ICICI Bank and ICICI Direct web site was down for more than 4 hours just few days back (I do not remember the exact date), so these technical glitches are across the Banks.

Sometimes those are not reported widely by Media.

Hence, as long as business is good, an investor should focus on the business fundamentals.

Off course in this case, fundamentals will be impacted to some extent but keep faith in your conviction and management’s capability to overcome such tough situations.

Probably they were little less cautious earlier and Hope that, they will learn a lesson and turn around the situation like many other banks.

Disclosure : Invested in Kotak Bank over past 2-3 years in staggered manner. Patience will be tested here.

I recently(few days back) entered in it and now kotak is my largest holding. Didn’t do any in-depth analysis but I understand the indistry. The sheer diversity of businesses it holds and the fact that Uday Kotak (according to me he is class apart from the rest) having 25% shareholding is enough. Sometimes we overthink and fail to act.

In short term , narratives sometimes outweights fundamentals of stock. Fundamentals after Regulatory action does’not change, but with good quarterly results , Narratives changes fast. Things which does not look good in bad narratives suddenly start showing some worthiness after positive narratives. What lies a fine difference between good and bad narrative is the patience. But I always try to remember that market can remain insolvent for very long time , enough to loose one patience. Let see where it ends and who wins- patience or narratives.

Disclaimer: Holding & biased.

Its not just glitches and outages. Its more to do with Data Protection and other IT compliance norms. We don’t know the dirty details of RBI communication with Kotak over the past two years, supposedly classified.

I have to say that this article actually challenges the integrity of Kotak Mahindra Bank by showing the proof from the Annual report and who could possibly be accountable.

I have been reading multiple articles and how most articles are left-right writing something but this looks something to give sometime to read.

We have seen that majority of the lenders regardless of their cachet have been found wanting (HDFC, Bajajfin, Kotak, many PSUs) in their IT infrastructure.

And it’s not a problem specific to India. Globally also many banks are running on legacy IT platforms and, for reasons best known to them, have put their infrastructure modernization on backburner. I faced many problems with a big international bank (including a recent fraudulent transaction on my credit card) and I moved my account to another bank.

In India, if every bank is found deficient, consumers don’t have any option but to put with all the risks and inconvenience. So it’s a very welcome step from RBI to crack down on this nonchalance from banks and full marks to them for being alert to such deficiencies in the system.

For banks, these are not tough problems to fix; they just needed a bit of rap on the knuckles.

HDFC and Bajajfin fixed their issues within 2-3 quarters. Recently Bank of Baroda did the same.

And I’m sure Kotak will get it done too sooner than later.

“Hemindra Kishen Hazari” has been highlighting such lapse of corporate governance across various banks in the past. He has timely highlighted certain issues related to IndusInd bank as well in the past and shareholders have seen massive correction in its stock price during COVID crisis.

This article has highlighted many governance issues and lazy approach by bank management in addressing IT risks and probably there are few other undocumented issues.

Concerns mentioned in the article are genuine. With due respect to the Kotak Bank management, the observations are quite serious. Overall handling of IT systems and Kotak 811 App seems below my expectations.

Having worked in IT industry for over 25 years, and Cyber Security for over 5 years, the issues highlighted in the article look serious to me.

Disc: Holding Kotak Bank from the past 2 years and it seems that, Market has de-rated the stock from P/B of 5 to 2.8-2.9 with logical reasons. Need to be watchful about future events.

Keeping short term noise aside, this could be an excellent opportunity to aggregate this stock if already holding or could be used as an entry point. With the rejig of the management, this could potentially be a multi decadal story of rise of an indian bank on global scale.

Even though it trades at premium than its peers, lot of players are aggregating this ‘silently’. Ignore the reports, buy if you believe the story. (INVESTED)

