotak Bank is a coffee can stock that can be considered if an investor is looking to minimize risk in their portfolio. Many consider Kotak Bank as gold standard in banking given their high quality underwriting standards and stock has been a consistent compounder for years generating wealth for its investors.

So one doesn’t have to do any analysis other than consider their time horizon and expected returns. The stock won’t double every 3-4 years so may not appeal to investors who are looking for high alpha in their portfolio. But it’s a stock that will let one sleep peacefully with decent compounding.

i partially disagree, although long term compunding should be somewhere around 18%, given the underperformance for almost half a decade, we should easily see it double in next the 3-4 years

My comment was “Stock wont’ double every 3-4 years” which incidentally is what I said in 2021 about it.

So yes it may double from here in 3-4 years (and this time I’m fairly confident) given its long underperformance. But then whether it will keep doubling every 3-4 years is anyone’s guess as it will translate into 18-24% average return every year in stock prices. And for large banks it’s very difficult to grow stock prices at double the rate of gdp unless there is significant rerating of valuations.

Compared to other Private banks, KMB has more potential to do value-unlocking, and given the fact, the increase in the affluent class, KMB poised to do well, although compounding at 25% for a decade is day-dream, 5-7 times in a decade should be their trajectory, yes I would agree no large company can grow beyond country GDP(unless export), India itself will grow 6-8%, and KMB themselves are not in top 3 or even top 5 for that matter, so I would say they are not systematically important bank yet.

Kotak Bk buys StanChart’s ₹4,100cr personal loan biz

Kotak Mahindra Bank is set to acquire Standard Chartered Bank’s Rs 4,100 crore personal loan portfolio, which primarily targets affluent customers. The deal aligns with Standard Chartered’s strategic shift to focus on wealth, affluent and SME segments, while continuing to invest in wealth & retail banking, and corporate & investment banking in India.

StanChart’s exit from personal loan business follows RBI’s advisories urging caution over unsecured loans and increasing risk weightage on specific segments. The move comes two years after MNC rival Citibank decided to exit its retail business in India, and sold it to Axis Bank.

“Our decision to divest the personal loan book aligns with the Bank’s focus to accelerate growth in the wealth, affluent and SME segments. India continues to be a key market for Standard Chartered network, with wealth & retail banking and corporate & investment banking as the cornerstones, and we will continue to invest and grow in India,” Aditya Mandloi, head (wealth & retail banking) at Stan dard Chartered Bank, said.

Earlier this month, StanChart had announced the retirement of Zarin Daruwala, CEO for India and South Asia, effective April 2025. Daruwala, who has been with the bank since 2016, played a pivotal role in expanding its presence in India. Last month, Sanjeev Mehta, managing director and head of transac tion banking sales for South Asia, also resigned after 17 years with the bank, with plans to start a greenfield venture. In a separate move, Standard Chartered sold its 3.09% stake in Protean eGov Technologies for Rs 225 crore in Aug, continuing a broader strategic reshuffling.

“India’s unsecured lending market offers significant growth potential for Kotak, especially in the higher-end segment. Our strong risk management, customer-centric products, and technology-driven approach position us for sustainable growth. This transaction supports our retail assets growth strategy and reinforces our commitment to retail lending,” said Ambuj Chandna, head (products), Kotak Bank.

With over 165 years in India, Standard Chartered remains one of the oldest foreign banks in the country, with 100 branches across 43 cities.

Anyone has a good view on the valuation of the subsiaderies?

Given the PAT runrate of the kotak investment, kotak amc and kotak securities has exploded all which deserve valuation twice standalone bank. Also kotak life has superior margin and return profile vis a vis industry.

my back of envelope calculations show subsidaires after 20% holding discount should be valued at 700-770 Rs/share. So core standalone bank is trading a 2x book value cheapest of all the banks.

I think it would be critical for kotak to get back to 20% growth runrate or also to look at good acquisitions as current leverage is low and the CAR is too high for it to do 16-18% ROE, even after being best on NIMs and ROA.

