I did some digging and found this to be true.

Promoter group had lent funds from Mcleod Russel to other promoter group companies. And those promoter group companies were loss making and had no capacity (or intention) to pay back. Interestingly, another promoter group company Eveready (the famous battery maker) has been struggling due to leverage.

To make it further complex, there’s a family dispute between Aditya Khaitan & Amritanshu Khaitan over certain family properties - Both of them are on board of Kilburn Engg.

To summarise, promoter group created financial troubles via leveraging for operationally wonderful companies and w/o those loans these companies fortune could have been different!

Moving to Kilburn, my observations (on which I would like comments from the fellow members)

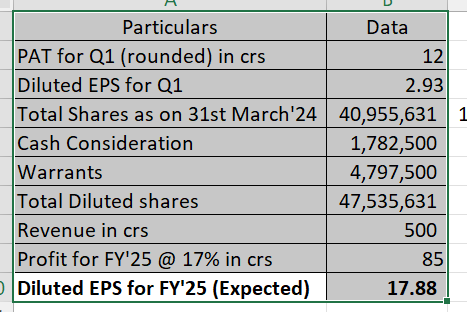

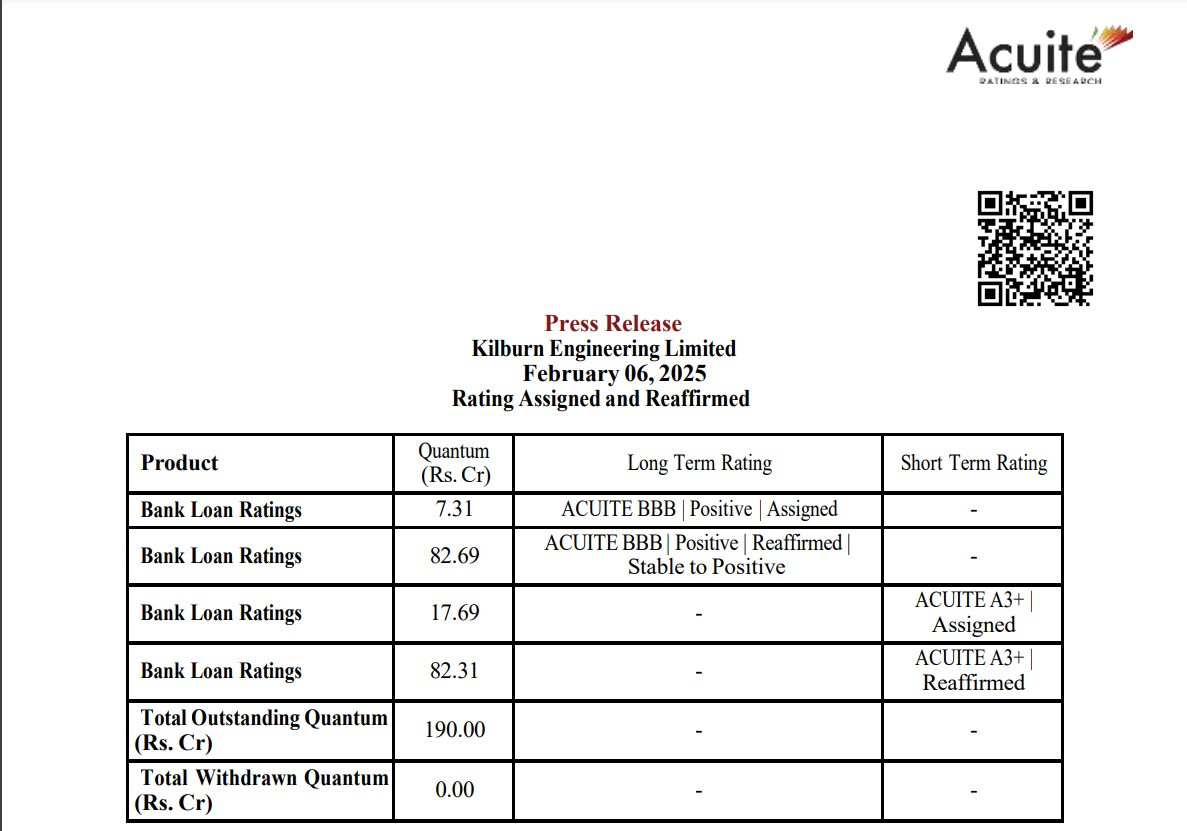

There’s not much leverage (Net debt of 0.2x as Mar’24);

But the Company has been diluting continuously - may be they have learned the lessons and want to stay away from leveraging - But still this will have an impact on the EPS growth

The positives (revenue growth) about the company have come in post joining of Ranjit Lala as MD who actually has relevant experience (PS: other promoter group companies too had professional management)

Have done a simple projected EPS calculation:

Pls share your take on the same.

