Are these tarrifs are common across all exports or wary from product to product. Need clarity on that?

Are these reciprocal tarrifs are on top of existing tarrif or not?

1 Like

Kitex MD Sabu Jacob, recons that the trump tariffs will boost Indian exports . Export heavy nations like China , Cambodia, Vietnam and Bangladesh has higher tariffs than India. So India should benefit .

From Manorama daily business page.

Disc: Invested with a tracking position

2 Likes

Trump “tariffs” may just be a tool for Trump Administration to force a discussion on other nations on reducing tarrifs on US goods. Recently I heard many countries like Vietnam, Israel etc. have reduced import tax on US goods to Zero. Should this not compel US to reduce reciprocal tarrifs on those countries and may not be that beneficial to India.

2 Likes

Yes. It’s an evolving situation . The tariffs are supposed to be a negotiating tool . India is also in advance talks with US for a bilateral agreement . The US president can change the tariffs upwards or downward for any country as per provisions of the tariff announced.

This is the benefit of engagging with different people with different mindsets. We always close our circle with india -us where as other nations also might be doing same or even better than us. We have to watch closely what other nations also doing. However one thing is clear industries which needed cheap labour or human intensified work can’t manufacture in US for sure

Don’t you all think this situation is still evolving? I came across a thesis that highlighted the importance of avoiding cyclical sectors like textiles. While India may benefit in the short term from higher tariffs on countries like Vietnam, we often overlook the bigger picture—if the US enters a recession and inflation remains high, overall demand could weaken, which would directly impact the textile sector.

4 Likes

Yes, I had considered this. Kitex is a textile company specializing in kids’ wear for children under two years old. Do we make purchases for these kids based on inflation or financial status? I believe that for children under two, clothing is more of a necessity rather than a discretionary purchase.Additionally, a significant portion of these purchases might be for gifting purposes. In that sense, Kitex is not purely a textile business—it operates in a segment where demand is relatively inelastic.

Furthermore, Kitex had planned an expansion in Kerala and had even purchased land for it. However, circumstances changed, and the expansion was moved to Telangana instead.

Kitex received significant incentives from Telangana, including:

- A 75% interest subsidy on loans

- Subsidies for ESI, PF, and GST

- Land at just 10% of the market cost

- Access to cheaper water resources

Even if tariffs pose a challenge, I believe these cost advantages provide Kitex with a strong competitive edge in the global market.(hoping)

The MD has stated that the current production facility in Kerala generates ₹100 crore in profit. If operations are shifted to Telangana, the profit could easily rise to ₹250 crore.

Whether staying invested in the company is the right choice—only time will tell.

Additionally, India’s textile exports stand at $30 billion, while China’s exports amount to $300 billion. This means India’s share is just 10% of China’s textile exports. The key question is: Can India capture 10% of China’s market share or expand into other countries?

Can Kitex expand into other markets like Europe, Australia, or even India?

Considering all these factors, along with the fact that I bought shares two years ago, I currently see no reason to exit my position. Again, time will tell.

I am deserved to be wrong because investment is a probabilistic game.

11 Likes

A Negotiation with Vietnam is on cards as per below news

1 Like

Came across this news article dated back in 2008, during the Great recession.

“Kohl’s and Wal-Mart reported that one of their few strengths in September was in children’s clothing. Kohl’s noted that purchases are ‘need-based’ and Wal-Mart said customers were ‘looking for basics for their families,’ while discretionary purchases were soft.”

Parents tend to cut down spending on their children as the absolute last resort, kidswear is to remain resilient during a recession. But regardless the current situation evolves into a recession or not, atleast in the short term we can see some impact on the margins.

8 Likes

Garment and toy manufacturers are ramping up capacity utilization during the typically lean April-to-September period—signaling a shift in production dynamics.

The huge capex planned by Kitex might just be perfectly timed, positioning the company to capitalize on this evolving opportunity.

5 Likes

Are we only better alternative for US for Garments exports?.

Before Covid hardly anyone know Vietnam but they catch the opportunity vey well China+1 and grow and we had so many narratives as super power but fact is we missed it. Is anyone else gearing up to catch this opportunity besides India?

We do have cheap labour agreed but what about near competetors?. what an edge we have over others?

