I was checking out KDDL and was slightly confused on the valuation mismatch I saw on Screener. I wanted to understand if I am doing something incorrect.

So, basically, here are the screenshots from screener that I have used for calculations:

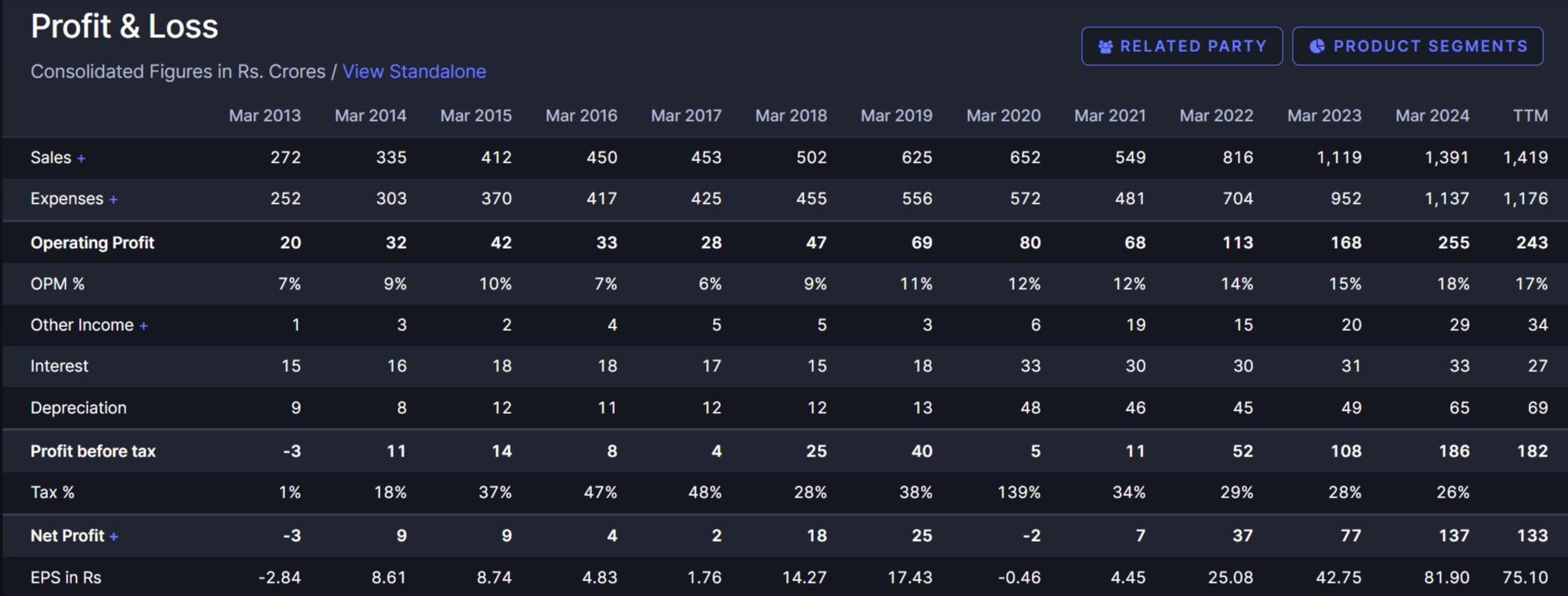

As per the MCap/Net Profit formula. the P/E comes out to be 3554/133 = 26.72. However, when looked at from Share Price/EPS, it comes out to be 2835/75.10 = 37.74! Why is there a discrepancy? Am I missing something? Are there any one time entities in PAT which is influencing this?

