Financial result for Q3/ 9 Months ended 31st Dec 2018 :

Attended Q2FY20 Investor call today (but got disconnected after 60 min for some reason).

Q2FY20 results : https://www.bseindia.com/xml-data/corpfiling/AttachLive/D02163BE_73BB_452E_B3F3_3DB1591F6534_125352.pdf

Updates from results, concall discussions :

Income - 8 YoY

PAT - 63Cr (down 24% YoY)

Deposits - 7 YoY

Gross Advances - 3%

GNPA - 8.89% (down by 28 bps from Q1)

NPA - 4.5% (down by 44 bps from Q1)

PCR - 61.8% (up by 2)

Incremental provisioning not required anymore. Improvement in situation of SMA1, SMA2 book.

Slippages increased from 474cr to 549cr. Mgmt said there has been good number of recoveries so net net remains same.

There is high liquidity within, which affected margins. Increase in retail book soon should offset this in coming quarters.

Business Updates :

-

Total Branches - 779

-

Focus will be in South & Western states from now on + Delhi. All branches are being trained for the retail push.

-

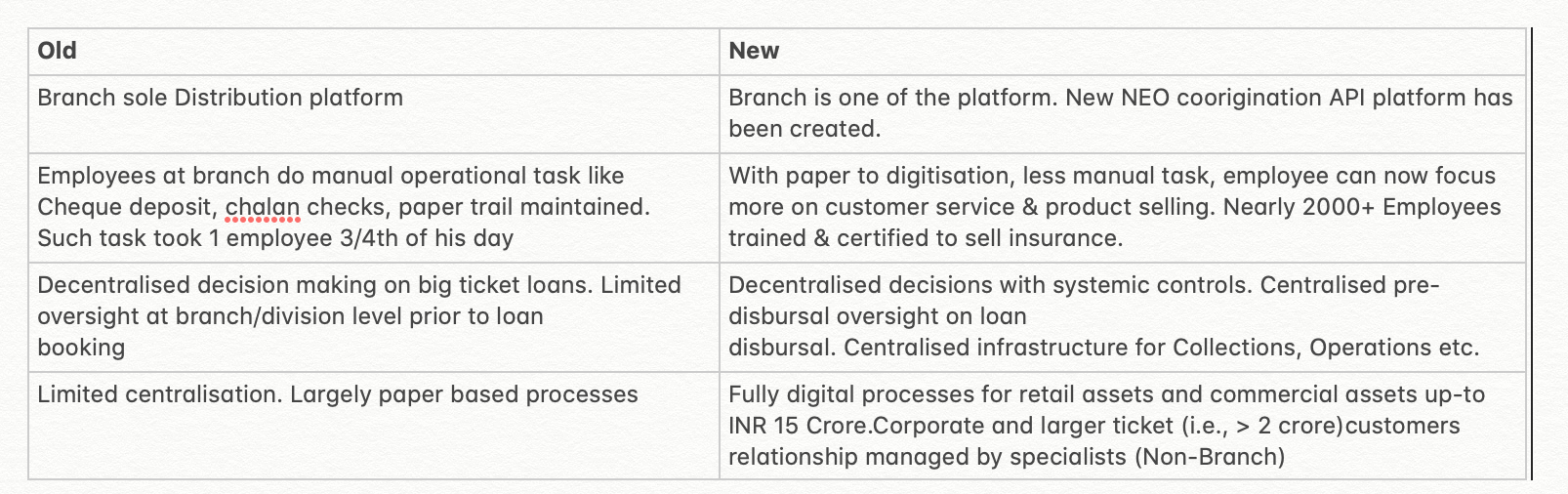

KVB is undergoing huge changes in their business model. From a corporate oriented bank, bank is moving towards retail focussed & small business commercial bank. In order to facilitate the change, bank has undergone series of changes & improvements:

A) Branch level changes in Business model, old vs new:

B) Distribution reach increase through Coorigination platform (NEO Gateway API) : KVB have been extensively working on a technology platform for integration to other financial institutions and products so that their distribution channels are now increased. This Co-origination platform is live with 4 live relationships. As an example, Mgmt described tie up with ‘Home Credit India (HCIN)’ (part of Home Credit group a global MNC). HCIN has a balance sheet of 7000 cr and does Consumer Finance. Mgmt explained that platform is very powerful in the sense that the time to market for such relationship in NEO platform, is less than a month. KVB will process loans through an app-based, end-to-end paperless solution. This partnership will help KVB leverage HCIN’s large user database and reach out to a segment which they have not pursued aggressively in the past. This is a joint lending. HCIN and KVB will disburse the loan as a single amount to the customer. HCIN gets exposure of KVB’s low cost of funds. KVB will be able to cross sell other banking products as well to these customers. Mgmt claimed that processing , underwriting is digitised & can be done within 60seconds. First loan went through in July and they are currently in pilot phase, but they have already done 140 Cr worth loans through the integration.

KVB has also tied up a similar distribution deal with ICICI Lombard,so insurer could sell insurance to KVB’s customer. Management also looking to tie up with Microfinance partners.

-

KVB is now retail focused. Mgmt claims they have deliberately not increasing Corporate book. Degrading corporate, large ticket corporate loans. Corporate 27% retail 24%. Advances are flat. Liquidity is more.

-

Retail grew 20%. Focus is on distribution setup to improve retail. Partnerships with HCIN, ICICI Lombard is a start.Small ticket commercial & retail will increase

-

Agriculture loan provided will be more on Gold collateral. This will increase Gold loans. Digital jewel loan roll-out continuing.

-

Small Business loans are grew 85% QoQ. This is also digital app loan process.

-

App transactions increasing nearly 50% QoQ since start of FY.

-

Bullion business to start from Q4 FY 20

10)Guidance - Retail Run rate in Q3 is positive , momentum strong. Overall, management wants to be conservative. A Growth 10% YoY is possible for the year.

3 Likes

If all the banks are going to focus on retail lending, i wonder who will lend corporate companies?

KVB had a policy of not issuing credit cards. Now, they have started to issue credit cards in partnership with SBI.

With new management, the company seems to be moving away from some of its core principles.

1 Like

They are not going completely retail though. They still say they will do retail & small business loans which is their core strength. Its a good thing IMO. KVB has suffered with NPAs for a while …atleast now with retail & small ticket business loans, they have a tight leash on NPAs. Their market is rural which is largely untapped in retail side

Now the bank is focussing on gold loan and they have disbursed approx Rs 10000 cr as gold loan .Gold loans are considered totally safe . I expect the bank to now perform better.

Investor Presentation on the Un-audited Financial Results of the Bank for the Quarter and Nine Months ended 31st December 2020

1 Like

Concall highlights

Business

Bank has formulated three year strategy to reach 1% ROA by FY24.

Growth - retail loan grew 9.5%YoY and are now completely sourced digitally. Stopped unsecured loans for time being. Rural loans doing well - LTV of 75% to manage price risk.

Commercial - strategic priority - most profitable segments. Overall bank expect credit growth of 12% in FY22. Open to organic and in-organic growth opportunities.

Bank took full wage revision impact by 3QFY21. In the 4Q, bank reversed provisions of INR620mn from provisioning line to employee cost line; impact was P&L neutral. Bank expects steady state run-rate of INR2.6bn per quarter for employee cost. 90% of employee under IBA. Bank has completely stopped IBA recruitment.

Bank has 54% branches in semi-rural and urban areas.

Home loan book - self-employed is 70% and salaried is 30% ? Commercial book yield at 10.5% with collateral cover of 1.3x.

Steady state tax rate of 25%.

Commenced credit monitoring department under leadership of GM to increase recoveries from Two pool Asset Quality ? Collection efficiency >90% in 4QFY21 and April. Bank expect drop in May.

Core slippages for the quarter were 740mn. FY21 Gross slippages were INR9.6bn and net slippages were INR5.27bn.

Restructuring stands at INR9.6bn (1.9% of loans). Restructuring 2.0 will have better quality customer.

Provisions - fully utilized covid buffer, covid buffer stands NIL. Bank has also made provisions of INR590mn towards stressed assets of which INR480mn was towards SR.