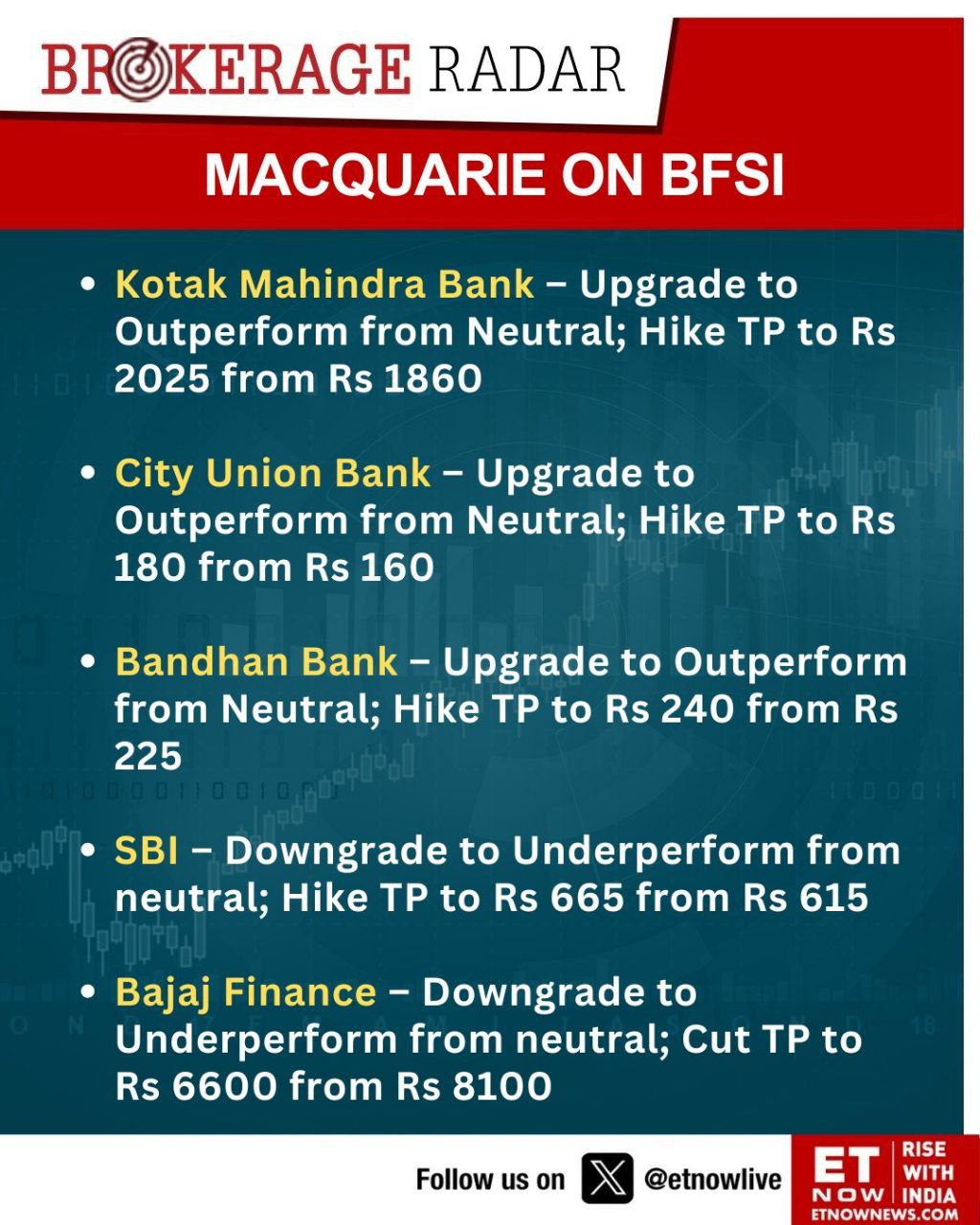

Brokerage calls don’t (and shouldn’t) mean anything. For every stock you will have brokerages with buy, sell and hold recommendations and every brokerage house has as much probability of being right or wrong as their peer. Macquaire has been wrong with lots of their calls but so have been other brokerages.

For Kotak Bank holder this seal of approval may seem like a good news but those holding Bajaj Finance and SBI shouldn’t get disheartened. They have made a lot of wealth for their investors and will continue to do well as fundamentally they are strong and well managed lenders.

