Dear ValuePickr members, I’m Tejas Venkatesan, an 18 year old student who’s passionate about investing. This is the first thread I’m writing about a company I found recently, and would appreciate your views and thoughts. Would highly appreciate any feedback on my research method. Thanks.

Business-

Knowledge Marine Engineering Works is primarily engaged in the business of owning, chartering/ hiring along with manning, operation and technical maintenance of marine crafts and repairs/ maintenance of marine crafts and marine infrastructure and allied works in India.

They started in 2013 as a repair and refit company based out of Mumbai and after 2 years they began owning and operating small crafts. Their revenue streams include dredging, carrying out repair & refit services of naval & merchant ships; Conducting hydrographic & magnetometer surveys; Providing technical solutions for maintenance and operations of vessels. Most of these are services provided at ports. The company has an order book of 250 crores and is expected to complete 125-130 crores of that in FY23. Dredging contracts have EBITDA margins of 50% and the company keeps a threshold of 40%.

Dredging-

Removal of sediments and debris from the bottom of oceans and harbours to create navigable waterways for shipping traffic at ports. Can be done to remove pollutants and underwater excavation to mine minerals as well. It can also be done for dams and rivers to remove sediments. It is classified into capital and maintenance dredging: Capital dredging- first time it’s done. When ports want to increase their depth to bring in larger vessels, they do capital dredging. Maintenance dredging- Done after capital dredging has been done as soil and silt get deposited over time.

Growth Plans-

Ship Building

They have set up a JV with Synergy shipyard in Goa, this is the shipyard where they usually place orders for the ships they use in-house for the past 3-4 years. They feel there is a larger market opportunity and hence are going to build ships for the external market as well. This is expected to materialize in the next 3-6 months and will be a 50:50 venture. KMEW will bring orders for the shipyard which already exists so capex will be zero. They expect to earn 20% profit margins from this segment.

Shipping Harbours

They have mostly been dredging at ports. They had made bids for developing fishing harbours in Gujarat. A day after mentioning this in their concall, they were awarded a contract for Capital Dredging at Mangrol Fishing Harbour Phase III Part B by DCI worth 67.85 Cr plus GST. This is in rock dredging which is a new segment for KMEW. They have partnered with Sahara Dredgers for this project and hence will have no upfront capex costs.

Cutter Suction Dredgers-

They are forming a JV with a company that owns 4-5 CSD which are ready to deploy. This will fetch orders for inland waterways and be operational in the next 6 months. Again, the partner company already has the dredgers and KMEW will deploy them by getting orders from the government. In comparison, dredging corporation of India (listed company) has only 2 CSDs but Adani ports has 16.

CSD:

Trailing:

Scrapping yard-

They are doing a JV through which they tie up with a scrap yard that already exists in which they will bring in vessels to scrap and eventually buy parts and sell them at a higher price or use them in shipbuilding processes as they have in the past.

The management has set a goal of reaching 500 Cr of revenue by 2025 in their latest concall.