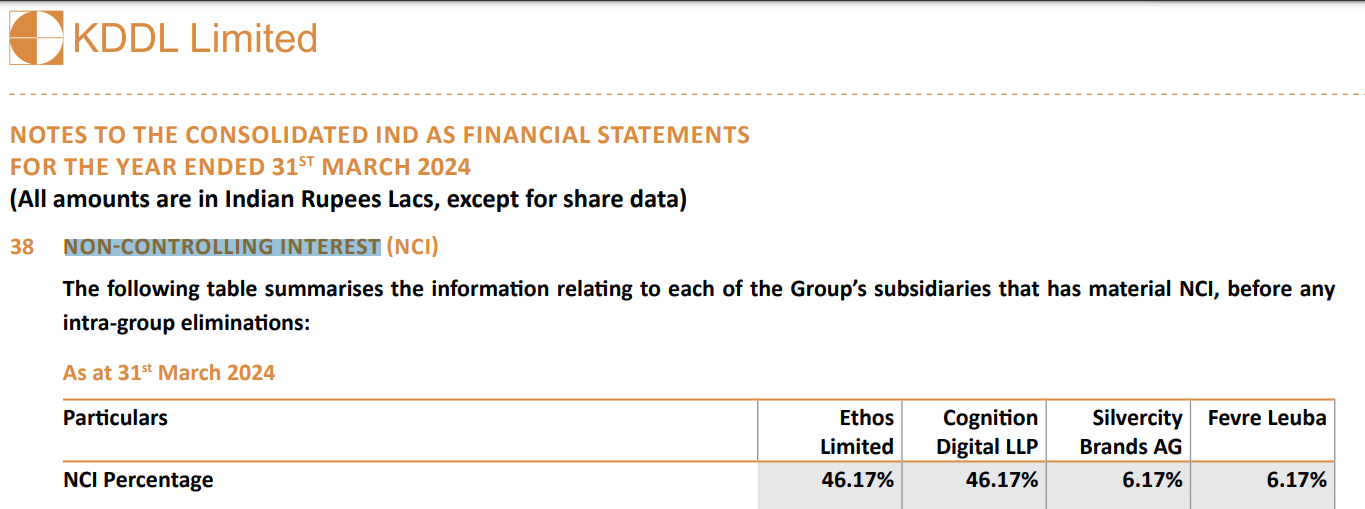

As shown below, four subsidiaries are not 100% owned by the company. Hence, their earnings are not considered 100% while calculating the EPS. Screener nets off this amount as ‘Minority Share’ under ‘Net Profit +’:

Detailed and a very interesting Deloitte research on the Luxury watch segment. This article focuses on Sustainability, the CPO market and importance of circular economy, Indian market as an opportunity, consumer preferences, NFT/Blockchains and impact and use cases of Gen AI for the Watch industry.

Attended the call today. Few of the pointers and honestly a mixed takeaway:

Most of the questions were asked about proposed GST structure and impact on sale.

Next set of questions primarily focused on margins taking a hit and they were aptly answered that due to new store openings, forex fluctuations, they had taken a hit.

Few questions that I would’ve loved to ask but will write to them anyways -

The business growth in Metro vs non Metro and how’s it looking.

CPO business growth- there’s not a huge delta between the growth in CPO and overall growth. A lot of exuberance was there about it a year back and now in the garb of expansion, it is not getting the same importance atleast in calls.

The repeat business and rising ASPs- If it’s fair to assume that their customer segment is now stabilised and we can see stable ASP growth or will it start to plateau now. The ASPs have grown upwards of 2 lakhs now.

Confused about- The management stated that they’ll now do half yearly calls. Now Pranav Saboo has been spearheading the last few calls and it’s okay that they want to focus on long term strategy but still don’t understand why this call has been taken all of a sudden when next 2 years are all about store expansion and lot of new initiatives are being taken.

All in all, still very bullish on the theme but I invested here initially because of Yashovardhan Saboo and while the leadership transition has possibly happened but seems like his focus is more towards KDDL.Will see now how business progresses. The valuation is anyways steep.

Disclaimer- A very big holding and have added in last few weeks as well post GST news when the stock corrected.

Revenue from operation increased by 18.8% year-over-year to INR 273.2 crores and increased by 26.3% year-over-year to INR 297.1 crores. H1 FY25 revenue stood at INR 570.4 crores, up 22.6% year-over-year.

In the Q1 FY25 EBITDA grew by 28.7% to INR 49.7 crores with a margin of 17.8% and for Q2 FY25 it expanded by 45.1% to INR 44.4 crores with a margin of 17% . H1 FY25 EBITDA stood at INR 98 crores, up 22.2% year-over-year. EBITDA margin were 16.8%.