Kotak given its 100% control over subsidiaries is probably quite antifragile as most of its subsidiaries dont carry balance sheet risk and would aid core bank to drive higher growth without diluting equity

A very lazy calculation without much rigor, by projecting full year numbers for subsidiaries

Kotak Life: 3x embedded value

16000*3 = 48000crores

Kotak prime: 9650crores = 2x book value: 19300crores

Other lending subsidiaries book value 5000crores valuation 2.5x book value = 12500crores

Isn’t it pretty much the same story for all major private banks? All of them are juggernauts with subsidiaries in AMC, Insurance and similar verticals. There’s hardly any differentiation on that aspect, except that it justifies these banks trading above 2x P/B multiple compared to smaller private bank peers who don’t have such subsidiaries.

Other banks don’t have a 100% ownership in all of there subsidiaries. In Kotaks case the value of subsidiaries is much higher as % almost 50% if you remove the holding company discount. But i take your point most banks are trading around 2.2-2.3x core PB value. ICICI bank may be the most expensive one.

Given small size feel Kotak can grow much faster than peers + there is optionality in terms of M and A, Increasing leverage(Kotak has least leverage) will see the Pat growth will be faster than balance sheet growth.

At 19-20x PE, Pat growth over next decade can be 18-20% believe it is fairly priced. Given the rest of the market is so expensive market could come back and start giving premium for 15% consistent growth companies if the rest of the market earnings growth slows down as it happened between 2014-2018

Mr. Kotak himself has told in past he is not inclined to demerger of the subsidiaries and more intrested in a consolidated house and believes in one unified kotak brand. So market won’t give any better valuation to Kotak for these subsidiaries unless it feels demerger is on the way to create shareholders.

In the year 2023:

Similar views in the past (2017):

Not sure if current CEO has different views.