Strengths-

Lower Capex costs-

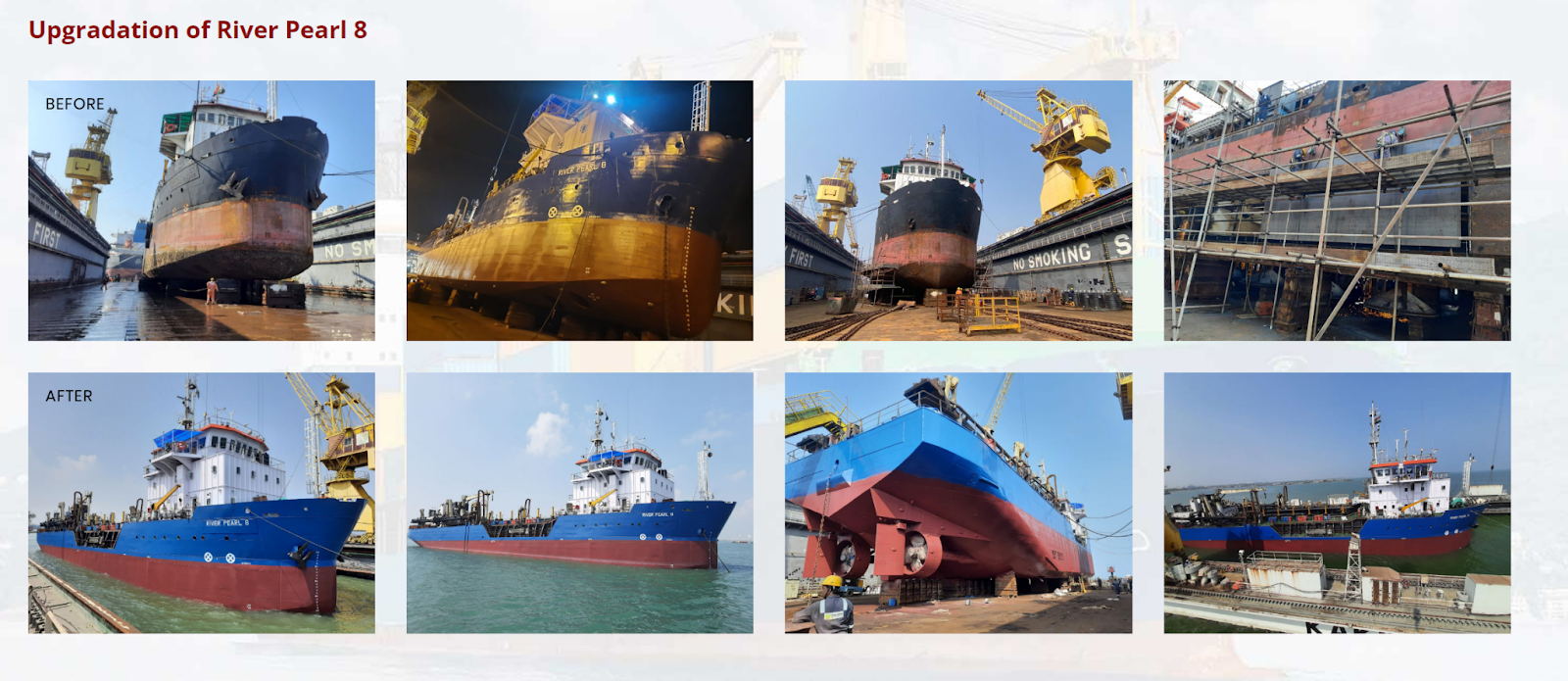

They have a team of 40 marine engineers that can repair ships with ease. Therefore, their capex costs, i.e. cost of adding to their fleet is much lower than their competition. For their Myanmar contract of 117 Cr, the capex was 5.5 Cr to buy a scrapped vessel and they spent 15Cr to develop the vessel. The vessel for the contract is River Pearl 8. For similar contracts, competitors would normally spend 100 Cr to make a similar dredger.

More efficient with time= better margins-

Dredging Corporation of India’s vessels go into repair or dry dock or conversion or upgrade facilities for around 6 months. KMEW does the same within three to four weeks. Therefore, their vessels continue working.

More downtime at DCI (from KMEW concall)

“They have a usual period of downtime every month of more than five days, five to six days, we find time during the day and night, we have a different staff, different set of crews which do our regular preventive maintenance, breakdown maintenance, so we have lesser down time as compared to them. Our employees, we have about 10 employees carrying out all the operations, they have more than 80 employees carrying out the same operations, so their overheads are much higher than us, so these are the reasons for which their margins are low.”

Young fleet-

Except for the Trailing Suction Hopper Dredger all our marine crafts are new and of make younger than 2016. This means better technology, lower maintenance costs, and downtime.

