KPL started its journey as a manufacturer of flat raffia tapes and HDPE

woven sacks. KPL marked its turnaround in 1999 when it began

manufacturing FIBCs and bulk bags. KPL has an annual capacity to manufacture 14600 tonne and 3350

tonne of FIBC and MFY, respectively. With FIBC sales volumes at

13627 tonne in FY16 (90%+ utilisation levels), KPL is witnessing

capacity constraints with largely flat sales in FY15-17E. Sensing the same, the management is now

gearing itself for a massive expansion amounting to | 85 crore, which involves restructuring of current

operations and incremental capacity addition of ~8500 tonne. It is expected to be financed with a mix of

debt (~60%) & equity (~40%). This is expected to be commissioned in H2FY19, thereby ushering in a

volume led growth from FY19E onwards. At peak utilisation levels, it will

generate sales of ~| 120 crore, with intended RoCE of ~16-18% . This expansion will take around 15 -18 months.

key risk:

1.if we remove the interest factor then Ebitda is 14-16%.

2.the ROE ratio is good.

3.dividend paying stock. 4.co is able to convert its net profit into cash.

Disclosure: small tracking quantity purchased

KPL is into industrial bulk packaging business and manufactures jumbo bags for cement, food grains, chemicals, fertilizers, pharmaceuticals etc. and the company exports those to Netherlands, UK, Germany, US etc.

Since more than 80 percent of their revenues come from exports, a stronger rupee particularly against Euro and Dollar is likely to have an adverse impact on there top line at least in the near future.

from the anuual report 15-16

1.The Company was among the first

FIBC companies in India to manufacture

stiff loops out of polypropylene (PP) that

strengthened product durability and

transportability;

2. Our

14,000 MTPA capacity makes us one of the

five largest global FIBC players with a 2%

market share, offering an attractive growth

opportunity.

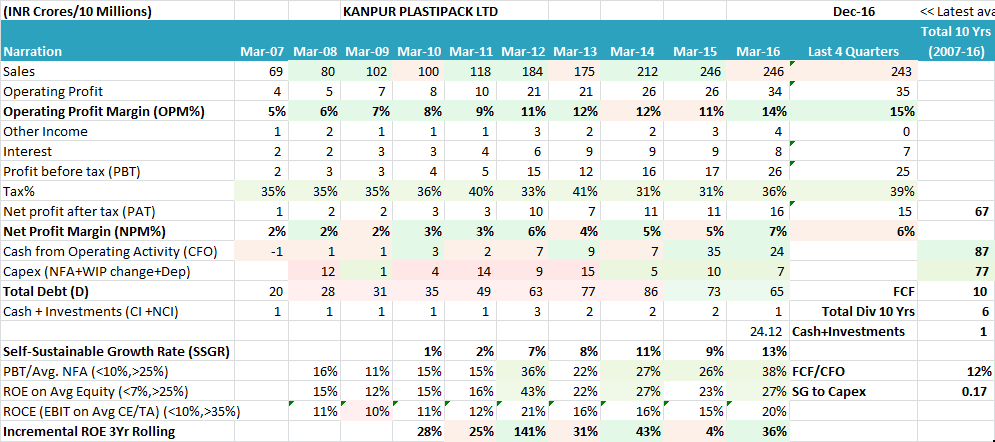

Expansion of Operating Margins from 11.33% in 2012 to a TTM of 14.60% is also exciting. Over the last 10 years they have kept the Raw Material cost b/w 56% to 65% of Sales so its not run away. Its backward integrated into MFY has helped in controlling the RM risk to some extent. Also the proposed expansion will bring in operating leverage benefits.

