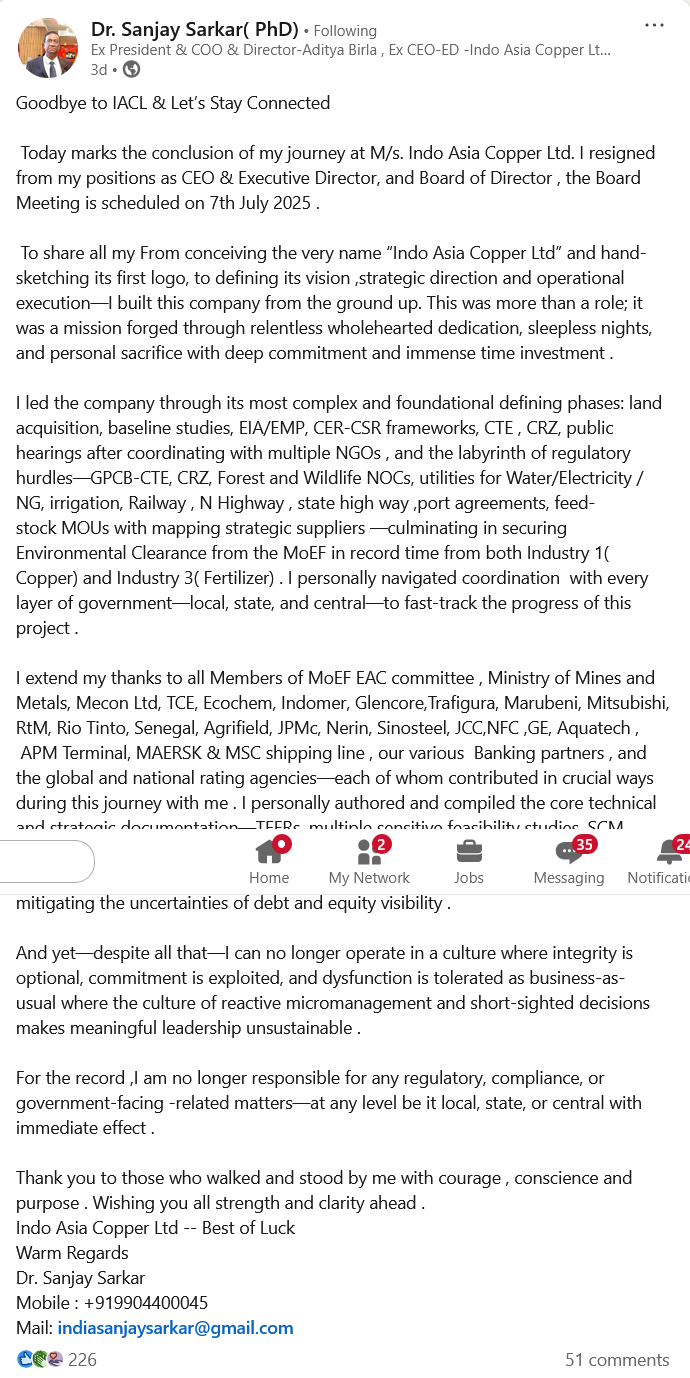

Based on his recently updated profile bio (screenshot attached below, referred below as Post 1) on LinkedIn and the above shared post (Post 2) by Dr. Sanjay Sarkar, allegedly (as no confirmation has been received from Kiri) outgoing CEO and Executive Director of Indo Asia Copper Ltd. (IACL), it’s evident he undertook a comprehensive array of activities to bring the integrated copper and fertilizer project to fruition. His statements indicate significant progress on the technical, regulatory, and contractual fronts, but also clearly state that financial closure has not yet been achieved.

Here’s a compiled report that helps understand his stated activities and helps us understand the risks that his void may create if not appropriately filled :

Detailed Report on Project Activities by Dr. Sanjay Sarkar for Indo Asia Copper Ltd. (as per his claims)

Project Overview:

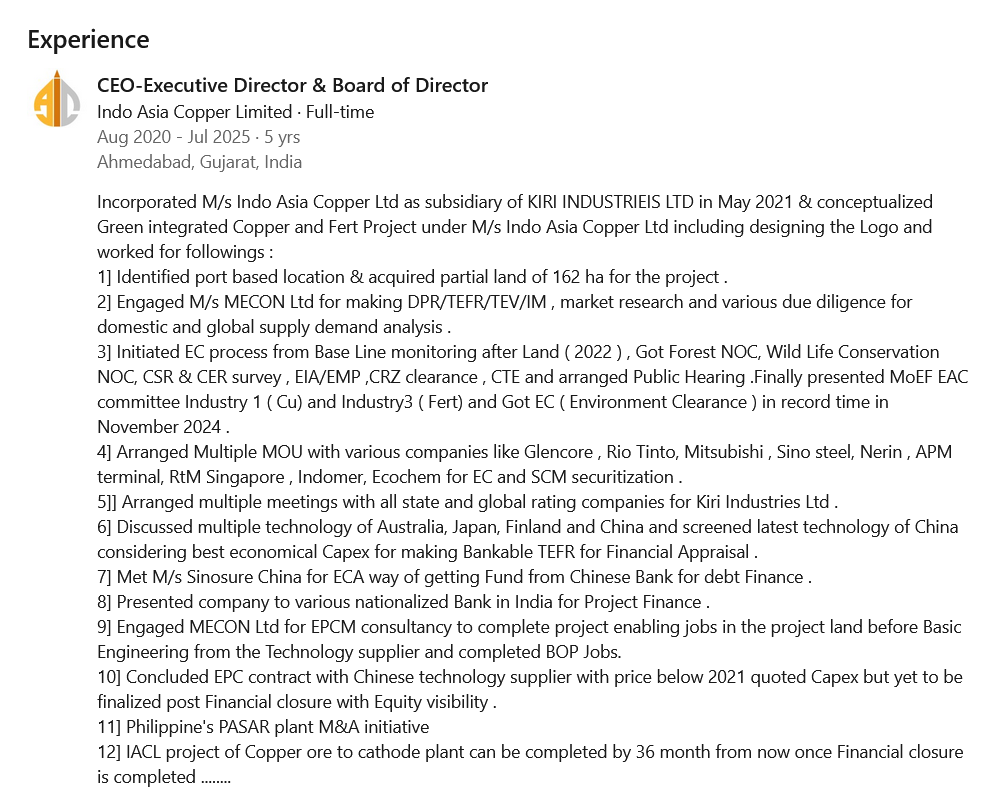

Dr. Sanjay Sarkar initiated and conceptualized an integrated Green Copper and Fertilizer Project under Indo Asia Copper Ltd. (IACL), a subsidiary of Kiri Industries Ltd., starting in May 2021. His role involved everything from naming the company and designing its logo to overseeing strategic direction and operational execution, focusing on making the project shovel-ready.

Key Activities Undertaken:

I. Land Acquisition & Site Development:

- Site Identification & Acquisition (Post 1, Point 1; Post 2): Identified a port-based location, which is strategically important for raw material import and finished goods export. Successfully acquired 162 hectares (partial land) for the project, laying the physical foundation.

II. Feasibility, Design & Due Diligence:

2. Engagement of Consultants for Detailed Reports (Post 1, Point 2): Engaged M/s MECON Ltd., a prominent engineering consultancy, for crucial studies:

* DPR (Detailed Project Report): A comprehensive report outlining all aspects of the project.

* TEFR (Techno-Economic Feasibility Report): Assesses the technical viability and economic profitability.

* TEV (Techno-Economic Viability): Confirms technical and economic soundness for financing.

* IM (Information Memorandum): A document for potential investors and lenders.

* Market Research & Due Diligence: Conducted extensive research and due diligence for domestic and global supply-demand analysis, essential for understanding market dynamics for copper and fertilizer.

3. Technology Screening & Capex Optimization (Post 1, Point 6): Discussed multiple technologies from Australia, Japan, Finland, and China. Screened the latest Chinese technology to ensure the best economical Capital Expenditure (Capex) for a “Bankable TEFR,” implying a focus on making the project attractive for financial appraisal.

4. EPCM Consultancy & Balance of Plant (BOP) Jobs (Post 1, Point 9): Engaged MECON Ltd. for EPCM (Engineering, Procurement, Construction Management) consultancy. This involved completing “enabling jobs” on the project land before the basic engineering phase from the technology supplier and completing BOP (Balance of Plant) jobs, which are supporting infrastructure not directly part of the core process unit.

5. Authoring Core Documentation (Post 2): Personally authored and compiled critical technical and strategic documents, including TEFRs, sensitive feasibility studies, Supply Chain Management (SCM) frameworks, risk analyses, financial projections, regulatory frameworks, and various Investment Memorandums (IMs) for six phase execution options.

III. Environmental & Regulatory Clearances:

6. Comprehensive Environmental Clearance Process (Post 1, Point 3; Post 2): This was a major achievement highlighted by Dr. Sarkar.

* Initiated EC process from baseline monitoring after land acquisition (in 2022).

