Q3 results on Feb 14th

Fingers crossed ![]() we’ll have a happy Valentine’s Day

we’ll have a happy Valentine’s Day ![]()

Q3 results on Feb 14th

Fingers crossed ![]() we’ll have a happy Valentine’s Day

we’ll have a happy Valentine’s Day ![]()

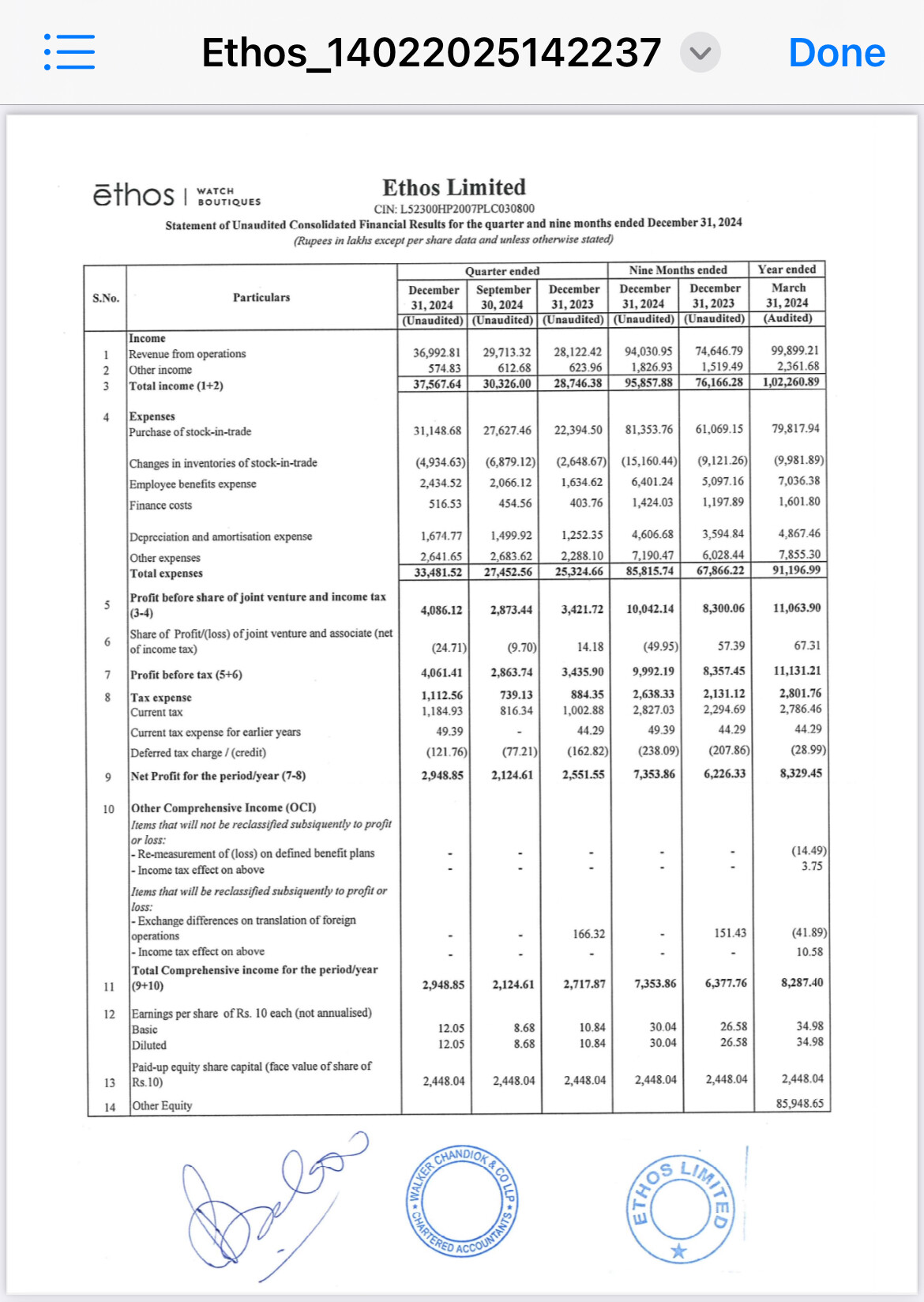

Ethos results announced. Couldn’t have got closer. Revenue of 375 crores posted by the company ![]()

![]()

![]()

Disc: Invested & biased

Summary of the investor PPT by chatgpt:

Ethos Limited demonstrated strong revenue growth and continued expansion in Q3 & 9M FY25, with a focus on luxury brand partnerships, digital sales, and store openings. Despite some margin pressure from expansion costs, the company remains committed to its long-term growth strategy.

