India’s textile industry is experiencing significant growth due to the uncertainty surrounding Bangladesh. This is beneficial for Indian textile companies. Bangladesh has achieved remarkable textile export figures over the years. In Q1 2025, Bangladesh’s textile exports were $10 billion, while India’s were $4 billion. Bangladesh’s exports were three times higher than India’s. Bangladesh gained this advantage due to its free trade agreements with the EU, USA, and Australia. I think a similar shift is happening in the textile sector now, like what we saw in the chemical sector.

Coming to kitex, Their massive expansion seems to have come at the right time. They are increasing production fourfold, from the current 5 lakh units of kids’ wear to 20 lakh new units at the new factory in Telangana. I believe they won’t face significant demand issues for the new factory, as the MD mentioned two years ago that they had already secured 8 new customers for material supply. Additionally, the uncertainty in Bangladesh and the expiry of their free trade agreements in 2027 will likely boost the demand for textile companies.

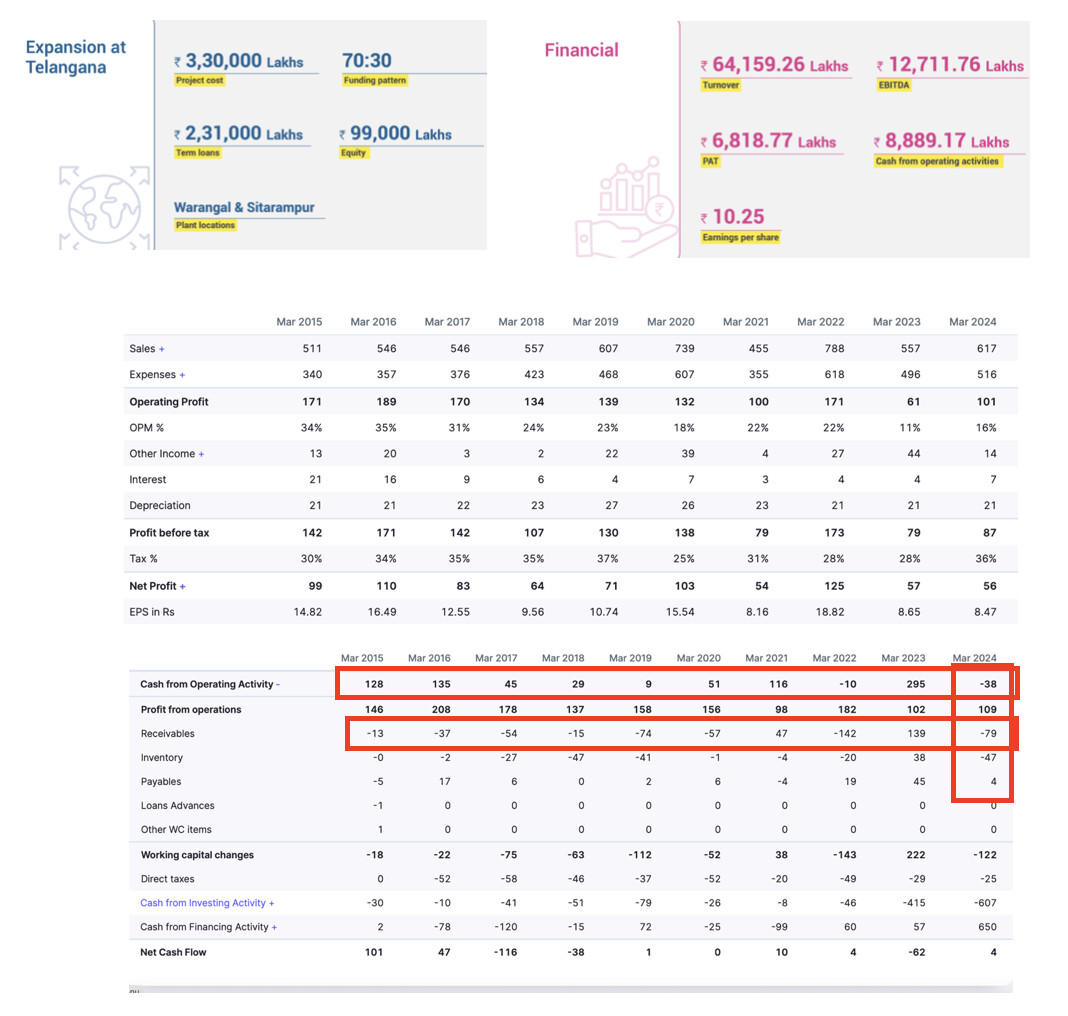

MD said that if the current factory were in Telangana, he would have made an annual profit of ₹250 crores, compared to ₹100 crores in Kerala. Additionally, the significant incentives for setting up the factory in Telangana, as opposed to Kerala, are expected to positively impact the company’s bottom line.