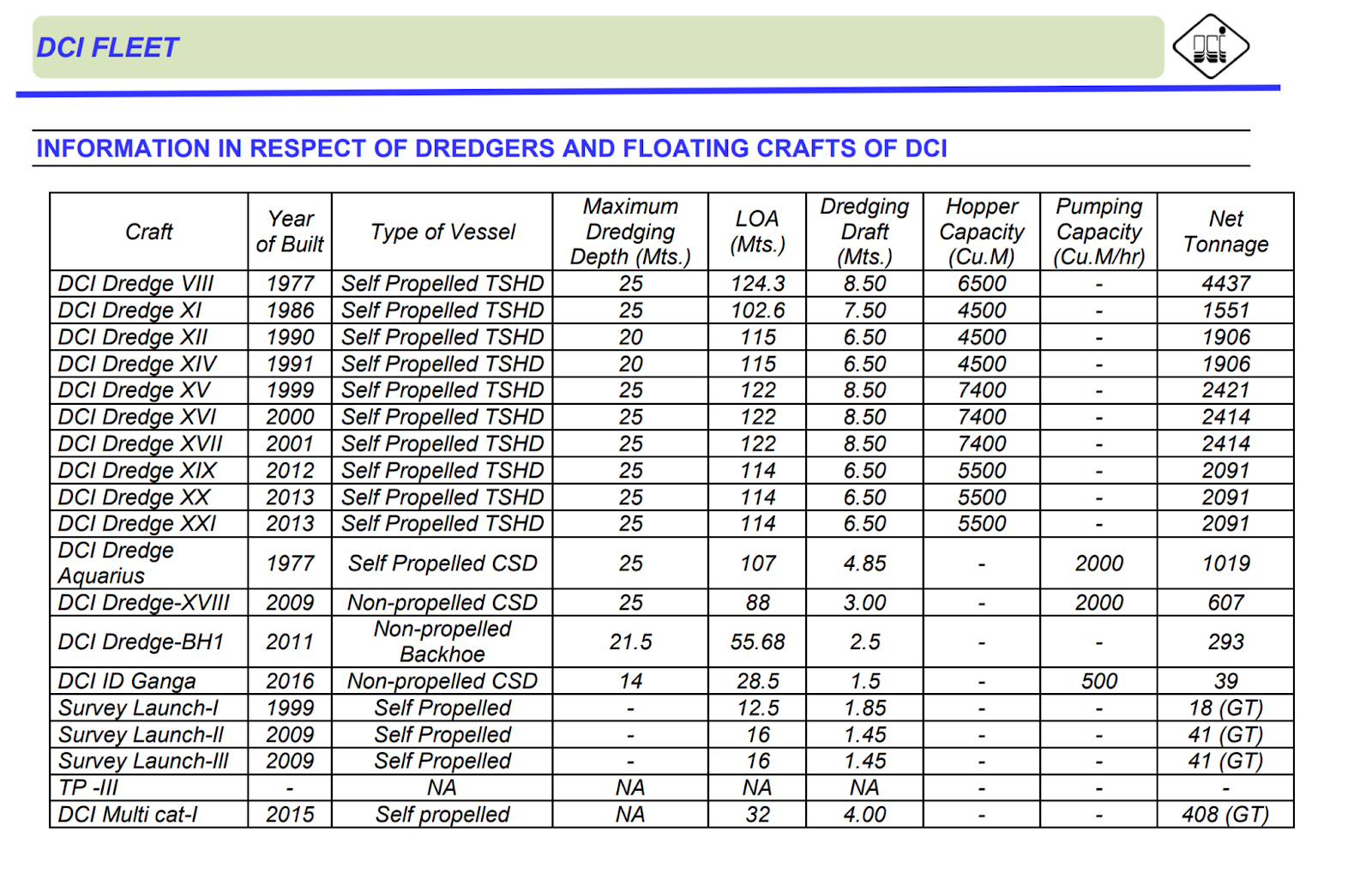

Compared to DCI:

Most of their dredgers are built before 2000, others are before 2016. Their average age is 20 years. DCI has 88% of market share in maintenance dredging in the domestic market.

From Dredging Corporation of India FY2021 AR.

This page shows dredgers owned by Adani ports:

Dredging and Reclamation Solutions - Adani Ports and SEZ Ltd.

They range from being made in 2007 to 2019 so are a bit older than KMEW’s but are European so may have better build quality and be operational for longer.

Great financial returns-

Example- they bought River Pearl 4 (Trailing Suction Hopper Dredger) for 16.5Cr and it is working on a 5-year contract worth 87 Crores. Their dredging contracts normally have 50% EBITDA margins. The lifeline of a vessel is around 15-20 years so the same dredger could get more contracts as well. They claim the payback period on their fleet is usually 2 years.

Opportunities-

New Dredging Guidelines 2021- “Sizeable dredging opportunities”: Views of DCI’s Dr George Yesu Vedha Victor - Indian Infrastructure

The Dredging Guidelines, 2021 envisage dredging to the tune of 3 billion cubic metres (bcm) (1.6 bcm capital dredging and 2.4 billion cum maintenance dredging) over the next 10 years. Currently, only 120 million cum annual dredging is being carried out at major ports and dockyards in the country.

Any dredging project under 200Cr has to be awarded to a domestic company.

Very few dredging companies bid for orders below 100 crores in India. The work requires a lot of skill and knowhow and this has allowed them to have a hit rate of over 50% on projects they place bids for.