SMA 30+ is 1.7%.

PCR - ideal working towards 60%.

2 Likes

I could not find the March shareholding pattern. Why it is not publish on BSE?

KVB Q1 Fy23 Results- Press Release

The Bank has a delivered a strong performance in terms of business growth, which has grown 12%

YoY as well as a commendable 110% growth in Net Profit.

Reduction in NPA, improved credit off take and stable NIM has resulted in improved profitability

Business performance

-

Total business as on 30th June 2022 stands at Rs. 1,30,780 crore, registering a Y-o-Y growth of 12.05% i.e. up Rs. 14,067 crore from Rs. 1,16,713 crore as on 30.06.2021. Business has grown by Rs. 4,554 crore during Q1, from a level of Rs. 1,26,226 crore as on 31.03.2022.

-

Credit portfolio grew by ~14% Y-o-Y (Rs. 7,297 crore) and gross advances stands at Rs. 59,612 crore as on 30.06.2022, up from Rs. 52,315 crore a year ago.

-

Credit off take continues to improve both Y-o-Y as well as Q-o-Q terms aiding the growth of advances portfolio.

-

Jewel Loan portfolio registered a Y-o-Y growth of Rs. 1,667 crore (~13%) and stands at Rs. 14,873 crore as on 30.06.2022 (up from Rs. 13,206 crore a year ago).

-

Total deposits grew by Rs. 6,770 crore (~11%) to Rs. 71,168 crore, up from Rs. 64,398 crore as of 30.06.2021. CASA portfolio and retail term deposits were growth drivers.

-

CASA share is up by 118 bps to 36.42%; CASA deposits are up at Rs.25,916 crore i.e. a growth of 14.23% on Y-o-Y basis (Rs. 22,688 crore a year ago).

-

Basel III CRAR stands at 19.21% (with CET1 Ratio of 17.25%), up from 19.06% as on 30.06.2021.

-

As at 30.06.2022, Gross NPA has declined to 5.21% (Rs. 3,107 crore) as compared to 7.97%

(Rs. 4,167 crore) a year ago. GNPA as on 31.03.2022 was Rs. 3,431 crore (5.96%). -

Net NPA stands at 1.91% (Rs. 1,098 crore) as on 30.06.2022 (3.69% a yr ago - Rs. 1,845 cr).

-

Provision Coverage Ratio stands at 82.74% (72.40% a year ago).

-

Branch and ATM + Cash Recyclers network as on 30.06.2022 stands at 789 & 2,237 respectively (corresponding position was 781 & 2,251 as on 30.06.2021).

Financial Performance

Net profit for the quarter grew by 110% and stood at Rs. 229 crore from Rs. 109 crore during Q1 of previous year.

Operating profit for the quarter was Rs. 475 crore as compared to Rs. 412 crore.

Net interest income for the quarter improved by ~17% (Rs. 108 crore) to Rs. 746 crore for the current quarter vis-à-vis Rs. 638 crore for Q1 of previous year.

Net interest margin stands at 3.82% up 27 bps from 3.55% a year ago.

Cost of deposits has improved by 44 bps and stands at 4.09% as compared to 4.53% during the previous year.

Yield on advances is at 8.27% (8.55% for Q1 of previous year).

Non-interest income for the quarter is Rs. 199 crore during the current

quarter as compared to Rs. 203 crore a year ago.

Fee based income has improved by Rs. 40 crore on Y-o-Y basis to Rs. 187 crore from Rs. 147 crore during the previous year.

Operating expenses for the quarter was Rs. 469 crore as compared to Rs. 429 crore during Q1 of previous year.

Cost to income ratio stands at 49.68% (51.03% for Q1 of previous year).