Source article on Family/Promoter group:

“So, the promoter group is basically two parts. One part is the promoter group from the Khaitan family, which has been the erstwhile promoters as well. And then we have had a strategic investor who has invested by the name of Firstview Investments. It’s an investment arm of the OCCL group, which is Oriental Carbon group.”

The presence of OCCL / Goenka group augurs well for the company.

It is the firstview trade that’s been adding from open markets and getting the warrants. But Amritanshu Khaitan does make appearances in concalls also along with Mr Ranjit Lala, if I am not wrong. Thanks for the info.

This is what the management clarified in the Q1FY24 concall. This is a snippet from my notes that I take after going through concalls of all the companies I hold/track. This info could be a bit dated especially when it comes to holding % of different promoters in the company.

Promotor Group Structuring:

□ One part is the promoter group from the Khaitan family. The Khaitan family holding is approximately 22% - 23%.

□ Second, we have a strategic investor who has invested by the name of Firstview Investments. It’s an investment arm of the OCCL group, which is Oriental Carbon group. This group holds 35%.

□ Promoters are there just to give strategic guidance, but it’s a professionally run company. Major promotors brought in new management to run the company but the promoters are not involved in day-to-day management.

□ One of the big changes that has happened is the management change. Mr. Khaitan just explained that now it’s a professionally run business. So, the decision-making processes are far faster, quicker, and very focused. This is a big change that has happened from the past.

Hope this helps to explain what Amritanshu Khaitan’s role is in the company.

78 crore standalone revenue and 104 crore consol with ME energy. So ME energy is still on target to meet or beat the 65-70 crore guidance for this year but less than 200 crore in two quarters means Killburn may need to deliver two really stellar quarters or they are going to miss the 500 crore guidance by quite a big margin. Generally December seems to be same as march. Maybe the new factory will come online in Q3 and the deficit will be met by the revenue there?

Must read page 20 or 24 on concall of Q2, FYE25:

Q: What has changed since COVID?

A: if that’s the whole journey of Kilburn post-COVID, we had brought in new management in the company at senior level. We’ve changed the whole strategy of getting business, which is beyond just dryers, more like a solution provider to our customers. Our product offering has increased. We have added new industries into our stable like API where we got a large order from Granule, which is going to be executed in the next one year. So a lot of new product introduction into new sectors, systematic equity raise, repaying of debt, timely opportunities of acquisitions. So all this put together with strong management team has led to gaining economies of scale, better profitability, and that has helped really scale the operations going forward.

In a recent discussion, Mr. Khaitan of Kilburn Engineering highlighted the limited competition in the Radio Frequency (RF) drying and heating market. During the Q2FY25 earnings call, he mentioned, “There are only basically two players globally who are in it,” in the context of Monga Strayfield’s position. However, further research suggests that while the market may be specialized, competition does exist, with several notable players operating globally. Some of these companies are not only diversified but also large and influential in the RF drying segment.

Key Players in RF Drying

The RF drying sector includes a few prominent global and regional players:

Stalam S.p.A. (Italy): A global leader with advanced RF technology and a diverse product portfolio serving industries like textiles, food, and pharma.

Thermex Thermatron (USA): Specializes in large-scale industrial RF systems, particularly for textiles and rubber. SAIREM (France): Combines RF and microwave technologies for innovative solutions in food processing and ceramics.

Monga Strayfield (India): A mid-tier player focusing on cost-effective, customized RF drying solutions for textiles, food, and rubber, now being strengthened by Kilburn Engineering’s acquisition.

Kerone (India): Offers a broad range of RF dryers, infrared heating, and UV curing systems for food processing, textiles, and pharmaceuticals.

Radio Frequency Company (USA): Known for industrial RF heating and drying equipment, catering to food, textiles, and pharmaceutical sectors.