Sagarmala-

India has 12 major and 205 notified minor and intermediate ports. Under the National Perspective Plan for Sagarmala, six new mega ports will be developed in the country. The government has envisioned a total of 189 projects for the modernisation of ports involving an investment of Rs 1.42 trillion (US$ 22 billion) by the year 2035. It is expected that by 2025, cargo traffic at Indian ports will be approximately 2500 MMTPA while the current cargo handling capacity of Indian ports is only 1500 MMTPA. A roadmap has been prepared for increasing the Indian port capacity to 3300+ MMTPA by 2025 to cater to the growing traffic. This includes port operational efficiency improvement, capacity expansion of existing ports and new port development.

Weaknesses-

They are a relatively small and new company in this space, this may hinder them from getting larger contracts. While some contracts are long-term in nature, revenue would tend to be lumpy and it may be hard to forecast sales growth.

Threats-

Revenue is linked to the government. It is a B2G business and receivables could become higher. In the past they have had no such problems, however in larger contracts they may face them.

There is competition from Adani ports which has a fully owned subsidiary called Shanti Dredgers that has a fleet of 23 dredgers. Though most of their operations seem to be projects at Adani ports itself, KMEW claims that they have recently started bidding for other large contracts. If Adani slows down the expansion at their ports, they may start bidding more with these dredgers and take market share and reduce contract prices.

Their Myanmar contract was exceptional- it is the second large contract (above 100Cr) they have received and is around 118 Cr. The company may not be able to get large contracts like Myanmar in the future.

By expanding using many JVs, they may face management issues.

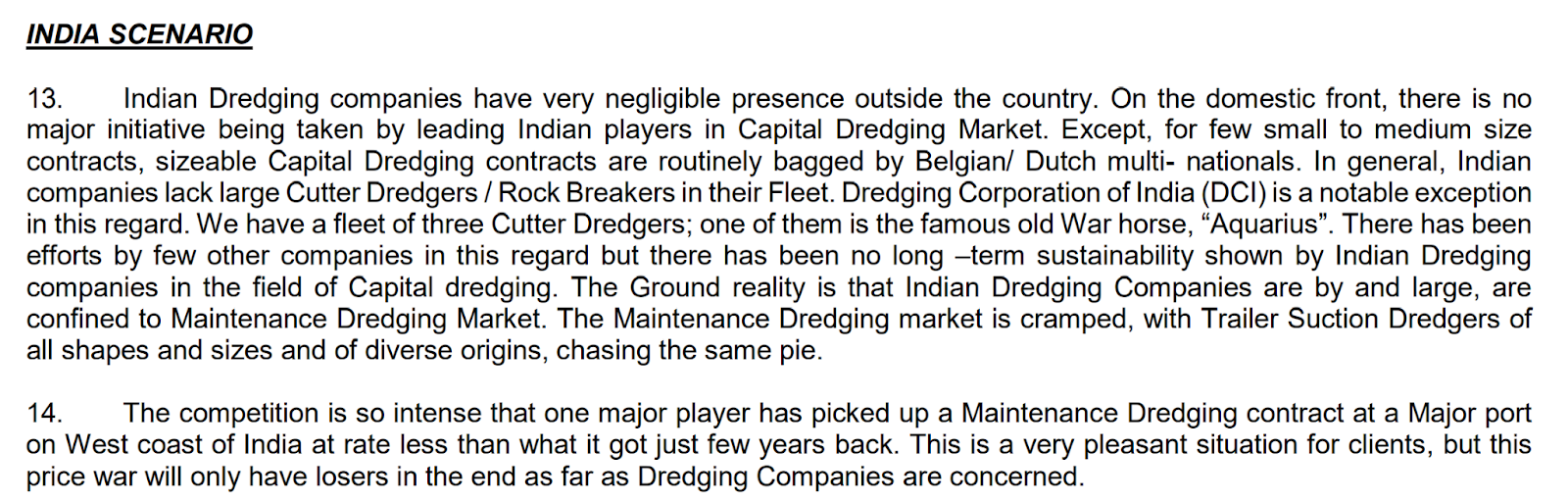

Dredging Corporation of India has painted a very negative picture of the domestic dredging industry in their MDA in FY21 Annual Report-

Valuations-

The company has an order book of 250 Cr and expects around half of it to be completed in FY 23. In this year, they will also incur negligible capex as all of their growth plans will be conducted through joint ventures. Therefore, revenue would be around 125 Cr and they estimate margins to fall by around 5% as future contracts may not be as profitable as Myanmar. An estimate for FY 23 PAT could be 41.9 Cr which is a forward P/E of 12

