About Bank

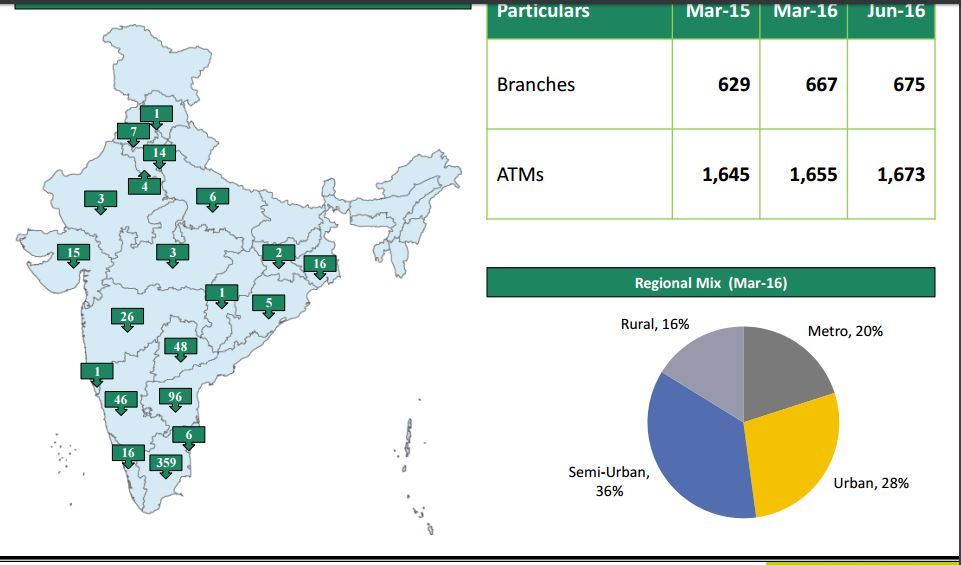

KVB is one of the oldest private banks in India . It started its operation in 1916 in Karur ,Tamilnadu. The bank has recently completed its 100 Years of operations.Currently it has pan India presence (barring Northeast and J&K ) with a network of 675 branches .359 of which are located alone in Tamilnadu. The breakup of branch is as : -