I am of the opinion that when a company can demonstrate real profits in its bottom line, the share price can rise, and the P/E ratio can be re-rated, even if there are some governance issues (such as the MD’s involvement in politics). As long as the business generates solid profits, I believe the share price will increase, and a P/E re-rating will occur. of course i am deserved to be wrong.

Disc - Invested from 150 level. views are personal.

MD said that if the current factory were in Telangana, he would have made an annual profit of ₹250 crores, compared to ₹100 crores in Kerala. Additionally, the significant incentives for setting up the factory in Telangana, as opposed to Kerala, are expected to positively impact the company’s bottom line.

I agree with the macrotrends, but I dont want to take his numbers at face value. He said those things during the time of Union protest and at the peak of his fight against CPM. He claimed that Telangana gave the land for free and was praising them, but you could see a quid pro quo after the electoral bond reveal - (25 crores from Kitex Ltd. and 25 crore from Kitex Childrenware Ltd)

A comparison of PAT v/s net cash operating activities

Kitex Garments 2019 2020 2021 2022 2023 2024 Total

PAT 71 103 54 124 57 56 465

CASH from operatiions 9 51 116 -10 295 -38 423

Based on the data, I don’t see any significant red flags suggesting profit manipulation, except for an investment in Kitex USA LLC, an associate company, amounting to ₹27 crore, which has impairment triggers but has not been written off in the books.

However, I don’t believe this sum poses a serious threat to the company’s existence or its ability to continue as a going concern.

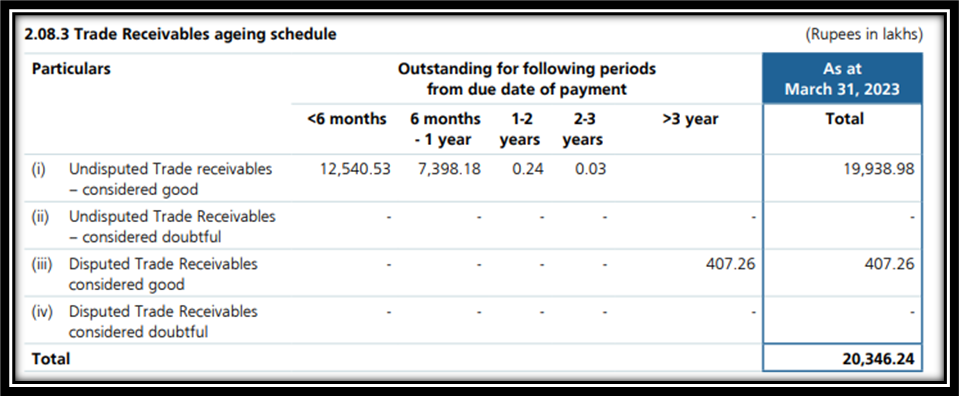

Additionally, a review of their trade receivables shows that they are within a reasonable range, further supporting the stability of their financial position.

I m invested since 2016 - there were issues of tussle with govt … and then there were issues of Sabu joining politics and then there were issues of pollution control board of kerala too… and then the orders were slowing down a lot… Toys R US stores went bankrupt… so these are headlines i can recall top of my head… issue is the order book… whatever sabu projected in the past never came true… now too with newly added capacity… i m nt sure how/where the new orders are coming… only thing now i m hoping is… US interest rate cuts… as kitex is major supplier for US.

But, kitex has very low equity base so if price jumps its very quick …

ON a valuation (Not considering Sabu’s proposals) average profit for the last few years say 70 crore from current project and Sabu say’s 3000 crores from new plant say 200 crore profit. Round to 250 crore on a P/E of 5000 Crore Market cap? by forgetting sabu’s comment instead what he delivered in the recent past was by valuation.

They did more than 100 crore on fixed assets of 240 cr. Now the capex is 3000 crore, so on peak capacity utilization and margin one can expect around 500 cr atleast by Fy26-27

) revenue of Rs 1000 cr by this FY

2) Revenue expectation of Rs 5000 cr on full potential

3) labour and water cost to reduce in Telangana

4) subsidy on capex

5) short term opportunity emerging from China and Bangladesh is 15 billion usd

6) long term opportunity estimate is 97 billion dollar

Awesome… Sabu was talking expansions and commitments from 2017 now it is going to become a reality. 5000 crore turnover into 20% PAT with a PE of 30 - 30,000 crore market cap. My expectation company will pass 5000 crore.

Kitex and Raymond are both into niche garment players in India. Both of them are saying huge tailwinds awaits the sector. May be a 10 bagger opportunity in next 3-5 years