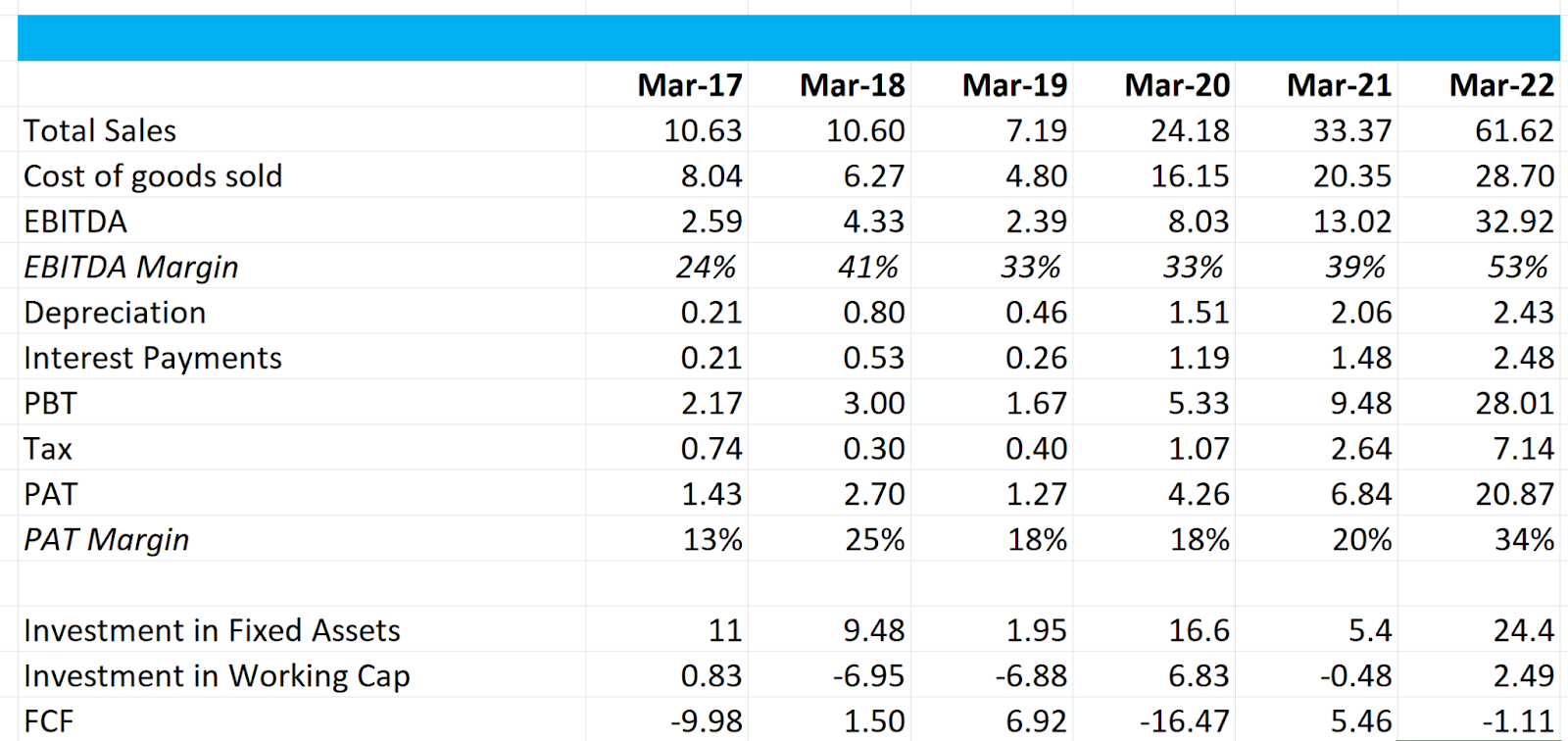

Past: The numbers in screener have few errors as compared to their own annual report. I have used data from their annual reports as found on their website.

They have grown their fleet from zero in 2016 to 10 in 2022 which explains negative FCF.

They state that the reason for the degrowth in sales in 2019 is that the company switched its clients from private to government segment.