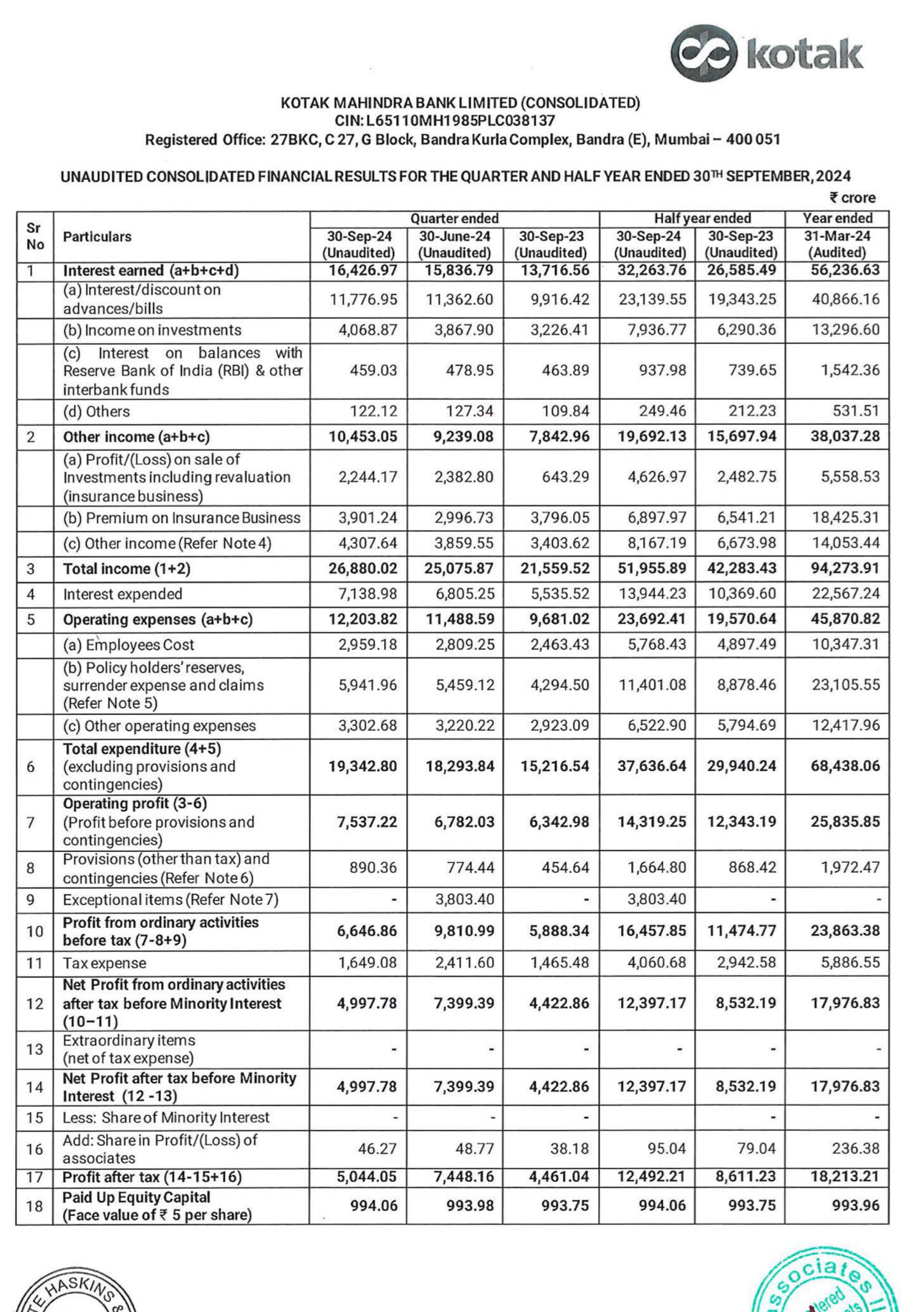

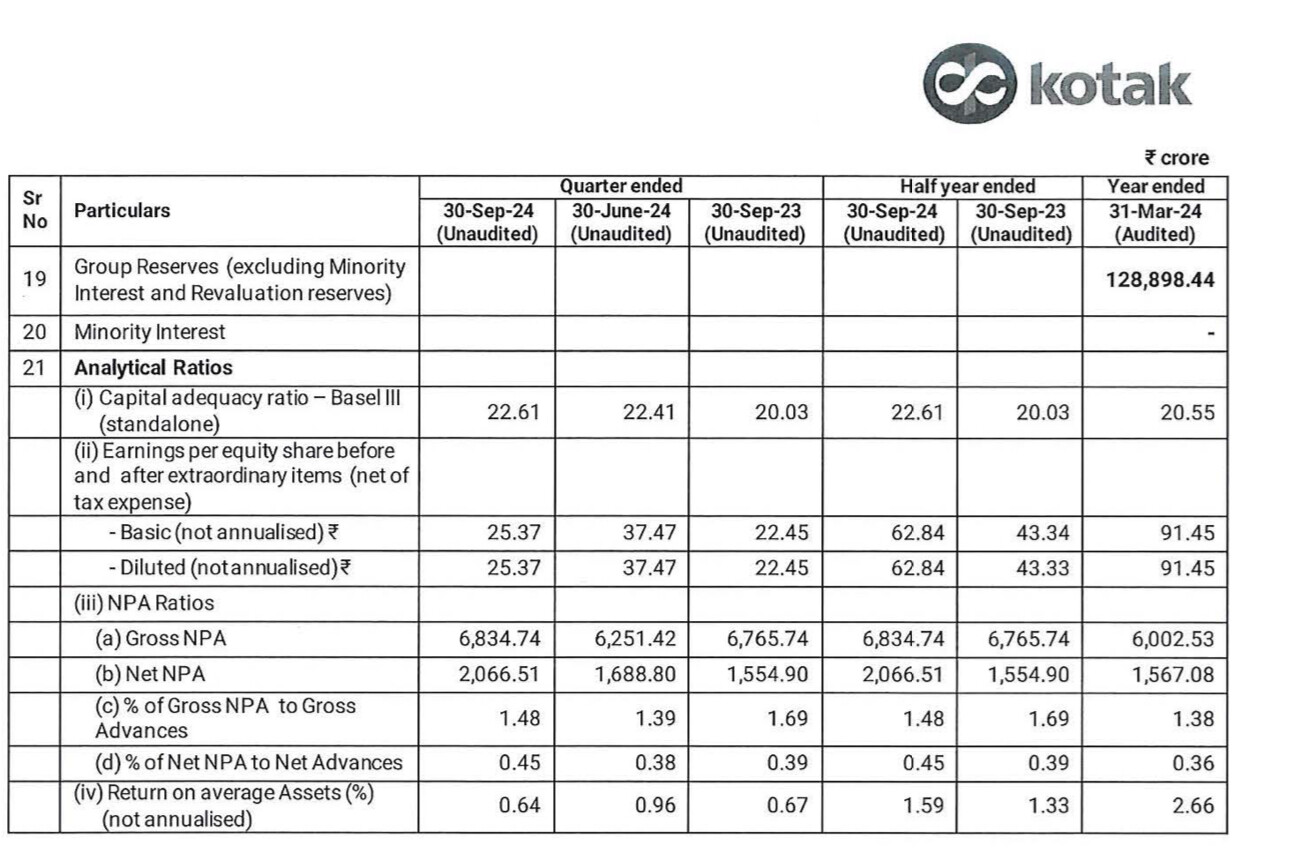

If you see the recent quarter results,they are not good in terms of standalone or the core banking business.It seems business has stopped growing and on top of that NPAs are increasing. However good show from the subsidiaries have saved the day for Kotak Bank.If you see kotak securities profit is 444 crore(compared to 400 crore in earlier quarter) and kotak life profit is 360 crore( compared to 170 crore in earlier quarter).So these businesses are in my view perfect for demerger and create good wealth for shareholders.But we as shareholder can only hope ultimate decision lies with leadership which is at current junction not inclined for demerger.

Disclaimer: Invested in kotak so views may be biased.

What makes you believe that these profitable businesses will be listed as demergers?

Like in case of HDFC, these cash hungry banks would prefer IPO route more than demergers. Even if these get listed, going as per other banks and also as per constant need of funds by banks, logically there are high chances of IPO and not demerger. So, no free shares for Kotak bank shareholders in that case.

My thoughts as well. I guess, this is what market is now pricing in. Shareholders are getting shortchanged these days. Only consolation is you get to apply for IPO in both categories - shareholder and retail/hni. But again even if you own 1 share you’re eligible for shareholder category.

well in this case, i would not say shortchanged…it would be rather unrealistic expectation of a demerger when the business dynamics itself demands an IPO…what actually happens is anyones guess and also shareholder/promoter sharehilding dynamics and rules/regulations…

From the concall, apparently, the pain can continue for next 2-3 quarters :

