Kitex is expanding again?

Today, Andhra Pradesh’s Textile Minister personally visited Kitex HQ in Kochi, inviting them to invest in the state. Kitex MD Sabu Jacob has agreed to meet the AP CM in two weeks.

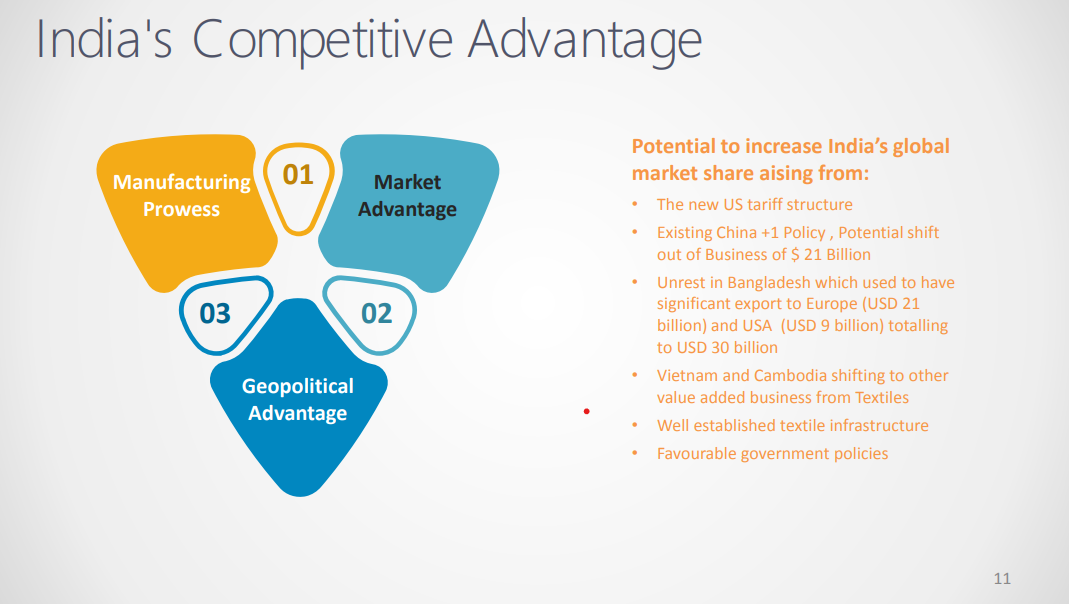

Opportunities for Indian Textile Manufactures

India’s textile exports are at $16 billion with almost full capacity utilization. Compare that to Bangladesh at $56B and China at $150B — it’s obvious that India has a long way to grow.

With FTAs (UK done, EU expected), geopolitical concerns in Bangladesh, and Western over-dependence on China, India’s textile industry stands at the edge of a new growth cycle.

Kitex Move - Massive Expansion with QIP ?

Kitex seems ready to seize the moment. Their recent investor presentation suggests a QIP (Qualified Institutional Placement) is preferred over fresh debt. That’s a welcome change — dilution for expansion is a healthier route, and shows Sabu is finally aligning with capital markets.

Finally, Focus on Valuation and Minority shareholders?

Till now, I hadn’t seen him show much concern about stock valuation. But it seems he has now realized its importance — possibly why he is merging Kitex Children’s Wear with the listed entity and considering the QIP route.

Can QIP and subsidies together pay off all the debt incurred for expansion?

Kitex was a debt-free company prior to this expansion. Now, the company is exploring QIP and a combined investment plan. As per the MD, they are eligible for a subsidy covering 50–60% of the total investment.

Then same can be used to repay the current loan??

If that happens, it would be a remarkable boost for the company’s valuation

Conclusion? Very promising times. Let’s allow the management to perform — and remain long-term investors.

Dis - Invested when P/E was 10 and Market Cap was less than 1000 Crores.

Ohh Quite Surprise.

Really another expansion??

Massive opportunities for Indian textiles, and the government is very keen on seizing them

Dis: Investor 3 years back..

keeping a sleeping mode

Buyers moving away from Bangladesh are likely to place new orders with Indian firms.

Tarrif on India is not yet finalized so I don’t think US vendors are in hurry to make any swift decision. We should also see India is not only alternative to Bangaldesh in the world. If you have data you can share what persentage of export increased for past one year from US. Only data can tell whether what we are so optimistic is it even real or a spade of cards.

@bijo_scaria Sir why is falling rapidly sir consecutively 3 lower circuits even though the current environment is positive for textile industries and export data of Kitex is also good any information we missing sir. Thank you in advance.

