Exited kitex today. Peak margins . It would not increase from here. Plus depreciation and interest cost won’t let the profits grow. Plus tariffs coming from USA

5 Likes

Gadi shuru ab hue he aue apne exit kar diya ![]()

![]()

![]() , 7000 cr max sales they can do and operating leverage just started and ur saying max opm:joy:

, 7000 cr max sales they can do and operating leverage just started and ur saying max opm:joy:![]()

![]() interest and depersonalisation will be there but its effect will be negligible upfront too the operating leverage, and last usa tarrif lagaya ga to 1$ ke cloth 5$ ko lene padegneg as its a labour heavy business, understand the business and take decision,

interest and depersonalisation will be there but its effect will be negligible upfront too the operating leverage, and last usa tarrif lagaya ga to 1$ ke cloth 5$ ko lene padegneg as its a labour heavy business, understand the business and take decision,

Invested may be biased

3 Likes

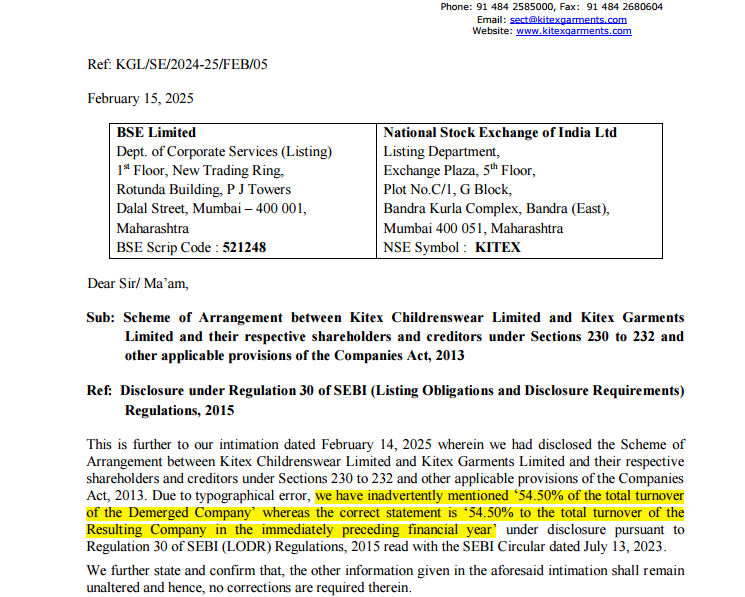

A correction in the disclosure from the company regarding the demerger. The entire Kitex Childrenswear Business is being demerged into KGL and not just 50% of it.

1 Like

What would be the interest payment in FY26? After reading ICRA report, can it be assumed that the PnL hit due to debt will be additional 12cr in FY26 over Fy25?