On the MFI side of the business, we restricted growth because as we called out about two quarters ago, we were seeing some strain, and we are being cautious of growing in the MFI space. We expect this trend to continue for the next quarter, maybe two quarters, and then it should get okay.

On the Unsecured Retail business, obviously, the tech embargo has had an effect, particularly on the credit card business. And as you can see, our total share of retail unsecured asset businesses has dipped a little bit to a shy over 11%. In the credit card business, we have also seen some level of credit stress due to the overleveraging of certain kind of customers.

Kotak Bank has reached a loan book size of approximately 4.5 lakh crores, similar to where ICICI and HDFC were ten years ago. ICICI managed a loan growth rate of ~ 13% in the past decade, even amidst significant challenges with non-performing assets (NPAs), where gross GNPA exceeded 5% for several years

Currently, Kotak Bank boasts superior asset quality, return on assets (ROA), return on equity (ROE), and less leverage than ICICI did a decade ago. Given this, I believe Kotak could feasibly grow its Advances by 15% annually over the next ten years, especially considering they’ve already achieved this growth rate in the past decade.

While I have numerous arguments supporting this investment thesis, I’m seeking counterpoints. What should I be cautious about before investing in Kotak Bank? or the banking sector altogether

Kotak Bank has not given not more than 5-6 % return for a year. In this quarter NPA has increased along with existing ban on credit card and 811 scheme.

Valuation seems to on lower side. That’s why I started buying it but increase in NPA has stopped any upside in prices. My conviction says it can deliver 20-25 percent return from here, if ban removes from it along with decrease in NPA.

New management seems to have fire in belly and expecting ban to remove within 6 months. Till then I am holding. Finger crossed. Let see where it goes.