Hi,

Have been assessing this company since the past few weeks. PS: I had never seen this company. I had a certain doubts around the company?

Q1. What would be a good holdco discount for Ethos

Q2. If the manufacturing facilities for dials/ hands/ and belts are in India, are the parts then exported to Switzerland and then imported back as a finished product?

Q3. Have the EBITDA margins in standalone peaked out at 21%?

Q4. What was the other income of INR 201cr for standalone in FY24?

Q5. I do not see much room for growth through Ethos as it’s a distribution model, does anyone else have a contrary opinion?

All are personal questions, just an enthusiast. Thanks

regarding question 2,can you kindly give me the source from where you got to know that they manufacture the watch components in India? maybe it applies to the more budget brands like Seiko, Tissot etc but not sure about the higher tier brands!

what do you mean ? KDDL manufactures watch components right ?

yes KDDL does but what about Ethos?

This thread sometimes gets confusing, are we discussing about Ethos or KDDL

Annual report states and so does this thread, that they’re expanding hands facilities and bracelet facilities.

They’ve nowhere mentioned what brands are catered by the facilities in India and which ones are catered by the Switzerland manufacturing facilities.

We are discussing about KDDL only.

[ETHOS] Promoter selling observed today, has it been dumped to public or to some other strong hands?

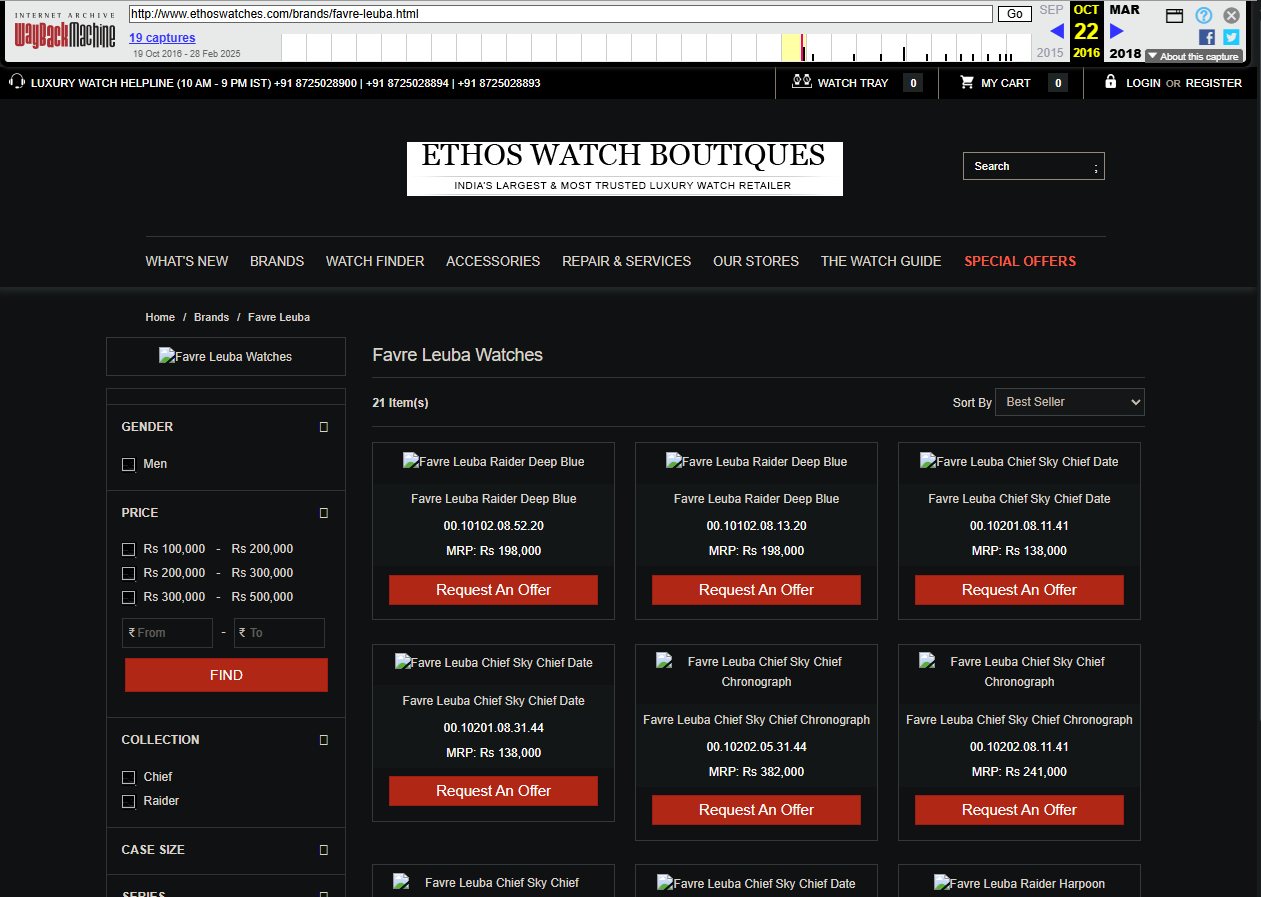

The much awaited Favre Leuba watches are now available & there are almost 140 SKUs listed on the website. The starting price of 1.25 lakhs upwards & with many styles near 3.5-4.5 lakhs range, this could be a very good project in terms of management capability in having exclusive rights wrt retailing an iconic brand.

Q4 results & subsequent concall should throw some light on initial customer response towards this legacy brand whose revival Ethos has taken a bet on.

Disc: Invested & Biased in Ethos

they had favre leuba from before as well right? for example this archive.org snapshot from 2016 shows they were already selling Favre from long back

Favre Leuba is a Swiss watch brand which is one of the oldest ones. Back in 2016 or sometime before that Titan had acquired this brand & possibly at that time Ethos would’ve also been retailing these watches.

Cut short, this brand has now been acquired by Silvercity which is a KDDL subsidiary & in which Ethos has minority stake.

Now KDDL has the exclusive rights to distribute FL watches throughout the world & Ethos has exclusive retailing rights in India.