How are we position with garments material?. do we have that supply chain integration which make us export ready?.

Welcome any Industry experts views.

1 Like

Kitex Garments primarily focuses on the manufacturing and export of knitted garments for infants and children.

When it comes to knitwear, India is a world leader - Tirupur being the Mecca of knitwear manufacturing. India had the manufacturing competitiveness here.

However, duty draw back was removed in 2018 by Indian Govt. and together with GST implementation, it created the unnecessary headwinds for the Indian knitwear manufacturers (GST was a factor here because quite a bit of work also gets outsourced to smaller guilds, which operated on cash. But after GST the unorganized sector was brought in to the organized frame, which eroded the cost advantage). As a result Indian manufacturers were left with very small edge. Important to note that in apparels industry the highest margins exist in engineered apparels, lingerie and kids-wear (relevant for Kitex).

Trump-tariffs, depending upon which way they go may create an edge for Kitex esp. relative to exporters from Vietnam and Bangladesh. It is a probable scenario.

I am one of the cofounders of foursource.com - a b2b apparels sourcing platform and have interacted a lot with the knitwear manufacturers.

Disclosure: Invested

5 Likes

The current change in tariffs make investing feel like driving on a road with ever changing traffic rules. Hopefully, the world will see a mean reversion to a more stable tarriff structure. With that perspective, we could invest in the long term but short term is anybody’s guess, especially now.

That said, the way the US is reacting to the stock market reactions, shows that we might ,hopefully, move to a more stable tarrif structure sooner than expected (fingers crossed).

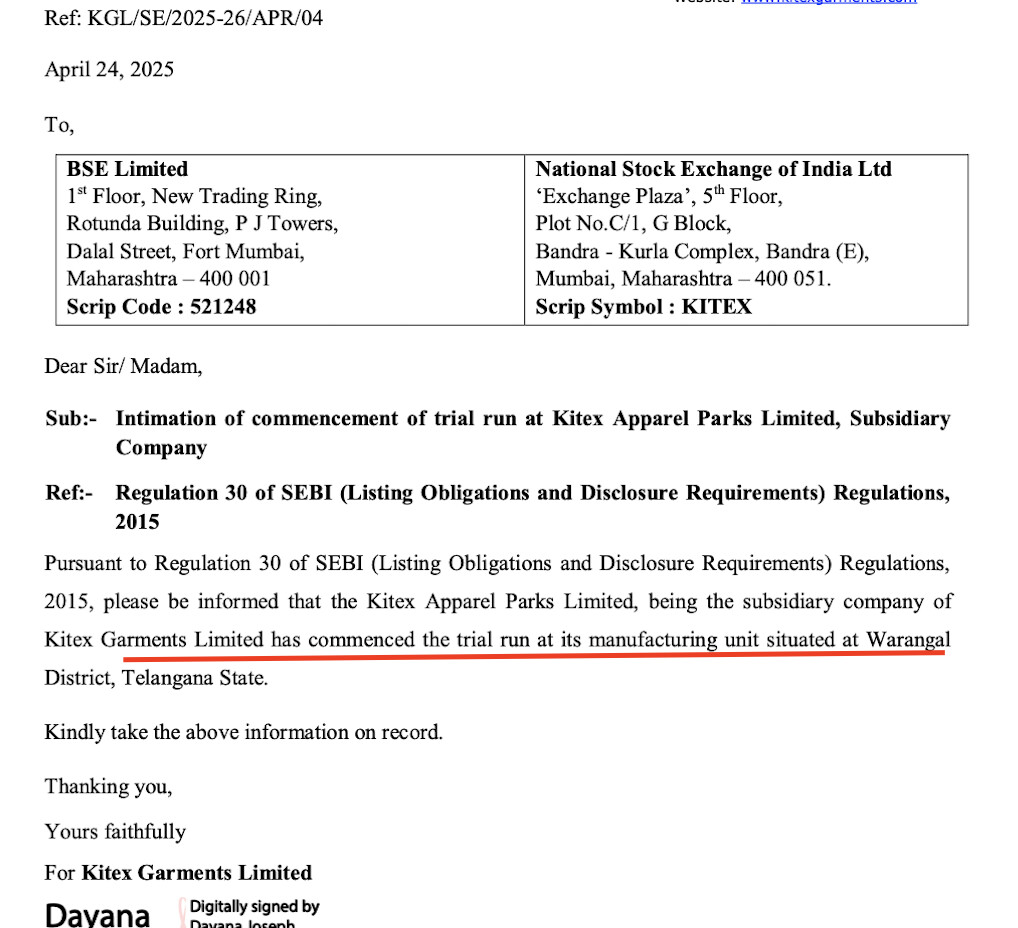

Here is a disclosure of the trial run at their Warrangal plant.