The company’s H1 FY25 PAT increased by 19.9% year-over-year to INR 44 crores, driven by a 25.6% growth in Q1 FY25 to INR 22.8 crores with 8.3% margin and a 14% growth in Q2 FY25 to INR 21.2 crores with 7% margin.

Ethos recorded a foreign exchange loss of INR 4.65 crores in Q2 FY25, due to fluctuations in the value of the Indian Rupee (INR) against the Swiss Franc (CHF).

The company’s H1 FY25 average selling price (ASP) increased to INR 2,15,952, up from INR 1,87,000 in H1 FY24. The company’s H1 FY25 same-store sales growth was 15.5%.

As of June 30, 2024 (Q1 FY25), inventory days stood at 156, increasing to 177 by September 30, 2024 (Q2 FY25), driven by investments in new brands and store openigs, with plans to reduce them as the market matures.

Stores and Brand expansion:

Ethos opened 3 new stores in Q1 FY25 in Kochi, Dehradun, and Pune. Between April 2024 and November 8, 2024, the company opened 12 new stores at a cost of INR 35 crores and plans to open 13 more by the end of FY25. Management sees an opportunity to open 20+ stores annually over the next five years.

Management noted that approximately 20% of Ethos’ stores were under renovation during Q2 FY25, in anticipation of new brand launches.

Ethos added three more exclusive brands between April 2024 and November 8, 2024: ID Genève, Singer Reimagined and Hautlence. Exclusive brands accounted for 31% of total revenue in Q2 FY25.

Lifestyle Division:

RIMOWA boutique in Mumbai is profitable and delivers strong sales per square foot. The company plans to open seven to eight new RIMOWA boutiques over the next five years

Ethos plans to open its first Messika boutique in Delhi in January or February 2025. Ethos operated a Messika “pop-up” shop in Delhi in the lead-up to the boutique opening. Management plans to open eight to ten more Messika boutiques over the next five years.

Ethos is in discussions with 7 or 8 other brands in the Lifestyle segment. The company plans to announce new partnerships in the Lifestyle segment in the coming quarter.

CPO Division:

In H1 FY25, revenue grew by 33% year-over-year to INR 43 crores, driven by a 31% increase in Q1 FY25 to INR 19.6 crores and INR 23 crores in Q2 FY25

.

Management noted that the growth of the CPO division has been constrained by the availability of certified pre-owned watches and a shortage of watchmakers to service watches

Future Outlook and Challenges:

Management expects that the EFTA agreement will be implemented before the end of FY25.

Management’s long-term vision is for Ethos to become a leading luxury retailer in India. The company is targeting a 10x increase in revenue over the next 10 years.

Management expressed confidence in its ability to manage the impact of a potential increase in the GST on luxury watches from 18% to 28%.

Ethos plans to launch Favre Leuba in India in January 2025. Ethos has already received pre-orders for more than 100,000 Swiss Francs

Ethos has a dedicated in-house design team that creates limited edition watches for India in partnership with brands. Ethos has already received INR 70 crores in orders for limited edition watches that will be delivered in the coming year.