Karur Vysya Bank Q3 concall highlights -

Current branch count at 780. Mostly concentrated in TN, Karnataka, AP, Telangana, Kerala, Maharashtra, Gujarat and WB

Key Data-

Advances -64,500cr,up 16 pc yoy

Deposits -76,175,up 14 pc yoy

CASA-up 7pc at 25800 cr ( needs improvement )

CASA ratio at 33 pc

NII -889 cr, up 30 pc yoy

NP -289 cr, up 56 pc yoy

RoA -1.32 vs 0.93 pc

RoE -14.04 pc

NIM -4.32 pc

GNPA -2.66, down 431 bps yoy (massive improvement)

NNPA -0.89 pc, down 166 bps yoy (massive improvement)

PCR -90.87 pc, up 1206 bps yoy (massive improvement)

PPOP -689 cr, up 72pc

Cost of Deposits-4.26 pc

Cost of Funds - 4.29 pc

Yield on advances - 9.04

Yield on funds - 7.92

NIMs- 4.32 pc

Spread - 3.63 pc

Cost/Income - 42.9 pc vs 54.47 (massive improvement)

Breakup of advances-

Commercial (< 25 cr) - 32 pc

Retail - 23 pc

Agri - 23 pc

Corporate - 22 pc

Expect to maintain NIM > 4 pc, RoA at 1.35 pc by Q4 end

Front loaded the provisions book as a matter of prudence, Tax planning and to improve PCR

Credit cost for 9M period at 1.02pc. Likely to be lower next year due front loading of provisions

Gross slippages in Q3 at 162 cr (very healthy) SMA 30+ book at less than 1 pc 86 pc of loan book linked to MCLR, EBLR CRAR at 17.86 ( 9M profits not included ), Liquidity coverage at 200 pc Rating profile of corporate loan book - 30 pc below BB. LY it was 45 pc

Current unsecured book at aprox 500 cr. Hence, bank now tied up with a few TN based micro finance institutions to enter this space. TN is a stable MF mkt. Bank intends to go slow here and build the book gradually

Likely to grow advances by 15 pc plus for Q4. For next yr, will provide guidance in Mar 23

This Qtr’s recovery from written off accounts at 85 cr

Aim to maintain cost/income ratio at 45-47 going fwd. Aim to open 25 new branches next yr ( a modest tgt )

Also hiring a dedicated sales team to mobilise liabilities so that they can keep pace with asset growth. This is a completely new initiative. The team shall also cross sell retail products

Net slippages for last 6 Qtrs have been negative

That’s how asset quality has shown massive improvement

Net slippages likely to remain negative for next 2-3 Qtrs as well !!!

Disc: invested , biased

1 Like

Karur Vysya Bank Q3 concall highlights -

Current branch count at 780. Mostly concentrated in TN, Karnataka, AP, Telangana, Kerala, Maharashtra, Gujarat and WB

Key Data-

Advances -64,500cr,up 16 pc yoy

Deposits -76,175,up 14 pc yoy

CASA-up 7pc at 25800 cr ( needs improvement )

CASA ratio at 33 pc

NII -889 cr, up 30 pc yoy

NP -289 cr, up 56 pc yoy

RoA -1.32 vs 0.93 pc

RoE -14.04 pc

NIM -4.32 pc

GNPA -2.66, down 431 bps yoy (massive improvement)

NNPA -0.89 pc, down 166 bps yoy (massive improvement)

PCR -90.87 pc, up 1206 bps yoy (massive improvement)

PPOP -689 cr, up 72pc

Cost of Deposits-4.26 pc

Cost of Funds - 4.29 pc

Yield on advances - 9.04

Yield on funds - 7.92

NIMs- 4.32 pc

Spread - 3.63 pc

Cost/Income - 42.9 pc vs 54.47 (massive improvement)

Breakup of advances-

Commercial (< 25 cr) - 32 pc

Retail - 23 pc

Agri - 23 pc

Corporate - 22 pc

Expect to maintain NIM > 4 pc, RoA at 1.35 pc by Q4 end

Front loaded the provisions book as a matter of prudence, Tax planning and to improve PCR

Credit cost for 9M period at 1.02pc. Likely to be lower next year due front loading of provisions

Gross slippages in Q3 at 162 cr (very healthy) SMA 30+ book at less than 1 pc 86 pc of loan book linked to MCLR, EBLR CRAR at 17.86 ( 9M profits not included ), Liquidity coverage at 200 pc Rating profile of corporate loan book - 30 pc below BB. LY it was 45 pc