Observations Supporting Limited Competition

Niche Applications and Specialized Technology:

RF drying technology caters to specific industrial needs, such as precise moisture control in textiles or food processing, which limits the number of players who can develop and deliver reliable solutions.

High Barriers to Entry:

Developing RF technology requires significant R&D investment, technical expertise, and industry know-how, discouraging new entrants.

Geographical Fragmentation:

Most players focus on specific regions, leaving gaps in global competition. For instance, Stalam dominates in Europe, while Monga Strayfield has a stronger presence in India and parts of the US.

Limited Large-Scale Competitors:

While there are many regional players, global-scale competitors are few. Companies like Stalam and Thermex Thermatron dominate high-capacity solutions, leaving smaller players to focus on niche markets.

Collaborative Growth:

Strategic partnerships and acquisitions, such as Kilburn’s acquisition of Monga Strayfield, consolidate market positions and reduce fragmentation.

Investor Takeaway

The RF drying industry’s limited competition creates opportunities for established players to strengthen their market share. Companies like Kilburn Engineering, through strategic acquisitions, are well-positioned to leverage this niche market’s potential. While Mr. Khaitan’s observation highlights the specialized nature of the industry, the presence of competitors such as Stalam, Thermex Thermatron, SAIREM, Kerone, and Radio Frequency Company suggests a competitive yet fragmented landscape.

With growing demand for energy-efficient and precise industrial drying solutions, the sector offers significant growth opportunities for investors aligned with technological innovation and market expansion.

Kilburn Engineering Ltd. acquires Monga Strayfield Pvt. Ltd. to expand its global footprint in drying and heating solutions.

Kilburn expects this acquisition to contribute an estimated ₹80 crore to its topline and be margin

improvement.

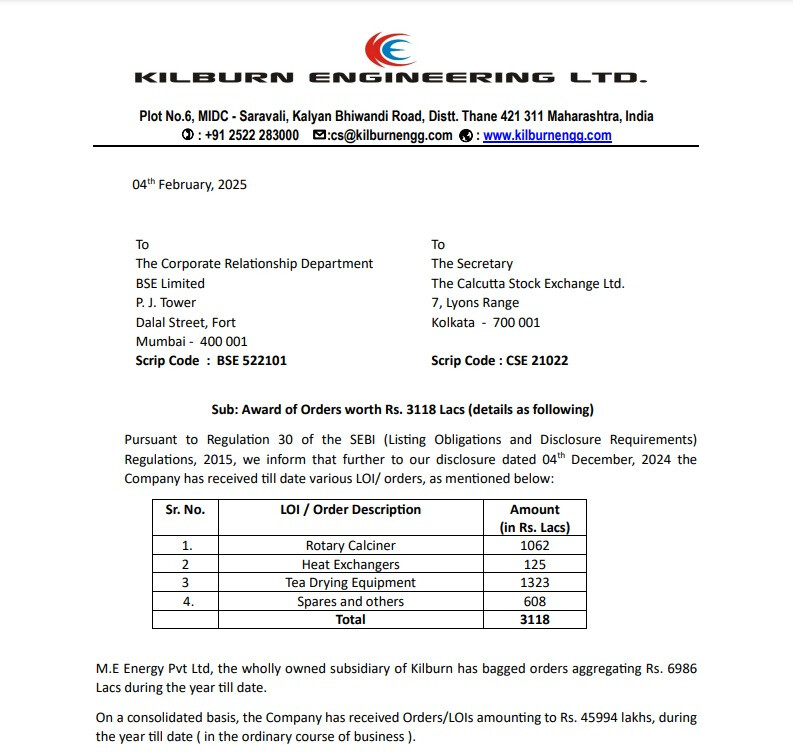

Company secured new orders worth ₹31.18 crore across various product categories, including rotary calciners, heat exchangers, tea drying equipment, and spares.

Additionally, its wholly-owned subsidiary, M.E Energy Pvt Ltd, has won orders totaling ₹69.86 crore so far this year.

On a consolidated level, Kilburn Engineering has received orders worth ₹459.94 crore in FY25 to date.