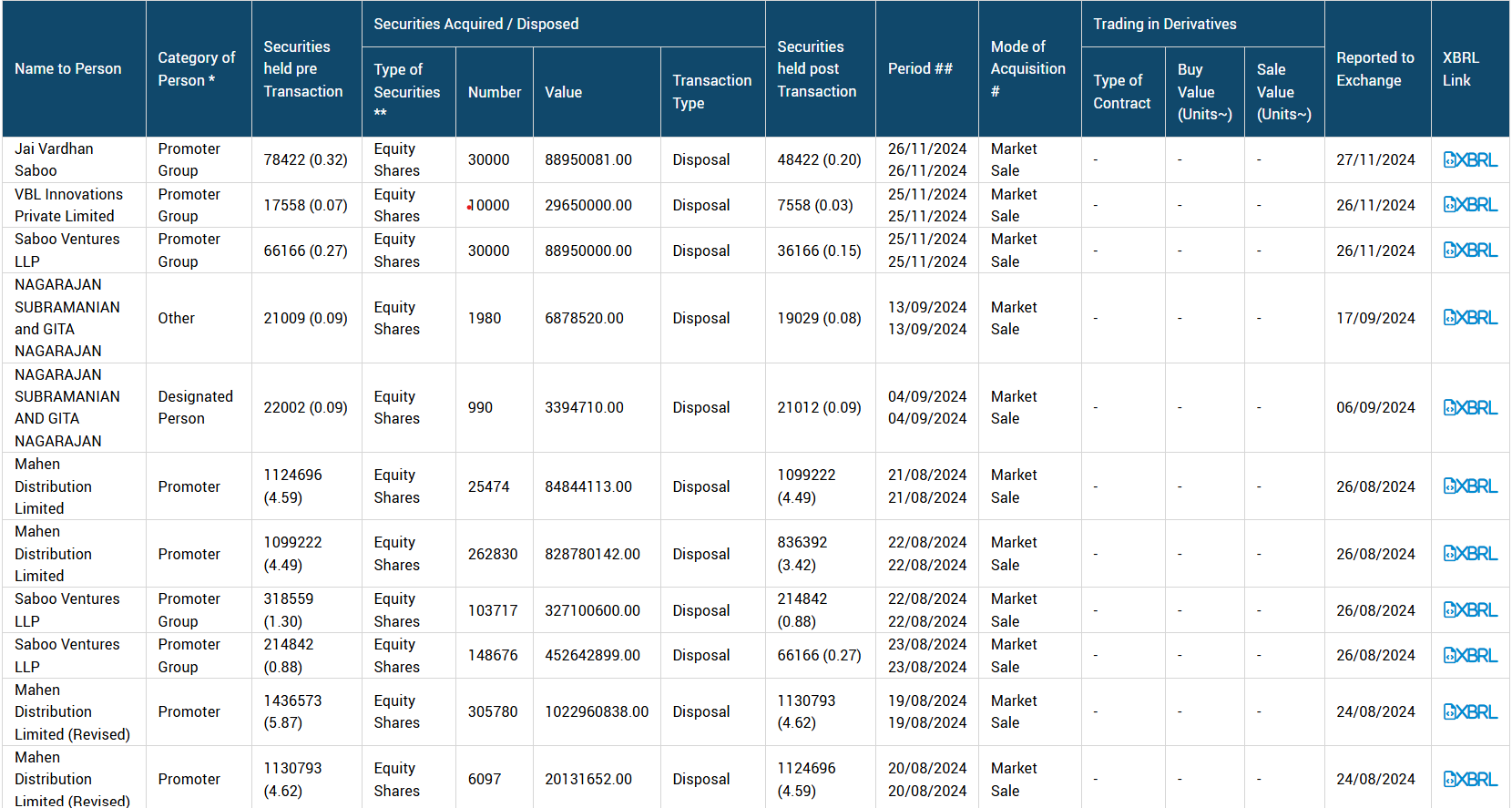

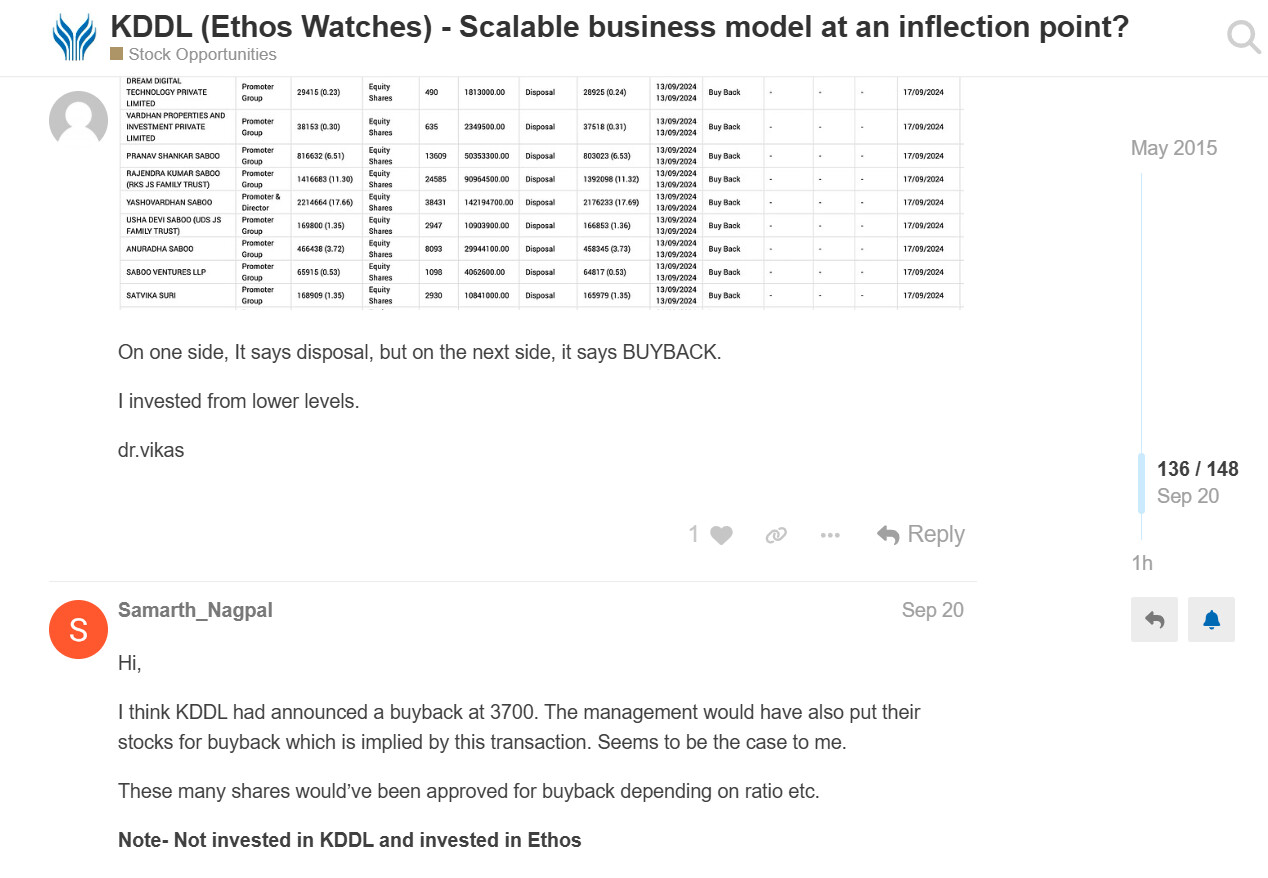

They’ve been doing this for over a year now, sell in bits and pieces every now and then.

An analyst raised this in a concall but no solid answer was given.

Here is the snapshot of my message.

Yes. Nothing wrong in promoters’ tendering their shares in their own company buyback. Its perfectly legal. But what I didn’t like is - the stock ran up to 3700 just before the buyback and then fell all the way to 2400. It felt like as if the price was rigged up till the buyback price so that promoters can take the cash officially from the company in their own account.

I felt like kind of cheated being a small share holder. So sold out.

Again My personal thinking and opinion. I maybe wrong.

Ethos Limited: Growth Amidst Challenges, Why the Stock Price Fall?

Key Highlights:

• Exceptional Growth in October 2024: Ethos reported a remarkable 47% year-over-year growth in October 2024, signaling strong performance for the current quarter (Q3 FY25).

• Strong Financials: Revenue for H1 FY25 rose by 22.6% YoY, while EBITDA margins held steady at 16.8%. PAT grew by 19.9% YoY, reflecting healthy profitability.

• Expansion in Stores and Brands: With 12 new stores opened this fiscal and plans for 13 more, Ethos is aggressively expanding its presence. Exclusive brands now contribute 31% of total revenue.

Why the Stock Price Dip?

Despite impressive growth, Ethos’ stock price has declined. Some potential reasons include:

GST Hike Concerns: Management has assured investors that the impact of a potential GST increase on luxury watches (from 18% to 28%) will not be entirely borne by Ethos, but market sentiment remains cautious.

Rising Inventory Days: Inventory days increased from 156 to 177 days, signaling higher working capital requirements due to new store openings and brand investments.

Forex Losses: The company faced INR 4.65 crores in foreign exchange losses in Q2 FY25 due to INR-CHF fluctuations.

Renovation Disruptions: Around 20% of stores were under renovation in Q2 FY25, potentially impacting near-term sales growth.