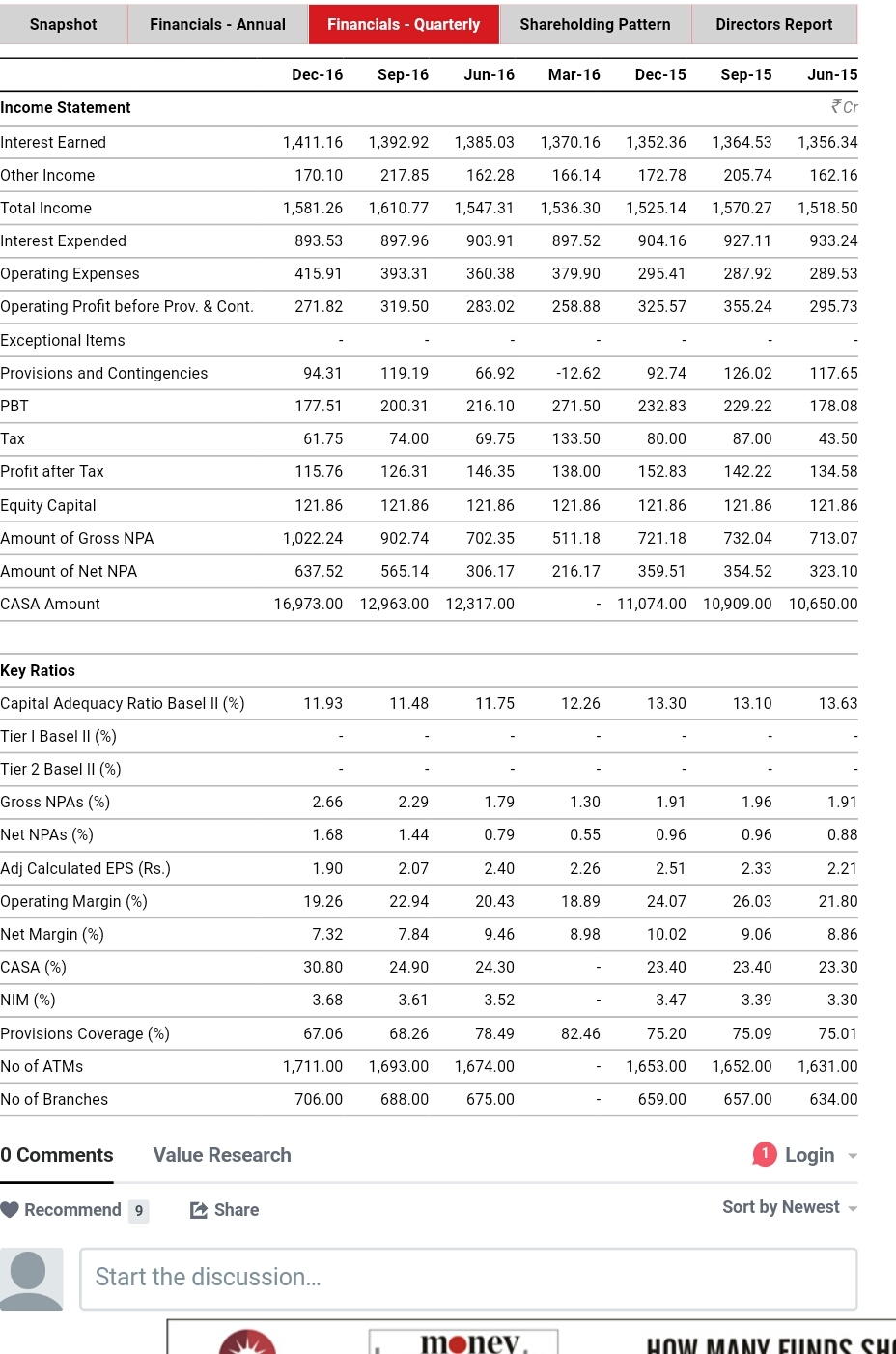

The key takeaway from the latest quarterly result is : -

Improvement in NIM,CASA

Bank has low NPA when most of the banks are suffering from Asset Quality destress

One of the best Provision coverage ratio in Indian banking industry

Flat total Income

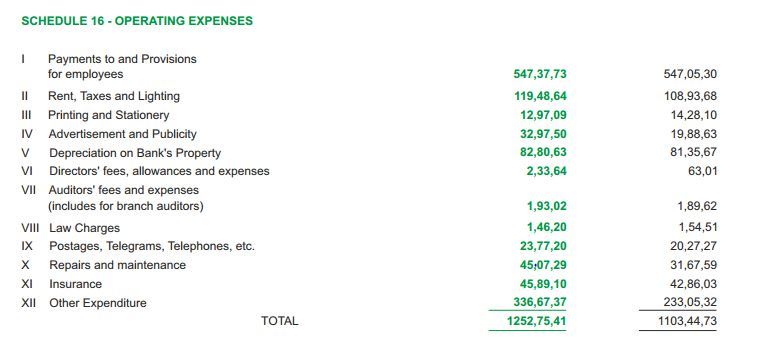

Increase in the operating expense (Mainly due to Other expenses). I could not find the breakup of other expenses

Provisions has decreased as NPA decreased (YoY)