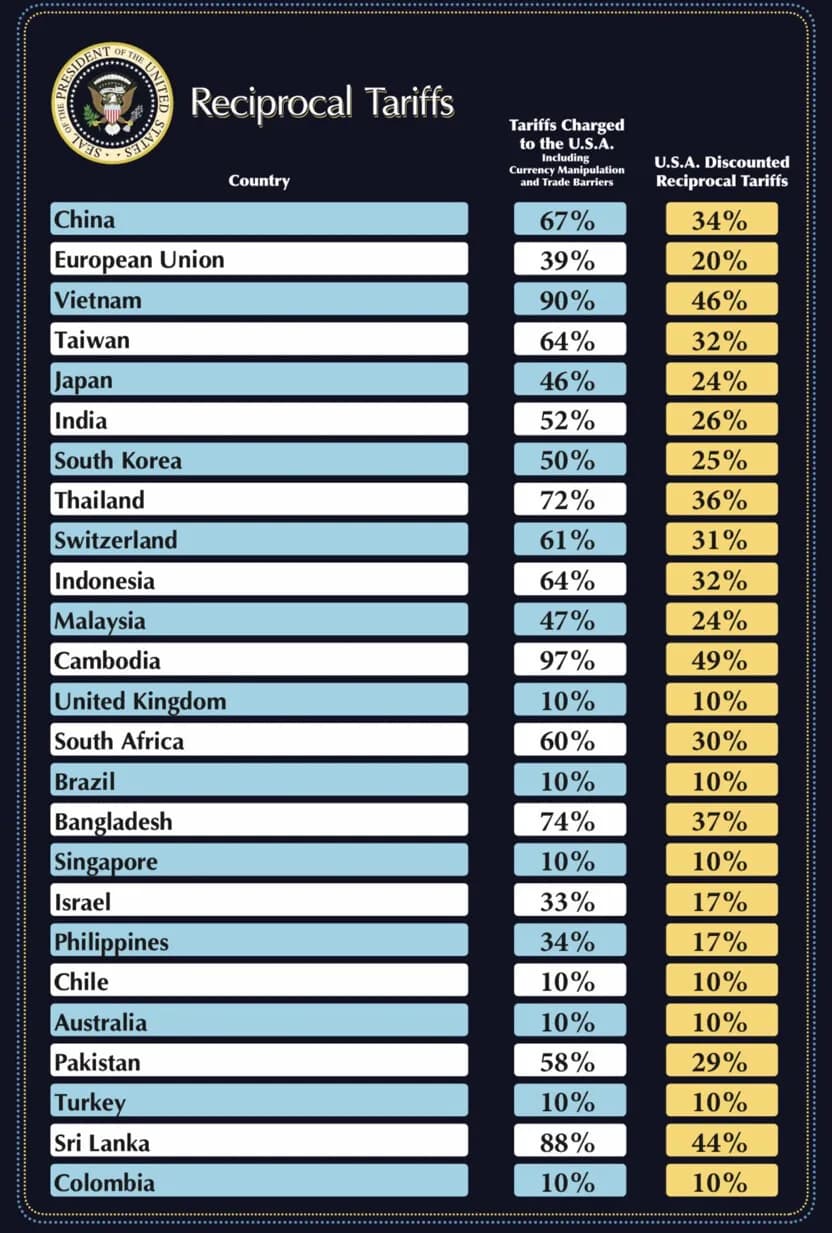

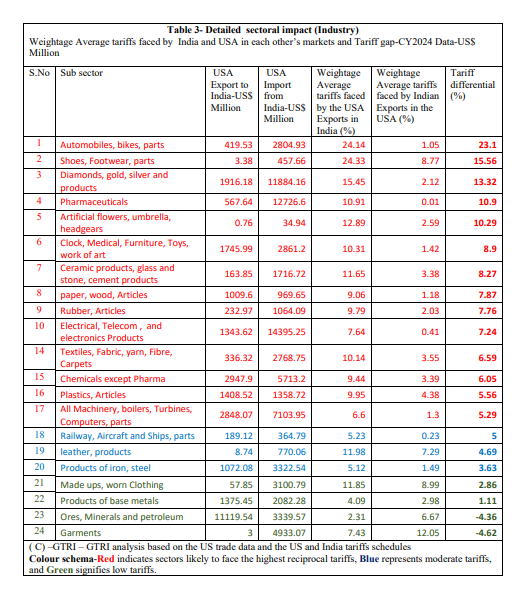

This says India and USA tariff is almost similar and TRUMPH impact may not affect much on textiles.

So kitex may be safe

4 Likes

Yes, Kitex is in position to encash opportunity. They have latest machines with huge capacity, just in time expansion.

1 Like

It’s pretty hard to pin down whether something is good or bad for Kitex at the moment because of constant change in tax/tariff policy in the US. Perhaps, best course of action is just to sit tight for the next four years and hope for some stability in the near future or after four years. My guess is that it is not going to be smooth sailing for any company including ones in the US.

This zen story fits the situation perfectly.

4 Likes

Could you share your opinion on meger of textile division of KCL into Kitex garments ltd…

People were discussing corporate governance issues at Kitex, and one of the concerns raised was related to kitex childrenswear , a private company that was set to be acquired by the listed company.

Before investing, I downloaded the financials and observed that the profit percentages of both companies were almost similar. I was not convinced about the corporate governance issues.

Now, with the acquisition of Kitex Childrenswear, I see this as a positive move.

Dis: Invested from the ₹50 range (post-bonus adjustments), focusing on business expansion. My views are very long-term more than 5 to 7 years.

1 Like

You must has seen its Accounts Receivable > Net Profit every year, its very scary for me , what is your view on that as for me its a red flag for any company

: image.png…

Comparing accounts receivables with net profit may not be appropriate, as it depends on factors such as profit margin, working capital cycle, and asset-light business models etc

However, comparing net profit with cash flow from operations is essential, and cross-checking with an age-wise analysis of debtors can provide further insights according to me.