* Obtained Forest NOC (No Objection Certificate).

* Obtained Wildlife Conservation NOC.

* Conducted CSR (Corporate Social Responsibility) & CER (Corporate Environmental Responsibility) surveys.

* Prepared EIA/EMP (Environmental Impact Assessment / Environmental Management Plan).

* Secured CRZ (Coastal Regulation Zone) clearance.

* Obtained CTE (Consent to Establish).

* Arranged Public Hearing.

* Secured EC (Environment Clearance) in record time (November 2024) from the MoEF EAC (Ministry of Environment, Forest and Climate Change Expert Appraisal Committee) for both Industry 1 (Copper) and Industry 3 (Fertilizer), indicating approval for both segments of the integrated project.

* Dr. Sarkar emphasized personally navigating coordination with every layer of government (local, state, central) and multiple NGOs to fast-track these regulatory hurdles.

IV. Supply Chain & Off-take Security:

7. MOU for SCM Securitization (Post 1, Point 4; Post 2): Arranged multiple Memorandums of Understanding (MOUs) with major global companies like Glencore, Rio Tinto, Mitsubishi, Sinosteel, Nerin, APM Terminal, RtM Singapore, Indomer, Ecochem. These MOUs are crucial for securing both raw material supply (feedstock mapping) and potential off-take agreements, essential for de-risking the project for lenders.

V. Financial Strategy & Engagement:

8. Meetings with Rating Companies (Post 1, Point 5): Arranged multiple meetings with state and global rating companies for Kiri Industries Ltd., likely to improve the overall credit profile and ratings of the parent company, which would indirectly benefit the subsidiary’s project financing efforts.

9. Engaging Export Credit Agencies (ECA) for Debt Finance (Post 1, Point 7): Met with M/s Sinosure China for ECA-backed financing, a common route for projects involving Chinese technology suppliers to secure funds from Chinese banks.

10. Presentations to Nationalized Banks for Project Finance (Post 1, Point 8): Presented the company and project to various nationalized banks in India to secure domestic project finance.

11. Addressing Debt and Equity Visibility (Post 2): Actively managed and mitigated uncertainties related to debt and equity visibility, indicating ongoing efforts to secure funding.

VI. Contracts & Future Outlook:

12. Conclusion of EPC Contract (Post 1, Point 10): Concluded the EPC (Engineering, Procurement, and Construction) contract with a Chinese technology supplier at a price below the 2021 quoted Capex, which is a positive sign for cost efficiency. However, he explicitly states this contract is “yet to be finalized post Financial closure with Equity visibility.”

13. M&A Initiative (Post 1, Point 11): Initiated an M&A (Mergers and Acquisitions) initiative regarding the Philippines’ PASAR plant, potentially a strategic move to expand or acquire existing assets.

14. Project Completion Timeline (Post 1, Point 12): Stated that the IACL copper ore to cathode plant can be completed within 36 months once financial closure is completed.

Status of Financial Closure

Based on Dr. Sarkar’s statements, financial closure has not yet been reached.

Several explicit statements confirm this:

- In Post 1, Point 10, regarding the EPC contract: “…but yet to be finalized post Financial closure with Equity visibility.” This clearly indicates that the finalization of the crucial EPC contract is contingent upon achieving financial closure and securing equity.

- In Post 1, Point 12: “IACL project…can be completed by 36 month from now once Financial closure is completed.” This reiterates that the project’s construction cannot begin until financial closure is in place.

- In Post 2, he mentions having compiled documentation “all while mitigating the uncertainties of debt and equity visibility.” This further suggests that while efforts were extensive, the funding was not fully secured by the time of his departure.

My Conclusion:

Dr. Sanjay Sarkar’s tenure at Indo Asia Copper Ltd. saw significant advancement in preparing the integrated copper and fertilizer project. He successfully navigated complex land acquisition, secured crucial environmental and regulatory clearances in record time, engaged key consultants, screened technologies, and forged important MOUs for supply chain. He also actively pursued both domestic and international debt financing and managed to conclude a cost-effective EPC contract.

However, despite these extensive efforts and the project being technically and contractually prepared, the crucial milestone of financial closure has not been achieved. The project is poised to begin construction once the equity and debt financing are fully secured and legally binding.

Also a person of his stature exiting in this fashion via a public spat doesn’t bode well for both the parties and all other stakeholders.

Next Steps:

I have reached out to the management to seek further clarity on this via their investor relations channel. I urge other shareholders of Kiri to also do the same for obvious reasons of corporate governance.

Disclosure: Invested.

Post 1 -

Post 2 -