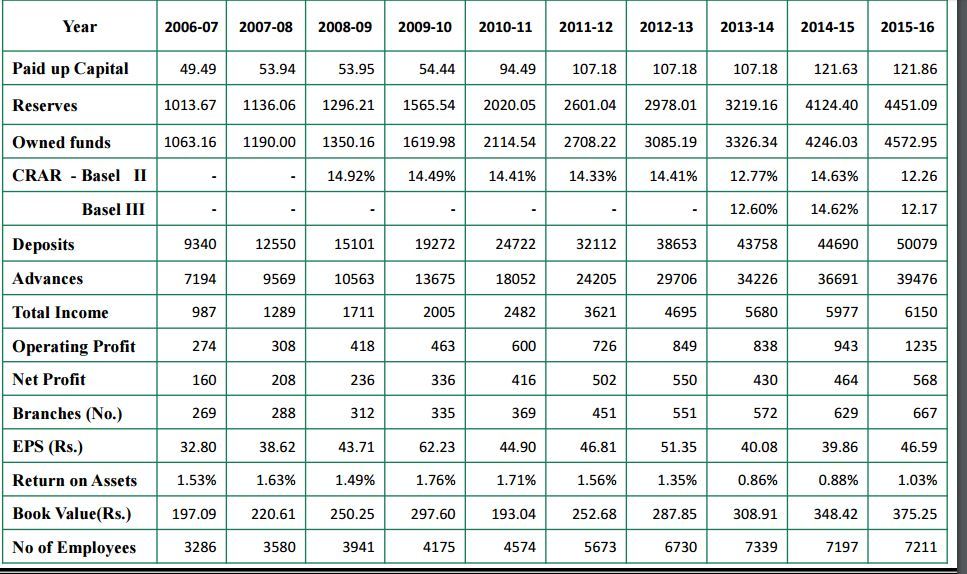

Now have a look at the Annual progress of KVB for last decades (Source KVB June 2016 Investor Presentation)

The bank has made a good progress till 2013 -14 but from last two years banks revenue growth is stagnant (less)

PAT growth is continuous

Bank has enjoyed a very good NPM till 2010-11 . After that bank has rapidly done its branch expansion . I believe thats the reason for drop in NPM. Now the pace of branch expansion is slowed down , I believe it will improve its NPM again.

The same branch expansion theory goes with RoA .