I don’t have any short-term views, and I don’t really understand the technical side of investing — so no views from my end. I’ve seen both ups and downs many times over the last three years since I made my bet.

For example, when I bought the stock (around ₹50 adjusted price), it almost doubled and went up to ₹100 in 2022. Then it fell back to the ₹50 range, moved up to around ₹90, dropped again to ₹60, then shot up to ₹300, corrected to ₹160, climbed again to ₹320, and now it’s back at around ₹240.

What did I do through all these ups and downs? Nothing. I see the company is expanding, and I’m quite happy with that.

While others may see multiple swing trading opportunities in this, I strongly believe real wealth is created through long-term bets. When we start a business, we don’t think of swing trading every few weeks. I like to keep it simple.

Disclaimer: I am not an expert, nor am I a SEBI-registered analyst. I could be wrong. But with my entry price at ₹50, I’m happy and have no plans to exit for the next couple of years

The 25%+ tariff on textiles might cause some strain for Kitex as well ..

Some news sources say Kitex generates 70% of its revenue from the US. But, on the flip side the markets and major index like SENSEX and NIFTY are ignoring the 25% tariffs assuming a India-US bilateral trade deal is in the works and will soon be announced in a month or two. So, the markets think this is a temporary pain point.

Kitex Garments, which earns 70% of revenue from the US market, fell 4%. Shares of KPR Mill and Vardhman Textiles also fell around 3% each.

“With a 25%+ tariff, India could now be relatively disadvantaged vs. some of the competing countries” including China (30% tariff), Vietnam (20%), Bangladesh (36%), Indonesia (19%), and Pakistan for home textiles, Jefferies noted. The analysis warns of demand destruction as “exporters will have to bear a part of the cost and there could also be end-user demand destruction due to price hikes.”

Mayank Jain’s assessment was equally stark: “The textiles, gems, and jewellery sectors, all of which are highly dependent on US demand, are bracing for significantly negative effects in the near term.”

Read more at:

Regardless of the tariff rates set between India and the US, both economies are resilient and will adapt over time. While there may be short-term, sector-specific advantages or challenges, entrepreneurs and businesses on both sides will continue to find ways to collaborate and grow.

Tariffs, in general, are not ideal — neither for India nor for the US — especially in today’s interconnected, global economy where isolation is not a viable strategy. What markets dislike most is uncertainty. Once clarity is provided, even if the tariff is set at 25%, markets are likely to factor it in swiftly — possibly within this week itself.

Moreover, 25% is viewed as the worst-case scenario. It is highly probable that the final trade agreement will settle at a lower rate, which would be seen as a relief by market participants.

Regarding Kitex Garments, the company had already demonstrated market strength well before these tariff discussions intensified. There’s no need for concern here. The key question now is whether Kitex can grow its EPS in both the short and long term. Given the company’s strong fundamentals and its status among India’s leading exporters, the answer is yes. Early indicators suggest a robust performance in Q1, and upcoming results are likely to reinforce confidence in its growth trajectory.

Remain patient and watch for Q1 earnings. Kitex is well-positioned, and macro noise should not overshadow its strong operational performance.

Board is meeting on 4th August to consider raising of funds and quarterly results

So, hopefully, the tarriffs never arrive. However, if they do, several companies in several countries will go under and these manufacturing capacities won’t be created in the US either. This will be loss-loss situation for everyone involved? Near future doesn’t look rosy.

Kitex is now planning to sell its Little Star brand in India as well, which until now was available only in the US. Known for its high quality, Kitex will not only benefit Indian customers but also strengthen its own position in the market.

Kitex has has orders booked until the end of December and is targeting ₹1,000 crore in sales within India . Exports to the EU are also on the rise.

This interview is in Malayalam. Turn on auto translate in Youtube for English/Hindi subtitles.

So Kitex has a 90% revenue coming from export to USA. With the tariffs in effect this will severely impact the company, is it a good time to invest or its better to stay on the sidelines.

Which apparel company should Kitex try to emulate as it gets into retail in India? Uniqlo? Zudio? Jockey/Page? Doesn’t retail business require different core competence than being a manufacturer/supplier? What makes an apparel company successful in India? Seems like tough times ahead for the company if the current tariff regime persists.

A possible outcome of the current tariff regime in the US would be a diversified customer base by region for Kitex.

Any improvement in the tariff situation would be a bonus for the company at this point.