2 Likes

Few Updates from Investor Presentation Held on April 2025

-

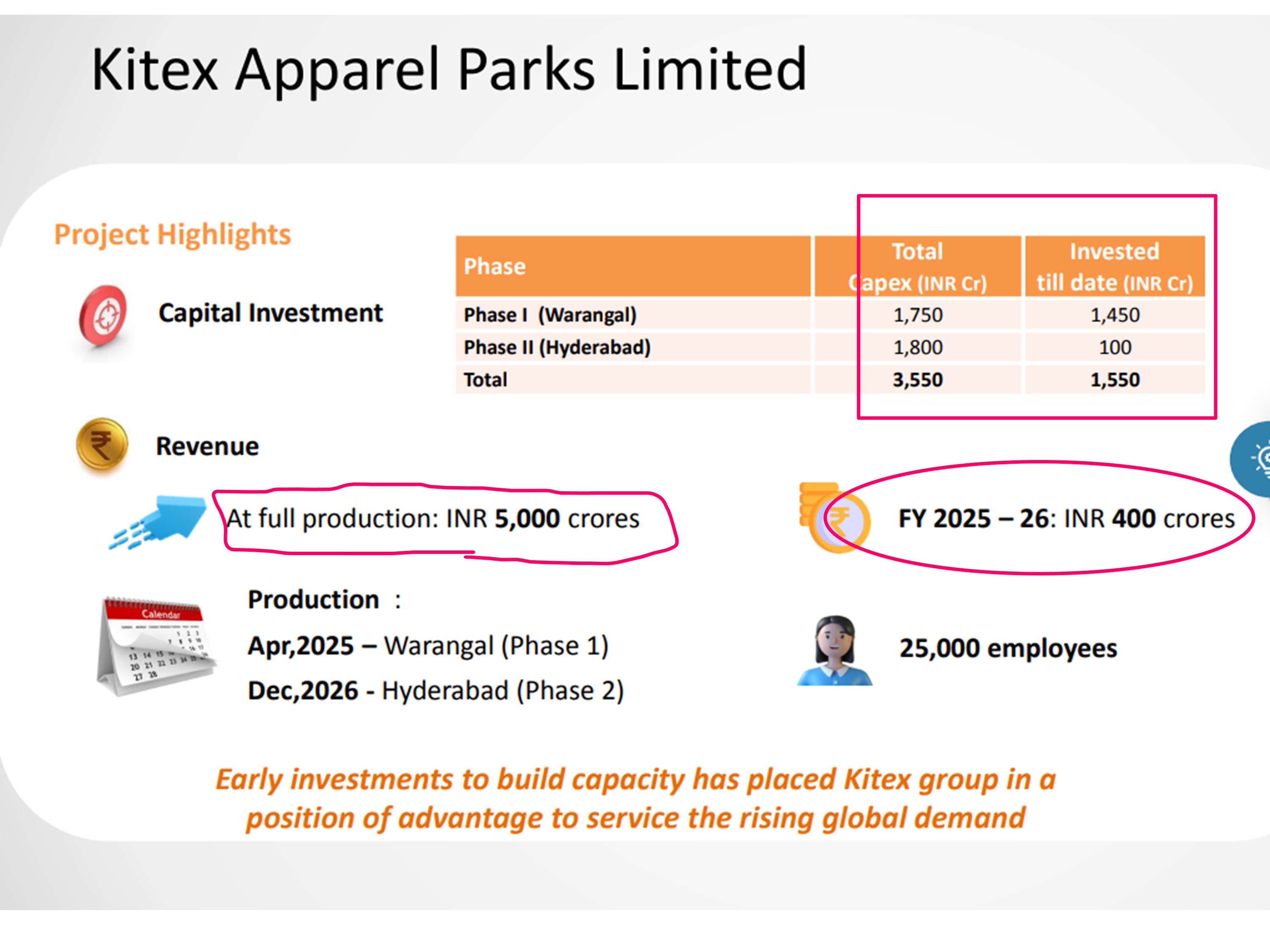

Phase I Warangal Plant Commenced:

Commercial production has begun at the Warangal facility in April 2025 under Kitex Apparel Parks Ltd (KAPL). This marks a key milestone in the group’s Rs. 3,550 Cr expansion project. -

Employment Impact:

Total direct employment from both phases is expected to exceed 25,000. -

Financial Outlook from Plants:

-

FY 2025–26 Revenue: ₹400 Cr

-

Full capacity potential revenue: ₹5,000 Cr

-

Capex Progress:

-

Warangal (Phase I): ₹1,750 Cr (₹1,450 Cr already invested)

-

Hyderabad (Phase II): ₹1,800 Cr (₹100 Cr invested so far)

-

Hyderabad Phase II Plant Timeline:

The Hyderabad unit is expected to commence production by December 2026. -

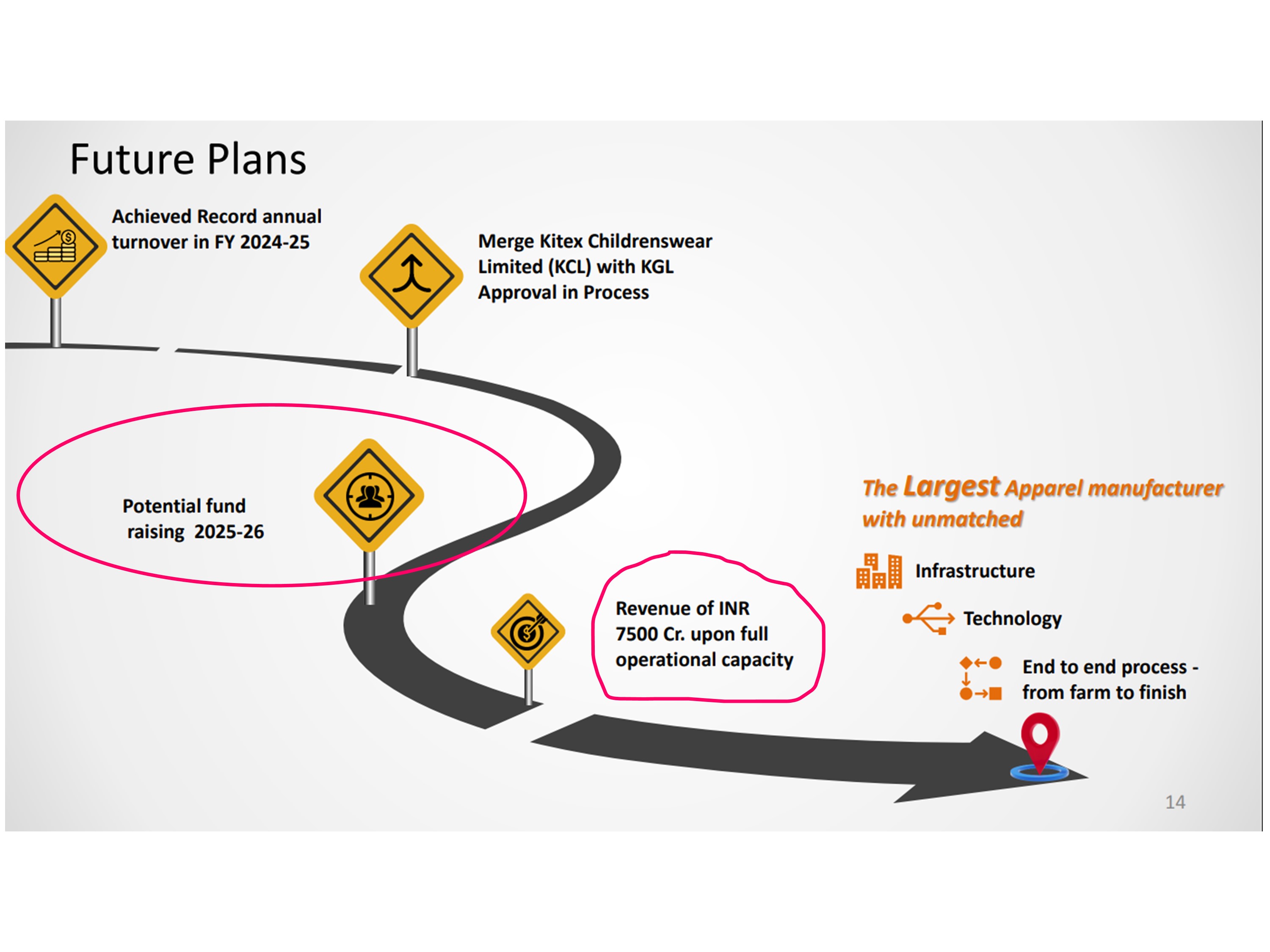

Merger Update:

Merger of Kitex Childrenswear Ltd (KCL) with KGL is underway. SEBI filings completed. NCLT process ongoing.

1 Like

My Observations from Recent investor presentation 2025 (Only Mine):

I have been closely watching Kitex’s actions over the last 4 years. During this time, they consistently spoke about funding their expansion through loans and internal accruals.

On the Expansion Progress:

- Warangal (Phase I) Capex: ₹1,750 Cr (₹1,450 Cr already invested)

- Hyderabad (Phase II) Capex: ₹1,800 Cr (₹100 Cr invested so far)

So, about 45% of the total planned capex has already been invested.

Important Change:

Now, for the first time, they are openly talking about raising funds for further expansion, which is a notable shift from their earlier stance.

My Views on the Fund Raise:

- Better Focus on Valuation and Governance:

Typically, companies aiming for fundraising give more attention to valuation and corporate governance. Earlier, governance was seen as a weak point for Kitex, but now things seem to be improving. We can see this through investor presentations and other proactive steps. This is a positive move for retail investors. - Debt Levels Likely to Stay Under Control:

Initially, they had spoken about ₹2,500 Cr of debt. Now, with fund-raising plans in place, a significant portion of the remaining expansion funding could come through equity. If the new entity achieves a valuation of over ₹8,000 Cr (based on current market perception), fund-raising should not be a major challenge. - Lower Debt Means Lower Interest Cost:

If debt is kept low, interest expenses will reduce, leading to improved profitability and healthier PAT (Profit After Tax) margins. - Impact of Government Subsidies:

They have mentioned earlier that they expect to receive 60-80% of the project cost back through subsidies.

Assuming a total expansion of ₹3,500 Cr and ₹1,500 Cr debt now, if they successfully raise funds and later receive, say, ₹2,500 Cr as subsidy refunds — it could be possible for them to completely repay all debts and become a debt-free company again.

(This is the single most important point I am eagerly waiting to see unfold.)

Disclaimer:

As always, I could be wrong — because investing is a game of probabilities and anything can unfold in the future.

I am not a SEBI-registered analyst. I am just a long-term (very long-term) investor who focuses on simple logic and basic calculations.

My approach is to maintain a peaceful, simple investment framework without overcomplicating things.

Invested around Rs 50 Range

11 Likes

Kitex is manufacturing Cotton clothing where as China is heavy on synthetic so no comparison

1 Like

Just reposting my Nov 1, 2024 post.

Can any financial expert work out future equity increase required after bonus issue?

You can get some input from page 2 of bonus filling done with exchanges.

Consider Telangana project cost @ 3000 Cr. Assume D/E ratio for textile industry.

Why my question…there can be QIP and/or right issue and/or Direct FII/institutional placement.

Disclaimer - Invested @ 4 year back, still holding.

MOST LIKELY THERE WILL BE QIP IN FY 2025-26.

1 Like

India’s textile exports to the UK, currently valued at $1.4 billion, are expected to double following the finalization of the Free Trade Agreement (FTA). The agreement will eliminate the existing 12% import duty on Indian textile products, significantly enhancing their price competitiveness in the UK market.

3 Likes

Hope to see a similar agreement signed with the European Union, so that India can better compete with Bangladesh’s dominance in textile exports.

3 Likes