Valuations

CMP - 478

Market Cap - 5829 Crs

Book Value - 387

TTM EPS - 47.54

P/E ~ 10

P/B ~ 1.27

Investment Rationale

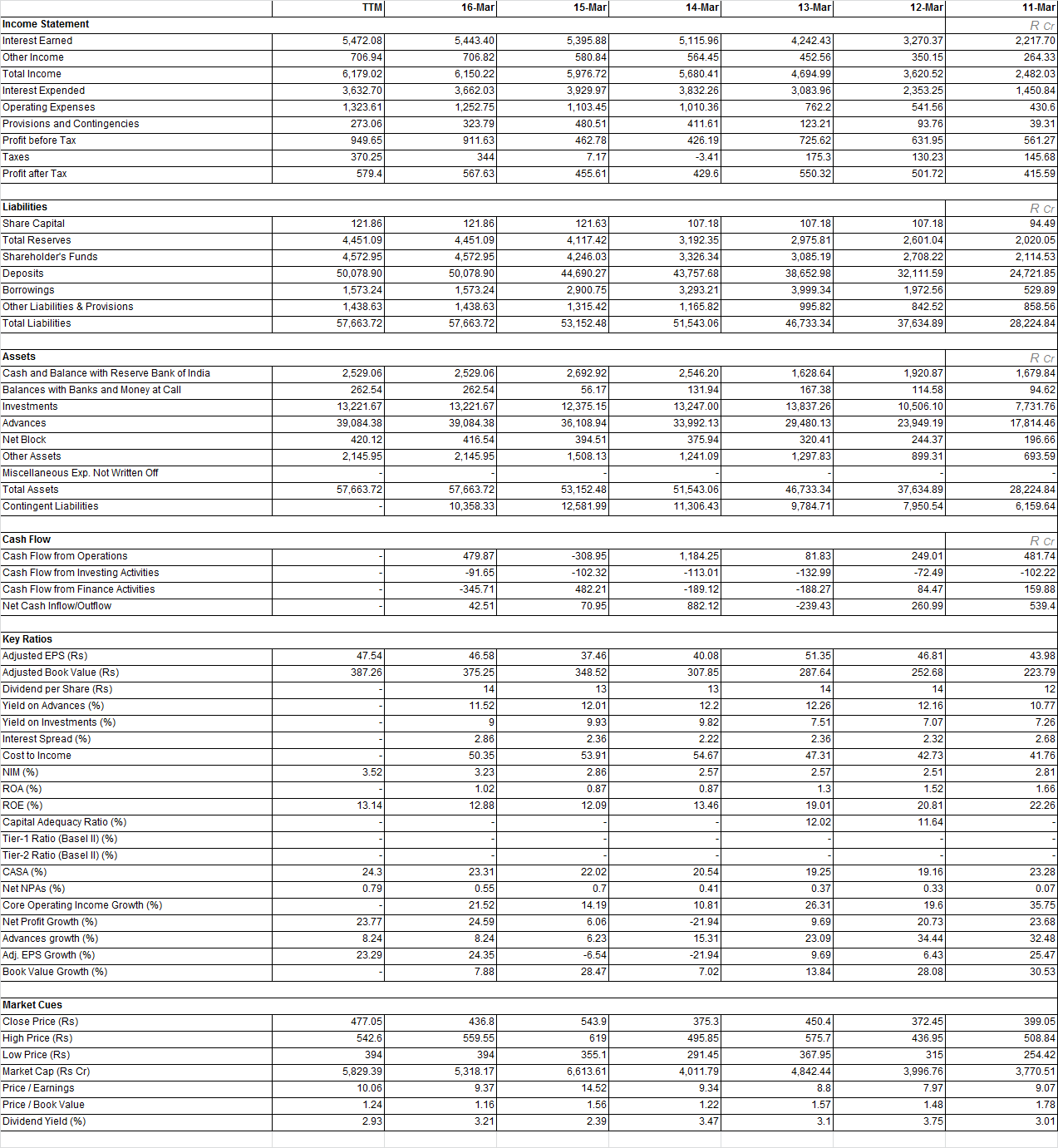

Let me put some data from Valueresearch which shows the financials of last 5 years

The bank is available at very attractive valuation of P/E 10 and p/B of 1.27

It has one of the best asset quality in the indian banking industry (Ofcourse I am not talking about HDFC here ). Current NPA is .77 . While most of the banks are suffering from the NPA crisis , it has managed to reduce the NPA in recent time . It has one of the best provison coverage ratio .

Deposits and advances has started picking up from last FY . We can expect the good business growth going forward

Continuous improvement in NIMs,RoA . I consider RoA as the best metric to asses the efficiency of the financial institutes. Although RoA is not the best among industry ,I would say its lagging too much from the industry leader . But I believe the bank was in the expansion mode for few years and than followed by adverse economic condition (In last two years where other banks has focused on growth ,KVB focued on asset quality hence e could not achieve more income growth)

NPAs are declining and with the pick up of the economy it would further decline . Company is also shifting its focus from corporate to SME and Retail which would further help in reducing the NPA

The increased number of branch should start the revenue contribution

Recent declines in repo rate will reduce the cost of funds<img

Increase in CASA will reduce the cost of funds.

Dividend yield of 3 %

Increase in other income . In case of banks other income is commission brokerage,transaction fee etc . Its a good sign to have an increase in other income

Bank’s most of the business comes from the south india (Concentration of branch is almost 70 %)

Increase in the other expense . I could not find the breakup . If the increase is continuously growing at the same pace then it might eat up lot of profit.

However I think you missed out on the restructured assets part of the story.

Currently the bank has a total restructured book of Rs 1281 cr. Plus Net NPAs of Rs 306 cr. Assuming that 25%of total Restructured loans end up being NPAs ( Conservative estimate ), so that makes it roughly Rs 320 cr.

If we add the two- Rs 306cr + Rs 320 cr = Rs 626 cr…roughly equal to one year profit of the bank. So, the bank has the capability of coming absolutely clean in one year.

Compare this to most other banks, the situation is not bad at all.

Plus the undervaluation and expected economic turnaround, it can give descent returns. Plus in an expensive market, it is one of the few reasonably priced opportunity.

Thanks @ranvir for pointing out the missing information.

I will take this point to my checklist whenever analyzing a financial company.

Actually I am new to investing world (hardly a year) so still lots of things to be learnt. And this is my first topic creation post.

It is not at all growing.

Possible takeover candidate.

for 100 year the celeberation, people are expecting bonus and rights - but Managment did not satisfy the expectations. Otherwise, it is shareholder firendly always and aggressive bank in past

@kkronline Bonus does not change any fundamentals of business.