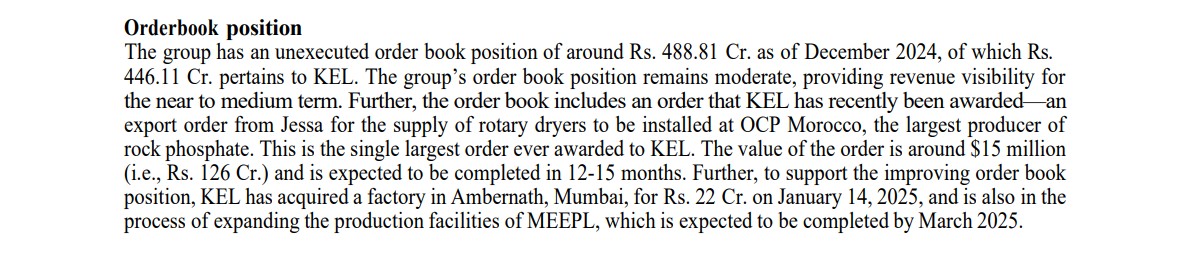

Healthy Order Book – ₹488.81 Cr (as of Dec 2024), including a $15M export order from OCP Morocco. Moderate Financial Risk – Net worth ₹175.93 Cr, Debt/Equity 0.47x.

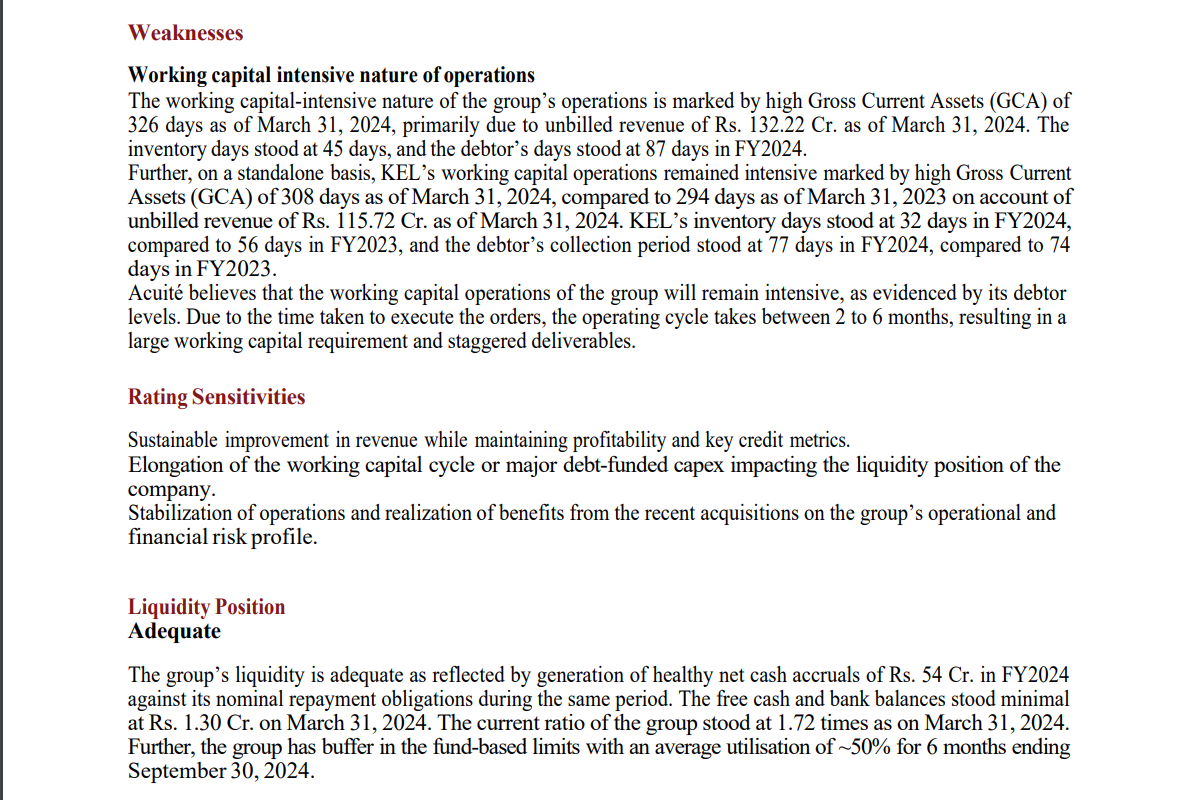

Key Risks – High working capital needs (GCA: 326 days) and capex risks (₹22 Cr investment in Ambernath factory). Liquidity – Adequate, with ₹54 Cr net cash accruals and 50% fund-based limit utilization.