Current unsecured book at aprox 500 cr. Hence, bank now tied up with a few TN based micro finance institutions to enter this space. TN is a stable MF mkt. Bank intends to go slow here and build the book gradually

Likely to grow advances by 15 pc plus for Q4. For next yr, will provide guidance in Mar 23

This Qtr’s recovery from written off accounts at 85 cr

Aim to maintain cost/income ratio at 45-47 going fwd. Aim to open 25 new branches next yr ( a modest tgt )

Also hiring a dedicated sales team to mobilise liabilities so that they can keep pace with asset growth. This is a completely new initiative. The team shall also cross sell retail products

Net slippages for last 6 Qtrs have been negative

That’s how asset quality has shown massive improvement

Net slippages likely to remain negative for next 2-3 Qtrs as well !!!

Disc: invested , biased

3 Likes

KARUR VYSYA BANK Q2 -

Advances up 15 pc YoY

Deposits up 13 pc YoY

Total business crosses 1.5 lakh cr for the first time ( Advances at Aprox 70k cr )

Q2 RoA @ 1.57 - highest in last 10 yrs (despite addititional contingency provisions of 25 cr) ![]()

Q2 Net Profit - 378 cr, highest ever

Gross NPAs @ 1.73 vs 1.99 pc in Q1

Net NPAs @ 0.47 vs 0.59 pc in Q1

Provision Coverage Ratio @ 94.5 pc ![]()

NIMs at 4.07 vs 4.19 pc in Q1 ( due higher increase in cost of deposits vs loans ) Guiding for 1.6 pc RoA , NIMs @ 3.8 pc for Q4 / qtr ending FY 24, Loan growth > 15 pc for FY 24

Credit cost guidance for FY 24 @ 75 bps !! ![]()

Restructured book at 1.2 pc with 25 pc provisions. Also, almost all of restructured book is secured

Q2 slippages @ only 115 cr ![]()

Expecting a recovery of aprox 250 cr from written off accounts

Thrust areas - Gold Loans, Mortgages in Tier -2,3 cities

Disc: holding, biased, not SEBI registered

3 Likes

Karur Vysya Bank -

Q3 concall highlights -

Advances up 17 pc @ 72.6k cr

Deposits up 13 pc @ 85.6k cr

CASA up 5 pc @ 27k cr

NIMs @ 4.2 pc, up 9 bps YoY

GNPAs - 1.58 pc ( down 112 bps !!! )

NNPAs - 0.42 pc ( down 48 bps !!! )

PCR - 95 pc, up 394 bps !!!

RoA @ 1.65 vs 1.32 pc

RoE @ 17.2 vs 14.1 pc

NII - 1001 vs 890 cr, up 13 pc

Other income - 358 vs 317 cr, up 13 pc

Op Profit - 676 vs 690 cr ( down 2 pc )

Provisions - 149 vs 364 cr ( down sharply )

Net Profit @ 412 vs 290 cr ( up 42 pc !!! )

Segment wise growth in advances -

Retail up 21 pc @ 17k cr

Commercial up 20 pc @ 24k cr

Agri up 19 pc @ 17k cr

Corporate up 6 pc @ 14k cr ( deliberate strategy by the bank to keep low margin business’s growth at moderate levels )

Fresh slippages @ 197 cr ( well within limits )

Bank is holding total provisions of 822 cr against Net NPAs of 305 cr !!!

Total bank branches @ 831 vs 790 LY. To open 8 new branches in Q4

Expecting to maintain NIMs of > 4 pc in Q4 as well

Confident of keeping the slippage ratios under 1 pc

Std restructured book @ 1.09 pc of advances. Holding 28 pc provisions against the std restructured book

Bank has a BNPL arrangement with Amazon. The book is growing well and credit costs are low

Demand from MSMEs continues to be very strong. Seeing good demand in Q4 as well. MSME book is now 33 pc of bank’s total book

Bank is going slow wrt loan disbursements to large corporates as the yields there r low and the bank believes that they can get better yields elsewhere

If the textile industry picks up, it should be positive for the bank as TN has a vibrant textile industry. Signing of UK, Switzerland FTA should also be a positive

Banking is going to increase its focus on retail home loans and builder loans over the next 2-3 yrs. This has been identified as a core growth area for the future

Going to expand slowly into the MFI segment as well (by tying up with various partners)

Disc : holding, not SEBI registered, biased

4 Likes

What is MFI, is it Mutual Funds or else?