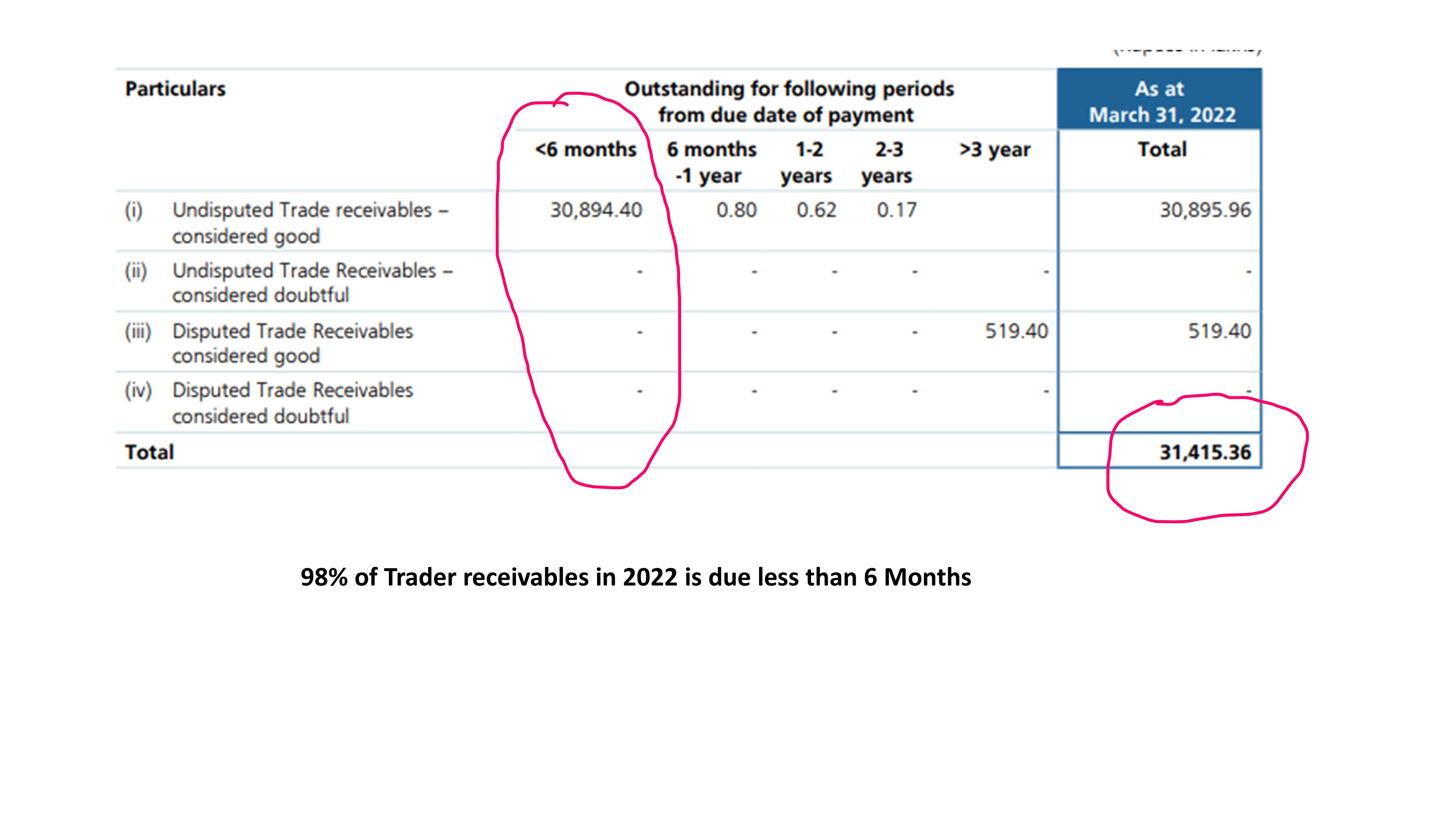

I have done the following 2 analyses (when i invested 2022/2023)

a) The net profit over five years is almost equal to cash from operations

and

- "98% of debtors have outstanding balances for less than six months.