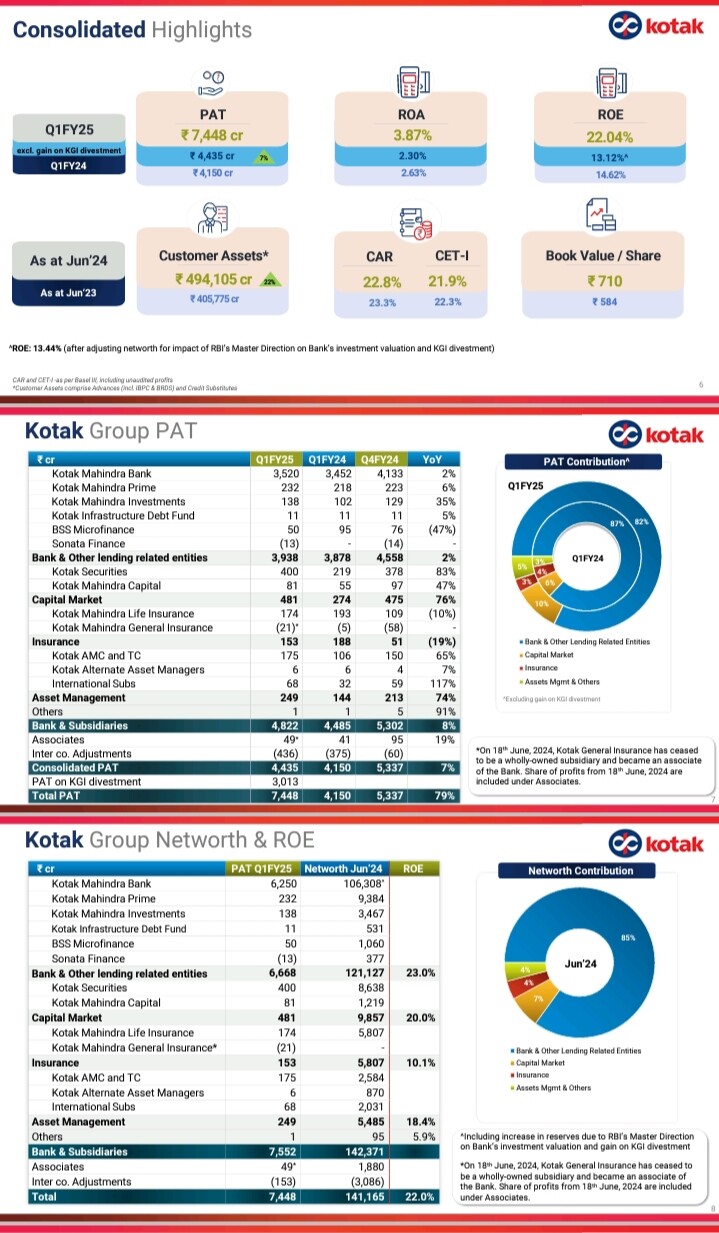

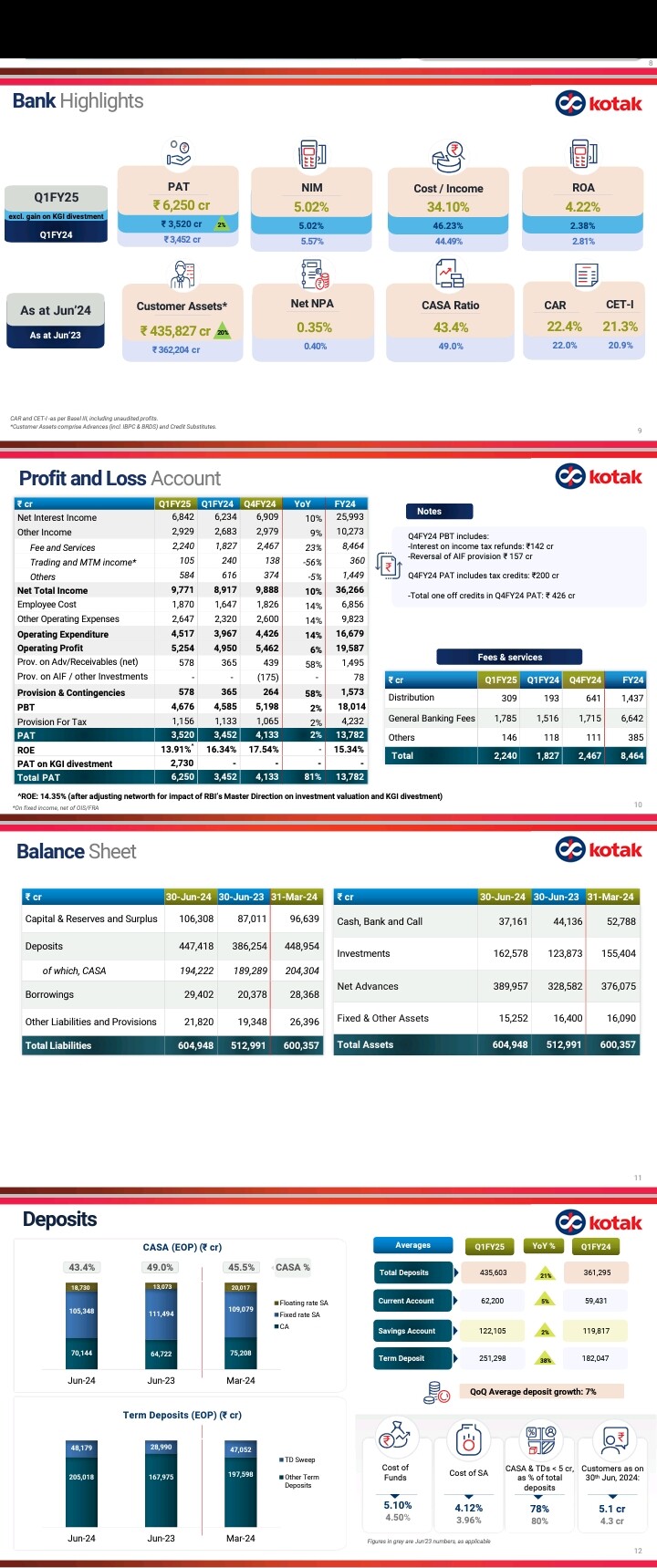

Material Financial Updates

•Profit (net of tax) on divestment of stake in Kotak General Insurance (KGI): ₹ 3,013 cr on consolidated and ₹ 2,730 cr standalone basis

•RBI’s Master Direction on Bank’s investment valuation: ₹ 3,414 cr increase in reserves (net of tax) as on 30thJune, 2024 Impact of above is included in figures / ratios computed above, as applicable