SilverCity was formed to make strategic investments in iconic watch brands etc.

What this means for Ethos & which I might have missed or I’ll edit my previous post is that they’ll have an iconic Swiss brand to which they’ll have exclusive retailing & part of design language rights also for India.

Hope I’m able to answer the query. You may also refer to KDDL & Ethos concalls for more clarity

thanks for the detailed explanation

in the future hopefully ethos can get similar rights for legendary brands like Cartier, Patek, AP etc..these 3 are very popular that ethos doesnt yet sell

FL was sold under distress to Titan and Titan failed to turn it around so sold it to Ethos.

I don’t think the other brands you mentioned fall in this category.

Ethos Q4 & FY 25 results declared. Revenue growth of 23.3% & PAT growth of 8.1% for Q4

Growth looks to be average in Q4 & store opening plan vs realisation has been weak for FY25. Against plan of 25 they’ve opened 14 stores with only 1 store in Q4. It’ll be interesting to see their store opening plan for FY26.

CPO business seems to have taken a backseat with only 32% odd growth Looks like the initiative couldn’t pick up as much as the promise being shown by management in terms of process & investments into it.

FY26 could be a strong start in terms of launches with 8 new stores scheduled to open in May 25 including 1 Messika store. But a lot of this seems to be spillover so need to see management commentary on total store additions plan.

Also ASP growth seems to have now reached steady state with ASPs reaching 2.04 lakhs

Disc: Invested & No recommendation

management continue to highlight the lofty ambition of 10x revenues in 10 years which translates to around 25% cagr of revenue growth

Please Look at their yearly growth numbers. They delivered 25% revenue growth in FY25 vs FY24

One thing is that they dont even talk about Rimowa now. Also I looked at their Rimowa store rating on google. It was horrible 2.7 star rating and many customers are complaining about their services and quality. Its very bad because such high class people who buy Rimowa are very unlikely to make purchase from their store if they see the ratings and complaints.

Secondly, As I remember they said that Messika Store was going to open in January 2025

exactly, as mentioned above by Samarth, there has indeed been noticeable spillovers and no doubt the stock fell today after the results were out. still i would like to hear the concall transcript when it is out

ICICI MF continues to add more shares. As per their recent declaration, they have added 5.54,721 shares in the period between 7/12/22 and yesterday.