Dis- “These are my personal views, and I acknowledge that I could be wrong and I invested around the 50 range (bonus-adjusted price).”

4 Likes

Thank you. Appreciate your reply ..Cash flow for five years definitely giving better picture

1 Like

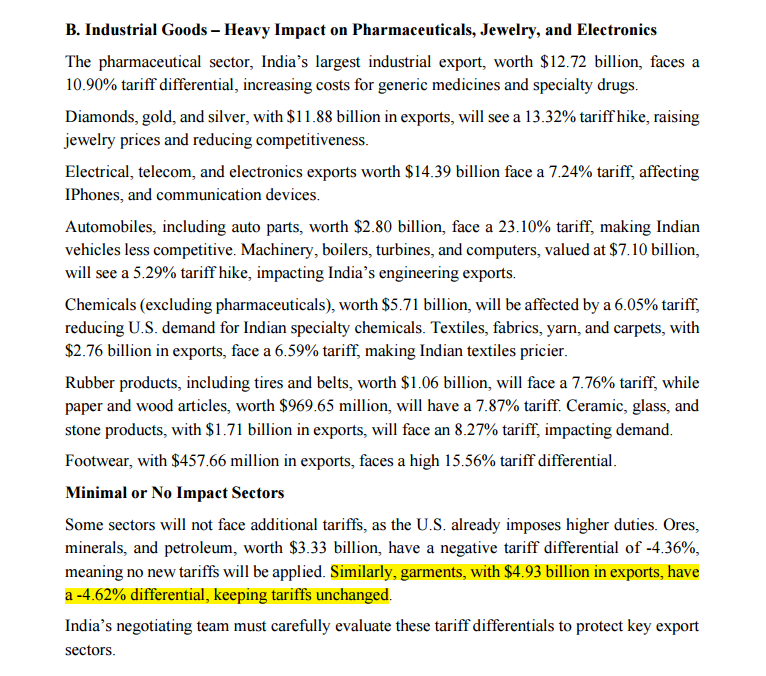

Global Trade Research Report suggests no implication of increased tariffs on the Garmenting sector since the reciprocal tariffs are to be implemented only on Indian sectors that have a high tariff differential with the USA.

The higher the tariff gap, the worse affected a sector will be.

Meanwhile, the Garmenting sector in Bangladesh continues to face severe crisis due to the interim regime’s lack of support.

