As per my thesis, KMB has the potential to grow at a rate of 25% for the next 5 years. Why?

- Lower base-Size of BS as well as Advances- as compared to top 4 banks

- All the top managers are from operations background with customer know-how as they have played various roles across the business verticals. Some of the verticals were started by them from ground zero.

- Uday Kotak, MD & CEO as well as the founder of the business, is leading the business for 33 Years. He started the business with bill discounting to take advantage of the huge gap between deposit and lending rates dominant in the banking industry in 1985, with 3 people and 30 lakh capital from family and friends. Over the time period, other parts of the business under the group’s umbrella were added. His knowledge and passion for the business stands out in public interactions such as interviews, conference calls. Considering his long term focus on building a bank of future, and the solid team that he has built and retained from the last 20 odd years, I categorize him as a Lion Manager. Considering his stake of 50,000+ Cr in the business in the form of stock ownership- his stock ownership in the business is almost 30% but will be reduced to 26% by Aug-2020 due to RBI’s directive. Also, from Apr 01, 2020 his voting rights will be capped to 15% even though holding will be 26%. UK cannot buy any more shares with voting rights unless his holding falls below 15%.- as compared to his annual salary of 3.5 Cr., I expect him to be an active manager for the next 7~9 Years during which he would continue to nurture the business with a long term focus.

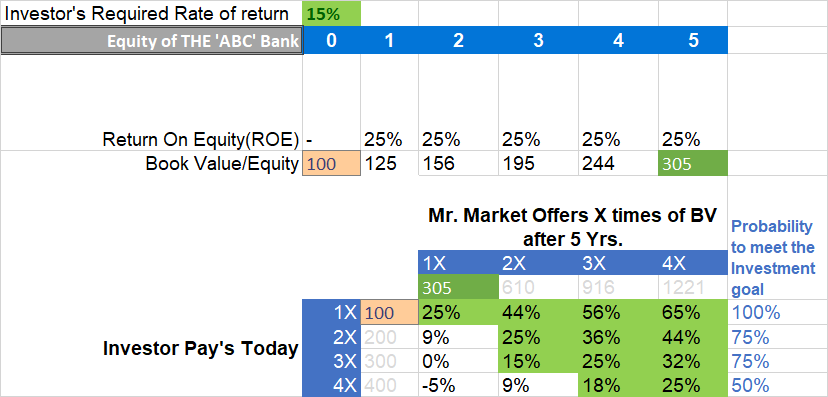

Valuation aspect for an Investor who aspires to earn 15% from his positions looks as below:

If an investor buys the equity at a P/B ranging from 1 ~3, he/she is most likely ( 75% to 100% chances) able to earn his/her expected IRR.

Disc: Waiting for Mr. Market to push the offer in my Sweet Spot before I swing the bat.