Management’s Confidence in Future Growth:

• Ethos aims for a 10x revenue growth over the next decade, with opportunities to open 20+ stores annually.

• New partnerships in the Lifestyle and CPO (Certified Pre-Owned) segments are expected to drive diversification.

• Pre-orders of INR 70 crores for limited-edition watches reflect strong demand in the luxury watch market.

Discussion Point:

While Ethos’ fundamentals and growth trajectory remain robust, why is the market discounting its stock price? Are the concerns around GST hike and rising inventory overblown, or is the market pricing in risks? What are your views?

Can’t speak on the price fall, but a few observations:

They said something similar in the Q1 concall when the sales was not as expected. Said the first month of Q2 has shown good recovery but then it did not reflect in the Q2 results.

The sale of Silvercity to KDDL felt a bit iffy. Management did not provide a clear cut answer to the move.

Constant sale of equity by promoters. They evaded the question in the concall.

Now they’ve declared that they’ll be hosting concalls only every 6 months. Why ?

I’m still invested , but that’s only because of the strong moat - the tie ups from brands.

I second the promotor selling part & the new concall schedule. The same I had reflected on in my post Q2 concall notes as well.

Not reading a lot into promotor selling though market might take it otherwise. Bigger negative for me is limiting concalls. Also in Jan some stake has been taken by Invesco again. So high chances that FII & DII have increased holding in lieu of promotor selling

With Pranav Saboo taking over charge & a very aggressive expansion plan it was a very big surprise.

Also wrt inventory won’t be concerned a lot since unlike Apparels & other categories seasonality isn’t a big factor & mark downs aren’t a big concern.

Also new store openings plus brand addition will need that investment.

Also many companies plan renovation around Sep since that’s somewhat a lean period in terms of sales before festive & wedding season. So some sort of hit happens ( alluding to post above)

The biggest thesis for me is the moat for Ethos & their industry knowledge to really leverage the luxury consumption. But I’m a little taken aback by the Management’s stance towards minority shareholders & moving away from quarterly updates.

Also had done some scuttlebutt & my sense says that Q3 should somewhat end around 375 crores top line. November was also good for them.

Still a major part of holding but a little watchful about management actions & communication with stakeholders.

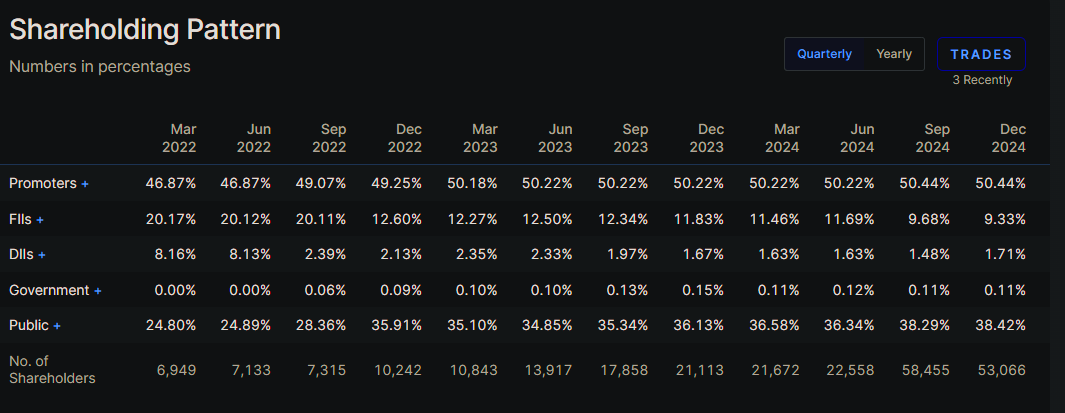

we will have to check the shareholding pattern in Dec quarter for both ethos and kddl…it will be good if promoters sold to strong hands…but if they sold to public i will be very disappointed

The upcoming budget will decisde the course.

Its high time, the tax liability of middle men to be reduced.

The consumption sector will be find positive in budget only if basic exemption limit or rebate is increased.

If tax till 10L is Nil, we will see good comeback.

Also, at this moment, only budget seems to be place maket is expecting to find any solace.