Micro Finance institution. They r planning to get into this space as the margins here are relatively higher

1 Like

They are trying to tie with other Banks or how will they do Micro finance business?

They r partnering with small / local Micro Fin Institutions to get a hang of the business. As they gain experience, they can then scale it up with their selected partners

Karur Vysya Bank -

Q2 FY 25 results and concall highlights -

Advances / Loans @ 80.2k cr, up 14 pc YoY

Deposits @ 95.8k cr, up 15 pc YoY

CASA deposits @ 28.3k cr, up 5 pc YoY

NII - 1060 vs 915 cr, up 16 pc

Other income - 472 vs 339 cr, up 39 pc

Operating expenses - 716 vs 616 cr, up 16 pc

Operating profits - 816 vs 638 cr, up 28 pc

Provisions - 180 vs 127 cr, up 42 pc

PBT - 636 vs 511 cr, up 24 pc

PAT - 473 vs 378 cr, up 25 pc

RoA @ 1.72 vs 1.57 pc

RoE @ 17.3 vs 16.5 pc

NIMs @ 4.11 vs 4.07 pc

Spreads @ 3.33 vs 3.32 pc

Cost/Income @ 46.72 vs 49.14 pc

Gross NPAs @ 1.10 pc, down 63 bps

Net NPAs @ 0.28 pc, down 19 bps

PCR @ 96 pc

Breakup of loan book -

Retail - 19.6k cr, up 21 pc YoY

Agri ( more than 90 pc are against gold ) - 18.8k cr, up 16 pc YoY

Corporate ( loans > 25 cr ) - 13.1k cr, down 9 pc YoY

Commercial ( loans < 25 cr ) - 28.7k cr, up 22 pc YoY

Avg ticket size of commercial loans is around 50 lakh. 38 pc of commercial loans are > 5 cr

Avg ticket size of corporate loans around 36 cr. 86 pc of corporate loans are < 150 cr

Slippages for Q2 @ 181 cr vs 155 cr YoY ( well within control )

Recoveries for Q2 @ 100 cr vs 115 cr YoY

Total number of branches @ 841 on 30 Sep 24 vs 799 on 30 Sep 23

Retail loan book growth was primarily driven by mortgages

Deposits growth remains a key priority for the bank. Expecting a 10 bps rise in rate of deposits in Q3

Bank is able to sustain NIMs > 4 pc due better growth in retail, agri segments vs low margin corporate segment

Expecting NIMs in Q3 to be around 4 pc mark ( vs 4.11 pc in Q2 due expectation of moderate increase in rate of deposits and no increase in yield on advances )

Confident of sustaining RoAs @ > 1.65 pc levels for rest of FY

Confident of maintaining the gross slippage ratio below 1 pc for full FY ( in Q2, it was 0.23 pc - not annualised )

Total unsecured book stands @ 2.4 pc ( being very cautious in growing the MFI book )

Bank is de-focussing on the corporate segment because of lower yeilds vs the funds they r raising via term deposits. Once CASA growth comes back, they ll re-focus on their corporate loan book

26 pc of bank’s book consists of Gold Loans ( under Agri + Retail segments )

Textile sector ( in the MSME segment ) in TN area is doing well vs last year

Yeild on Loan against property is around 9.5 pc. Company’s LAP portfolio is majorly concentrated in South India ( TN + Karnataka + AP + Telangana )

Spending aggressively on IT + Cyber Security + New branches. Aim to open 100 branches in current FY

Aim to keep growing the Retail + Agri + MSME book at rates > 18 pc. Achieving this is absolutely critical for the bank as the corporate book is expected to continue to de-grow for some time

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

1 Like