Can someone please help me understand how the company is paying such low interest on loan? B/S shows 870 cr. of long term loan but only 3 cr. as interest payment. I read something related to 75% loan subsidiary from the Govt. of Telangana, but couldn’t find any details regarding it to fully understand.

1 Like

Term loan (600Cr) from Banks was taken during the financial year 2023-24 and interest is chargeable at six months SBI MCLR Rate (7.7% to 8.45%). The loan is repayable in 28 quarterly instalments starting from October 1, 2025.

2 Likes

The loan will be mostly for new projects in Telangana. Normally, loans accumulated interests are capitalized during construction period.

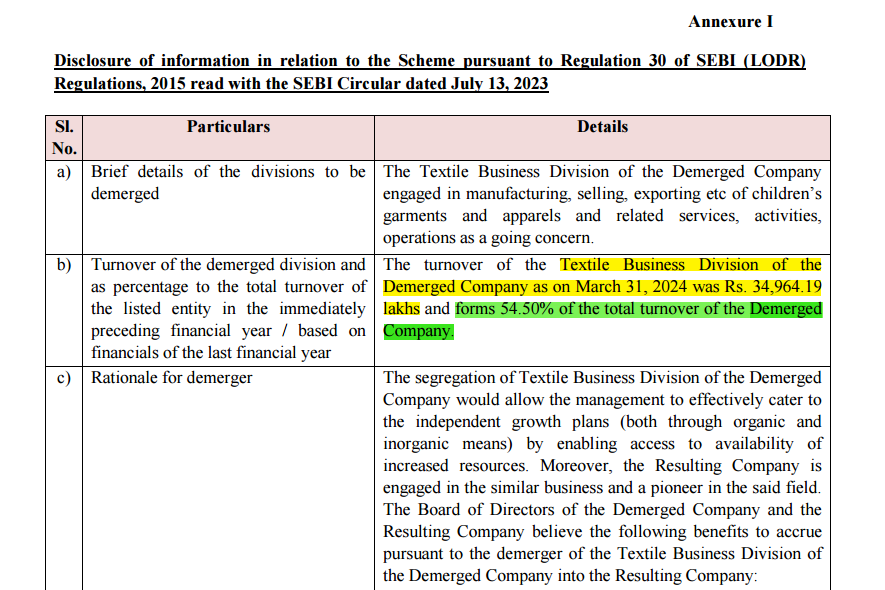

Further development from Kitex - https://www.bseindia.com/xml-data/corpfiling/AttachLive/be0388ff-f3dd-451c-ad6c-a8522351a379.pdf

The news flow is likely indication of QIP or right issue in future.

2 Likes

why company is not focusing on domestic market share it will further boost company’s revenue .can anyone have a reason why company is not focusing on domestic market & one more thing i would like to mentioned about subsidy by the government it will impacted if there is rulling party change

Another positive development for retail investors and the company’s valuation is the bonus issue

It appears that the management has recognized the importance of increasing market capitalization.

While the exact reason for this move is unclear, it could be due to several factors:

- Attracting larger customers

- Seeking private funding

- Promoter dilution, etc.

The best investment returns could come from price re-rating combined with business growth (a Value plus Growth Strategy).

The first phase—price re-rating—seems to have already occurred in Kitex. Next, if the company can deliver sustained business growth, the stock has the potential to multiply.

Disclaimer: Invested in the range of ₹150 to ₹200. These are my personal views, and my investment perspective is, of course, very long-term oriented.

cfdc3c26-b494-491b-a026-a5083ee85f00.pdf (275.1 KB)

2 Likes

Bonus declared, 2 shares for 1 held.

File_1732258411024.pdf (375.5 KB)

1 Like

Can any financial expert work out future equity increase required after bonus issue?

You can get some input from page 2 of bonus filling done with exchanges.

Consider Telangana project cost @ 3000 Cr. Assume D/E ratio for textile industry.

Why my question…there can be QIP and/or right issue and/or Direct FII/institutional placement.

Disclaimer - Invested @ 4 year back, still holding.

1 Like

After bonus share 13 crore will move from reserve of 1000 crore to equity capital. Company is taking loan around 2400 Crore. For that loan company having enough capital adequacy. When you combine Kitex garments + Kitex childrens capital I think combined equity will be more than 1500 Crore.

Loan already have been sanctioned my SBI as lead banker

Disc - invested around 150 to 180 Range when company was 1000 crore seems their share price will cross 10,000 crore within next 5 year

1 Like

What are the risks to Kitex in the near future? Will the Trump govt be a drag on the company’s revenue?

4 years back trump was the president. Did not see that issue in fact that time company market cap touched 5000 crore.

Dis - Risk is part and parcel of investment game

1 Like

How bonus issues helps in any of these things?

It was another one

What I meant by reading their few of the last activities these things may happen

- Major one was merger of kitex garments and kitex children’s

- Bonus issue

I don’t see much impact for second one

Even though few people especially retail will buy small value shares.

Bonus issue may create more number of shares in the market.

2 Likes

Kitex telengana factory will start operation in December also one more factory construction is underway, once it starts production there will be significant increase in production.

1 Like

Trumps reciprocal tax on India… will it hurt kitex profit margins… any comments? as US is biggest customer for kitex.

Yes, I was thinking about this. Since my view is very long-term, I’m not overly worried. The stock has risen almost 5x, and considering their growth plan, I believe management must have some strategy in place, especially since the company has been in the market for the last two decades.

Also, during Mr. Trump’s presidency from 2016 to 2020, Kitex recorded its highest turnover and PAT (Profit After Tax), and the share price reached a record high as well.

Today, I saw a prominent businessman from the textile sector make some comments about Trump’s proposed tariff hike on products imported by the USA. He mentioned that if this happens, India could be a beneficiary because Trump is likely to target Chinese goods aggressively (a point Mr. Trum reiterated many times). His view was that this scenario could somehow benefit Indian textile players. However, he also suggested that Trump might consider the impact on US inflation and may not take such a bold step, indicating this could be part of a strategic mind game.

Indian textiles export v/s China (2023 - 2024)

India - $35 Billion

China - $ 293 Billion

India’s textile exports are only 10% of China’s export market. If India manages to capture segments of the market currently dominated by China, it would be highly beneficial for Kitex as well.

Nevertheless, I don’t want to make any predictions—it’s simply not possible at my level. Even so-called expert economists, despite having access to extensive data, often fail to predict accurately (as seen recently with GDP growth forecasts of over 7.5% versus the actual 5.4%).

6 Likes

One more consideration with regards to tariffs on textile industry is that US can’t possibly try to encourage textile manufacturing in the US as opposed to outsourcing its production to countries with lower cost of labour. How will a tariff on textile industry help the US rather than hurt its consumers? Some would argue that all tariffs end up hurting the consumer but in the case of textiles and apparel manufacturing, it will be worse than say semiconductor or auto manufacturing.

My guess is that tariffs on textile and particularly apparel manufacturing makes very little sense and therefore unlikely to affect Kitex Garments.

On a sidenote, here is the latest ratings update on Kitex Garments Ltd.

Here is a report on garment manufacturing published in 2020.

3 Likes

Patagonia is a unique apparel company. Would be good for Kitex to follow in their footsteps? What are some of the USPs of Kitex?

You are right, any labour intensive industry will not get affected. It is simply not possible to manufacture in US.

2 Likes

Any idea on why there’s such an increase in other expenses in Q3FY25 results. Looks like they have written off investments in the US subsidiary, but the statement given for the same below standalone results looks confusing.

Any views on this?

Disc - Invested