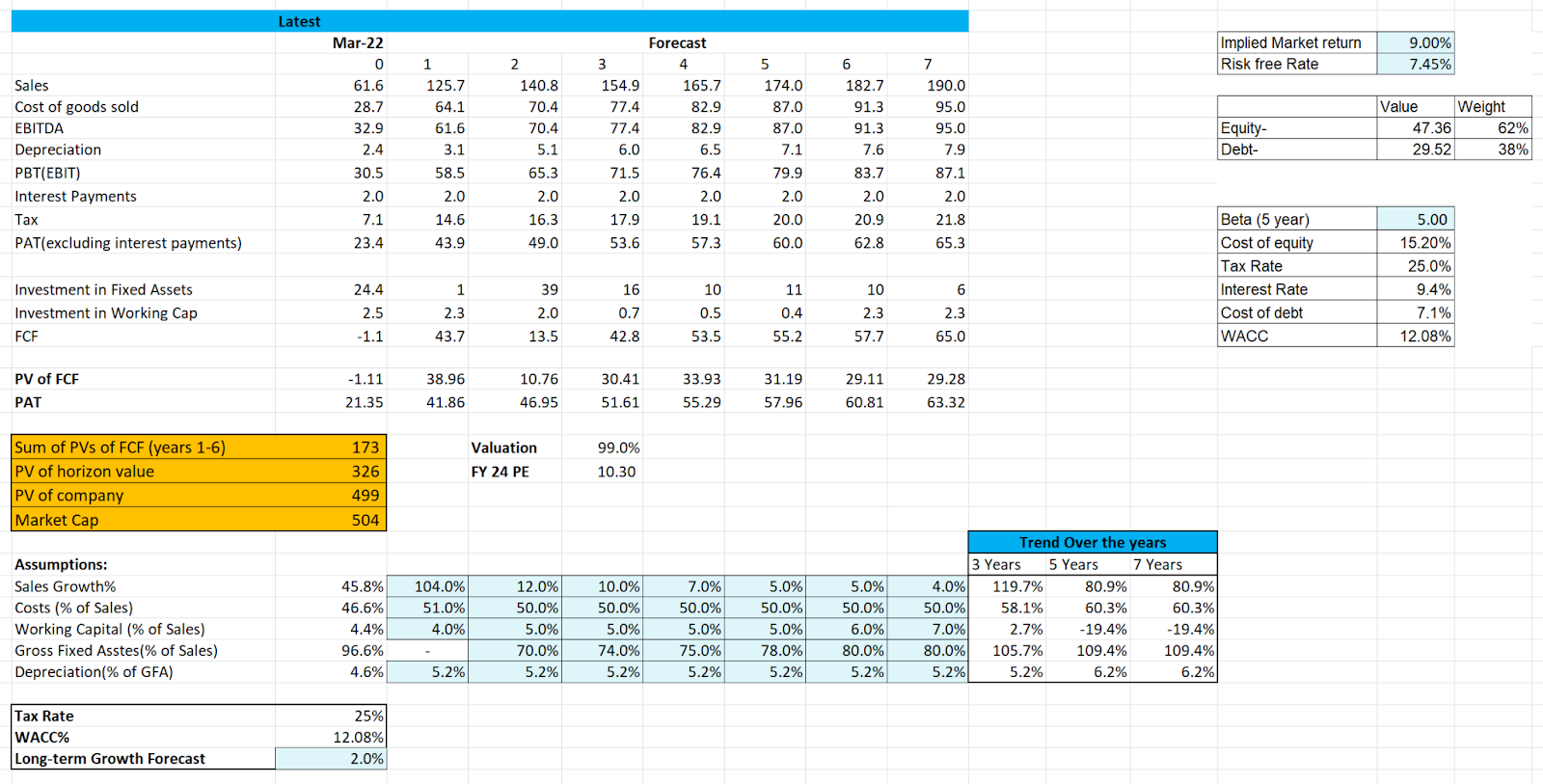

Rough DCF estimate-

In a base case scenario with medium to slow growth after this year, the company seems fairly valued. Any increases in receivables would harm FCFs but the company has not had such problems in the past.

I believe that any further upsides from their new JVs or fulfilling half their order book this year would result in the stock performing extremely well. Moreover, the domestic dredging and ports services space is expected to do well in line with upgradation of ports and waterways. The management seems financially adept, hungry for growth and is communicating openly with shareholders.

I request @sahil_vi, @Worldlywiseinvestors, @basumallick, @ayushmit, @Tar and any other members to please share your views on the company and ways to improve my research method and build conviction in investment ideas.

(Disclosure- Tracking, have not invested yet as it trades in lots of 750 shares, so need to be sure when I buy)