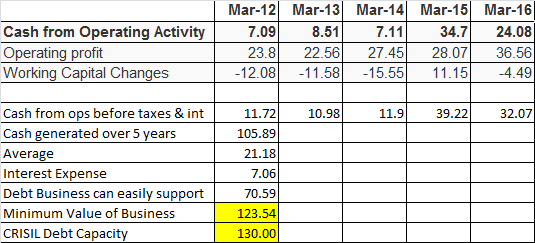

Another way to look at this is the debt capacity. Its got a Operating Profit of ~35cr. Assuming a comfortable Interest Coverage ratio of 4 would bring the amount of interest that it can comfortably service to 8.75cr. Assuming people will lend to it at 10% would mean it can take on debt of about ~88cr, its market cap is about 175cr. So its available at 2x debt capacity from this view.

When you look at the CRISIL ratings its rated BBB+ /A2 for a total debt capacity of 130cr. So its available at 1.34x from this angle.

Professor Bakshi in his lecture notes gives an example of how to value a business based on debt capacity ( reproducing the relevant portions below ). He valued Container Corporation of India using this methodology.

One small question

70.59*1.75 y h have multiplied by 1.75 only …means y not any other number.

And what method do you follow to arrive at intrinsic value

According to Ben Graham a company has to be logically worth more than the debt it can comfortably service ( beautifully explained by Prof Bakshi in his various blog posts ). If someone is willing to lend me 100 cr after looking at my earning capacity then the value of my company has to be much more than 100cr. Ben Graham thought that multiple was 1.75 i.e if the someone lends me 100cr after looking at my earnings capacity then the value of my company has to be at least 175cr if not more. This rule is to be applied only when the current debt is less than your debt capacity ( and preferably zero debt) The current debt as per 2016AR is ~66cr. The debt capacity as assessed by crisil is 130cr. So its feasible to apply this thinking.

So in effect if CRISIL feels that the debt capacity is 130cr then the value of the company should logically be at least ~227cr. (the market cap is currently ~175cr)

To be on the safer side, I have taken the lesser of the amount that i have derived ( 70.59 ) and the one derived by CRISIL (130 cr.). But i am inclined to go with CRISIL as they are a better judge.

In any case, i think this is an opportunity with the odds heavily stacked in your favour valuation wise. Any positive improvement in the business numbers would add to the flavour

Thanks for d wonderful reply.

So value arrived by debt capacity methodology is the minimum value of bussiness . How to calculate intrinsic valur of the Bussiness?

The amount mentioned in the CRISIL rationale does not indicate the debt capacity of the company but the current and proposed bank facilities (fund and non fund based) of the company which is also mentioned in the report below Rating agencies do not assess the debt capacity of the company but just rate credit profile of the companies.

The jury is out on that! It depends heavily on what you think the growth prospects are. However if the company is able to grow by taking on intelligent debt decisions it is a potential investment candidate.

For kanpur plastipack the key question to ask is what level of debt it can take on without jeopardizing its business. If crisil ratings are to be believed that level is 130cr. After all its been rated for 130 cr ( a level that has been communicated to it by its mgt).

It has stated a capex of 85 cr to expand its facilities which are maxed out on capacity. So i am just trying to get a sense of whether thats feasible. If it can pull off a capacity expansion without any balance sheet risk it may well lead to a better valuation for it than what is currently being assigned.

A company called Shree Tirupati Balalji FIBC LTd is coming with an IPO. It has capacity of 6000mt and expanding to 7500Mt. Much lower than what Kanpur Plastipack has( capacity of 14400MT going to 23000MT). Also this company may need some more serious look because most of the other competitors are struggling with high debt and lower OPM. Debt equity is 1:1.

Gross block has also increased from 73cr to 103 cr during FY13-FY17 period as company is working on setting up new plant which will be operational in H2FY18.

Trying to get in touch with Management. will share more details

Disc : Invested with tracking position. still working to get more detail.

Hi @bheeshma,

Just gone through the presentation…thanks for same…one query as from where 2000 Cr comes into calculating minimum interistic value of the company. Pl guide.

The management has forecasted a topline of 450cr by 2020 with similar margins from the current 280cr in the AR. With capacity utilization picking up in expansion projects over the next one year, we should see a bump in earnings if the execution goes per plan.