3 Likes

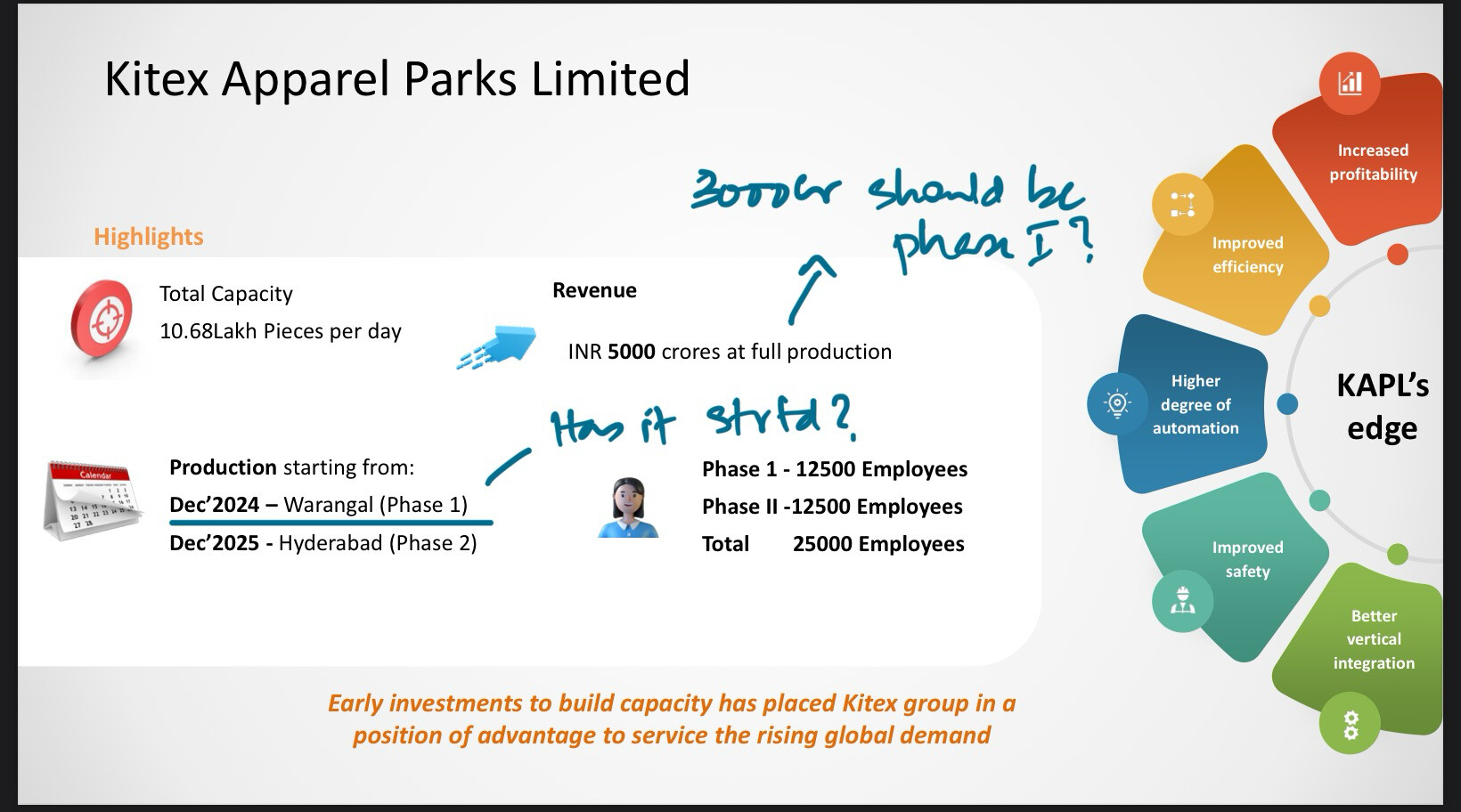

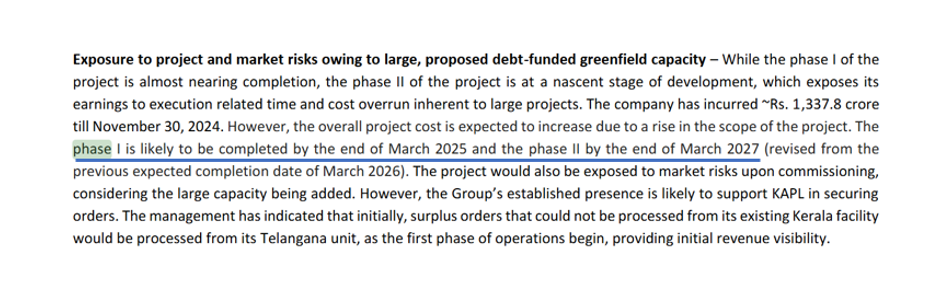

Kitex was supposed to launch their Warangal facility by December 2024.Not able to find any update regarding the same given to exchanges . Does anybody have any updates on the same ?

This is from Presentation post Q2 results.

Disclosure : Not invested

Phase 1 likely to be completed by end of March 2025. This is from a rating update note.

So we should wait for an update by April 1st week.

1 Like

12 Likes

Good to see

Also new technologies in production line

35 lakhs capacity is massive compared to current 5 lakhs

Looking for

- execution

- expansion of 2nd plant

- Govt subsidies

Dis : invested 2 years back

2 Likes

Updates post the 25k recruitment ad in business page of Malayala Manorama daily .

-

Warangal plant started trial production . Now reached 15 tonnes / day.

-

Planning to reach 170 tonnes / 22.6 lakh dresses per day after both Warangal and Sitharampur plants get fully operational.

-

Currently in Kerala they produce 35 tonnes / 9 lakh dresses / day. Kerala used to employ 11k workers . They have reduced 2k out of it so far.

-

Out of the 25k employees for Warangal , 16k is for sewing with 80% female positions. The plant is most modern hence require qualified technicians too.

-

Proposed capex is ₹3400 cr for both the plants put together .

-

Telangana govt has given free land, power , subsidies etc.

- These are points given in the business section, just reproducing here post translation. Ideally these should have been filed to exchanges .

Disc: Not invested. Actively tracking

11 Likes