I have also read similar post on mmb of takeover and expectation of bonus. People getting frustrated because of not getting bonus (and mainly they are traders). People can expect anything for quick bucks. And regarding takeover candidate, I have not seen any reliable source. If you know please post it.

Regarding the slow growth, Yes I agree with you. The growth is stagnant for past two to three years.

Hi,

Regarding takeover - I heard from one of the middle managment of KVB. Promoters want to hold the stable till cenetary year and they successfully did. Now they may look for right partner. No onus on information.

Regarding Bonus and Rights - It is one way of rewarding customer. not on business perspective. also a sper their pattern. If economy set to boom due to low interest rate, it is prudent to raise capital via Rights which is win win for bank and shareholders though cost of equity is high.

PS: holding from 300 levels. I am interested to buy small banks with low NPA at their book value.

A lot rides on the q2 results. The bank’s asset quality has been steadily improving . Growth in top line has been moderate. Its the bottomline where the growth is muted or missing I must say ( Due to heavy provisioning to maintain asset quality) .

But if Q2 shows some green shoots of trend reversal, the stock could be in for a re- rating and PE expansion.

Could anybody elaborate on the asset sale to ARCs by KVB? This analyst report says, bank sold stressed assets at a loss of 497 Cr which will be amortised in the next seven quarters. So apart from the current NPA (~ 565 Cr) this is another 497 Cr that they will have to provide for in the coming quarters?

I was invested in KVB for below reasons ,but they are not working as expected

Asset quality

Now that asset quality is deteriorating. (Though better than many peers)

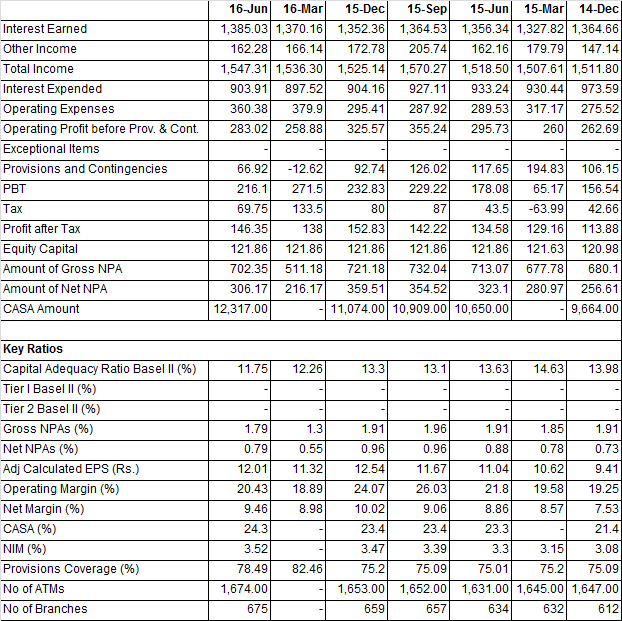

It’s Net NPAs has grown three fold in last 4 quarter and GNPA is doubled.

Provision coverage ratio has come down from 82 to 68

Growth pickup

The top line growth is muted…

You can see the NPA and provision coverage ratio figures from the attached screenshot from value research.

What is the procedure for applying for the rights offering?

I did receive the CAF and filled up all the information. I do not have an account with the any of the KVB SCSB branch, but do have an account with other branch.

Can any seniors help with the steps needed to apply for the rights offering? Thank you in advance!

There is no need to maintain a/c with KVB.

If you intend to opt for your rights plus additional shares

(It is advisable to apply around 20 %additionally) you may issue cheque

for the total amount and to deposit with the designated branches of kvb

along with CAF .Alternatively by Registered post to Registrar to the issue.

I intend to apply for more than 200k in amount and have to only use ASBA. So I do not know if they will accept Cheque for ASBA application at a KVB branch.

). Current NPA is .77 . While most of the banks are suffering from the NPA crisis , it has managed to reduce the NPA in recent time . It has one of the best provison coverage ratio .

). Current NPA is .77 . While most of the banks are suffering from the NPA crisis , it has managed to reduce the NPA in recent time . It has one of the best provison coverage ratio .