•Customer Assets:Up 20% YoY •Avg Deposits: Up 21% YoY •NNPA:0.35% Customer reach

Bank Customers 5.1 cr

ATM 3279

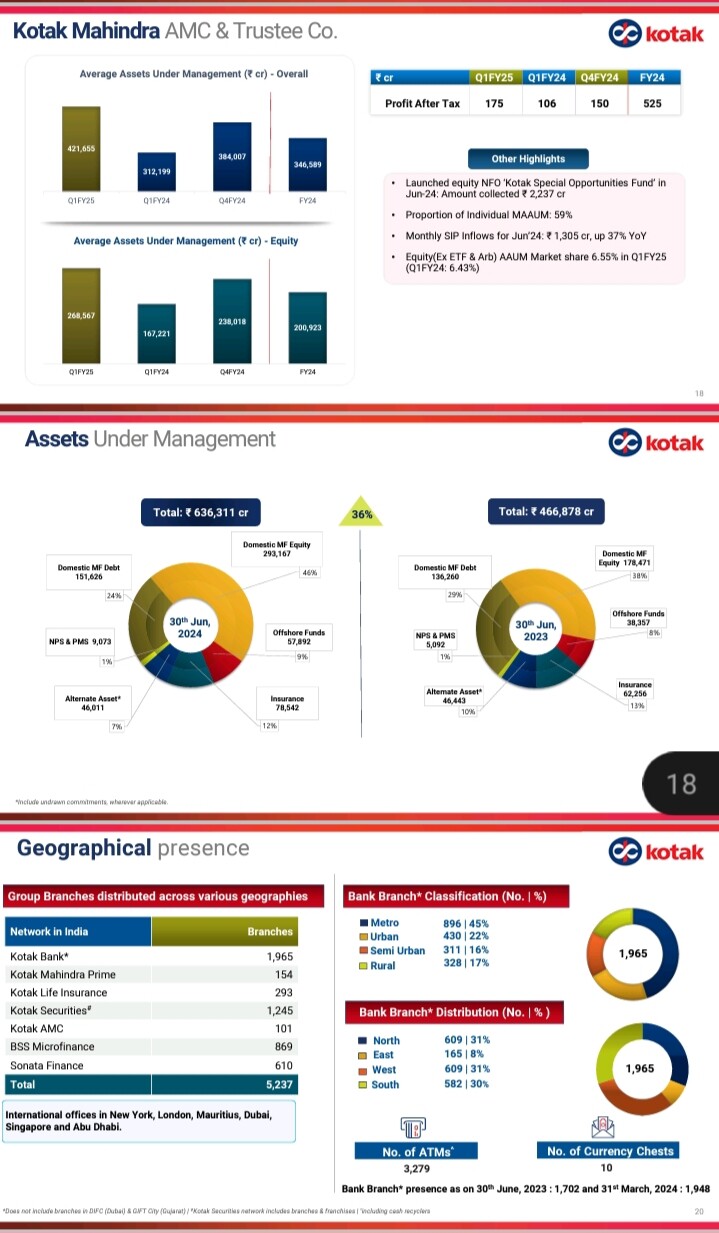

Group AUM ₹636,311 Update on RBI Supervisory Action

Reserve Bank of India (“RBI”) order of 24th April 2024, directs the Bank to cease and desist:

•Onboarding new customers through the Bank’s online and mobile banking channel

•Issuing fresh Credit Cards. The order does not impact:

•Servicing and cross-sell of products (excl. new Credit Cards) to the existing customer base through all channels

•On-boarding of new customers through other than online/mobilebanking channels Action taken by bank

•External auditor appointed and scope of audit finalized in consultation with the Regulator

•Augmented capacity through onboarding external IT vendors to expedite

compliance

•Remedial action plan are on track

•Constant interaction and update to Regulator on progress Business & Financial Impact

•Potential financial impact continues to be in line with the initial estimate

•Redeployment of resources to deepen existing relations, improve cross-sell Divestment of stake in Kotak General Insurance

•Zurich has acquired 70% stake in KGI for ~₹5,560 Cr by way of fresh growth capital (~₹1,460 cr) + secondary acquisition from Bank (~₹4,100 cr)

•KGI post money valuation : ~₹7,940 cr

•KMBL’s total capital infusion in KGI: ₹875 cr

•Post this transaction, KMBL holds 30% stake in KGI and will continue to act as corporate agent of KGI for distribution of general insurance products Consolidated Results

•Q4 FY24 PBT includes: -Interest on income tax refunds: ₹142 cr-Reversal of AIF provision ₹ 157 cr

•Q4 FY24 PAT includes tax credits: ₹200 cr

•Total one off credits in Q4 FY24 PAT: ₹ 426 cr

•Unsecured retail advances (incl. Retail Microcredit) as a % of Net Advances:

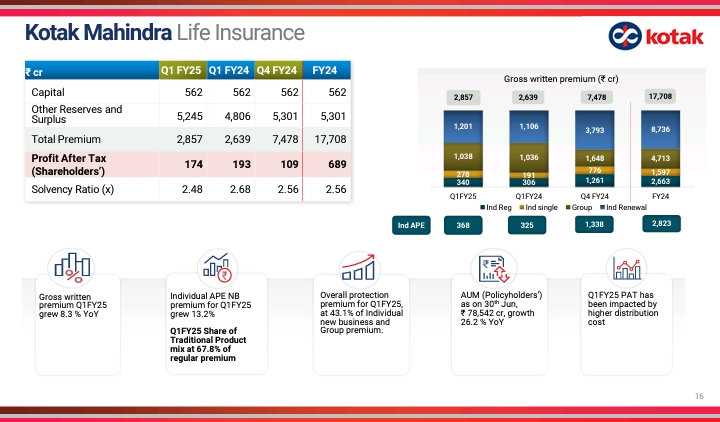

•31stMarch, 2024: 11.8% Kotak life insurance

Hello, I am new to banking sector so just wanted to understand why Kodak’s NIMs are more than that of ICICI/HDFC/Axis even though they have similar cost of funds?

Kotak has lower debt to equity ratio (<5.00x) than other 3 (>6.5x), which means they are using higher proportion of their own funds (which has no interest cost associated with it). Another metric to check can be Interest spread, (Interest yield-Cost of funds, ignores effects of leverage)

I do not know if there is difference in customer segments, haven’t studied the business in detail.